Navigating the Motor City: Your Ultimate Guide to Bad Credit Car Loans in Detroit

Navigating the Motor City: Your Ultimate Guide to Bad Credit Car Loans in Detroit Carloan.Guidemechanic.com

Detroit, the heart of the American automotive industry, is a city where owning a reliable vehicle isn’t just a luxury—it’s often a necessity. From commuting to work to exploring the vibrant neighborhoods, a car provides essential freedom and connectivity. However, for many residents, a less-than-perfect credit score can feel like a roadblock to securing the auto financing needed.

If you’re in Detroit and grappling with bad credit, the thought of getting approved for a car loan might seem daunting. You might even feel like your options are limited, or that you’re destined for high-interest traps. Based on my experience in the auto finance landscape, I can assure you that this isn’t necessarily the case. While challenging, obtaining a bad credit car loan in Detroit is absolutely achievable with the right knowledge and approach.

Navigating the Motor City: Your Ultimate Guide to Bad Credit Car Loans in Detroit

This comprehensive guide is designed to be your trusted resource. We’ll demystify the process, explore your best options, and provide actionable strategies to help you drive away in a car you need, even with bad credit. Our ultimate goal is to empower you with the information to make informed decisions and secure financing that works for your unique situation in the Motor City.

Understanding Bad Credit and Its Impact on Car Loans

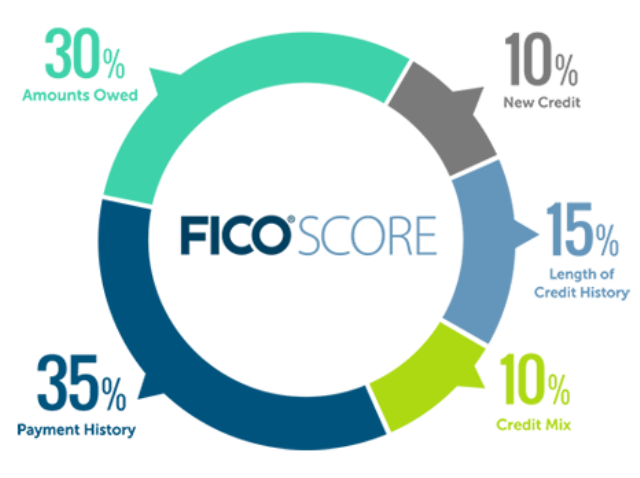

Before diving into solutions, it’s crucial to understand what "bad credit" truly means in the eyes of a lender. Your credit score, typically a FICO or VantageScore, is a three-digit number that represents your creditworthiness. A score generally below 620 is often considered "subprime" or "bad credit." This number is derived from your credit history, including payment history, amounts owed, length of credit history, new credit, and credit mix.

Why does this matter for a car loan? Lenders use your credit score as a primary indicator of risk. A low score suggests a higher likelihood of defaulting on payments, making them more hesitant to lend money. This hesitation often translates into less favorable loan terms, such as higher interest rates or larger down payment requirements, to offset their perceived risk.

Based on my experience, many people misunderstand that a bad credit score is a permanent barrier. It’s not. It’s a snapshot of your financial past, and while it impacts your present, it doesn’t dictate your future. The key is to demonstrate to lenders that despite past challenges, you are now a reliable borrower, or that specific circumstances led to your current score.

Why Detroit? Unique Considerations for the Motor City Car Buyer

Detroit’s unique character influences the car buying and financing landscape significantly. Unlike some major cities with extensive public transportation networks, Detroit is a sprawling metropolis where personal vehicles are often indispensable. Relying solely on ride-sharing or limited public transit can severely restrict job opportunities, access to services, and overall quality of life.

The local automotive culture also plays a role. Detroit is a hub for car dealerships, mechanics, and auto-related businesses. This concentration can mean more options for car buyers, but it also requires a savvy approach to navigate the competitive market. Understanding these local dynamics is crucial when seeking Detroit auto loans with bad credit.

Pro tips from us: The sheer volume of dealerships in and around Detroit means you have leverage. Don’t settle for the first offer you receive. Take the time to compare different lenders and dealerships, as their approaches to bad credit financing can vary widely.

Navigating the Detroit Landscape: Where to Find Bad Credit Car Loans

Finding a lender willing to approve a bad credit car loan in Detroit requires knowing where to look. Not all financial institutions or dealerships specialize in subprime lending. Here’s a breakdown of the most common avenues:

1. Specialty Bad Credit Dealerships

These dealerships often brand themselves specifically to cater to individuals with credit challenges. They understand the nuances of bad credit financing and have established relationships with subprime lenders. Their application processes are typically streamlined, focusing less on your credit score and more on your ability to repay the loan based on current income.

What to look for: While convenient, it’s important to research their reputation. Check online reviews and customer testimonials. Ensure they are transparent about all loan terms and fees. These dealerships can be a good starting point, but always compare their offers with others.

2. Buy Here Pay Here (BHPH) Dealerships

Buy Here Pay Here dealerships operate differently. They are both the seller and the lender, meaning they finance the car directly themselves. This model is often considered a last resort for those with very poor credit, as they approve loans based almost entirely on your income and down payment, rather than your credit score.

