Navigating the Road Ahead: A Comprehensive Guide to Car Loans for Disabled Veterans with Bad Credit

Navigating the Road Ahead: A Comprehensive Guide to Car Loans for Disabled Veterans with Bad Credit Carloan.Guidemechanic.com

For disabled veterans, owning a reliable vehicle isn’t just a convenience; it’s often a necessity for independence, medical appointments, and connecting with the community. However, the path to securing a car loan can seem daunting, especially when navigating the complexities of bad credit. Many assume their credit history is an insurmountable barrier, but based on my extensive experience in financial guidance and SEO content, this is far from the truth.

This in-depth guide is designed to empower disabled veterans with bad credit, offering clear, actionable insights into securing a car loan. We’ll explore specialized programs, effective strategies, and the vital steps you can take to drive off the lot with confidence. Our ultimate goal is to provide you with a comprehensive roadmap, ensuring you understand every available option and how to leverage your unique veteran status.

Navigating the Road Ahead: A Comprehensive Guide to Car Loans for Disabled Veterans with Bad Credit

The Unique Landscape for Disabled Veterans: More Than Just a Credit Score

Serving our country comes with immense sacrifices, and for many disabled veterans, these sacrifices can unfortunately extend to financial challenges. Medical expenses, periods of unemployment or underemployment, and the sheer effort of transitioning back to civilian life can all impact credit scores. It’s crucial to understand that your credit history doesn’t define your worth or your ability to secure a loan.

Lenders often view disabled veterans differently, recognizing the stability that VA disability compensation can provide. This consistent income stream, coupled with various veteran-specific programs, can significantly open doors that might otherwise appear closed due to past credit issues. Your service and unique circumstances are powerful factors that can be leveraged in your favor.

Unpacking "Bad Credit": Why It’s Not a Dead End for Car Loans

The term "bad credit" often conjures images of rejection and closed doors. In simple terms, it typically means your credit score falls below a certain threshold, usually indicating a higher risk to lenders. Factors like missed payments, high debt, or even limited credit history can contribute to a lower score. However, for a car loan for disabled veterans with bad credit, this label doesn’t automatically mean "no."

Based on my experience working with numerous individuals in similar situations, many believe that a poor credit history automatically slams the door shut on significant financial endeavors like car loans. This simply isn’t the case. While bad credit might mean different loan terms or a higher interest rate, it certainly doesn’t eliminate your options. Many lenders specialize in what are known as "subprime" loans, specifically designed for individuals with less-than-perfect credit.

Essential Financial Assistance & Programs for Disabled Veterans

One of the most significant advantages disabled veterans have is access to specific government and non-profit programs designed to support their unique needs. Understanding and utilizing these can dramatically improve your chances of securing an affordable car loan.

VA Adaptive Automotive Assistance Program

This is a cornerstone benefit for many disabled veterans. The U.S. Department of Veterans Affairs (VA) provides grants to eligible disabled veterans for the purchase of a new or used automobile or other conveyance. Crucially, these grants can also cover adaptive equipment necessary to make the vehicle accessible, such as power steering, power brakes, power windows, or even a modified van.

To qualify, veterans generally need to have a service-connected disability that prevents them from operating a vehicle without special equipment, or makes it impossible to enter or exit a standard vehicle. The grant amount is typically a one-time payment. It’s not a loan, but rather a direct financial contribution that can significantly reduce the overall cost of the vehicle, thereby lowering the amount you need to finance and making a loan more manageable. This is a critical first step for many.

Leveraging VA Disability Compensation as Stable Income

Your VA disability compensation is a powerful asset when applying for a car loan. Unlike some other forms of income, it is generally tax-free and incredibly stable. Lenders view consistent, reliable income very favorably, as it demonstrates your ability to make regular loan payments. Even with bad credit, a strong, verifiable income stream from your VA benefits can significantly mitigate perceived risk.

When preparing your loan application, always highlight your VA disability compensation. Provide official documentation from the VA clearly stating your monthly benefit amount. This robust proof of income often outweighs some of the negative aspects of a low credit score in the eyes of many lenders, especially those experienced in veteran financing.

