Navigating the Fast Lane: Your Ultimate Guide to Pre-Approved Car Loans – How It Works and Why It Matters

Navigating the Fast Lane: Your Ultimate Guide to Pre-Approved Car Loans – How It Works and Why It Matters Carloan.Guidemechanic.com

Buying a car is a significant financial decision, often ranking second only to purchasing a home. For many, the process can feel overwhelming, especially when it comes to financing. Imagine walking into a dealership with the power of a committed loan in your pocket, knowing exactly what you can afford and at what rate. This isn’t a dream; it’s the reality offered by a pre-approved car loan.

As an expert blogger and SEO content writer, I’ve seen firsthand how understanding this critical financial tool can transform the car-buying experience. This comprehensive guide will demystify pre-approved car loans, explain exactly how they work, and equip you with the knowledge to drive away with confidence. We’re talking about more than just a quick glance; we’re diving deep to give you the ultimate edge.

Navigating the Fast Lane: Your Ultimate Guide to Pre-Approved Car Loans – How It Works and Why It Matters

What Exactly is a Pre-Approved Car Loan?

At its core, a pre-approved car loan is a commitment from a lender (like a bank, credit union, or online financier) to loan you a specific amount of money, at a particular interest rate, for a set period. This commitment is made before you’ve even chosen the car you want to buy. Think of it as having a pre-negotiated budget and financing terms in hand, ready to go.

Unlike a simple "pre-qualification," which is often a soft inquiry into your credit and provides only an estimate, a pre-approval involves a more thorough assessment of your financial health. The lender performs a hard credit inquiry, reviews your income, and evaluates your debt-to-income ratio. This rigorous process allows them to provide a concrete offer, giving you a powerful tool in your car-buying journey.

Based on my experience, many buyers confuse pre-approval with pre-qualification. The key distinction is the "commitment." A pre-approval is a conditional offer, meaning the lender is serious about giving you the money, provided certain conditions (like the car’s age or mileage) are met and your financial situation hasn’t drastically changed.

The Unseen Advantages of Getting Pre-Approved for Your Car Loan

Why go through the effort of getting pre-approved? The benefits extend far beyond just knowing your budget. They fundamentally shift the power dynamics of the car-buying process in your favor.

-

Budgeting Clarity and Confidence: This is perhaps the most immediate and impactful benefit. With a pre-approval, you know precisely how much money a lender is willing to give you. This clarity empowers you to set realistic expectations for your car purchase, preventing you from falling in love with a vehicle outside your financial reach. It transforms "how much car can I afford?" into "I know exactly how much car I can afford."

-

Stronger Negotiating Power: When you walk into a dealership with a pre-approval letter, you’re not just a shopper; you’re a cash buyer in the eyes of the salesperson. You already have your financing secured, which means the dealership’s primary incentive to make money off your loan is removed. This puts you in a much stronger position to negotiate the actual price of the vehicle, focusing solely on the car’s cost rather than getting entangled in financing discussions.

-

Faster and Less Stressful Car Buying Process: Time is precious, and buying a car can be a lengthy ordeal. A pre-approved loan streamlines the entire process significantly. You spend less time in the dealership finance office, avoiding lengthy applications and waiting periods. This efficiency translates into a much smoother and less stressful experience, letting you focus on the excitement of your new vehicle.

-

Avoid Dealership Pressure and Upsells: Dealerships often have their preferred lenders and may push financing options that are more profitable for them, not necessarily better for you. With a pre-approval, you can politely decline these offers, or at least use them as a benchmark. You’re less susceptible to high-pressure tactics or unexpected add-ons in the finance office, as your main financing decision is already made.

-

Potentially Better Interest Rates and Terms: Lenders who offer pre-approvals often compete for your business, especially online lenders and credit unions. This competition can lead to more favorable interest rates and loan terms than what you might be offered on the spot at a dealership. Shopping around for pre-approvals allows you to compare offers and select the one that best suits your financial situation. Pro tips from us: Always compare the APR (Annual Percentage Rate), not just the stated interest rate, as it includes fees.

The Step-by-Step Process: How Does a Pre-Approved Car Loan Work?

