Navigating the Labyrinth: Your Comprehensive Guide to a Divorce Car Loan Under Your Name

Navigating the Labyrinth: Your Comprehensive Guide to a Divorce Car Loan Under Your Name Carloan.Guidemechanic.com

Divorce is undeniably one of life’s most challenging experiences, an emotional rollercoaster that reshapes futures and often brings unforeseen financial complexities. While the immediate focus might be on emotional healing and child custody, the practical realities of shared assets and debts can quickly become overwhelming. Among these, a common and particularly thorny issue arises when a car loan is solely under your name, but the vehicle was part of your marital life.

What happens when the car you paid for, or for which you are legally responsible, is driven by your ex-spouse, or is simply a major financial anchor tied to your name? This situation can feel like navigating a dense fog, filled with uncertainty and potential pitfalls for your credit and financial stability. Based on my extensive experience helping individuals through these intricate financial transitions, I can tell you that ignoring this issue is not an option.

Navigating the Labyrinth: Your Comprehensive Guide to a Divorce Car Loan Under Your Name

This comprehensive guide is designed to be your beacon, offering a detailed, step-by-step roadmap to understanding, managing, and ultimately resolving the complexities of a divorce car loan under your name. We’ll dive deep into your options, reveal common mistakes to avoid, and provide pro tips to safeguard your financial future. Our ultimate goal is to empower you with the knowledge to make informed decisions and emerge from your divorce financially resilient.

Understanding the Core Challenge: The Car Loan Dilemma in Divorce

When a car loan is "under your name," it signifies a critical legal and financial responsibility. This isn’t just a casual arrangement; it means you are the primary borrower, and the lender holds you accountable for every single payment, regardless of who drives the car or what your divorce decree states. This fundamental truth is where many people encounter their first major hurdle during a divorce.

The Legal vs. Practical Reality

It’s crucial to distinguish between what your divorce decree might say and what your loan agreement with the bank dictates. Your divorce decree is a legal document between you and your ex-spouse. It can assign responsibility for the car loan payments to your ex-spouse. However, this decree does not, in most cases, override your original contract with the lender.

From the lender’s perspective, if your name is on the loan, you are obligated to pay. If your ex-spouse misses payments, the lender will come after you, and your credit score will suffer significantly. This disconnect between legal assignments in a divorce and existing financial obligations is a major source of stress and potential financial damage.

Why "Under My Name" Matters So Much

Being the sole borrower means the debt is entirely yours on paper. This impacts your credit utilization, debt-to-income ratio, and overall financial health. If your ex-spouse is awarded the car and is supposed to make payments, but fails to do so, it’s your credit report that takes the hit. This can make it difficult to secure new loans, rent an apartment, or even get a new job in the future.

Furthermore, if the car is repossessed due to missed payments, that negative mark also goes on your credit history. The financial fallout can be long-lasting and severe, emphasizing the urgency of addressing this issue head-on during the divorce proceedings. Protecting your credit should be a top priority.

Common Scenarios You Might Face

Based on my experience, individuals often find themselves in one of several scenarios:

- The car is solely in your name, but your ex-spouse uses it and is expected to make payments. This is perhaps the riskiest situation for the primary borrower.

- The car is in your name, and you’ve both been using it, but now one of you wants to keep it. Deciding who gets the car and how the loan is handled becomes central to negotiations.

- The car is in your name, you use it, but your ex-spouse expects some form of compensation for its value or contributions to payments. This often involves complex asset division.

- The car is in your name, and your ex-spouse was a co-signer. While slightly different from "solely under your name," the principles of shared responsibility and removing one name remain similar, but the lender has two parties to pursue. For this guide, we’ll focus on the primary borrower’s perspective.

Understanding which scenario applies to you is the first step toward formulating an effective strategy.

Initial Steps: What to Do Immediately After Deciding on Divorce

Once the decision to divorce has been made, time is of the essence, especially concerning shared finances like car loans. Proactive steps taken early can prevent significant headaches down the line. Don’t wait until the final decree is being drafted; begin your due diligence now.