Exploring State-Specific Veteran Programs and Non-Profits

Beyond federal initiatives, many states offer their own veteran assistance programs that might include vehicle-related aid or financial counseling. These programs vary widely by location, so it’s essential to research what’s available in your specific state or county. A quick search for "veteran car assistance " can often yield valuable results.

Furthermore, a multitude of non-profit organizations are dedicated to assisting veterans. Groups like the Disabled American Veterans (DAV), the American Legion, and various local veteran charities often provide financial grants, transportation assistance, or help connecting veterans with resources. While they might not directly offer car loans, their support can free up funds for a down payment or provide crucial financial advice.

Navigating the Loan Application Process with Bad Credit: A Step-by-Step Guide

Securing a car loan with bad credit requires a strategic approach. It’s not about hoping for the best; it’s about preparing thoroughly and knowing where to look.

Step 1: Assess Your Current Financial Situation

Before you even think about visiting a dealership, take an honest look at your finances. Create a detailed budget that includes all your income sources (VA disability, employment, etc.) and all your monthly expenses. This will help you determine how much you can realistically afford for a car payment, insurance, fuel, and maintenance without stretching yourself too thin.

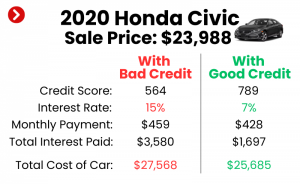

Pro Tip from us: While it’s tempting to focus solely on the monthly payment, always calculate the total cost of the loan over its entire term. A lower monthly payment might come with a much longer term and significantly more interest paid overall. Understanding your debt-to-income ratio (DTI) is also crucial; this is the percentage of your gross monthly income that goes toward paying your monthly debt payments. Lenders prefer a lower DTI, typically below 43%.

Step 2: Check Your Credit Score and Report

Knowing your credit standing is the first step toward improving it and understanding what lenders will see. Obtain a copy of your credit report from all three major bureaus: Experian, Equifax, and TransUnion. You can get free copies annually at AnnualCreditReport.com (this is an external link to a trusted source for credit reports). Review these reports meticulously for any errors or inaccuracies.

Disputing errors can potentially boost your score quickly. Furthermore, understanding the factors contributing to your low score will help you address them. A credit score is a snapshot of your financial reliability, and knowing its details empowers you to speak confidently with lenders.

Step 3: Gather All Necessary Documentation

Preparation is key. Lenders will require specific documents to verify your identity, income, and veteran status. Having these ready will streamline the application process and demonstrate your seriousness.

You’ll typically need:

- Proof of Income: VA disability letters, recent pay stubs (if employed), tax returns.

- Proof of Residency: Utility bills, lease agreements.

- Identification: Driver’s license, military ID, VA ID card.

- VA Disability Rating Letter: Clearly stating your service-connected disability and rating.

- Bank Statements: To show financial stability and cash flow.

- List of References: Sometimes requested for subprime loans.

Step 4: Explore Your Loan Options Strategically

Not all lenders are created equal, especially when it comes to bad credit and veteran-specific needs. Targeting the right institutions is vital.

- Specialized Lenders for Bad Credit (Subprime Lenders): Many financial institutions focus specifically on helping individuals with low credit scores. These lenders understand the risks but are willing to work with borrowers who demonstrate stable income. They often have more flexible criteria than traditional banks.

- Credit Unions: Often veteran-friendly, credit unions are member-owned and tend to offer more personalized service and potentially more flexible lending terms than larger banks. If you’re a member of a credit union or eligible to join one (many serve specific communities or professions, including military), they can be an excellent option.

- Dealership Financing: Many dealerships have financing departments that work with a network of lenders, including those specializing in bad credit. While convenient, always compare their offers with pre-approvals you might receive elsewhere to ensure you’re getting a competitive rate.

- Co-Signers: If you have a trusted family member or friend with good credit who is willing to co-sign, this can significantly improve your chances of approval and potentially secure a lower interest rate. Be aware that a co-signer is equally responsible for the loan, so both parties must understand the commitment.

- Secured Loans: In some cases, you might be offered a secured loan where you use an asset (like savings) as collateral. While this can make approval easier, it also carries the risk of losing that asset if you default on the loan. Proceed with caution.

Strategies to Improve Your Chances of Approval

Even with bad credit, there are proactive steps you can take to make your application more appealing to lenders.

