Navigating the Digital Highway: Your Comprehensive Guide to Applying for a Car Loan Online

Navigating the Digital Highway: Your Comprehensive Guide to Applying for a Car Loan Online Carloan.Guidemechanic.com

In today’s fast-paced world, nearly every aspect of our lives has transitioned online, from grocery shopping to banking. Car financing is no exception. The traditional dealership office, filled with paperwork and lengthy waiting times, is rapidly being replaced by the convenience and speed of digital platforms. But the big question remains: Can you apply for a car loan online, and if so, how can you ensure a smooth, successful, and stress-free process?

The answer is a resounding yes! Applying for a car loan online is not only possible but has become a preferred method for millions seeking auto financing. This in-depth guide will demystify the entire process, providing you with the knowledge and confidence to secure the best possible loan from the comfort of your home. We’ll explore the benefits, walk you through each crucial step, highlight common pitfalls to avoid, and share expert tips to maximize your chances of approval and secure favorable terms.

Navigating the Digital Highway: Your Comprehensive Guide to Applying for a Car Loan Online

The Digital Revolution in Car Financing: Why Online?

The shift towards online car loan applications isn’t just a trend; it’s a fundamental change driven by consumer demand for efficiency, transparency, and choice. Digital financing platforms offer a myriad of advantages that traditional methods simply can’t match. Understanding these benefits is the first step towards embracing the future of auto lending.

Convenience and Accessibility

Imagine securing financing for your next vehicle without ever leaving your couch. That’s the power of online applications. You can initiate the process at any time of day or night, fitting it seamlessly into your schedule, whether it’s during a lunch break or late in the evening. This eliminates the need to travel to multiple banks or dealerships, saving you precious time and effort.

Furthermore, geographical barriers disappear. You’re no longer limited to lenders in your immediate vicinity. Online platforms connect you with a national network of financial institutions, significantly broadening your options and increasing your chances of finding a competitive rate. This unparalleled accessibility puts you, the borrower, firmly in control.

Speed and Efficiency

Time is often of the essence when purchasing a car, especially if you need a vehicle quickly. Online applications are designed for speed. Many lenders offer instant pre-approvals or rapid responses, sometimes within minutes. This quick turnaround allows you to proceed with car shopping with a clear understanding of your budget and borrowing power.

The digital nature also streamlines the documentation process. Instead of physical copies, you’ll typically upload required documents directly to a secure portal. This reduces paperwork, minimizes errors, and accelerates the entire loan processing time, getting you closer to driving away in your new car much faster.

Wider Range of Options

When you apply for a car loan online, you gain access to a vastly larger marketplace of lenders. This includes traditional banks, credit unions, and a growing number of online-only lenders specializing in auto financing. Each lender might have different criteria, interest rates, and loan products.

This extensive choice means you’re more likely to find a loan that perfectly matches your financial situation and needs. You can compare offers side-by-side, scrutinize terms, and select the option that provides the best value, rather than settling for the first offer presented to you at a dealership. This competitive environment often translates into better rates and more flexible terms for borrowers.

Transparency and Comparison

One of the most significant benefits of online car loan applications is the enhanced transparency. Online platforms often provide clear breakdowns of interest rates, fees, and repayment schedules upfront. This allows for easy comparison between different loan offers, empowering you to make an informed decision without feeling rushed or pressured.

Many websites offer tools like loan calculators, which allow you to experiment with different down payments, loan terms, and interest rates to understand their impact on your monthly payments. This level of insight ensures you fully comprehend the financial commitment before signing on the dotted line, fostering trust and clarity in the lending process.

The Step-by-Step Guide to Applying for a Car Loan Online

Navigating the online car loan application process can seem daunting at first, but by breaking it down into manageable steps, you’ll find it quite straightforward. Based on my experience, a methodical approach significantly increases your chances of securing a favorable loan.

Step 1: Assess Your Financial Health (Pre-Application)

Before you even think about filling out an online form, take a moment to honestly evaluate your financial standing. This foundational step is crucial for understanding what kind of loan you can realistically afford and what lenders will expect.

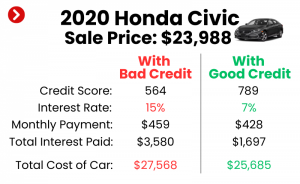

Credit Score Check: Your credit score is arguably the most critical factor lenders consider. It tells them how reliable you are at repaying debts. A higher score typically qualifies you for lower interest rates. You can obtain a free copy of your credit report from AnnualCreditReport.com and check your scores through services like Credit Karma or your bank. Review it carefully for any errors that might be negatively impacting your score.

Budgeting and Affordability: Determine how much you can comfortably afford to pay each month, not just for the car loan, but also for insurance, fuel, maintenance, and registration. Pro tips from us: your car payment should generally not exceed 10-15% of your take-home pay. Don’t forget to factor in a potential down payment, as a larger down payment can reduce your loan amount and often lead to better terms.