Gather All Pertinent Documents

Organization is your best friend during a divorce. Before you can make any informed decisions or present a clear picture to your attorney, you need all the facts.

Collect every document related to the car loan:

- The original loan agreement: This is vital, as it outlines the terms, interest rate, payment schedule, and default clauses.

- The car This shows who legally owns the vehicle.

- Insurance policies: Understand who is covered and what happens if the policy needs to change.

- Payment history: Demonstrate who has been making payments and when.

- Any communication with the lender: Keep records of calls, emails, or letters.

Having these documents readily available will streamline discussions with your legal and financial advisors.

Consult Legal Counsel Immediately

This cannot be stressed enough. While this article provides extensive information, it is not a substitute for personalized legal advice. A qualified divorce attorney is essential to navigate the legal intricacies of your specific situation.

Your attorney can:

- Explain your rights and obligations under state law.

- Help you negotiate the car loan in your divorce settlement.

- Draft crucial clauses in the divorce decree to protect you, such as indemnification agreements.

- Advise on potential legal recourse if your ex-spouse fails to uphold their end of the agreement.

Based on my experience, attempting to handle these legal aspects without professional guidance is a common mistake that often leads to unfavorable outcomes.

Conduct a Thorough Financial Assessment

Before proposing any solutions, you need a clear picture of your current financial health. This includes understanding your income, expenses, assets, and all debts.

Specifically for the car loan:

- Determine the outstanding balance: How much do you still owe?

- Assess the car’s current market value: Use reputable sources like Kelley Blue Book (KBB) or Edmunds to get an estimate. This helps determine if you have equity or negative equity.

- Evaluate your ability to pay: Can you afford the monthly payments on your own if necessary?

This assessment will inform which options are truly viable for you.

Open Communication (If Possible and Appropriate)

While emotions run high during a divorce, if possible, try to engage in open and honest communication with your soon-to-be ex-spouse regarding shared debts like the car loan. This isn’t always feasible or advisable, especially in high-conflict situations.

However, if both parties can discuss the issue calmly:

- You might find common ground on how to address the loan.

- It can lead to a more amicable and efficient resolution, potentially avoiding costly legal battles.

Pro tip from us: Always discuss these financial matters with your attorney first. They can advise you on what to say, what not to say, and if it’s even safe to communicate directly.

Exploring Your Options: Strategies for the Car Loan Under Your Name

Once you’ve gathered your documents, consulted legal counsel, and assessed your finances, it’s time to explore the practical strategies available to address the car loan under your name. Each option comes with its own set of advantages, disadvantages, and specific steps.

Option 1: Refinancing the Car Loan

Refinancing is often the cleanest and most recommended solution when a car loan is under one spouse’s name, and the other spouse will keep the car. It essentially replaces the old loan with a brand new one.

In-Depth Explanation of Refinancing

When you refinance, a new lender pays off the existing loan. A new loan agreement is then created, ideally with only the name of the spouse who will keep the car. This legally removes your name and financial responsibility from the debt. Beyond simply removing your name, refinancing can also offer benefits like a lower interest rate, which can reduce monthly payments, or a shorter loan term, which can save money over the life of the loan.

Eligibility for Refinancing

To qualify for refinancing, the spouse taking over the loan (your ex-spouse, in most cases) must meet the lender’s criteria. Key factors include:

- Credit Score: A good credit score is crucial for securing favorable terms.

- Income: The borrower must demonstrate sufficient income to comfortably make the monthly payments.

- Debt-to-Income Ratio (DTI): Lenders look at how much of the borrower’s income is already allocated to debt payments.

- Car’s Value and Age: The car’s value must typically exceed the loan amount, and older cars might be harder to refinance.

The Refinancing Process

The process usually involves:

- Application: The spouse applying for the new loan submits an application to various lenders.

- Credit Check: Lenders pull a credit report and assess financial stability.

- Approval and Offer: If approved, the lender provides new loan terms.