- Offer a Larger Down Payment: Putting down a significant portion of the car’s price reduces the amount you need to borrow, thereby lowering the lender’s risk. This can often sway a lender, even with a less-than-perfect credit score.

- Show Stable Income: Reiterate the reliability of your VA disability compensation. If you also have employment, highlight its stability and duration. Lenders prioritize consistent income that can cover monthly payments.

- Choose the Right Vehicle: Opt for a reliable, affordable vehicle that fits within your budget. Lenders are more comfortable financing a reasonably priced car than an expensive luxury model when dealing with bad credit.

- Get Pre-Approved: Seek pre-approval from several lenders before you step foot in a dealership. This gives you a clear idea of how much you can borrow, at what interest rate, and empowers you to negotiate confidently for the car you want.

- Common mistakes to avoid include applying to too many lenders simultaneously, which can negatively impact your credit score due to multiple hard inquiries. Instead, aim for pre-approvals from a few selected lenders within a short timeframe (usually 14-45 days), as these are often counted as a single inquiry.

Understanding Loan Terms and Avoiding Pitfalls

Securing the loan is only half the battle; understanding its terms is crucial to avoid financial distress down the line.

- Interest Rates: With bad credit, you should expect a higher interest rate than someone with excellent credit. This is how lenders mitigate their increased risk. However, don’t settle for the first offer. Compare rates from multiple lenders. Even a percentage point difference can save you hundreds, if not thousands, over the life of the loan.

- Loan Length (Term): While a longer loan term (e.g., 72 or 84 months) might offer lower monthly payments, it almost always means you’ll pay significantly more in total interest. Aim for the shortest loan term you can comfortably afford to minimize the overall cost of the vehicle.

- Fees: Be aware of potential fees like origination fees, documentation fees, or processing fees. Always ask for a full breakdown of all costs associated with the loan before signing any agreement.

- Hidden Clauses: Always read the fine print of any loan agreement. Understand prepayment penalties (if any), late payment charges, and what happens in case of default. Pro Tip: Don’t rush into signing anything; take the document home, review it carefully, and ask questions about anything you don’t understand.

Beyond the Loan: Building a Stronger Financial Future

Securing a car loan for disabled veterans with bad credit is a significant achievement, but it’s also an opportunity to build a stronger financial foundation for the future.

Strategies for Credit Building

Your new car loan, if managed responsibly, can be a powerful tool for rebuilding your credit.

- Make On-Time Payments: This is the most critical factor in improving your credit score. Set up automatic payments to ensure you never miss a due date.

- Keep Other Accounts Current: Ensure all your other bills – credit cards, utilities, rent – are paid on time.

- Consider a Secured Credit Card: If you don’t have active credit cards, a secured card (backed by a cash deposit) can help build a positive payment history.

- Credit Counseling: Non-profit credit counseling agencies can provide personalized advice and help you create a debt management plan.

For more in-depth advice on improving your financial standing, you might find our guide on Budgeting for Veterans: Maximizing Your Benefits incredibly helpful. It offers practical strategies for managing your money effectively and setting long-term financial goals.

Budgeting and Financial Planning

Long-term financial stability comes from smart budgeting and planning. Continuously monitor your income and expenses, and look for opportunities to save. Even small, consistent savings can add up and provide a crucial financial cushion for unexpected expenses. Understanding your financial habits will empower you to make better choices and avoid future credit pitfalls.

Additionally, choosing the right vehicle that aligns with your needs and budget is paramount. Our article on Choosing the Right Vehicle for Your Lifestyle and Budget provides excellent insights into making an informed decision that will serve you well in the long run.

Conclusion: Your Road to Independence Awaits

Securing a car loan for disabled veterans with bad credit is absolutely achievable. It requires diligence, a clear understanding of your options, and a strategic approach. By leveraging your VA benefits, exploring specialized programs, meticulously preparing your application, and understanding loan terms, you can overcome credit challenges and gain the independence a reliable vehicle provides.

Remember, your service to our nation has earned you unique support and consideration. Don’t let past financial hurdles deter you. Take the time to research, prepare, and seek out the lenders and programs that are designed to help you. Your journey towards a new vehicle, and the freedom it brings, is within reach. Start today, and drive towards a brighter, more independent future.