Navigating the Road Ahead: A Comprehensive Guide to Car Loans for Low-Income Single Mothers

Navigating the Road Ahead: A Comprehensive Guide to Car Loans for Low-Income Single Mothers Carloan.Guidemechanic.com

Life as a single mother is a testament to incredible strength and resilience. Juggling childcare, work, and household responsibilities often means every minute counts, and reliable transportation isn’t just a convenience—it’s an absolute necessity. Yet, for many low-income single mothers, securing an affordable car financing option can feel like an uphill battle, especially when facing credit challenges or limited income.

At our core, we understand these struggles. Based on my extensive experience helping families navigate complex financial landscapes, I know that obtaining a car loan for low-income single mothers is entirely possible with the right knowledge and strategy. This in-depth guide is designed to empower you, offering practical advice, resources, and expert tips to help you secure reliable transportation and open doors to new opportunities. Let’s drive into the details.

Navigating the Road Ahead: A Comprehensive Guide to Car Loans for Low-Income Single Mothers

Why a Reliable Car is a Game-Changer for Single Mothers

For single mothers, a car is far more than just a vehicle; it’s a lifeline. It represents freedom, stability, and access to essential services that can dramatically improve daily life.

Unlocking Employment Opportunities

Having a dependable car significantly expands your job search radius. It means you can apply for positions further from home, potentially accessing better-paying jobs or those with more flexible hours. Public transport schedules often don’t align with childcare drop-offs or evening shifts, making a personal vehicle indispensable for consistent employment.

Ensuring Childcare and School Access

Imagine the ease of dropping off and picking up your children without relying on multiple bus transfers or expensive ride-shares. A car provides consistent and safe transport for school, daycare, and after-school activities. This reliability reduces stress and allows for more structured routines, which benefits both you and your children.

Managing Emergencies and Healthcare

Emergencies don’t wait for public transport. Whether it’s a late-night trip to the emergency room or a sudden urgent care visit for a sick child, having your own vehicle offers peace of mind. It ensures you can respond quickly and efficiently to unexpected situations, which is crucial for the safety and well-being of your family.

Enhancing Independence and Quality of Life

Beyond the practicalities, a car provides a profound sense of independence. It allows you to run errands efficiently, attend appointments, and even enjoy recreational activities with your children. This improved quality of life can reduce feelings of isolation and contribute significantly to overall mental well-being.

Understanding the Hurdles: What Makes Car Loans Challenging?

While the need for a car is clear, securing a loan can present specific challenges for low-income single mothers. Recognizing these hurdles is the first step toward overcoming them.

Limited Income and Debt-to-Income Ratio

Lenders assess your ability to repay a loan based on your income. A lower income might mean a higher debt-to-income (DTI) ratio if you have existing debts, which can make lenders hesitant. They want to ensure you have enough disposable income to comfortably manage monthly car payments.

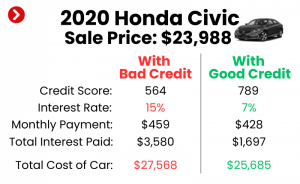

Credit Score Concerns

Many single mothers, particularly those who have faced financial hardships, may have a low or non-existent credit score. A poor credit history signals higher risk to lenders, often leading to higher interest rates or outright loan rejections. This is a common barrier, but it’s not insurmountable.

Lack of a Down Payment

A significant down payment reduces the amount you need to borrow and can offset some risk for lenders. However, saving a substantial sum can be incredibly difficult when managing a tight budget. Without a down payment, the loan amount is higher, and monthly payments follow suit.

Navigating Complex Loan Terms

The world of car financing can be confusing, filled with jargon like APR, loan terms, and various fees. Understanding these details and knowing how to negotiate for the best terms requires time and research, which are often scarce resources for busy single mothers.

Strategic Steps to Securing Your Car Loan

Don’t let these challenges deter you. Based on my experience, there are concrete strategies and resources available to help you secure a car loan for low-income single mothers.

1. Boosting Your Financial Standing

Before approaching lenders, taking steps to improve your financial profile can make a significant difference.

Improving Your Credit Score

Your credit score is a snapshot of your financial reliability. Even small improvements can open up better loan options.

- Check Your Credit Report: Start by obtaining free copies of your credit report from Equifax, Experian, and TransUnion. Review them carefully for errors, which you can dispute to potentially improve your score.

- Pay Bills on Time: Payment history is the biggest factor in your credit score. Make sure all your bills—utilities, rent, credit cards—are paid consistently and on time. Setting up automatic payments can be a huge help.

- Reduce Existing Debt: Focus on paying down high-interest debts, like credit card balances. Lowering your credit utilization (the amount of credit you use versus your available credit) can positively impact your score.

- Become an Authorized User: If a trusted family member with excellent credit is willing, becoming an authorized user on one of their credit cards can add positive payment history to your report. Pro tip from us: Ensure they have a strong track record of on-time payments.

Budgeting and Saving for a Down Payment

Even a small down payment can make your loan application more attractive.

- Create a Detailed Budget: Track every dollar coming in and going out. Identify areas where you can cut back, even temporarily. Every little bit saved adds up.

- Set Realistic Savings Goals: Start with a modest goal, perhaps $500 or $1,000. Once you hit it, you’ll feel motivated to save more. Consider opening a separate savings account specifically for your car down payment.

- Explore Down Payment Assistance Programs: Some non-profit organizations or local community programs offer grants or assistance for down payments, especially for those in specific circumstances. We’ll delve into these further.

Managing Your Debt-to-Income Ratio

Lenders look at your DTI to gauge your ability to take on new debt.

- Lower Your Debts: Prioritize paying off smaller debts to quickly reduce your overall debt load. This not only improves your DTI but also frees up more money for your monthly budget.

