Navigating the Dallas Roads: Your Ultimate Guide to Securing the Best Car Loan in Dallas

Navigating the Dallas Roads: Your Ultimate Guide to Securing the Best Car Loan in Dallas Carloan.Guidemechanic.com

Dallas, a vibrant metropolis pulsating with energy, is a city where life moves fast, and often, that movement requires a reliable set of wheels. Whether you’re commuting across the sprawling urban landscape, exploring the lively arts district, or heading out for a weekend escape, a car is more than just transportation—it’s a gateway to convenience and freedom. For many, acquiring that perfect vehicle hinges on securing the right car loan.

But in a market as dynamic as Dallas, navigating the world of auto financing can feel like a complex journey in itself. From understanding interest rates to choosing between various lenders, there’s a lot to consider. This comprehensive guide is designed to be your trusted co-pilot, providing in-depth insights and practical advice to help you secure the best car loan in Dallas, ensuring you drive away with confidence and a deal that truly suits your financial situation.

Navigating the Dallas Roads: Your Ultimate Guide to Securing the Best Car Loan in Dallas

Why Dallas? Understanding the Local Car Loan Landscape

Dallas isn’t just a dot on the map; it’s a major economic hub with a unique automotive market. The city’s robust economy and diverse population contribute to a competitive lending environment, which can be a significant advantage for car buyers. However, it also means a plethora of options, making an informed decision even more crucial.

The sheer number of dealerships, banks, and credit unions in the Dallas-Fort Worth Metroplex creates a vibrant marketplace. This competition often translates into more flexible terms and better rates for consumers who know how to shop around effectively. Understanding this local dynamic is your first step towards a successful car loan experience.

Unpacking the Types of Car Loans Available in Dallas

Before diving into applications, it’s essential to understand the different types of car loans available. Each comes with its own set of characteristics, catering to varying needs and financial profiles. Knowing these distinctions will empower you to choose the path best suited for you.

New Car Loans: Driving Off the Lot with Confidence

New car loans are specifically designed for brand-new vehicles. These loans typically come with lower interest rates compared to used car loans, primarily because new cars are considered less of a risk for lenders due to their predictable value depreciation and warranty coverage. When you’re eyeing that latest model with zero miles, this is the loan category you’ll be exploring.

The terms for new car loans can range from 36 to 72 months, and sometimes even longer, depending on the lender and your creditworthiness. A longer term means lower monthly payments but potentially more interest paid over the life of the loan. It’s crucial to balance affordability with the total cost.

Used Car Loans: Smart Financing for Pre-Owned Vehicles

Used car loans are for vehicles that have had previous owners. Given the rapid depreciation of new cars, opting for a used vehicle can be a smart financial move, and Dallas has a massive market for pre-owned vehicles. While interest rates for used car loans might be slightly higher than for new ones, the overall cost of the vehicle itself is significantly lower, often resulting in more manageable payments.

Lenders assess used cars differently, often considering the age, mileage, and condition of the vehicle. Based on my experience, reputable lenders in Dallas will often have specific requirements for used car financing, such as a maximum age or mileage limit for the vehicle. It’s always wise to get a pre-purchase inspection for a used car, which can also influence the lender’s decision.

Refinance Car Loans: Optimizing Your Existing Loan

Perhaps you already have a car loan but your financial situation has improved, or interest rates have dropped since you first financed your vehicle. This is where a refinance car loan comes into play. Refinancing involves taking out a new loan to pay off your existing car loan, ideally at a lower interest rate or with more favorable terms.

Many Dallas residents find refinancing to be an excellent strategy to reduce their monthly payments, save on total interest, or even shorten their loan term. It’s a proactive step that can significantly improve your financial health post-purchase. We’ll delve deeper into refinancing later in this guide.

Lease vs. Buy: A Quick Consideration

While not strictly a "loan," the decision to lease or buy often comes up when discussing car financing. Leasing involves paying to use a car for a set period, typically 2-4 years, without owning it. Buying, on the other hand, means you finance the purchase and eventually own the vehicle.

For those who enjoy driving new cars every few years and don’t want the hassle of selling, leasing can be attractive. However, if you prefer long-term ownership, unlimited mileage, and the ability to customize your vehicle, a car loan for purchase is the way to go. Your choice here significantly impacts your long-term financial commitment.

The Car Loan Application Process in Dallas: A Step-by-Step Guide

Securing a car loan doesn’t have to be daunting. By breaking down the process into manageable steps, you can approach it strategically and increase your chances of getting approved with favorable terms.

