Navigating the Maze: Understanding and Overcoming a 22 Percent APR Car Loan

Navigating the Maze: Understanding and Overcoming a 22 Percent APR Car Loan Carloan.Guidemechanic.com

Facing a 22 percent APR on a car loan can feel like a punch to the gut. It’s a number that immediately signals high costs and a potentially challenging financial road ahead. But understanding this situation, rather than panicking, is your first and most crucial step towards overcoming it.

This comprehensive guide is designed to shed light on what a 22 percent APR car loan truly means for your finances. We’ll explore why you might be offered such a rate, the long-term impact, and most importantly, actionable strategies to improve your situation. Our goal is to empower you with the knowledge to make informed decisions and pave your way to a more favorable financial future.

Navigating the Maze: Understanding and Overcoming a 22 Percent APR Car Loan

What Exactly Does 22 Percent APR Mean for Your Car Loan?

When you see "22 percent APR," it’s more than just the interest rate. APR stands for Annual Percentage Rate, and it represents the true annual cost of borrowing money. This figure encompasses not only the interest charged by the lender but also any additional fees or costs associated with the loan.

Think of it as the total price tag for borrowing money, expressed as a yearly percentage. While the interest rate is what the bank charges you to use their money, the APR provides a more complete picture. It helps you compare different loan offers more accurately, as it includes things like origination fees or other lender charges rolled into the loan.

For a car loan, a 22 percent APR is exceptionally high. It indicates that a significant portion of your monthly payment will go towards paying interest, rather than reducing your principal balance. This can make the car much more expensive over the life of the loan than its sticker price suggests.

Why You Might Be Offered a 22 Percent APR Car Loan

Receiving an offer for a 22 percent APR car loan can be disheartening, but it’s crucial to understand the underlying reasons. Lenders assess risk, and a high APR is their way of mitigating what they perceive as a higher risk borrower. Several factors contribute to this assessment, and it’s rarely just one isolated issue.

Based on my experience in the financial sector, these are the most common culprits:

Poor Credit History

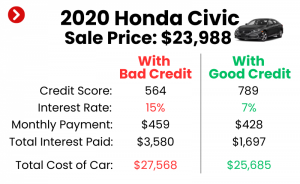

This is arguably the most significant factor. Your credit score is a numerical representation of your creditworthiness. A low FICO score, typically below 620, signals to lenders that you have a history of late payments, defaults, or perhaps even bankruptcies. Lenders view these as indicators of a higher likelihood that you might not repay your new loan.

A less-than-stellar credit history suggests a pattern of financial difficulty. To offset this perceived risk, lenders will charge a much higher interest rate. They are essentially charging you more for the privilege of borrowing, as they are taking on greater uncertainty about repayment.

Limited or No Credit History

It’s a common misconception that having no credit is better than bad credit. While it avoids the negatives, it also means lenders have no data to evaluate your repayment behavior. This makes you an unknown quantity, which can be just as risky in their eyes. Young adults or recent immigrants often fall into this category.

Without a track record, lenders have no basis to trust your ability to manage debt responsibly. They might offer a high APR as a default, "prove yourself" rate. Building credit takes time, but it’s an essential step towards securing better loan terms in the future.

High Debt-to-Income (DTI) Ratio

Your DTI ratio compares your total monthly debt payments to your gross monthly income. If a significant portion of your income is already committed to other debts—like credit card bills, student loans, or mortgage payments—lenders might see you as stretched too thin. A high DTI indicates that you might struggle to take on another substantial monthly payment.

Lenders prefer to see a DTI ratio below 36%, with anything above 43% generally considered high-risk. If your DTI is elevated, even with a decent credit score, a lender might increase your APR to compensate for the perceived financial strain. It shows you have less disposable income available to comfortably make new loan payments.

The Type of Vehicle You’re Buying

Believe it or not, the car itself can influence your APR. Older, high-mileage vehicles or those with a poor resale value are considered riskier collateral by lenders. If you default on the loan, the lender might struggle to recoup their losses by repossessing and selling the car.

Conversely, newer, more reliable vehicles with strong resale values present less risk. This is because the collateral holds its value better. When considering a high APR, sometimes opting for a slightly newer or more in-demand used car could paradoxically lead to a lower interest rate, as the lender’s risk is reduced.