Common mistakes to avoid are focusing solely on the "guaranteed approval" aspect. While they offer accessibility, BHPH loans often come with significantly higher interest rates, shorter loan terms, and a limited selection of older, higher-mileage vehicles. Furthermore, not all BHPH dealerships report payments to credit bureaus, which means timely payments might not help rebuild your credit. Always ask about their credit reporting practices.

3. Credit Unions

Credit unions are member-owned financial cooperatives known for their community-focused approach. They often offer more flexible lending criteria and lower interest rates than traditional banks, even for members with less-than-perfect credit. If you’re a member of a local Detroit credit union, or eligible to join one, this can be an excellent option.

Their lending decisions are often more personalized, taking into account your overall financial picture rather than just your credit score. They might be more willing to work with you if you have a stable income and can explain past credit issues. It’s definitely worth exploring credit unions in the Detroit metropolitan area.

4. Online Lenders

The digital age has brought a plethora of online lenders specializing in bad credit auto financing Michigan. These platforms offer the convenience of applying from home and often provide pre-approval in minutes. They can connect you with a network of subprime lenders, allowing you to compare multiple offers without visiting various dealerships.

The key advantage here is the ability to shop around efficiently. However, ensure you are dealing with reputable online lenders. Always check for security measures on their websites and read reviews. Transparency about terms, rates, and fees is paramount.

5. Banks (Traditional & Non-Traditional)

While traditional banks might have stricter lending criteria for bad credit, some have dedicated subprime lending departments or partnerships. It’s always worth checking with your current bank, especially if you have a long-standing relationship with them. Non-traditional banks or finance companies that specialize in auto loans can also be a viable option, often having more flexible underwriting processes than the big national banks.

The Application Process: What to Expect and How to Prepare

Preparing thoroughly for the application process can significantly improve your chances of approval for a bad credit car loan in Detroit. Lenders, especially those specializing in subprime loans, want to see stability and an ability to repay.

Essential Documents: You’ll typically need to provide proof of income (pay stubs, bank statements, tax returns), proof of residency (utility bills, lease agreement), a valid driver’s license, and references. If you have a down payment, proof of funds will also be required. Gather these documents beforehand to streamline the process.

Understanding Your Credit Report: Pro tips from us: Obtain a copy of your credit report from all three major bureaus (Equifax, Experian, TransUnion) before you start applying. Review it carefully for any errors or inaccuracies. Disputing and correcting these can potentially boost your score, even slightly, which can make a difference. Knowing what’s on your report also allows you to proactively address any concerns a lender might have.

Down Payment: A significant down payment is one of the most powerful tools you have when seeking a bad credit car loan. It reduces the amount you need to borrow, thereby lowering the lender’s risk. It also demonstrates your financial commitment to the loan. Even a modest down payment can make a big difference in approval odds and interest rates.

Co-Signer: If you have a trusted individual with good credit who is willing to co-sign your loan, it can dramatically improve your chances of approval and secure better terms. The co-signer essentially guarantees the loan if you default. However, this is a serious responsibility for the co-signer, as their credit will also be impacted if you miss payments. Ensure both parties fully understand the implications.

Key Factors Lenders Consider for Bad Credit Loans

When evaluating your application for a Detroit auto loan with bad credit, lenders look beyond just your credit score. They aim to assess your current financial stability and capacity to repay.

Income Stability: Lenders want to see a steady and reliable source of income. This demonstrates your ability to make consistent monthly payments. A long history with the same employer is a strong positive indicator.

Debt-to-Income Ratio: This ratio compares your total monthly debt payments to your gross monthly income. A lower ratio indicates that you have more disposable income available to cover a new car payment, making you a less risky borrower.

Down Payment Size: As mentioned, a larger down payment reduces the loan amount and the lender’s risk, making you a more attractive applicant. It shows you have some savings and are serious about the purchase.

Employment History: A stable employment history, typically two years or more with the same employer, signals reliability. Frequent job changes can raise red flags for lenders, as it suggests potential income instability.

Vehicle Choice: The type of vehicle you choose can also influence approval. Lenders are often more comfortable financing a reliable, moderately priced used car than an expensive new luxury vehicle, especially for bad credit loans. The value of the car also serves as collateral.

From my perspective working with lenders, they are looking for mitigating factors. If your credit took a hit due to a medical emergency or a temporary job loss, and you can clearly demonstrate a return to stability, explain that to the lender. Transparency can build trust.

Understanding Loan Terms: Interest Rates, APR, and Loan Duration

Navigating the jargon of car loans is crucial, especially when dealing with bad credit. Understanding these terms will help you compare offers effectively and avoid costly mistakes.

Interest Rates: With bad credit, you should expect a higher interest rate than someone with excellent credit. This is how lenders compensate for the increased risk. The interest rate is the cost of borrowing money, expressed as a percentage of the principal.

APR vs. Interest Rate: This is a crucial distinction. The Annual Percentage Rate (APR) is the total cost of the loan over a year, including the interest rate and any additional fees (like origination fees). Always compare APRs when looking at different loan offers, as it gives you a truer picture of the total cost. Common mistakes to avoid are only looking at the advertised interest rate and ignoring the APR.

