Navigating the Road Ahead: A Comprehensive Guide to Active Duty Car Loans

Navigating the Road Ahead: A Comprehensive Guide to Active Duty Car Loans Carloan.Guidemechanic.com

Embarking on a new chapter, whether it’s your first duty station or a fresh deployment, often brings with it the excitement of new experiences. For many active duty service members, a reliable vehicle is not just a convenience; it’s a necessity for daily life, commuting to base, or exploring new surroundings. However, securing a car loan while serving can present a unique set of challenges and opportunities that differ significantly from civilian financing.

This ultimate guide is designed to be your go-to resource for understanding Active Duty Car Loans. We’ll delve deep into everything you need to know, from finding military-friendly lenders to understanding your financial rights and avoiding common pitfalls. Our goal is to empower you with the knowledge to make informed decisions, ensuring you drive away with a great deal and peace of mind.

Navigating the Road Ahead: A Comprehensive Guide to Active Duty Car Loans

Understanding the Unique Financial Landscape of Active Duty Service Members

The financial lives of active duty personnel are distinct. While a steady income, often supplemented by allowances like Basic Allowance for Housing (BAH) and Basic Allowance for Subsistence (BAS), provides stability, the lifestyle also involves frequent relocations (Permanent Change of Station or PCS) and potential deployments. These factors play a crucial role in how lenders view your creditworthiness and the types of military car loans available to you.

Frequent moves can sometimes make it harder to establish a consistent credit history, especially if you’re new to the service or moving across state lines regularly. Additionally, deployments can complicate the logistics of managing finances and making big purchases like a car. Understanding these nuances is the first step toward smart auto financing.

Why Active Duty Service Members Need Specialized Car Loan Advice

The unique circumstances of active duty service members can make them targets for less scrupulous lenders, especially those operating near military installations. These "buy here, pay here" lots or high-interest lenders often prey on service members who might have limited credit history or feel pressured to get a vehicle quickly. Without proper guidance, it’s easy to fall into a high-interest trap that can impact your financial health for years.

Based on my experience working with countless service members, specialized advice isn’t just helpful; it’s essential. Knowing your rights, understanding military-specific protections, and identifying truly military-friendly lenders can save you thousands of dollars and significant stress. We aim to equip you with the knowledge to navigate this complex landscape confidently.

Key Factors Lenders Consider for Active Duty Car Loans

When you apply for an auto loan for military personnel, lenders assess several critical factors to determine your eligibility and interest rate. Understanding these can help you prepare and present yourself as a low-risk borrower.

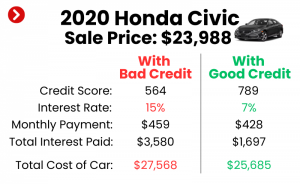

Your Credit Score: The Foundation of Your Loan

Your credit score is a numerical representation of your creditworthiness. A higher score indicates a lower risk to lenders, typically translating to better interest rates and terms. Many service members, especially those fresh out of basic training, might have a limited credit history, which can make securing favorable rates challenging.

It’s vital to understand that a low or non-existent credit score doesn’t automatically disqualify you, but it might mean a higher interest rate initially. Pro tips from us: actively work on building good credit well before you need a car loan. For a deeper dive into improving your credit score, check out our guide on .

Income Stability and Employment Verification

Active duty service members generally benefit from stable employment and a consistent income stream. Lenders appreciate this reliability. You’ll typically need to provide proof of employment, such as your Leave and Earnings Statement (LES), and demonstrate that your income can comfortably cover the monthly car payment along with your other expenses.

Your BAH and BAS allowances are often considered as part of your total income, which can significantly boost your borrowing power. Ensure you have recent LES statements ready when you apply.

Time in Service and Deployment Status

Some lenders view longer time in service as an indicator of stability and commitment, which can be favorable. Your deployment status can also be a factor. While lenders are generally supportive, they may ask about your plans for the vehicle during a deployment to ensure the loan will be managed responsibly.

Having a plan in place for car payments and maintenance during deployment can reassure lenders. Consider designating a trusted individual with Power of Attorney to handle financial matters if you’ll be out of communication.

