Navigating the Road Ahead: 9 Essential Insights for Securing Your Ideal Car Loan

Navigating the Road Ahead: 9 Essential Insights for Securing Your Ideal Car Loan Carloan.Guidemechanic.com

Embarking on the journey to purchase a new vehicle is undeniably exciting. The allure of a fresh set of wheels, the promise of new adventures, and the sheer convenience of personal transportation are powerful motivators. However, for most people, this journey inevitably leads to the critical intersection of financing – specifically, securing a car loan. Understanding the intricacies of auto loans isn’t just about getting approved; it’s about making an informed decision that saves you money, minimizes stress, and aligns with your long-term financial goals.

As an expert blogger and someone deeply entrenched in the world of automotive financing, I’ve seen firsthand how crucial it is for consumers to be well-prepared. Many common pitfalls can be easily avoided with the right knowledge. This comprehensive guide is designed to demystify the car loan process, transforming what might seem like a daunting task into a manageable and even empowering experience. We’ll delve deep into nine essential aspects of car loans, providing you with the insights and pro tips you need to confidently navigate the road to vehicle ownership.

Navigating the Road Ahead: 9 Essential Insights for Securing Your Ideal Car Loan

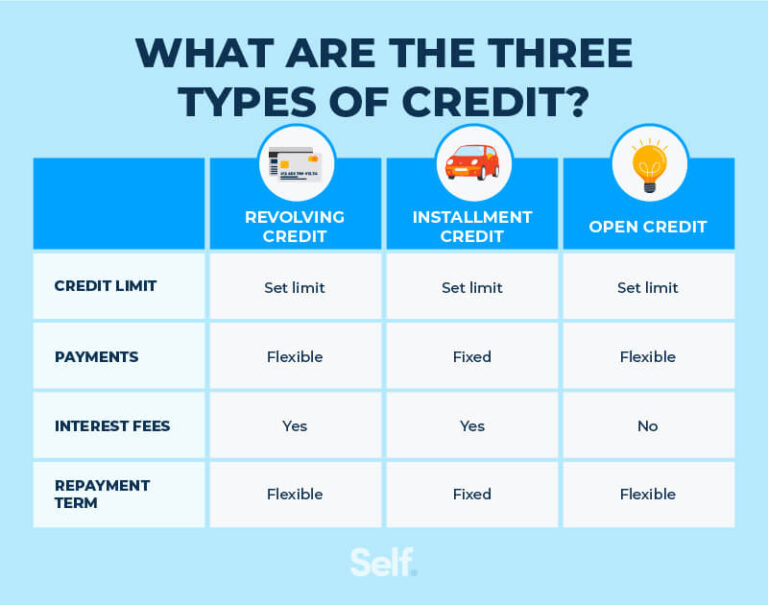

1. Understanding the Different Types of Car Loans Available

Not all car loans are created equal, and recognizing the distinctions is your first step towards making an educated choice. The type of loan you choose can significantly impact your interest rate, repayment terms, and even the vehicles you qualify for. It’s crucial to explore these options before you even step foot in a dealership.

Firstly, you’ll encounter the fundamental difference between new car loans and used car loans. Generally, new car loans tend to offer lower interest rates because the vehicle is brand new, depreciates predictably, and thus presents less risk to lenders. Used car loans, conversely, often come with slightly higher rates due to the inherent uncertainties of a pre-owned vehicle’s condition and history. Lenders perceive used cars as having a higher potential for mechanical issues, which could affect the borrower’s ability to repay.

Beyond new versus used, there’s the distinction between direct lending and dealership financing. Direct lending involves securing a loan directly from a bank, credit union, or online lender before you go shopping. This approach gives you significant leverage at the dealership because you arrive as a cash buyer, knowing exactly how much you can spend and what your interest rate will be. Dealership financing, on the other hand, means the dealership acts as an intermediary, arranging financing through various lenders they partner with. While convenient, this method might not always yield the best rates, as the dealership may add a markup to the interest rate to increase their profit. Pro tips from us: Always get pre-approved through a direct lender first; it gives you a benchmark for comparison.