Gathering Documents: Lenders will require documentation to verify your identity, income, and residency. Having these ready beforehand will expedite your application. Typically, you’ll need proof of income (pay stubs, tax returns), proof of identity (driver’s license, passport), and proof of residency (utility bill, lease agreement). Keep digital copies handy for easy uploading.

Step 2: Researching Online Lenders

With your financial picture clear, it’s time to find the right lender. The online landscape offers a diverse array of options, each with its own advantages.

Types of Lenders: Explore different categories. Traditional banks (e.g., Chase, Bank of America) offer competitive rates to well-qualified borrowers. Credit unions often provide excellent rates and personalized service, especially to their members. Online-only lenders (e.g., Capital One Auto Finance, LightStream) specialize in digital applications and can sometimes offer very fast approvals. Don’t forget dealership financing platforms, which aggregate offers from various lenders.

Reading Reviews and Reputations: Before committing, always read reviews from other customers. Websites like Trustpilot, Google Reviews, and the Better Business Bureau can provide valuable insights into a lender’s customer service, transparency, and overall reliability. Look for consistent patterns in positive or negative feedback.

Step 3: Understanding Loan Types & Terms

Not all car loans are created equal. Familiarizing yourself with the different types and their associated terms will help you make an informed decision.

New vs. Used Car Loans: Lenders often differentiate between loans for new and used vehicles. New car loans typically come with lower interest rates and longer terms due to the predictable depreciation of new cars. Used car loans might have slightly higher rates due to perceived higher risk, but this varies greatly based on the vehicle’s age and mileage.

Interest Rates, APR, Loan Term, Fees: The interest rate is the cost of borrowing money, expressed as a percentage. The Annual Percentage Rate (APR) is a more comprehensive measure, including the interest rate plus certain fees. Always compare APRs, not just interest rates. The loan term (e.g., 36, 48, 60 months) affects your monthly payment and the total interest paid. Be wary of excessive fees, such as origination fees or prepayment penalties.

Step 4: The Online Application Process Itself

This is where you’ll input your personal and financial information into the lender’s secure portal. Accuracy and honesty are paramount.

Filling Out Forms: Carefully complete all required fields. This includes your personal details, employment history, income information, and details about the car you intend to purchase (if known). Double-check all entries for typos or errors, as these can delay processing or lead to rejection.

Soft vs. Hard Credit Inquiries: Many online lenders offer a "pre-qualification" option, which involves a soft credit inquiry. This allows you to see potential rates without impacting your credit score. Once you formally apply, a hard credit inquiry will be made, which can temporarily lower your score by a few points. Pro tips from us: try to get pre-qualified with multiple lenders using soft inquiries before selecting one for a full application.

Submitting Documents Electronically: As mentioned, you’ll typically upload scanned copies or photos of your required documents. Ensure they are clear, legible, and contain all necessary information. Most platforms have secure encryption to protect your sensitive data.

Step 5: Reviewing Offers and Making a Decision

Once you’ve submitted your application, you’ll hopefully receive one or more loan offers. This is a critical stage for comparison and negotiation.

Comparing Multiple Offers: Do not jump at the first offer. Compare the APR, monthly payment, total interest paid over the loan term, and any associated fees from each offer. A slightly higher interest rate on a shorter term might result in less overall interest paid. Use online calculators to model different scenarios.

Understanding the Fine Print: Common mistakes to avoid are neglecting to read the entire loan agreement. Pay close attention to clauses regarding late payment penalties, prepayment penalties, and any additional charges. If anything is unclear, don’t hesitate to contact the lender for clarification before signing. Your understanding is key to a positive borrowing experience.

Negotiation (if applicable): While online platforms are generally less flexible for direct negotiation on rates, having multiple pre-approved offers can give you leverage. You might use a lower offer from one lender to ask another for a better deal. This is especially true if you are also considering dealership financing.

What to Expect After You Apply Online

The application doesn’t end with hitting ‘submit’. There are a few more steps before the funds are disbursed and you can purchase your vehicle.

Instant Pre-Approval vs. Further Review

Many online lenders boast "instant pre-approval." This means their automated system quickly assesses your basic information and credit score to give you an immediate idea of what you qualify for. However, this is often conditional. A full approval still requires human review and verification of your submitted documents. Some applications, especially for those with less-than-perfect credit, may require a longer review period.

Conditional Approval and Verification

If you receive conditional approval, the lender will then verify the documents you uploaded. They might call your employer to confirm your income or contact your bank to verify account information. This due diligence is standard practice to prevent fraud and ensure all information is accurate. Be prepared to respond promptly to any requests for additional information to keep the process moving.