Loan Duration: This refers to the length of time you have to repay the loan, typically measured in months (e.g., 36, 48, 60, 72 months). A longer loan duration means lower monthly payments, but you’ll pay more in total interest over the life of the loan. A shorter duration means higher monthly payments but less total interest. For bad credit loans, lenders might push for longer terms to make payments more "affordable," but be aware of the increased total cost.

Fees and Charges: Be diligent about asking about all fees associated with the loan. These can include application fees, origination fees, documentation fees, and pre-payment penalties. Ensure every fee is itemized and explained before you sign anything.

Strategies for Improving Your Credit While Paying Off Your Loan

Securing a bad credit car loan in Detroit is not just about getting a car; it’s an opportunity to rebuild your credit. By making timely payments, you can significantly improve your credit score over the loan’s duration.

Make Payments On Time: This is the single most important factor. Payment history accounts for 35% of your FICO score. Every on-time payment demonstrates reliability to credit bureaus. Set up automatic payments to avoid missing due dates.

Keep Old Accounts Open: Even if they have a zero balance, old credit accounts contribute to your length of credit history, which is another factor in your score. Only close accounts if absolutely necessary.

Maintain Low Credit Utilization: Keep balances on credit cards and other revolving credit lines as low as possible, ideally below 30% of your credit limit. This shows you’re not over-reliant on credit.

Regularly Check Your Credit Report: Continue to monitor your credit reports for accuracy and to track your progress. You are entitled to a free report from each of the three major bureaus annually through AnnualCreditReport.com.

Pro Tips for Detroit Car Buyers with Bad Credit

Navigating the car buying process with bad credit requires a strategic approach. Here are some actionable tips:

- Do Your Research Thoroughly: Don’t rush into a purchase. Research dealerships that specialize in bad credit loans in Detroit. Look up reviews, check their Better Business Bureau ratings, and understand their reputation. Research the specific car models you’re interested in, including their reliability and fair market value.

- Get Pre-Approved: Seek pre-approval from several lenders (credit unions, online lenders, banks) before stepping onto a dealership lot. This gives you concrete offers to compare and strengthens your negotiating position. It also separates the financing from the car purchase, reducing pressure.

- Negotiate Wisely: Don’t just focus on the monthly payment. Negotiate the total price of the car, the trade-in value (if applicable), and the loan terms (APR, duration). Remember, the dealership makes money on both the car sale and the financing.

- Read the Fine Print: Never sign a contract without reading every single word. Understand all terms, conditions, fees, and penalties. If something is unclear, ask for clarification.

- Don’t Settle for the First Offer: Competition among lenders and dealerships can work in your favor. Be prepared to walk away if an offer doesn’t feel right or if you believe you can get a better deal elsewhere.

- Consider a Reliable Used Car: For bad credit loans, a reliable used car is often a more sensible choice than a new one. Used cars are less expensive, meaning you’ll need to borrow less, and they depreciate slower. Focus on cars known for their longevity and lower maintenance costs.

Common Pitfalls and How to Avoid Them

Even with the best intentions, certain traps can ensnare bad credit car buyers. Being aware of these can save you significant money and stress.

High-Pressure Sales Tactics: Dealerships sometimes use urgency or emotional appeals to push you into a deal. Stay firm, stick to your budget, and don’t be afraid to take a break or leave if you feel pressured.

Balloon Payments: Some loans might offer very low monthly payments initially, only to hit you with a massive "balloon payment" at the end of the loan term. Ensure your loan agreement does not include such a clause unless you are fully prepared for it.

Negative Equity (Upside Down Loan): This occurs when you owe more on your car than it’s worth. This can happen if you put little to no down payment, choose a very long loan term, or buy a car that depreciates quickly. If you need to sell or trade in the car, you’d still owe the difference. Aim for a substantial down payment to avoid this.

Scams and Predatory Lenders: Be wary of lenders promising "guaranteed approval" without any credit check, or those that pressure you into signing documents without explanation. Always verify the legitimacy of the lender and dealership. Check for proper licensing and look for reviews.

External Link Pro Tip: For more detailed information on your consumer rights when buying a car, including protections against unfair practices, consult resources from the Federal Trade Commission (FTC). Their website provides invaluable guidance on avoiding scams and understanding car-buying contracts.

Conclusion: Your Path to a Car in Detroit is Within Reach

Securing a bad credit car loan in Detroit may present challenges, but it is by no means an impossible feat. The Motor City offers numerous avenues for individuals with credit imperfections to find reliable transportation. With thorough research, careful preparation, and a strategic approach, you can navigate the process successfully.

Remember, your credit score is a reflection of your financial past, not necessarily your financial future. By being informed, transparent, and persistent, you can not only secure the car you need but also take significant steps toward rebuilding your credit for a stronger financial tomorrow. Don’t let past credit issues deter you from exploring your options. Equip yourself with knowledge, compare offers, and drive confidently toward your goal.

Ready to take the next step? Start by reviewing your credit report and exploring the various lending options available in Detroit. Your journey to owning a car, even with bad credit, begins with empowering yourself with the right information.