Debt-to-Income Ratio: Balancing Your Books

Your debt-to-income (DTI) ratio compares your total monthly debt payments to your gross monthly income. Lenders use this to gauge your ability to take on additional debt. A lower DTI ratio indicates you have more disposable income available to manage new payments.

Common mistakes to avoid are taking on too much debt before applying for a car loan. Try to pay down credit card balances or other outstanding loans to improve your DTI ratio before seeking financing.

The Power of a Down Payment

A significant down payment reduces the amount you need to borrow, which can lower your monthly payments and the total interest paid over the life of the loan. It also shows lenders you are serious about your purchase and have good financial habits.

Based on my experience, even a modest down payment of 10-20% can make a substantial difference in loan approval and terms, especially if your credit history is limited. It reduces the lender’s risk and can lead to more favorable interest rates.

Types of Lenders & Where to Find Them for Active Duty Car Loans

Not all lenders are created equal, especially when it comes to serving active duty military personnel. Knowing where to look can make all the difference in securing the best possible terms for your financing for active duty vehicle.

Military-Friendly Banks & Credit Unions

These institutions often have a deep understanding of the military lifestyle and offer products specifically tailored for service members.

- USAA and Navy Federal Credit Union: These are often the first choice for many service members, known for their competitive rates, flexible terms, and military-specific financial advice. They understand PCS moves, deployments, and the unique pay structure.

- Local Credit Unions Near Bases: Many credit unions located near military installations have strong ties to the community and offer excellent car loans for service members with competitive rates and personalized service. They often have programs to help those with limited credit history.

Traditional Banks

Large national banks also offer car loans, and while they may not have military-specific programs, they can be a good option if you have a strong credit history. It’s always worth comparing their rates with military-focused institutions.

Always read the fine print and compare Annual Percentage Rates (APRs) carefully. Don’t assume a lower monthly payment always means a better deal overall.

Dealership Financing: Proceed with Caution

Dealerships often offer their own financing options or work with a network of lenders. While convenient, it’s crucial to be wary. Some dealerships near military bases have a reputation for predatory practices, offering high-interest loans to service members who may be less informed.

Pro tips from us: never rely solely on dealership financing. Always get pre-approved elsewhere first, so you have a benchmark for comparison. This empowers you to negotiate better terms.

Online Lenders

A growing number of online lenders specialize in auto loans. They offer convenience and can provide competitive rates. However, ensure the lender is reputable and transparent about all fees and terms.

Look for lenders with strong reviews and clear disclosures. Be cautious of any lender promising guaranteed approval without checking your credit or employment.

Special Programs & Benefits for Active Duty Car Loans

Beyond standard lending options, active duty service members have access to certain protections and potential benefits that can impact their car loan experience.

The Servicemembers Civil Relief Act (SCRA)

While not a direct car loan program, the SCRA is a critical piece of legislation that protects service members from certain financial obligations during active duty. It allows you to reduce interest rates on pre-service debt to 6% under specific circumstances and provides protections against repossessions without a court order.

Understanding your SCRA rights is paramount. It’s a powerful tool that can provide financial relief and protection. If you’re interested in learning more about the Servicemembers Civil Relief Act, we have an extensive article dedicated to .

Guaranteed Asset Protection (GAP) Insurance

GAP insurance is particularly relevant for service members. If your vehicle is totaled or stolen, and you owe more on the loan than the car’s actual cash value, GAP insurance covers the difference. Given that military personnel often drive off-base and can face unique storage challenges during deployment, this coverage offers vital protection.

Common mistakes to avoid include skipping GAP insurance, especially if you put down a small down payment or financed a significant portion of the vehicle’s value. It’s a small cost for potentially large protection.

Manufacturer Incentives

Many auto manufacturers offer special discounts or rebates for active duty military personnel. These incentives can range from a few hundred dollars off the purchase price to preferred financing rates. Always ask about military discounts when you’re shopping for a new vehicle.

These programs are often advertised on the manufacturer’s website or at the dealership. Don’t be shy about inquiring; it’s a benefit you’ve earned.

The Application Process: A Step-by-Step Guide

Navigating the application process for active duty car loans doesn’t have to be daunting. Following a structured approach can save you time, money, and stress.