Finalizing the Loan and Funding

Once all verifications are complete and your loan is fully approved, you’ll receive the final loan documents. Read these carefully one last time. If everything is satisfactory, you’ll electronically sign the agreement. The funds will then typically be disbursed directly to you, or in some cases, directly to the dealership where you are purchasing the car. This usually happens within a few business days, making the online process remarkably efficient.

Common Mistakes to Avoid When Applying for an Online Car Loan

Based on my experience helping countless individuals secure financing, certain pitfalls repeatedly trip up applicants. Being aware of these common mistakes can save you time, money, and stress.

Not Checking Your Credit Score First

This is a fundamental error. Going into an application blind means you don’t know where you stand. You might apply for loans you’re not qualified for, leading to rejections and multiple hard inquiries on your credit report. Conversely, you might settle for a higher interest rate than you deserve because you’re unaware of your true credit standing. Always know your credit score before you begin.

Applying with Too Many Lenders (Hard Inquiries)

While it’s smart to compare offers, indiscriminately applying to dozens of lenders can be detrimental. Each formal application triggers a hard credit inquiry, which can slightly lower your credit score. A few inquiries within a short period (typically 14-45 days, depending on the scoring model) are usually grouped as one for car loans, minimizing impact. However, too many spread out over time can signal to lenders that you’re a high-risk borrower. Focus on 3-5 reputable lenders after pre-qualification.

Ignoring the Fine Print

This mistake can be costly. Loan agreements are legal documents, and every clause matters. Overlooking details like prepayment penalties, late fees, or specific conditions for default can lead to unexpected expenses or legal issues down the line. Common mistakes to avoid are skimming through the terms and conditions. Always read every word and ask questions if anything is unclear.

Borrowing More Than You Can Afford

It’s tempting to get approved for a larger loan amount than you initially planned, especially if the offer looks attractive. However, borrowing more than your budget allows can lead to financial strain, missed payments, and even repossession. Always stick to your carefully calculated budget, regardless of how much a lender says you qualify for. Remember the total cost of ownership, not just the monthly payment.

Rushing the Process

While online applications are fast, don’t let the speed pressure you into making hasty decisions. Take your time to research lenders, compare offers, and thoroughly understand the terms. A few extra hours of due diligence can save you thousands of dollars over the life of the loan. Patience and thoroughness are virtues in car financing.

Pro Tips for a Smooth Online Car Loan Application

To ensure your journey to secure online auto financing is as smooth and successful as possible, here are some invaluable pro tips from us, honed through years of experience in the financial landscape.

Get Pre-Approved Before Car Shopping

This is perhaps the most powerful tip for any car buyer. Obtaining a pre-approval letter from an online lender gives you a clear budget and turns you into a cash buyer at the dealership. You’ll know exactly how much you can spend, empowering you to negotiate on the car’s price rather than getting caught up in monthly payment discussions. This also provides a benchmark to compare against any financing offers from the dealership, ensuring you get the best deal.

Improve Your Credit Score

A higher credit score unlocks lower interest rates. If you have time before needing a car, work on improving your score. Pay bills on time, reduce existing debt, and avoid opening new credit accounts. Even a small improvement can translate into significant savings over the life of your loan. This proactive step demonstrates financial responsibility, which lenders highly value.

Have All Documents Ready

As discussed earlier, preparation is key. Having digital copies of your driver’s license, proof of income, utility bills, and any other required documents organized and ready for upload will dramatically speed up the application and verification process. This prevents delays and shows the lender you are organized and serious.

Consider a Co-Signer (if needed)

If you have a lower credit score or limited credit history, a co-signer with excellent credit can significantly improve your chances of approval and help you secure a better interest rate. A co-signer shares responsibility for the loan, so ensure they understand the commitment involved. This can be a great strategy for younger borrowers or those rebuilding credit.

Don’t Be Afraid to Ask Questions

Even with all the information available, you might encounter terms or conditions you don’t fully understand. Never hesitate to contact the online lender’s customer service. A reputable lender will be happy to clarify any doubts. Clarity and understanding are essential before you commit to any financial agreement.

Conclusion: Embrace the Digital Future of Car Financing

The question of Can you apply for a car loan online? has evolved from a novel concept to a widely accepted and highly efficient reality. The digital landscape has transformed how we approach auto financing, offering unparalleled convenience, speed, and a wealth of options that empower consumers like never before. By understanding the process, avoiding common pitfalls, and leveraging expert tips, you can confidently navigate the online lending world and secure the best possible terms for your next vehicle.

Applying for a car loan online isn’t just about saving time; it’s about gaining control, transparency, and access to a competitive market designed to benefit you. So, take the driver’s seat in your car buying journey, embrace the digital highway, and embark on a smooth path to owning your dream car. With the right preparation and knowledge, securing your ideal auto loan online is well within your reach.

Further Reading:

- (Simulated Internal Link)

- (Simulated Internal Link)

- (https://www.consumerfinance.gov/consumer-tools/auto-loans/)