- Payoff and New Loan: The new lender pays off the old loan, and a new loan agreement is signed by the new borrower.

- Title Transfer: The car title is updated to reflect the new owner (if applicable) and the new lienholder.

Pro Tips for Refinancing

- Shop Around: Don’t just go with the first offer. Compare rates and terms from multiple banks, credit unions, and online lenders.

- Boost Credit: Encourage your ex-spouse (or yourself, if you’re keeping the car) to improve their credit score before applying.

- Consider a Co-signer (Cautiously): If the primary borrower struggles to qualify, a co-signer (other than you) might help, but this should be approached with extreme caution, as it links another person to the debt.

- Be Patient: The process can take a few weeks, so start early.

Common Mistakes to Avoid

Based on my experience, many individuals overlook the power of refinancing, or make critical errors. Common mistakes include:

- Not checking the credit score first: This leads to rejections or high-interest offers.

- Refinancing with a higher interest rate: This negates the financial benefit.

- Assuming the ex-spouse will qualify: It’s important to verify their financial standing.

Option 2: Selling the Car

If refinancing isn’t viable, or if neither party wants the car, selling it can be an effective way to eliminate the debt entirely. This option is particularly appealing if the car has positive equity.

In-Depth Explanation of Selling the Car

When you sell the car, the proceeds are used to pay off the outstanding loan balance. If the sale price is more than what is owed (positive equity), the remaining funds can be divided between you and your ex-spouse as part of the asset division in the divorce. If the sale price is less than what is owed (negative equity), you and your ex-spouse will need to decide how to cover the shortfall.

Negative Equity: What to Do

Negative equity, or being "upside down" on your loan, is a common challenge. If you owe more than the car is worth, selling it won’t fully cover the loan. In this scenario, you’ll need to:

- Pay the Difference: Both parties contribute funds to cover the remaining balance after the sale.

- Personal Loan: One or both parties might take out a personal loan to cover the gap, though this creates new debt.

- Short Sale (Rare for Cars): In some very specific cases, the lender might agree to accept less than the full amount owed, but this is uncommon for car loans and can still impact credit.

Determining Fair Market Value

Before selling, get an accurate assessment of the car’s value. Use online tools like Kelley Blue Book (KBB.com), Edmunds.com, or NADAguides.com. Consider the car’s condition, mileage, and features. This information is crucial for setting a realistic selling price and for negotiations during the divorce settlement.

Logistics of Selling

- Agreement: Both you and your ex-spouse must agree to sell the car and how the proceeds will be handled. This should be explicitly stated in the divorce decree.

- Title Transfer: Once sold, the lienholder (lender) will release the title, which is then transferred to the new owner.

Pro Tips for Selling

- Sell Privately: You generally get a higher price selling privately than trading it in or selling to a dealership.

- Prepare the Car: Clean it thoroughly, address minor repairs, and gather maintenance records to increase its appeal and value.

- Be Realistic: Don’t overprice the car; it will sit on the market.

Common Mistakes to Avoid

A common mistake I’ve seen is rushing to sell without understanding the market value or the implications of negative equity. Another error is not having a clear agreement with the ex-spouse on how to handle the proceeds or the shortfall.

Option 3: Transferring the Loan (Rare but Possible)

Directly transferring a car loan from one person’s name to another is exceedingly rare. Most lenders do not allow this because it fundamentally changes the original loan agreement and the credit risk assessment.

In-Depth Explanation of Transferring

In essence, a loan transfer would mean the lender agrees to remove you as the primary borrower and replace you with your ex-spouse without a new loan being issued. Lenders are typically unwilling to do this because they underwrote the loan based on your credit and financial profile. Replacing you with someone else is equivalent to issuing a new loan without the usual underwriting process.

Requirements (If a Lender Considers It)

If a lender were to even consider a transfer, your ex-spouse would need to have an exceptionally strong credit history, high income, and a very low debt-to-income ratio. They would essentially need to prove they are an even less risky borrower than you were initially. This is why it’s so uncommon.

