Navigating the Green Mountain State: Your Comprehensive Guide to Bad Credit Car Loans in Vermont

Navigating the Green Mountain State: Your Comprehensive Guide to Bad Credit Car Loans in Vermont Carloan.Guidemechanic.com

Driving in Vermont isn’t just a convenience; for many, it’s a necessity. From navigating winding country roads to commuting through Burlington, a reliable vehicle opens up opportunities and connects communities. However, if you’ve faced financial hurdles in the past, the thought of securing a car loan with bad credit in Vermont can feel like an uphill battle. It’s a common misconception that a less-than-perfect credit score closes the door to car ownership.

Based on my experience working within the auto finance industry, I can tell you unequivocally that this isn’t true. While challenging, obtaining bad credit car loans in Vermont is absolutely achievable. This isn’t about magic; it’s about understanding the landscape, preparing thoroughly, and knowing where to look. This ultimate guide is designed to empower you with the knowledge and strategies needed to confidently secure a vehicle, even with a tarnished credit history, right here in the Green Mountain State. We’ll delve deep into every aspect, ensuring you’re well-equipped for success.

Navigating the Green Mountain State: Your Comprehensive Guide to Bad Credit Car Loans in Vermont

Understanding the Landscape: What "Bad Credit" Really Means for Car Loans

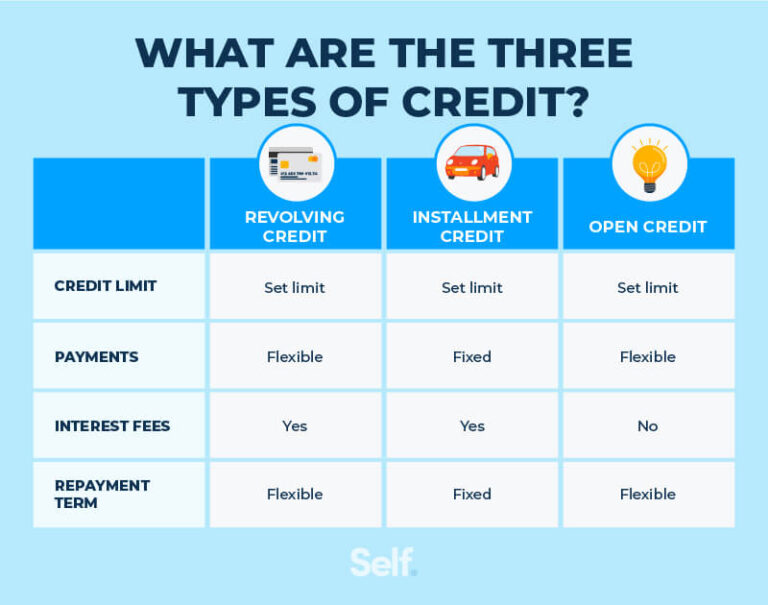

Before we explore solutions, let’s clarify what "bad credit" signifies in the eyes of an auto lender. Your credit score is a numerical representation of your creditworthiness, primarily generated by credit bureaus like Equifax, Experian, and TransUnion. FICO scores, which range from 300 to 850, are widely used.

Generally, a FICO score below 620 is considered "subprime" or "bad credit." This range signals to lenders that you might have a higher risk of defaulting on a loan. Factors contributing to a low score include missed payments, high credit utilization, bankruptcies, or foreclosures. Lenders view these as indicators of past financial instability.

However, it’s crucial to understand that a low score doesn’t automatically disqualify you. It simply means lenders will approach your application with more caution. They’ll scrutinize other aspects of your financial life more closely, and the terms of your loan will likely reflect the perceived higher risk. This often translates to higher interest rates, but it doesn’t mean no loan at all.