Understanding the "how" is crucial to leveraging the power of pre-approval. It’s a structured process, and knowing each step will ensure a smooth journey.

Step 1: Assess Your Financial Health

Before you even think about applying, take an honest look at your financial standing. Lenders want to see a responsible borrower.

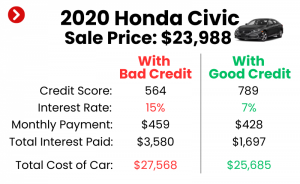

- Check Your Credit Score: Your credit score is the single most important factor. Lenders use it to gauge your creditworthiness and determine your interest rate. Order a free copy of your credit report from AnnualCreditReport.com to check for any errors and understand your current standing. A higher score typically means lower interest rates.

- Evaluate Your Debt-to-Income (DTI) Ratio: This ratio compares your monthly debt payments to your gross monthly income. Lenders prefer a lower DTI, as it indicates you have enough disposable income to comfortably make your car payments. Calculate yours to get a sense of where you stand.

Step 2: Gather Your Documents

Preparation is key. Having all your necessary paperwork ready will expedite the application process.

- Proof of Income: This typically includes recent pay stubs (usually 2-3 months), W-2 forms, or tax returns if you’re self-employed. Lenders need to verify your ability to repay the loan.

- Proof of Identity: A government-issued ID, such as a driver’s license or passport, is essential.

- Proof of Residency: Utility bills, a lease agreement, or mortgage statements can serve this purpose.

- Social Security Number: Required for credit checks.

- Employment Information: Details about your employer, including their contact information.

Step 3: Research Lenders

Don’t just go with the first lender you find. Different lenders cater to different types of borrowers and offer varying rates and terms.

- Banks: Traditional banks are a common choice, often offering competitive rates for customers with good credit.

- Credit Unions: Known for their member-focused approach, credit unions often provide excellent rates and more flexible terms, especially for those with less-than-perfect credit.

- Online Lenders: These platforms specialize in efficiency and often offer quick approvals and competitive rates, particularly for tech-savvy borrowers. Look for reputable names in the online lending space.

Step 4: The Application Process (Hard Inquiry)

Once you’ve chosen a few potential lenders, it’s time to apply. This step involves a "hard inquiry" on your credit report.

- Filling Out the Application: You’ll provide all the gathered information to the lender, either online, over the phone, or in person. Be thorough and accurate.

- Credit Check: The lender will perform a hard inquiry, which temporarily lowers your credit score by a few points. However, financial models typically treat multiple hard inquiries for the same type of loan (like car loans) within a short period (usually 14-45 days) as a single inquiry, so shopping around for rates won’t severely penalize your score. This is a crucial point many borrowers misunderstand.

Step 5: Receiving Your Pre-Approval Offer

If approved, the lender will present you with an offer. This is the moment you’ve been working towards!

- Loan Amount: The maximum amount the lender is willing to finance.

- Interest Rate: The percentage charged on the borrowed money.

- Loan Term: The duration of the loan (e.g., 36, 48, 60, or 72 months).

- Other Conditions: There might be conditions related to the age, mileage, or type of vehicle you can purchase. For example, some lenders might not finance vehicles older than 10 years or with very high mileage.

Step 6: Understanding the Offer Letter

Don’t just skim your pre-approval letter. It contains vital information.

- Expiration Date: Pre-approvals are not indefinite; they typically have an expiration date, often 30-90 days. Make sure to buy your car within this window.

- Specific Terms and Conditions: Read all the fine print. Are there any fees? What are the payment due dates? Are there prepayment penalties? Understanding these details prevents surprises later.

Step 7: Car Shopping with Confidence

This is where the pre-approval truly shines. You now have a clear budget and financing in hand.

- Focus on the Car Price: Your pre-approval allows you to negotiate the purchase price of the vehicle as if you were paying cash. This separates the car negotiation from the financing negotiation, making both simpler.

- Test Drive and Inspect: With financing sorted, you can concentrate on finding the right vehicle that meets your needs and fits within your pre-approved budget.

Step 8: Finalizing the Loan at the Dealership

Once you’ve found your perfect car, the final steps are straightforward.