1. Get Pre-Approved First

This is perhaps the most crucial step. Getting pre-approved for a loan before you even set foot in a dealership gives you a clear understanding of how much you can afford and the interest rate you qualify for. This empowers you to negotiate the car price as a cash buyer, rather than focusing on monthly payments.

Based on my experience, pre-approval removes the financing mystery and allows you to concentrate on getting the best deal on the vehicle itself. It also helps you resist pressure from dealership finance departments.

2. Gather Your Documents

Lenders will require specific documentation to verify your identity, income, and military status.

- Proof of Identity: Driver’s license, military ID.

- Proof of Income: Recent Leave and Earnings Statement (LES), pay stubs.

- Proof of Residence: Utility bill, lease agreement.

- Military Orders: If applicable, especially for PCS or deployment.

- Credit Report: While lenders will pull it, it’s good practice to review yours beforehand.

Having these documents organized and ready will streamline the application process.

3. Understand the Loan Terms

Before signing anything, meticulously review the loan agreement. Pay close attention to:

- Annual Percentage Rate (APR): This is the true cost of borrowing, including interest and fees.

- Loan Term: The length of the loan (e.g., 60, 72, 84 months). Longer terms mean lower monthly payments but more interest paid overall.

- Total Loan Cost: Calculate the total amount you’ll pay over the life of the loan.

- Prepayment Penalties: Ensure there are no fees for paying off your loan early.

Common mistakes to avoid are rushing through the paperwork and not asking questions if something is unclear. It’s your right to understand every clause.

Common Mistakes Active Duty Service Members Make When Getting a Car Loan

Even with the best intentions, service members can inadvertently make decisions that cost them money or lead to frustration. Here are some common pitfalls to avoid.

Not Shopping Around for the Best Loan

Settling for the first loan offer you receive, especially from a dealership, is a common and costly mistake. Always compare offers from multiple lenders – military credit unions, traditional banks, and online lenders.

Pro tips from us: Treat car loan shopping like you would any other significant purchase. Get at least three different quotes to ensure you’re getting a competitive rate.

Focusing Only on the Monthly Payment

While the monthly payment is important for budgeting, it shouldn’t be your sole focus. A low monthly payment can often be achieved by extending the loan term, which means you pay significantly more in interest over time.

Instead, consider the total cost of the loan and your ability to comfortably afford the payment without stretching your budget too thin.

Buying More Car Than You Can Afford

It’s tempting to want the latest model or a luxury vehicle, but purchasing a car that’s beyond your means can lead to financial strain. Remember to factor in not just the loan payment, but also insurance, maintenance, fuel, and registration costs.

Based on my experience, a general rule of thumb is that your total car-related expenses (payment, insurance, gas, maintenance) shouldn’t exceed 10-15% of your net monthly income.

Falling for High-Pressure Sales Tactics

Some dealerships near military bases are notorious for aggressive sales tactics. They might try to rush you into a decision, add unnecessary extras, or push high-interest loans. Don’t succumb to pressure.

You have the right to take your time, review documents, and walk away if you feel uncomfortable. A reputable dealer will respect your decision-making process.

Ignoring the Annual Percentage Rate (APR)

The APR is the real measure of your loan’s cost. A seemingly low monthly payment with a high APR means you’re paying a lot more in interest. Always compare APRs when evaluating loan offers.

Common mistakes include being distracted by a low monthly payment and overlooking a high APR, which significantly increases the total cost of your vehicle.

Not Checking Your Credit Report Regularly

Errors on your credit report can negatively impact your credit score, leading to higher interest rates. It’s crucial to check your credit report annually from all three major bureaus (Experian, Equifax, and TransUnion) for inaccuracies. You can get free copies at AnnualCreditReport.com.

Catching and disputing errors can significantly improve your credit standing and, consequently, your loan terms.

Pro Tips for Securing the Best Active Duty Car Loan

Equipped with knowledge about potential pitfalls, let’s now focus on strategies to ensure you get the absolute best deal on your next vehicle.

Build Good Credit Early and Consistently

Start building a positive credit history as soon as possible. Open a secured credit card or a small loan, make all payments on time, and keep your credit utilization low. This proactive approach will pay dividends when you need a car loan.