Why Vermont? Unique Considerations for Car Loans in VT

While the general principles of bad credit auto loans apply nationwide, there are nuances when seeking bad credit car loans in Vermont. The state’s unique character, from its rural nature to its community-focused ethos, can influence your options. For instance, Vermont’s population centers are less dense than in many other states, meaning access to public transportation can be limited, making a personal vehicle even more essential for daily life and work.

This vital need for transportation often translates into a more understanding approach from local lenders and dealerships. They recognize the practicalities of living in Vermont and the importance of helping residents maintain mobility. While state-specific consumer protection laws are generally aligned with federal standards, the local banking and credit union landscape can offer a more personal touch. Understanding this local context is key to successfully navigating the process of getting an auto loan with bad credit in Vermont.

Laying the Groundwork: Essential Preparation for Your Loan

Securing Vermont car financing with bad credit requires thorough preparation. This isn’t just about showing up; it’s about presenting yourself as a responsible borrower despite past challenges. Based on my insights, the more prepared you are, the better your chances of approval and securing more favorable terms.

1. Know Your Credit Score and Report

Your credit report is your financial resume. Before you even think about stepping into a dealership, obtain a copy of your credit report from all three major bureaus (Equifax, Experian, TransUnion). You are entitled to a free report annually from each through AnnualCreditReport.com. Review it meticulously for any errors or discrepancies.

Even minor inaccuracies can negatively impact your score. If you find mistakes, dispute them immediately. Correcting errors can sometimes boost your score enough to move you into a better lending tier. Knowing your score upfront also prevents surprises and helps you set realistic expectations for interest rates.

2. Craft a Realistic Budget

One of the most common mistakes people make is looking at cars they can’t genuinely afford. Pro tips from us: create a detailed budget before you start shopping. Factor in not just the monthly loan payment, but also insurance, fuel, maintenance, and registration.

Remember, a higher interest rate on a bad credit loan means more of your payment goes towards interest, not the principal. A responsible budget ensures you can comfortably make your payments, preventing further damage to your credit. This also shows lenders you’re serious about financial responsibility.

3. Accumulate a Down Payment

A significant down payment is one of your most powerful tools when seeking bad credit car loans in Vermont. It reduces the amount you need to borrow, thereby lowering your monthly payments and the total interest paid over the life of the loan. More importantly, it signals to lenders that you have "skin in the game."

A substantial down payment mitigates some of the lender’s risk, making them more willing to approve your loan. Even 10-20% of the car’s value can make a huge difference in how your application is perceived. Start saving early, as this single step can dramatically improve your loan prospects.

4. Leverage Your Trade-In

If you currently own a vehicle, consider its trade-in value. This can act as a de facto down payment, reducing your financing needs. Get an accurate appraisal of your car’s worth from multiple sources, such as Kelley Blue Book or Edmunds, before heading to the dealership.

Don’t accept the first offer if it feels low. A well-maintained trade-in can be a significant asset in securing a better deal on your new loan. It’s essentially free money that you can put towards your purchase, reducing the burden of a new loan.

5. Gather All Necessary Documents

Lenders will require a range of documents to verify your identity, income, and residency. Having these ready will streamline the application process and show your seriousness. Common documents include:

- Proof of Identity: Driver’s license or state ID.

- Proof of Residency: Utility bill, lease agreement, or mortgage statement with your Vermont address.

- Proof of Income: Recent pay stubs (usually 2-3 months), bank statements, or tax returns if self-employed.

- References: Sometimes requested, especially for subprime loans.

- Insurance Quote: Proof of insurance will be required before you drive off the lot.

Being organized demonstrates reliability, which is a key trait lenders look for in borrowers with a challenging credit history.

Finding the Right Lender for Bad Credit Car Loans in VT

Not all lenders are created equal, especially when it comes to financing for individuals with bad credit. Your search for dealers with bad credit car loans in Vermont should be strategic and focused. Common mistakes to avoid are applying to too many places at once (which can hurt your credit score) or only considering traditional banks.