- Present Your Pre-Approval: Inform the dealership that you have your own financing.

- Compare Dealership Offers: The dealership might still offer their own financing options. It’s wise to compare their offer with your pre-approval. If they can beat your pre-approved rate, fantastic! If not, you proceed with your pre-approved loan.

- Sign the Papers: Once you’ve agreed on the car price and chosen your financing, you’ll sign the necessary loan documents and vehicle purchase agreements.

Key Factors Lenders Consider for Pre-Approval

Lenders aren’t just guessing when they offer you a pre-approval. They use a structured approach to assess risk.

- Credit Score: As mentioned, this is paramount. A FICO score generally above 660 is considered good, while scores above 720 usually qualify for the best rates. Lenders use your credit history to predict your likelihood of repaying the loan.

- Income and Employment Stability: Lenders want to see a consistent and reliable source of income. Stable employment history over several years demonstrates your ability to make regular payments. They’ll look at your gross income to ensure it’s sufficient for the loan amount requested, in addition to your other living expenses.

- Debt-to-Income (DTI) Ratio: A DTI ratio below 43% is generally preferred, though some lenders might approve higher ratios depending on other factors. This ratio directly impacts your ability to take on new debt without becoming financially strained.

- Loan-to-Value (LTV) Considerations: While pre-approval is for a set amount, the actual car you choose will have an impact. Lenders look at the car’s value to ensure it’s worth the loan amount. If you’re looking at a car with an LTV ratio that’s too high (meaning you’re borrowing significantly more than the car’s market value), it might affect the final approval or require a larger down payment.

- Down Payment: While not always mandatory for pre-approval, making a down payment significantly improves your chances of approval and can lead to better terms. It reduces the amount you need to borrow, lowers your monthly payments, and demonstrates your financial commitment. It also lowers the LTV, making the loan less risky for the lender.

Pre-Approval vs. Pre-Qualification: What’s the Difference?

This distinction is crucial and often misunderstood. While both terms sound similar, they represent very different stages in the loan process.

- Pre-Qualification: This is a preliminary assessment based on basic financial information you provide, often without a hard credit inquiry. It gives you an estimate of what you might be approved for. It’s a soft check, doesn’t affect your credit score, and is not a guarantee of a loan. Think of it as a casual conversation.

- Pre-Approval: This is a conditional offer of credit based on a more thorough review of your finances, including a hard credit inquiry. It states the maximum loan amount, interest rate, and terms the lender is willing to provide. It’s a commitment, assuming no significant changes to your financial profile and that the chosen vehicle meets their criteria. This is a serious offer.

Based on my experience, many people get excited about a "pre-qualified" offer, only to be disappointed when they apply for the actual loan. Always aim for pre-approval if you want true buying power.

Common Myths and Misconceptions About Pre-Approved Car Loans

There are several persistent myths that deter people from seeking pre-approval. Let’s debunk them.

- "It’s a Guaranteed Loan": While a pre-approval is a strong commitment, it’s not 100% guaranteed. The final loan is still contingent on the vehicle meeting the lender’s criteria (e.g., age, mileage, condition) and no significant changes occurring in your financial situation between pre-approval and purchase.

- "It Hurts Your Credit Score Too Much": Yes, a hard inquiry will temporarily lower your score by a few points. However, as mentioned, multiple inquiries for the same type of loan within a specific window (typically 14-45 days) are often treated as a single inquiry by credit scoring models. This allows you to shop for the best rates without significant credit damage. The benefit of securing a lower interest rate often far outweighs the minimal, temporary credit score dip.

- "You’re Locked Into One Lender": Not at all. A pre-approval simply gives you an option. You are free to explore other financing options, including those offered by the dealership. The pre-approval acts as your baseline or backup, ensuring you have a competitive offer in hand.

Pro Tips for Maximizing Your Pre-Approval Benefits

To truly make the most of your pre-approved car loan, consider these expert recommendations.

- Shop Around for Multiple Offers: Don’t stop at just one pre-approval. Apply to 2-3 different lenders (within that 14-45 day window) to compare interest rates, terms, and conditions. This competition among lenders works in your favor.