Finally, most car loans are secured loans, meaning the vehicle itself serves as collateral. If you default on the loan, the lender has the right to repossess the car. Less common are unsecured personal loans used to purchase a vehicle; these typically have much higher interest rates because there’s no collateral backing the loan, making them riskier for the lender. Understanding these categories empowers you to seek out the loan type that best fits your financial situation and vehicle choice.

2. The Indispensable Role of Your Credit Score

Your credit score isn’t just a number; it’s a financial report card that profoundly influences the terms of your car loan. Lenders use this three-digit figure to assess your creditworthiness and predict your ability to repay debt. A higher credit score signals to lenders that you are a responsible borrower, making you eligible for more favorable interest rates and better loan terms.

Based on my experience, a strong credit score (typically FICO scores above 700) can translate into thousands of dollars in savings over the life of a car loan. Lenders offer their most competitive Annual Percentage Rates (APRs) to applicants with excellent credit because they represent a lower risk of default. Conversely, a lower credit score indicates a higher risk, leading lenders to charge higher interest rates to compensate for that perceived risk. This difference in interest rates can dramatically inflate your monthly payments and the total cost of the vehicle.

Improving your credit score before applying for a car loan is one of the smartest financial moves you can make. This involves consistently paying your bills on time, keeping your credit utilization low, and correcting any errors on your credit report. Even a modest improvement can make a noticeable difference in the loan offers you receive. Common mistakes to avoid are applying for multiple lines of credit simultaneously or closing old credit accounts, as these actions can temporarily lower your score. For a deeper dive into credit improvement, you might find our article on incredibly helpful. Taking the time to nurture your credit health will pay dividends when it comes to financing your next car.

3. The Power and Impact of a Down Payment

Making a down payment on your car loan is often overlooked but incredibly beneficial. It’s the initial sum of money you pay upfront towards the purchase price of the vehicle, reducing the amount you need to borrow. The size of your down payment directly impacts your loan terms, your monthly payments, and the overall cost of your financing.

A substantial down payment offers several significant advantages. Firstly, it immediately reduces your principal loan amount, which in turn lowers your monthly payments. This makes your car more affordable on a day-to-day basis and frees up cash flow for other expenses. Secondly, a larger down payment demonstrates financial stability to lenders, potentially qualifying you for lower interest rates. It signals that you have a vested interest in the vehicle and are less likely to default on the loan.

Moreover, a generous down payment helps combat the immediate depreciation a new car experiences. As soon as a new car drives off the lot, its value drops significantly. If you finance 100% of the vehicle’s price, you could quickly find yourself "upside down" on your loan, meaning you owe more than the car is worth. This situation, known as negative equity, can create problems if you need to sell or trade in the car before the loan is paid off. Pro tips from us: Aim for at least a 10-20% down payment on a new car and ideally 10% on a used car to build immediate equity and secure better terms. While it might require saving up, the long-term financial benefits are well worth the wait.

4. Decoding Loan Terms and Interest Rates (APR)

When you’re comparing car loan offers, two critical factors demand your closest attention: the loan term and the Annual Percentage Rate (APR). Understanding how these elements interact is essential for making a financially sound decision. Misjudging either can lead to higher costs or uncomfortable monthly payments.

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). While a longer loan term might seem appealing because it reduces your monthly payment, it comes with a significant trade-off. You’ll end up paying more in total interest over the life of the loan. Conversely, a shorter loan term means higher monthly payments but substantially less paid in interest overall. Common mistakes to avoid are extending the loan term purely to achieve a lower monthly payment without considering the total cost implications.