1. Dealerships Specializing in Bad Credit Financing

Many dealerships, particularly larger ones, have departments dedicated to "special finance" or "subprime lending." These dealerships often work with a network of lenders who specialize in approving auto loans for bad credit in Vermont. They understand the unique challenges and are equipped to help.

Some dealerships operate as "Buy Here, Pay Here" (BHPH) lots. These dealerships finance the loan in-house, meaning you make payments directly to them. While they can be a viable option for those with very poor credit, they often come with significantly higher interest rates and less flexible terms. Always read the fine print carefully and compare rates before committing to a BHPH dealer.

2. Local Credit Unions

Credit unions are member-owned financial institutions known for their community focus and often more flexible lending criteria compared to large banks. If you’re a member, or eligible to become one, a local Vermont credit union might be an excellent place to inquire about car loans with bad credit in Vermont.

They may be more willing to look beyond your credit score and consider your overall financial situation, including your relationship with the credit union. Building a relationship with a credit union can pay dividends in the long run.

3. Online Lenders

The digital age has brought a plethora of online lenders who specialize in bad credit auto loans. These platforms offer convenience, allowing you to apply from home and often receive multiple offers. This can be a great way to compare rates and terms without visiting multiple physical locations.

However, exercise caution. Research online lenders thoroughly, read reviews, and ensure they are reputable. Always verify their licensing and check for any hidden fees. While convenient, the personal touch might be missing, so you’ll need to be your own best advocate.

4. Traditional Banks (With a Caveat)

While major banks are generally stricter with credit requirements, it doesn’t hurt to inquire, especially if you have an existing relationship with one. If your bad credit is due to a specific, explainable event (e.g., medical emergency) and you’ve shown recent financial stability, your current bank might be willing to work with you. They might offer a more competitive rate than a subprime lender if they see you as a long-term client.

The Application Process: What to Expect and How to Succeed

Once you’ve identified potential lenders, the application process for bad credit car loans VT will begin. This stage requires honesty, patience, and a clear understanding of what lenders are looking for.

Lenders specializing in subprime loans will look beyond just your credit score. They will heavily weigh your income stability, your debt-to-income (DTI) ratio, and your employment history. A consistent job and reliable income demonstrate your ability to make payments, even if your past credit history is shaky.

When discussing terms, pay close attention to the Annual Percentage Rate (APR), which includes the interest rate plus any fees. For bad credit loans, APRs can be significantly higher than for prime loans. Also, understand the loan term (how many months you’ll be paying) and any prepayment penalties.

Consider a Co-signer: If you have a trusted friend or family member with good credit who is willing to co-sign, it can dramatically improve your chances of approval and potentially secure a lower interest rate. A co-signer essentially guarantees the loan, taking on responsibility if you default. This significantly reduces the lender’s risk. However, this is a serious commitment for the co-signer, as their credit will also be affected if you miss payments.

Strategies to Improve Your Chances (and Your Credit)

Even if you need a car now, implementing strategies to improve your credit will benefit you in the long run. Based on our insights, these steps can help you secure better financing in the future, and even slightly improve your current standing.

1. Actively Build Your Credit

There are proactive steps you can take to start rebuilding your credit. Secured credit cards, where you put down a deposit as collateral, are a great way to show responsible credit use. Credit builder loans, offered by some credit unions, are another option where you make payments into a savings account, and the money is released to you after the loan term. Consistent, on-time payments on these tools will gradually improve your score.

For a deeper dive into understanding and improving your credit, you might find our article on Understanding Your Credit Score: A Comprehensive Guide helpful. (Internal Link Placeholder)

2. Review and Dispute Credit Report Errors

As mentioned earlier, regularly checking your credit report is crucial. Errors are more common than you might think and can unfairly lower your score. Disputing inaccuracies with the credit bureaus can lead to a quick bump in your score. It’s a simple yet effective way to ensure your report accurately reflects your financial history.