Why it’s Difficult

Lenders prefer the security of the original borrower. Their primary concern is getting repaid. Changing the borrower increases their perceived risk. It’s almost always easier for your ex-spouse to apply for a new loan (refinance) in their own name than to convince the original lender to "transfer" the existing one.

Pro Tips (If You Pursue This)

- Direct Communication: Both you and your ex-spouse should contact the lender together to inquire about any transfer possibilities. Be prepared for a firm "no."

- Be Prepared to Refinance: Always have refinancing as your primary backup plan.

Option 4: Ex-Spouse Assumes Payments (With Safeguards)

This option means the car loan legally remains in your name, but your divorce decree states that your ex-spouse is responsible for making the monthly payments. This is the riskiest option for you as the primary borrower.

In-Depth Explanation of Assumption

The divorce decree is a court order. If it assigns the car and its associated payments to your ex-spouse, they are legally obligated to fulfill that. However, as discussed, this does not release you from your obligation to the lender. If your ex-spouse misses a payment, the lender will report it to credit bureaus under your name, and your credit score will plummet.

The HUGE Risk to Your Credit

The biggest danger here is that your financial well-being is entirely dependent on your ex-spouse’s payment reliability. If they forget, refuse, or simply cannot make payments, your credit takes the hit. You might have to make the payments yourself to protect your credit, and then pursue legal action against your ex-spouse to recover the money – a costly and emotionally draining process.

Essential Safeguards

If this is the only viable option, your divorce decree must include robust safeguards:

- Indemnification Clause: This is critical. It states that if your ex-spouse fails to make payments and you incur any financial loss (e.g., late fees, credit damage, having to make payments yourself), they must reimburse you. While it doesn’t protect your credit initially, it gives you legal recourse.

- Direct Payment to Lender: The decree can stipulate that your ex-spouse must send payments directly to the lender, not to you. This reduces the chance of funds being diverted.

- Payment Monitoring: You should have the right to receive proof of payment each month or to monitor the loan account directly (with lender permission, which is rare). Alternatively, you can regularly check your credit report for missed payments.

Legal Recourse

If your ex-spouse violates the divorce decree by not making payments, you can file a motion for contempt of court. This means asking the court to enforce its order. While effective, it requires time, legal fees, and further engagement with your ex-spouse and the court system.

Pro Tips

Based on my experience, this is often the riskiest option unless robust legal safeguards are in place and your relationship with your ex-spouse is highly amicable and trustworthy – a rare combination during divorce. If you go this route, ensure your attorney drafts the indemnification clause with utmost precision.

Option 5: Buyout by One Spouse

A buyout occurs when one spouse (who wishes to keep the car) pays the other spouse for their share of the car’s equity. This is typically done as part of the overall asset division in the divorce.

In-Depth Explanation of Buyout

If the car has positive equity (its market value is higher than the outstanding loan balance), the spouse keeping the car can "buy out" the other spouse’s interest. This means they pay the other spouse a sum equivalent to half of the car’s net equity (market value minus loan balance). The spouse keeping the car would then either continue to make payments on the existing loan (if it’s already in their name) or refinance it into their sole name.

Equity Calculation

- Determine Market Value: Get an accurate estimate of the car’s current worth.

- Subtract Loan Balance: Deduct the outstanding loan amount from the market value.

- Divide Equity: The remaining figure is the net equity, which is typically divided equally.

Example: Car value = $20,000; Loan balance = $10,000. Net equity = $10,000. The spouse keeping the car would pay the other spouse $5,000.

Funding the Buyout

The spouse buying out the other can fund this payment through various means:

- Savings: Using their personal savings.

- New Loan: Taking out a personal loan or including the buyout amount in a new car loan (if refinancing).

- Marital Asset Offset: Trading other marital assets. For example, if one spouse gets the car, the other might get a larger share of a retirement account or a portion of the house equity.

Title Transfer

If the car is in your name and your ex-spouse is buying you out, the title will need to be transferred to their name. If the loan is also in your name, they will need to refinance it into their name to complete the transfer and release you from liability.