The Annual Percentage Rate (APR) is perhaps the most crucial number to scrutinize. It represents the true cost of borrowing money, encompassing not only the interest rate but also any other fees associated with the loan. A lower APR directly translates to less money paid in interest over the loan’s duration. Based on my experience, comparing APRs from different lenders is the most effective way to find the best deal. Don’t just look at the monthly payment; always ask for and compare the total APR. This comprehensive figure allows for an apples-to-apples comparison between different financing offers, ensuring you truly understand the cost of your vehicle financing.

5. Navigating the Car Loan Application and Approval Process

The car loan application and approval process can feel like a maze, but with the right preparation, it becomes a straightforward path. Knowing what to expect and having your documents in order will significantly streamline the experience and increase your chances of securing a favorable loan. Lenders look for stability and reliability in potential borrowers.

To begin, you’ll typically need to provide personal identification, proof of income, and residency verification. This usually includes a valid driver’s license, recent pay stubs or tax returns, and utility bills or lease agreements. Lenders want to confirm your identity, assess your ability to make regular payments, and verify your address. Having these documents readily available will prevent delays. From years of observing the automotive financing landscape, I can tell you that incomplete applications are a major reason for hold-ups.

Once you submit your application, the lender will perform a hard inquiry on your credit report. This allows them to evaluate your credit history, payment behavior, and existing debt obligations. They’ll then use this information, along with your income and debt-to-income ratio, to determine your loan eligibility, the interest rate they can offer, and the maximum amount you can borrow. Be prepared for a decision within minutes or a few business days, depending on the lender. Pro tips from us: Always review your credit report for inaccuracies before applying. Understanding your credit standing beforehand allows you to anticipate potential challenges and address them proactively, smoothing out the entire car loan approval process.

6. Securing a Car Loan with Less-Than-Perfect Credit

The idea of getting a car loan with a low credit score can be daunting, but it’s far from impossible. While you might not qualify for the absolute lowest interest rates, there are viable options and strategies available to help you secure the financing you need. The key is to be realistic, proactive, and explore all avenues.

One common strategy for individuals with bad credit car loan needs is to work with lenders who specialize in subprime auto lending. These lenders are more willing to take on higher-risk borrowers, though they will typically charge higher interest rates to offset that risk. It’s crucial to shop around, even with a lower score, as different subprime lenders will offer varying terms. Don’t just take the first offer you receive; compare as many as possible.

Another effective approach is to make a larger down payment. As discussed earlier, a substantial down payment reduces the amount you need to borrow and signals to lenders that you are serious about your commitment. Having a co-signer with good credit can also significantly improve your chances of approval and help you secure a better interest rate. The co-signer essentially guarantees the loan, taking on responsibility if you default. Common mistakes to avoid are accepting excessively long loan terms (e.g., 84 months) just to get a lower monthly payment, as this dramatically increases the total interest paid and leaves you with negative equity for longer. Focus on proving your ability to repay responsibly, and over time, you can even look into refinancing once your credit score improves.

7. Uncovering Hidden Costs and Fees to Watch Out For

While the advertised price of a car and its loan interest rate are significant, they don’t always tell the whole story. Many car loans come with additional costs and fees that can subtly inflate your total expenditure. Being aware of these potential extras is crucial for accurate budgeting and preventing unpleasant surprises.

One common fee is the origination fee, which lenders charge for processing the loan application. While not all lenders impose this, it’s something to ask about upfront. Another often-overlooked cost is the prepayment penalty. Some loans include clauses that charge you a fee if you pay off your loan early. This is designed to compensate the lender for the interest income they lose. Based on my experience, always ask if there are prepayment penalties, especially if you anticipate paying off your loan ahead of schedule.

Beyond loan-specific fees, dealerships often try to upsell various add-ons and extended warranties. These can include gap insurance, paint protection, fabric sealant, or service contracts. While some might offer legitimate value (like gap insurance, which covers the difference between your car’s value and what you owe if it’s totaled), many are overpriced and unnecessary. Pro tips from us: Always scrutinize every line item on the sales contract. Never feel pressured to accept add-ons you don’t fully understand or believe you need. Remember, you can often purchase extended warranties or gap insurance from third-party providers at a much lower cost. Understanding all the potential costs associated with car ownership, including these hidden fees, is vital for your financial health. You might find more details on this in our guide to .