3. Maintain Stable Income and Employment

Lenders prioritize stability. If you’re seeking bad credit car loans in Vermont, demonstrating a consistent employment history and a steady income stream is paramount. Avoid changing jobs frequently during the application process, as this can raise red flags for lenders. The longer you’ve been with your current employer, the better.

4. Show Overall Financial Responsibility

Even if your credit score isn’t perfect, showing responsibility in other areas of your financial life can help. Paying all your bills on time—not just credit accounts, but also utilities, rent, and phone bills—demonstrates a commitment to financial obligations. While these don’t always directly impact your credit score, they can be considered by lenders when making a subjective decision on a subprime loan.

What to Watch Out For: Red Flags and Common Pitfalls

When dealing with bad credit car loans VT, vigilance is key. Unfortunately, some less scrupulous lenders may try to take advantage of your situation.

- Exorbitant Interest Rates: While higher rates are expected, be wary of rates that seem outrageously high (e.g., above 25-30% for a standard auto loan). Shop around and compare offers.

- Hidden Fees: Always ask for a full breakdown of all costs associated with the loan. Look out for excessive "documentation fees," "processing fees," or mandatory add-ons you don’t need or understand.

- Pushy Sales Tactics: If a dealer or lender pressures you into making a decision quickly, walk away. A reputable lender will give you time to review the terms.

- "Guaranteed Approval" Claims: No legitimate lender can "guarantee" approval without reviewing your financial information. These are often marketing ploys that lead to unfavorable terms.

- Unclear Terms: If you don’t understand any part of the loan agreement, ask for clarification. Do not sign anything you don’t fully comprehend. Understanding the fine print is paramount for consumer protection. For more information on your rights as a borrower, consult resources like the Consumer Financial Protection Bureau (CFPB) at www.consumerfinance.gov. (External Link)

Driving Forward: After You Get Your Loan

Congratulations! You’ve secured your bad credit car loan in Vermont. Now, the real work begins: using this opportunity to rebuild your credit and secure your financial future.

1. Make Payments On Time, Every Time

This is the single most important step. Consistent, on-time payments are reported to credit bureaus and are the fastest way to improve your credit score. Set up automatic payments or calendar reminders to ensure you never miss a due date. This loan can be a powerful tool for credit rehabilitation.

2. Understand Your Credit Score’s Evolution

As you make timely payments, you’ll see your credit score gradually improve. This means that in the future, you’ll be eligible for better interest rates on other loans, like mortgages or personal loans. This initial bad credit auto loan Vermont is an investment in your financial future.

3. Explore Refinancing Opportunities

Once your credit score has improved significantly (typically after 12-18 months of consistent payments), you may be able to refinance your car loan at a lower interest rate. Refinancing can save you hundreds or even thousands of dollars over the life of the loan by reducing your monthly payments and total interest paid.

4. Maintain Your Vehicle

Beyond the loan, remember that vehicle maintenance is crucial. Regular servicing protects your investment and prevents costly repairs down the line. A reliable car is essential in Vermont, and keeping it in top shape helps ensure you can meet your daily needs without unexpected financial burdens. For tips on managing car expenses, consider reading our article on Budgeting for Your First Car: What You Need to Know. (Internal Link Placeholder)

Your Journey to a Reliable Ride in Vermont

Securing bad credit car loans in Vermont might seem daunting, but it is far from impossible. By approaching the process with preparation, knowledge, and a strategic mindset, you can overcome past financial challenges and get behind the wheel of a reliable vehicle. Remember, this isn’t just about getting a car; it’s about taking a significant step towards financial recovery and establishing a stronger credit history for the future.

Armed with the insights from this comprehensive guide, you are now well-equipped to navigate the unique landscape of auto financing in the Green Mountain State. Don’t let a bad credit score define your ability to access essential transportation. Take control, prepare thoroughly, and confidently pursue your journey towards a brighter, more mobile future.