Step 1: Assess Your Credit Score and History

Your credit score is arguably the most critical factor in determining your car loan eligibility and interest rate. Lenders use it to gauge your financial reliability. A higher credit score signals lower risk, often leading to better interest rates and more flexible terms.

- Understanding Your Score: Your FICO score, ranging from 300 to 850, is what most lenders consider. Generally, scores above 700 are considered good, while those above 780 are excellent.

- Accessing Your Report: You’re entitled to a free credit report from each of the three major bureaus (Equifax, Experian, TransUnion) annually via AnnualCreditReport.com. Review it for any errors and understand your current standing.

- Improving Your Score: If your score needs a boost, focus on paying bills on time, reducing existing debt, and avoiding new credit inquiries just before applying for a car loan.

Based on my experience, many people skip this crucial first step. Knowing your credit score upfront allows you to set realistic expectations and negotiate more effectively.

Step 2: Establish a Realistic Budget and Consider a Down Payment

Before you even look at cars, determine how much you can truly afford. This isn’t just about the monthly payment, but the total cost of ownership, including insurance, fuel, maintenance, and registration fees. A common mistake is to only focus on the monthly payment without considering these additional expenses.

- The 20/4/10 Rule: A popular guideline suggests a 20% down payment, a loan term no longer than four years, and total car expenses (payment, insurance, fuel) not exceeding 10% of your gross monthly income. While a guideline, it’s a good starting point for budgeting.

- The Power of a Down Payment: A larger down payment reduces the amount you need to borrow, which directly translates to lower monthly payments and less interest paid over the loan term. It also shows lenders you are serious and reduces their risk. Even 10-20% can make a significant difference in your loan terms.

Pro tips from us: Factor in Dallas-specific costs like higher insurance rates in some areas or potential parking fees if you work downtown.

Step 3: Gather Necessary Documents

Lenders require specific documentation to verify your identity, income, and financial stability. Having these ready beforehand can significantly expedite the application process.

Typical documents include:

- Proof of identity (driver’s license, passport).

- Proof of residence (utility bill, lease agreement).

- Proof of income (pay stubs, W-2s, tax returns for self-employed individuals).

- Bank statements.

- Trade-in title (if applicable).

Being prepared shows professionalism and can make the process much smoother.

Step 4: Shop for Lenders – Don’t Just Rely on the Dealership

This is where many car buyers miss an opportunity to save significantly. While dealership financing can be convenient, it’s not always the best option. Shopping around for a loan before you step onto the lot gives you leverage.

- Banks: Traditional banks like Chase, Bank of America, or Wells Fargo offer competitive rates, especially for those with excellent credit. They often have branches throughout Dallas, making in-person consultations easy.

- Credit Unions: Credit unions, such as Dallas Credit Union or Texas Trust Credit Union, are member-owned and often provide some of the lowest interest rates due to their non-profit structure. They are an excellent option to explore.

- Online Lenders: Companies like Capital One Auto Finance, LightStream, or Carvana offer streamlined online application processes and can provide quick pre-approvals. They offer convenience and competitive rates.

- Dealership Financing: Dealerships work with a network of lenders and can offer various financing options, sometimes including special manufacturer incentives. However, their primary goal is to sell you a car, so always compare their offers to your pre-approved rates.

Common mistakes to avoid are: accepting the first offer you receive without comparing. Always get at least three different loan offers.

Step 5: Get Pre-Approved for a Loan

Pre-approval is a game-changer. It means a lender has reviewed your financial information and tentatively agreed to lend you a specific amount at a certain interest rate. This is usually a "soft inquiry" on your credit, which doesn’t harm your score.

- Advantages of Pre-Approval:

- Know Your Budget: You walk into the dealership knowing exactly how much you can spend, allowing you to focus on the car, not the financing.

- Negotiating Power: You become a cash buyer in the eyes of the dealership, giving you significant leverage to negotiate the car’s price.

- Faster Process: It streamlines the car-buying experience, as much of the financial paperwork is already handled.

Pro tips from us: Aim to get pre-approved from multiple lenders within a 14-day window. This period is typically treated as a single credit inquiry, minimizing the impact on your score.

Step 6: Understand the Loan Offer and Read the Fine Print

Once you have loan offers, it’s time to scrutinize them. Don’t just look at the monthly payment.

- Interest Rate (APR): The Annual Percentage Rate (APR) is the true cost of borrowing, encompassing the interest rate plus certain fees. Always compare APRs, not just advertised interest rates.

- Loan Term: The length of the loan (e.g., 60 months, 72 months). Longer terms mean lower monthly payments but more interest paid overall.

- Fees: Look out for origination fees, document fees, or prepayment penalties. Some loans charge a fee if you pay off the loan early.