A strong credit profile is your best asset for securing low interest rates on best car loans for military.

Save for a Substantial Down Payment

As discussed, a larger down payment reduces your loan amount, lowers monthly payments, and can secure better interest rates. Aim for at least 10-20% of the vehicle’s purchase price.

The more you can put down upfront, the less risk the lender takes on, and the more favorable your loan terms are likely to be.

Get Pre-Approved Before You Shop

This cannot be stressed enough. Pre-approval from a military-friendly lender gives you leverage and clarity. It separates the car-buying process from the financing process, allowing you to focus on getting a fair price for the vehicle.

It’s like having cash in hand; you know your spending limit and won’t be swayed by unfavorable dealer financing.

Understand Your Budget Beyond the Payment

Before you even start looking at cars, create a comprehensive budget. Include not only the potential car payment but also estimated costs for insurance (which can be higher for younger service members), fuel, maintenance, and registration.

Pro tips from our team of military finance experts: Use a budget planner to visualize your entire financial picture. This prevents "payment shock" once you’ve made your purchase.

Read Every Line of the Fine Print

Never sign a document you haven’t thoroughly read and understood. If anything is unclear, ask for clarification. Don’t let anyone rush you through the signing process.

This includes all terms and conditions, warranties, and any additional fees. Knowledge is your best defense against unfavorable terms.

Negotiate Everything, Not Just the Price

Negotiate the purchase price of the car, the value of your trade-in (if any), and the interest rate. Remember, everything is negotiable.

Be prepared to walk away if the terms aren’t right. There are always other vehicles and other lenders.

Consider a Reliable Used Car

Especially for service members who may face frequent PCS moves or deployments, a reliable used car can be a more practical and financially sound option than a brand-new vehicle. Depreciation hits new cars hardest in the first few years.

A certified pre-owned (CPO) vehicle from a reputable dealership can offer a good balance of reliability, warranty coverage, and lower cost.

Navigating Car Ownership During Deployment & PCS

The military lifestyle often means being prepared for the unexpected, and that includes managing your vehicle during deployments or PCS moves.

Storage Options During Deployment

If you’re deploying and can’t take your vehicle, research secure storage options. Some military bases offer long-term storage, or you might consider a trusted family member’s garage. Ensure the car is properly prepared for storage (battery disconnected, tires inflated, fluid levels checked).

Don’t forget to adjust your insurance coverage during storage to save money, but ensure it still covers fire, theft, or other non-driving incidents.

Shipping Vehicles for PCS

During a PCS, you might have the option to ship one vehicle at the government’s expense, depending on your orders. Research the official military transportation office guidelines and compare them with commercial shipping options.

Understanding the timelines and requirements for vehicle shipping can save you significant headaches and costs during a PCS.

Utilizing a Power of Attorney

If you’re deploying or moving overseas, consider granting a trusted individual a General or Special Power of Attorney (POA) to handle your vehicle-related matters. This could include making payments, authorizing maintenance, or even selling the car if necessary.

Ensure the POA is legally sound and clearly outlines the scope of authority granted.

SCRA Benefits and Your Vehicle

Remember, the SCRA offers protections if you are unable to make payments due to deployment or military service. You may be able to request a reduction in interest rates on pre-service loans or protections against repossession. Consult with a legal assistance officer on base for guidance.

These benefits are designed to protect you, so know how and when to leverage them.

Conclusion: Drive Confidently with Active Duty Car Loans

Securing an Active Duty Car Loan doesn’t have to be a source of stress. By understanding your unique financial standing as a service member, knowing where to find military-friendly lenders, and being aware of common pitfalls, you can navigate the process with confidence and clarity. The road ahead, whether it’s to your next duty station or a weekend adventure, should be smooth and worry-free.

Remember to leverage your military benefits, shop around for the best rates, and never hesitate to ask questions. Your service to our country deserves the best possible financial treatment. Drive smart, drive safe, and enjoy the journey! For more financial literacy resources tailored for service members, visit trusted external sources like Military OneSource or the Consumer Financial Protection Bureau (CFPB).