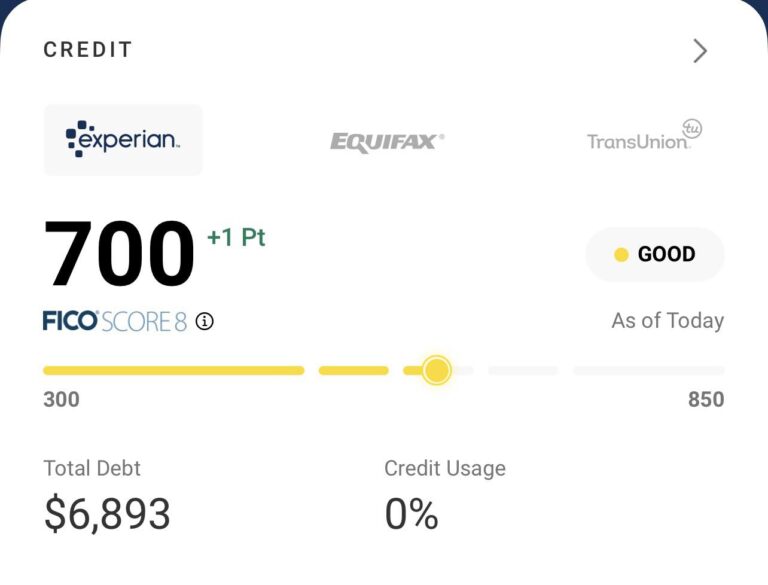

Protecting Your Credit Score During and After Divorce

Your credit score is a vital financial asset. Divorce, especially with shared debts like car loans, poses significant risks to it. Proactively protecting your credit should be a paramount concern throughout the entire process.

Ensure Timely Payments

This is the golden rule. Even if your divorce decree states your ex-spouse is responsible for the car loan payments, you remain legally obligated to the lender if your name is on the loan. If payments are missed, your credit score will be negatively impacted.

If you suspect your ex-spouse might default, or if you simply can’t get your name off the loan quickly, it’s often advisable to make the payments yourself to protect your credit. You can then seek reimbursement from your ex-spouse through legal channels, as provided by your divorce decree. It’s a bitter pill to swallow, but it can save your credit score.

Monitor Your Credit Reports Regularly

Regularly check your credit reports from all three major bureaus (Equifax, Experian, TransUnion). You are entitled to a free report from each once a year via AnnualCreditReport.com.

Look for:

- Missed payments: Any late payments on the car loan.

- New accounts: Any accounts opened in your name without your knowledge.

- Errors: Any inaccuracies in reporting.

Monitoring helps you catch problems early and take corrective action. Read more about how divorce impacts your credit score here.

Communicate with Your Lender (Cautiously)

You can inform your lender about your divorce, but be cautious. While some lenders might offer guidance, they are primarily concerned with getting paid. Do not assume they will make special arrangements or release you from the loan simply because you are divorced.

Focus on:

- Inquiring about refinancing options.

- Understanding their policies on name changes or transfers (even if rare).

- Never tell them you are no longer responsible for payments, as that’s a breach of your contract.

Dispute Errors Promptly

If you find any errors on your credit report, such as a missed payment incorrectly attributed to you, dispute it immediately with both the credit bureau and the lender. Provide all documentation to support your claim. Swift action can prevent long-term damage.

Legal Considerations and the Divorce Decree

While your focus might be on financial strategies, the legal framework of your divorce decree is the foundation for how these strategies are enforced and what protections you have.

The Power of the Decree

Your divorce decree is a legally binding court order. It can:

- Assign responsibility for debts, including the car loan, to one spouse.

- Order one spouse to refinance the loan within a specific timeframe.

- Include indemnification clauses to protect the other spouse.

However, it’s vital to remember that the decree generally cannot force a third-party lender to release you from a loan. It’s an agreement between you and your ex-spouse, not between you and the bank.