Economic Factors and Lender Policies

Sometimes, the prevailing economic climate or the specific lender’s internal policies play a role. During periods of higher interest rates set by central banks, all loan rates tend to increase. Additionally, some lenders specialize in "subprime" loans and naturally have higher average APRs across the board.

It’s also worth noting that some lenders are simply more aggressive in their pricing for higher-risk borrowers. This highlights the importance of shopping around, as different institutions have different appetites for risk and varying pricing structures. Don’t assume the first offer is the only offer.

The True Cost: Understanding the Long-Term Impact of 22% APR

A 22 percent APR isn’t just a number; it’s a financial burden that can significantly inflate the total cost of your vehicle. The long-term impact extends far beyond your monthly payment, affecting your financial flexibility and wealth-building potential.

Let’s illustrate this with an example. Imagine you’re taking out a $20,000 car loan over 60 months (5 years) with a 22% APR.

- Monthly Payment: Approximately $567

- Total Paid Over 5 Years: $34,020

- Total Interest Paid: $14,020

In this scenario, you’d be paying over $14,000 in interest alone—nearly 70% of the original loan amount. That’s money that could have gone into savings, investments, or other essential expenses.

Opportunity Cost

This high interest rate comes with a significant opportunity cost. The money spent on excessive interest could have been invested, grown, or used to pay down other higher-interest debts. Instead, it’s essentially "lost" to the lender. This erodes your ability to build wealth or save for future goals, such as a down payment on a home or retirement.

Difficulty Building Equity

With a high APR, a large portion of your early payments goes straight to interest. This means you pay down the principal balance much slower. It becomes very difficult to build equity in your car, making it more likely you’ll be "upside down" on your loan (owing more than the car is worth) for an extended period. Being upside down can complicate selling or trading in the vehicle, as you’d need to pay the difference out of pocket.

Pro tips from us: Always focus on the total cost of the loan, not just the monthly payment. A slightly lower monthly payment over a much longer term can still mean significantly more interest paid overall. Don’t let a seemingly manageable monthly figure blind you to the true expense.

Navigating the High-Interest Waters: Strategies When You Have a 22% APR Loan

While a 22 percent APR is tough, it doesn’t mean you’re powerless. There are several strategies you can employ to mitigate the damage and work towards a better financial standing.

1. Negotiate Aggressively

Even with a high APR offer, there might be room for negotiation. Don’t accept the first rate you’re given without question. Ask the lender if there’s any flexibility, especially if you can offer a larger down payment or a shorter loan term. Sometimes, showing commitment can sway their decision.

It’s important to come prepared. Know your credit score, understand your budget, and be ready to walk away if the terms aren’t acceptable. Your willingness to explore other options can be a powerful negotiation tool.

2. Increase Your Down Payment

A larger down payment directly reduces the amount of money you need to borrow. This lowers the principal balance, which in turn reduces the total interest you’ll pay, even if the APR remains high. It also shows the lender you have skin in the game, potentially making them more willing to offer a slightly better rate.

Every dollar you put down is a dollar you won’t pay 22% interest on. If you can save up even a few extra hundred dollars, it can make a tangible difference over the life of the loan.

3. Opt for a Shorter Loan Term (If Affordable)

While a longer loan term means lower monthly payments, it also means paying significantly more interest over time. If your budget allows, choose the shortest loan term you can comfortably afford. This will result in higher monthly payments but drastically reduce the total interest paid and accelerate your path to ownership.

For example, on that $20,000 loan at 22% APR, reducing the term from 60 to 48 months would increase the monthly payment to about $643, but cut total interest paid to roughly $10,864 – a savings of over $3,000!

4. Shop Around Aggressively

Never settle for the first loan offer. Different lenders have different risk appetites and pricing models. Apply for pre-approvals from multiple sources: banks, credit unions, and online lenders. Credit unions, in particular, often offer more favorable rates to their members, even those with less-than-perfect credit.

Common mistakes to avoid are: only applying with the dealership’s finance department. Dealerships often work with multiple lenders but may prioritize those that offer them a higher commission. Doing your homework beforehand gives you leverage.