- Look Beyond Just the Interest Rate: While the interest rate is critical, also consider the loan term, any associated fees, and prepayment penalties. A slightly higher interest rate on a shorter term might result in less overall interest paid.

- Be Aware of the Expiration Date: Keep track of when your pre-approval expires. If you don’t find a car within that timeframe, you’ll need to reapply.

- Understand the Loan Terms Fully: Before signing anything, ensure you comprehend every aspect of the loan agreement. Ask questions if anything is unclear. This includes understanding the monthly payment, total interest paid over the loan’s life, and any specific clauses.

- Don’t Settle for the First Car You See: With your financing secured, you have the luxury of patience. Take your time to find the right car that fits your needs and budget.

- Consider a Down Payment: Even if not required, a down payment reduces your loan amount, lowers your monthly payments, and decreases the total interest paid over the life of the loan. It also provides immediate equity in the vehicle.

Common Mistakes to Avoid When Seeking Pre-Approval

Even with the best intentions, some common pitfalls can derail your pre-approval process.

- Applying with Too Many Lenders Simultaneously (Outside the Shopping Window): While shopping for rates within a short window is fine, spreading applications over several months can lead to multiple hard inquiries that do negatively impact your score. Be strategic.

- Not Understanding the Terms and Conditions: Skipping the fine print can lead to unexpected fees or restrictive clauses later on. Always read your pre-approval letter carefully.

- Ignoring Your Credit Report Before Applying: Failing to check your credit report for errors or inaccuracies beforehand means you might be penalized for something that isn’t even your fault. Correcting errors can significantly boost your score.

- Making Major Financial Changes During the Process: Avoid opening new credit lines, closing old ones, or making large purchases between getting pre-approved and finalizing your car loan. These actions can alter your credit profile and DTI, potentially invalidating your pre-approval.

- Assuming All Dealers Accept All Pre-Approvals: While most major dealerships work with various lenders, some might have specific policies or partnerships. It’s always a good idea to confirm with the dealership if they can process your chosen pre-approved loan.

What Happens If You’re Denied Pre-Approval?

A denial isn’t the end of the road. It’s an opportunity to understand and improve.

- Understanding the Reasons: Lenders are legally required to provide you with a reason for denial. This could be a low credit score, high DTI, insufficient income, or errors on your credit report.

- Steps to Improve Your Chances:

- Review Your Credit Report: Dispute any errors.

- Improve Your Credit Score: Make on-time payments, reduce credit card balances, and avoid new debt.

- Increase Your Income or Reduce Debt: Lowering your DTI makes you a more attractive borrower.

- Consider a Larger Down Payment: This reduces the loan amount and the risk for the lender.

- Look for a Co-signer: A co-signer with good credit can help you get approved, but remember they are equally responsible for the loan.

Is a Pre-Approved Car Loan Right for You?

For most car buyers, the answer is a resounding yes. A pre-approved car loan empowers you, gives you control, and simplifies a complex process. It transforms the car buying experience from a potentially stressful negotiation into an exciting and confident search for your ideal vehicle.

Whether you’re a first-time buyer or a seasoned car owner, taking the proactive step of securing pre-approval is a smart financial move. It ensures you get the best possible deal on your financing, allowing you to focus on getting the best deal on your car.

For more insights into managing your finances effectively, consider exploring resources on understanding your credit score . Additionally, if you’re comparing different loan offers, our guide on what to look for can be invaluable . To further deepen your knowledge on consumer financial protection, we recommend checking out the Consumer Financial Protection Bureau’s auto loan resources .

Conclusion: Drive Away with Confidence

A pre-approved car loan is more than just a financial instrument; it’s a strategic advantage. It shifts the power dynamic from the seller to the buyer, allowing you to approach the dealership with a clear budget, competitive financing in hand, and the confidence to negotiate for the best possible price on your desired vehicle.

By understanding how a pre-approved car loan works, leveraging its benefits, and avoiding common pitfalls, you can navigate the complexities of car financing with ease. Take control of your car-buying journey, secure your pre-approval, and drive away not just with a new car, but with peace of mind. Your dream car is within reach, and with pre-approval, you’re on the fastest route to getting it.