8. The Strategic Move of Refinancing Your Car Loan

Refinancing your car loan means replacing your existing loan with a new one, typically with more favorable terms. This strategic financial maneuver can save you a substantial amount of money over the life of your loan and is an option many car owners overlook. It’s not just for those struggling; even if you’re comfortable with your current payments, there might be a better deal out there.

One of the primary reasons to consider refinancing your car loan is to secure a lower interest rate. If your credit score has improved significantly since you first took out the loan, or if market interest rates have dropped, you might qualify for a much better APR. A lower interest rate translates directly to less money paid in interest and lower monthly payments, freeing up your budget. For example, reducing your APR by even a couple of percentage points can save hundreds, if not thousands, over the loan term.

Another reason to refinance might be to adjust your monthly payments. If your financial situation has changed, you could opt for a longer loan term to reduce your monthly outlay (though be mindful of increased total interest). Conversely, if you’ve had a salary increase, you might choose a shorter term to pay off the loan faster and save on interest. Pro tips from us: Don’t wait too long to refinance. The sweet spot is usually when you still owe a significant amount on the car but before its value depreciates too much. Common mistakes to avoid are refinancing without first comparing offers from multiple lenders, as you might miss out on the best possible deal. Always do your homework and calculate the potential savings before committing to a new loan.

9. Expert Tips for Landing the Best Car Loan Deal

Securing the best possible car loan deal isn’t about luck; it’s about preparation, knowledge, and strategic negotiation. Arming yourself with the right information and approach can significantly impact your financial outcome. Having guided countless individuals through this process, I’ve compiled essential car loan tips that consistently yield superior results.

Firstly, get pre-approved by multiple lenders before you even start serious car shopping. This is arguably the most powerful tool in your arsenal. Pre-approval gives you a firm offer with a specific interest rate and loan amount, transforming you into a cash buyer at the dealership. You’ll know your maximum budget and the lowest interest rate you qualify for, which serves as a benchmark. If the dealership offers a higher rate, you have leverage to negotiate or walk away.

Secondly, focus on the total cost, not just the monthly payment. While a low monthly payment is appealing, a longer loan term or a higher interest rate can make your car significantly more expensive in the long run. Always ask for the total amount you’ll pay over the life of the loan. This comprehensive figure provides the clearest picture of the actual cost of your financing. Common mistakes to avoid are letting the salesperson distract you with low monthly payments without revealing the true interest rate or extended term.

Finally, negotiate everything, and be ready to walk away. This applies to both the car’s price and the loan terms. Dealerships have flexibility, but they won’t offer their best deal unless you push for it. Don’t be afraid to compare offers from different dealerships and lenders. Your willingness to walk away is your ultimate bargaining chip. Remember, patience and thorough research are your best allies in securing the ideal car loan that fits your budget and financial goals. For more detailed advice, you can consult trusted resources like the Consumer Financial Protection Bureau’s guide on auto loans at – an excellent external resource for all things auto financing.

Conclusion: Driving Towards Financial Confidence

Navigating the world of car loans might initially seem complex, but by understanding these nine essential aspects, you’re now equipped with the knowledge to make informed, strategic decisions. From discerning between various loan types and understanding the profound impact of your credit score to wisely managing down payments, deciphering APRs, and meticulously reviewing hidden fees, each insight empowers you to approach vehicle financing with confidence.

Remember, the goal isn’t just to get a car; it’s to secure a car on terms that genuinely benefit your financial well-being. By applying these expert tips – getting pre-approved, focusing on total cost, and being prepared to negotiate – you’re setting yourself up for success. This comprehensive guide serves as your roadmap, ensuring that your journey to car ownership is not only exciting but also financially sound and stress-free. Drive smart, and drive confidently!