5. Consider a Co-signer

If you have a trusted family member or friend with excellent credit who is willing to co-sign, this can significantly improve your chances of getting a lower APR. A co-signer essentially pledges their good credit, assuring the lender that if you default, they will be responsible for the payments.

However, understand the risks involved. If you miss payments, it negatively impacts both your credit and your co-signer’s. This can strain relationships. Ensure both parties fully understand the commitment before proceeding.

6. Look for Dealer Incentives (with Caution)

Sometimes, dealerships offer special financing deals or cash back incentives. While these can be attractive, read the fine print carefully. Often, the lowest advertised APRs are only for borrowers with excellent credit. The cash-back offers might be tied to accepting a higher interest rate on the loan.

Always compare the total cost. A cash-back offer might seem good, but if it locks you into a much higher APR, you could end up paying more in the long run.

Is a 22% APR Car Loan Always a Bad Idea? When It Might Make Sense (Temporarily)

While a 22% APR car loan is far from ideal, there are very specific, limited circumstances where it might be a necessary, albeit temporary, solution. This is not a recommendation for long-term acceptance but rather a strategy for immediate needs with a clear exit plan.

1. Emergency Transportation is Essential

If you absolutely need a car for work, medical appointments, or other critical daily functions, and you have exhausted all other options, a high APR loan might be the only way to secure transportation. This situation typically arises when public transport isn’t feasible and ride-sharing costs would quickly exceed loan payments. It’s about survival, not luxury.

2. As a Credit-Building Opportunity

For individuals with very limited or poor credit, taking on a high APR loan and meticulously making every payment on time can serve as a stepping stone. Successfully managing this debt demonstrates creditworthiness to future lenders. This strategy requires immense discipline and a clear plan to refinance as soon as possible.

It’s a high-risk, high-reward approach to credit building. If you miss payments, it will only worsen your credit situation. The goal is to prove you can handle a loan, then shed the high interest.

3. No Other Options Available

In rare cases, after exploring every alternative, a 22% APR loan might genuinely be the last resort. This means you’ve been denied by other lenders, cannot secure a co-signer, and don’t have access to alternative transportation or funds.

Crucially, this should always come with a concrete plan to refinance the loan once your financial situation or credit score improves. Without a clear path to a better rate, a high APR loan can become a long-term financial trap.

Your Path to a Better Rate: Improving Your Financial Standing for Future Loans

The best long-term strategy for avoiding high APRs is to improve your financial health. This takes time and consistent effort, but the rewards are substantial.

1. Boost Your Credit Score

This is your most powerful tool. Focus on these key areas:

- Pay Bills On Time, Every Time: Payment history accounts for 35% of your FICO score. Even one late payment can significantly drop your score. Set up automatic payments to avoid missing deadlines.

- Reduce Credit Card Debt: Your credit utilization ratio (how much credit you use vs. how much you have available) impacts 30% of your score. Aim to keep this below 30%, ideally below 10%. Pay down balances aggressively.

- Check Your Credit Report for Errors: Obtain free copies of your credit report from AnnualCreditReport.com. Dispute any inaccuracies, as they can unfairly depress your score.

- Become an Authorized User: If a trusted family member has excellent credit, ask them to add you as an authorized user on one of their long-standing credit cards. Their good payment history can positively reflect on your report.

Pro tip: Consistency is key. There are no quick fixes for a bad credit score, but steady, responsible behavior will yield results.

2. Increase Your Income or Reduce Other Debt

Improving your debt-to-income ratio makes you a more attractive borrower. Look for ways to boost your income, whether through a side hustle, a raise, or a new job. Simultaneously, aggressively pay down other debts, especially high-interest credit card balances. This frees up more of your income for new loan payments.

3. Save for a Larger Down Payment

The more money you put down upfront, the less you need to borrow, and the less risk the lender takes. This can often translate into a lower APR. A substantial down payment also helps prevent you from being upside down on your loan early on.

4. Build a Relationship with a Bank or Credit Union

Having an established banking relationship can sometimes lead to better loan offers. If you’ve been a loyal customer with a checking or savings account, your bank or credit union might be more willing to work with you on loan terms, even if your credit isn’t perfect. They have a more holistic view of your financial behavior.

Refinancing Your 22% APR Car Loan: Your Best Escape Route

Once you’ve secured a 22% APR car loan, your primary goal should be to escape it. Refinancing is often the most effective strategy for reducing your interest rate and overall cost.