- Total Cost: Calculate the total amount you will pay over the life of the loan (monthly payment x loan term + down payment). This is the real cost of the car.

Based on my experience, many consumers overlook the total cost, focusing solely on the monthly payment. Always ask for the amortization schedule to see how interest accrues over time.

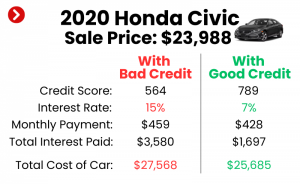

Navigating Car Loans with Less-Than-Perfect Credit in Dallas

Having a low credit score doesn’t mean you can’t get a car loan in Dallas; it just means the process might require a different approach. Subprime lenders and specific strategies can still help you secure financing.

Challenges and Opportunities

Lenders view applicants with lower credit scores as higher risk, which typically translates to higher interest rates. However, the competitive Dallas market often provides options for various credit tiers. There are specialized lenders who cater to individuals with bad credit, often called subprime lenders.

Strategies for Bad Credit Car Loans in Dallas:

- Larger Down Payment: As mentioned, a significant down payment reduces the lender’s risk and can help offset a lower credit score.

- Co-signer: A co-signer with good credit can significantly improve your chances of approval and help you secure a better interest rate. Remember, they are equally responsible for the loan.

- Demonstrate Stability: Show proof of stable income and employment. Lenders want to see that you have the capacity to repay the loan consistently.

- Improve Your Credit: If possible, take a few months to make timely payments on existing debts, reduce credit card balances, and resolve any outstanding collections. Even a small improvement can make a difference.

- Seek Out Specialized Lenders: Some credit unions and online lenders in Dallas specialize in helping individuals with challenging credit histories. They might offer programs designed for credit rebuilding.

Common mistakes to avoid are: accepting an extremely high-interest rate without exploring all options, or falling for "buy here, pay here" dealerships without understanding their typically higher costs and limited credit reporting. While these can be options, they should be carefully vetted.

Key Factors Affecting Your Car Loan in Dallas

Beyond your credit score, several other elements play a pivotal role in the terms of your car loan. Understanding these can help you position yourself for the best possible outcome.

1. Credit Score

We’ve covered this extensively, but it bears repeating: your credit score is the foundation of your loan application. A strong score means access to prime rates; a weaker score means higher rates and potentially fewer options.

2. Debt-to-Income (DTI) Ratio

This ratio compares your total monthly debt payments to your gross monthly income. Lenders want to see a manageable DTI, typically below 40%, to ensure you have enough disposable income to comfortably make your car payments.

3. Loan Term

The length of your loan directly impacts your monthly payment and the total interest paid. Shorter terms (e.g., 36 or 48 months) mean higher monthly payments but less interest. Longer terms (e.g., 72 or 84 months) offer lower monthly payments but accumulate more interest over time.

4. Interest Rate (APR)

The interest rate is the cost of borrowing money, expressed as a percentage. A lower APR means a cheaper loan. Your credit score, the loan term, and the lender’s current market rates all influence this.

5. Vehicle Type (New vs. Used)

As discussed, new cars generally command lower interest rates due to their lower risk profile for lenders. Used cars, while often more affordable upfront, can come with slightly higher rates because of their age, mileage, and potential for unforeseen issues.

6. Down Payment Amount

A larger down payment reduces the amount you need to finance, thereby decreasing your monthly payments and the total interest you’ll pay. It also signals financial stability to lenders.

Pro Tips for Securing the Best Car Loan in Dallas

Armed with knowledge, you’re ready to tackle the Dallas auto loan market like a seasoned pro. Here are some invaluable tips to ensure you drive away with the best deal.

- Negotiate Everything: Don’t just negotiate the car’s price. Be prepared to negotiate the interest rate, loan term, and any fees associated with the loan. Everything is potentially negotiable.

- Read the Fine Print Thoroughly: Before signing any documents, carefully review every line of the loan agreement. Understand all terms, conditions, and potential penalties. If something is unclear, ask for clarification.

- Don’t Rush the Process: Car buying and loan securing can be emotional, but resist the urge to rush. Take your time, compare offers, and make an informed decision. Impulsive decisions often lead to regret.

- Get Multiple Pre-Approvals: As mentioned, apply for pre-approval with several different lenders (banks, credit unions, online lenders) within a short window. This allows you to compare actual offers and choose the most favorable one.

- Consider a Shorter Loan Term (If Affordable): While longer terms offer lower monthly payments, a shorter term saves you significant money in interest over the life of the loan. If your budget allows, opt for the shortest term you can comfortably manage.