Indemnification Clauses: Your Legal Shield

An indemnification clause is a crucial legal tool that should be included in your divorce decree if your name remains on a car loan for which your ex-spouse is responsible. This clause states that if your ex-spouse fails to make payments, causing you financial harm (e.g., late fees, damage to your credit, having to pay yourself), they are legally obligated to reimburse you for those damages.

While an indemnification clause doesn’t prevent credit damage in the first place, it provides you with a legal pathway to recover your losses and hold your ex-spouse accountable in court.

Contempt of Court

If your ex-spouse violates a court order (such as failing to refinance the car loan or make payments as stipulated in the decree), you can file a motion for contempt of court. This asks the court to enforce its order and can result in various penalties for your ex-spouse, including fines or even jail time in extreme cases. This is a serious legal step and should only be pursued with your attorney’s guidance.

Mediating Financial Agreements

Divorce mediation can be an excellent alternative to costly litigation. A neutral third-party mediator helps both spouses negotiate and reach mutually agreeable solutions for all financial matters, including car loans. This often leads to more creative and less contentious resolutions.

Common Mistakes to Avoid

As a professional, I’ve seen too many people make these avoidable errors, often leading to prolonged financial distress and credit damage. Learning from these mistakes can save you considerable heartache.

- Ignoring the Car Loan Issue: The biggest mistake is hoping it will just "sort itself out." Debts don’t disappear; they accumulate interest and damage your credit.

- Assuming the Divorce Decree Protects Your Credit: As repeatedly emphasized, a divorce decree doesn’t release you from a contract with a third-party lender. Your name on the loan means you’re still responsible.

- Delaying Action: The longer you wait to address the car loan, the more complicated and potentially damaging it becomes. Interest accrues, car value depreciates, and credit can worsen.

- Not Understanding Negative Equity: Many people sell a car only to realize they still owe money. Always know the car’s market value versus the loan balance.

- Failing to Monitor Payments: If your ex-spouse is responsible for payments, you must actively monitor the loan or your credit report to ensure payments are being made on time.

- Co-signing a New Loan for an Ex-Spouse Without Thinking: While well-intentioned, co-signing a new car loan for your ex-spouse (even if it’s to get your name off the old one) simply shifts your liability to a new loan. Unless there’s no other option, and you fully trust them, this is rarely a wise decision.

Pro Tips for a Smoother Transition

Beyond avoiding pitfalls, these proactive strategies can significantly ease your journey through this complex financial landscape.

- Prioritize Clear Communication: While divorce can be fraught with emotion, try to maintain clear, business-like communication regarding financial matters. Document everything.

- Get Everything in Writing: Any agreements with your ex-spouse regarding the car loan must be explicitly detailed in your divorce decree. Verbal agreements are often unenforceable.

- Build an Emergency Fund: Having a financial cushion can provide peace of mind and allow you to make payments if your ex-spouse defaults, protecting your credit while you seek legal recourse.

- Seek Professional Advice: Don’t hesitate to consult with both a divorce attorney and a financial advisor. Their combined expertise is invaluable. For more financial tips during divorce, check out our guide on managing assets.

- Be Patient and Persistent: Resolving car loan issues in a divorce can take time and effort. Stay persistent in pursuing the best outcome for your financial future.

Beyond the Divorce: Rebuilding Your Financial Foundation

Once the dust settles and your car loan situation is resolved, it’s time to focus on rebuilding your financial foundation. This might involve:

- Reviewing your budget: Adjusting to single-income living.

- Rebuilding credit: If your score took a hit, focus on timely payments on all remaining debts.

- Setting new financial goals: Planning for your future, whether it’s buying a new car, a home, or saving for retirement.

For more detailed information on consumer rights related to debt and financial protection, you can visit the Consumer Financial Protection Bureau’s website at https://www.consumerfinance.gov/. This trusted external source provides invaluable resources for navigating complex financial situations.

Conclusion

Navigating your divorce car loan under your name doesn’t have to be an overwhelming or credit-damaging ordeal. While the process is complex and often emotionally charged, armed with the right knowledge and a proactive approach, you can safeguard your financial future.

By understanding your