Refinancing means taking out a new loan to pay off your existing car loan. The hope is that your financial situation has improved since you first took out the loan, allowing you to qualify for a lower interest rate. Based on my experience, many people successfully refinance their high-APR loans within 6-12 months of consistent, on-time payments.

When to Consider Refinancing:

- Your Credit Score Has Improved: This is the most common reason. If you’ve diligently made payments, paid down other debts, and corrected credit report errors, your score should have increased.

- Interest Rates Have Dropped: General market interest rates can fluctuate. If rates are lower now than when you first borrowed, you might qualify for a better deal.

- Your Debt-to-Income Ratio Has Improved: Less debt or more income makes you a less risky borrower.

- You Want a Shorter Term: You can refinance into a new loan with a shorter term to pay it off faster, even if the APR isn’t dramatically lower, reducing total interest.

Steps to Refinance:

- Improve Your Credit First: Before applying, double down on all the credit-boosting strategies mentioned above. Every point matters.

- Shop for New Lenders: Don’t just go back to your original lender. Apply to multiple banks, credit unions, and online lenders. Compare their pre-qualification offers without impacting your score.

- Gather Your Documents: You’ll need proof of income, your current loan details (account number, payoff amount), and personal identification.

- Compare Offers: Look at the new APR, the new monthly payment, and the total interest you’d pay. Make sure the new loan truly saves you money.

- Complete the Process: Once approved, the new lender will pay off your old loan, and you’ll begin making payments to the new institution at your hopefully much lower rate.

Consider this example: If you refinance that $20,000 car loan (originally 22% APR, 60 months) after 12 months (with $1,020 principal paid and $5,784 interest paid) into a new 48-month loan at 10% APR, your new monthly payment would be around $460, and your remaining interest would drop significantly. You could save thousands! For more in-depth advice on this, check out our guide on How to Successfully Refinance Your Car Loan for a Lower Rate.

Alternatives to a High APR Car Loan

If a 22% APR car loan seems unavoidable, but you still have reservations, consider these alternatives before committing:

1. Buy a Cheaper, Older Used Car with Cash

If your budget allows, even a few thousand dollars can buy a reliable older vehicle outright. This completely eliminates interest payments and the burden of a loan. While it might not be your dream car, it provides essential transportation while you save for a better option.

2. Utilize Public Transportation or Ride-Sharing

In urban areas, public transport, cycling, or ride-sharing services like Uber or Lyft might be a more cost-effective solution in the short term. Calculate the monthly cost of these alternatives versus the high monthly payment and interest of a 22% APR loan. Sometimes, it makes financial sense to wait.

3. Borrow from Friends or Family (with a Formal Agreement)

If you have supportive loved ones, a private loan from friends or family can be an option. Crucially, treat this like a formal loan: put the terms, repayment schedule, and any interest (even if low) in writing. This protects both parties and prevents misunderstandings.

4. Consider a Personal Loan (Carefully)

Sometimes, a personal loan from a bank or credit union might have a lower APR than a subprime auto loan, especially if it’s unsecured. However, personal loan rates can also be very high, and they typically have shorter repayment terms. Compare rates diligently and understand that the car won’t serve as collateral, which can sometimes push rates higher on unsecured loans. For general financial literacy, consider resources like the Consumer Financial Protection Bureau (CFPB) for understanding various loan types and managing debt effectively: www.consumerfinance.gov.

Conclusion: Taking Control of Your Financial Journey

A 22 percent APR car loan is undoubtedly a challenging situation, but it’s not a dead end. By understanding what this rate means, why it’s offered, and the significant financial impact, you’ve taken the first critical step. Remember, knowledge is power, and with the right strategies, you can navigate these high-interest waters.

Focus on improving your credit, exploring all your options, and having a clear plan for refinancing. Every on-time payment you make and every point you add to your credit score brings you closer to a more favorable financial future. Don’t let a high APR define your long-term financial health; instead, use it as a catalyst to build stronger, more responsible financial habits. Your journey to a lower interest rate and financial freedom begins now. Start by assessing your current credit and exploring refinancing options today! For more tips on managing your credit, check out our article on How to Improve Your Credit Score Fast for Better Loan Rates.