- Build a Relationship with Local Lenders: Establishing a banking relationship with a local Dallas credit union or bank can sometimes lead to preferential rates or more personalized service when you need a loan. They might be more willing to work with their existing customers.

Pro tips from us: Be wary of add-ons that significantly increase your loan amount, such as extended warranties or GAP insurance, unless you fully understand their value and genuinely need them. Often, these can be purchased separately for less.

Common Mistakes to Avoid When Getting a Car Loan in Dallas

Even with the best intentions, it’s easy to fall into common traps. Being aware of these pitfalls can save you money and stress.

- Not Checking Your Credit Report: Relying solely on a dealer’s credit check or not knowing your score beforehand puts you at a disadvantage. Always know where you stand.

- Focusing Only on Monthly Payments: This is a classic mistake. A low monthly payment might sound appealing, but it often comes with a longer loan term and significantly more interest paid over time. Always consider the total cost of the loan.

- Skipping Pre-approval: Walking into a dealership without a pre-approved loan is like going to a battle without armor. You lose valuable negotiating power and might end up with a less favorable rate.

- Ignoring the Total Cost of the Loan: Don’t just look at the vehicle’s price tag. Calculate the total amount you’ll pay, including interest, fees, and the principal, over the loan’s lifetime.

- Falling for High-Pressure Sales Tactics: Some dealerships use aggressive tactics to push you into a deal. Stand firm, don’t be afraid to walk away, and remember you are in control of your decision.

- Not Budgeting for Additional Car Costs: Beyond the loan, remember to budget for auto insurance (which can be substantial in Dallas), vehicle registration, maintenance, and fuel. These can add hundreds of dollars to your monthly expenses.

For more detailed budgeting strategies, you might find our article on (internal link placeholder) helpful.

Refinancing Your Car Loan in Dallas: Is It Right for You?

As mentioned earlier, refinancing can be a powerful tool for optimizing your existing car loan. It’s not just for those with bad initial deals; it can benefit anyone whose financial situation has improved or if market rates have dropped.

When to Consider Refinancing:

- Lower Interest Rates: If current market interest rates are significantly lower than your original loan’s rate.

- Improved Credit Score: If your credit score has improved since you first took out the loan, you likely qualify for a better rate.

- Reduced Monthly Payments: If you need to lower your monthly expenses, extending the loan term (though not always advisable for total cost) or getting a lower rate can help.

- Shorter Loan Term: Conversely, if you want to pay off your loan faster and can afford higher payments, refinancing to a shorter term with a better rate can save you money.

- Removing a Co-signer: If your credit has improved, you might be able to refinance the loan in your name only, releasing your co-signer from their obligation.

The Refinancing Process:

The process mirrors that of securing an initial car loan:

- Check Your Credit: Ensure your score has improved.

- Shop for Lenders: Compare offers from banks, credit unions, and online lenders in Dallas.

- Gather Documents: Have your current loan information, income proof, and identity documents ready.

- Submit Application: Apply for the new loan.

- Review and Sign: Understand the new terms before finalizing the deal.

For a deeper dive into credit improvement strategies, check out this guide from the Consumer Financial Protection Bureau on Understanding Your Credit. (External link placeholder).

Beyond the Loan: What Else to Consider in Dallas

Securing the loan is a significant milestone, but your car-buying journey in Dallas isn’t quite over. There are practicalities to handle once you’ve made your purchase.

- Auto Insurance Requirements: Texas law mandates minimum liability insurance. However, lenders will require full coverage (comprehensive and collision) until your loan is paid off. Dallas insurance rates can vary, so get quotes before finalizing your car purchase.

- Vehicle Registration and Taxes: You’ll need to register your vehicle with the Texas Department of Motor Vehicles (TxDMV) and pay sales tax (6.25% of the sales price or standard presumptive value, whichever is greater). Dealerships often handle this, but it’s good to be aware of the costs.

- Maintenance and Running Costs: Remember to factor in ongoing costs like routine maintenance, oil changes, tire rotations, and fuel, especially with Dallas’s traffic and distances.

For insights into long-term car ownership costs, you might find our article on (internal link placeholder) helpful.

Drive Confidently: Your Dallas Car Loan Journey Awaits

Securing a car loan in Dallas is a significant financial decision, but it doesn’t have to be overwhelming. By understanding the types of loans available, meticulously preparing your finances, diligently shopping for lenders, and avoiding common pitfalls, you can confidently navigate the process.

Remember, knowledge is power. Arm yourself with information, compare your options, and don’t hesitate to ask questions. With this comprehensive guide, you are well-equipped to find the best car loan in Dallas, ensuring you hit the road with peace of mind and the perfect vehicle for your Dallas adventures. Happy driving!