- Increase Your Income: While easier said than done, exploring options for a side hustle, part-time work, or applying for government assistance programs can help boost your reported income.

2. Exploring Loan Options Tailored to Your Situation

Not all lenders are created equal, especially when it comes to bad credit car loans for single moms or limited income situations.

Traditional Lenders: Banks and Credit Unions

- Banks: While traditional banks often offer competitive rates, they typically have stricter credit requirements. If your credit score is strong, they’re a good first stop.

- Credit Unions: These member-owned financial institutions are often more flexible and understanding than large banks. They may offer better rates and more personalized service, especially if you have a relationship with them. Pro tip from us: Credit unions are often a great option for those with less-than-perfect credit.

Dealership Financing (In-House and Manufacturer Programs)

Many dealerships offer their own financing or work with a network of lenders.

- In-House Financing: Some dealerships, often called "Buy Here, Pay Here" lots, finance loans directly. While they are more likely to approve applicants with poor credit, their interest rates can be significantly higher, and vehicle choices might be limited. Common mistakes to avoid here are not reading the fine print and accepting extremely high interest rates without exploring other options.

- Manufacturer Programs: Occasionally, car manufacturers offer special incentives or financing deals, sometimes including programs for first-time buyers or those with specific needs. It’s worth asking if any such programs are available.

Subprime Lenders

These lenders specialize in offering subprime auto loans for single mothers and others with low credit scores.

- How They Work: Subprime lenders take on more risk, so their interest rates are generally higher than traditional lenders. However, they can be a viable option when other avenues are closed.

- Caveats: Always compare offers from multiple subprime lenders to ensure you’re getting the best possible rate and terms. Be wary of predatory lenders with exorbitant fees.

Used Car Loans for Low Income

Focusing on a reliable used car can make a loan much more manageable.

- Lower Price Point: Used cars are significantly cheaper than new ones, meaning you’ll need to borrow less and have lower monthly payments.

- Depreciation: New cars lose a lot of value quickly. A used car has already taken that initial depreciation hit, making it a more financially sound purchase.

- Certified Pre-Owned (CPO): These vehicles come with a warranty and have undergone rigorous inspections, offering peace of mind similar to a new car but at a lower price.

3. Exploring Alternative Funding and Assistance

Sometimes, a direct loan isn’t the only path to a car.

Government Programs and Grants

While direct government grants for single mothers car purchases are rare, indirect assistance can free up funds for a car.

- TANF (Temporary Assistance for Needy Families): While not for direct car purchases, TANF funds can help with general living expenses, allowing you to allocate more of your income towards car savings or loan payments.

- Local and State Programs: Some states or counties have specific transportation assistance programs or grants for low-income individuals, especially those needing a car for work or medical appointments. It’s essential to research what’s available in your specific area.

Non-Profit Organizations and Community Programs

Many organizations are dedicated to helping single mothers and low-income families achieve self-sufficiency.

- Cars for Causes/Wheels to Work: Organizations like these often accept donated vehicles, refurbish them, and provide them to eligible individuals at a reduced cost or even free. Eligibility typically depends on income, need, and a demonstrated ability to cover insurance and maintenance.

- Local Churches and Charities: Many local community groups and religious organizations offer financial assistance or have programs to help individuals secure transportation. Don’t hesitate to reach out to local resource centers.

- Family and Friends: While not a formal loan, if you have supportive family or friends, consider discussing a private loan. If you do, always put the terms in writing to avoid misunderstandings.

The Application Process: What to Expect and How to Prepare

Once you’ve done your homework, it’s time to apply for a car loan for low-income single mothers. Being prepared will streamline the process.

Required Documents

Lenders will need specific documents to verify your identity, income, and financial stability. Gather these in advance:

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Pay stubs (last 2-3 months), tax returns, or benefit statements.

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Credit Report: While lenders will pull their own, having yours reviewed helps you understand your standing.

- Bank Statements: To show financial activity and savings.

- References: Sometimes requested, especially for those with limited credit history.

Understanding Loan Terms

Before signing anything, make sure you fully understand the loan agreement.

- Annual Percentage Rate (APR): This is the true cost of borrowing, including interest and some fees. A lower APR means lower overall cost.

- Loan Term: The length of time you have to repay the loan (e.g., 36, 48, 60 months). Longer terms mean lower monthly payments but more interest paid over time.

- Fees: Look out for origination fees, late payment fees, or prepayment penalties.

- Total Cost: Always calculate the total amount you’ll pay over the life of the loan.

Shopping Around for Rates

Never take the first offer. Based on my experience, comparing loan offers from at least three different lenders can save you hundreds, if not thousands, of dollars over the loan term. Use online comparison tools or visit multiple financial institutions.

Negotiating with Dealers

Once you have loan pre-approval (if possible), you’re in a stronger negotiating position with the dealership. Focus on the total price of the car, not just the monthly payment. Be firm but polite.

Pro Tips for Single Mothers Seeking a Car Loan

Here are some insights gathered from years of guiding individuals through similar situations.

- Focus on Reliable Used Cars: As mentioned, a well-maintained used car is a much more sensible investment than a new one. Prioritize reliability over luxury. Look for models known for their longevity and low maintenance costs.

- Get Pre-Approved: Obtaining loan approval tips for single mothers often starts with pre-approval. This tells you how much you can afford, gives you leverage at the dealership, and makes the car-buying process less stressful.

- Consider a Co-Signer: If your credit score is a significant hurdle, a trusted family member or friend with good credit who can co-sign the loan can increase your chances of approval and potentially secure a lower interest rate. Ensure both parties understand the responsibilities involved.

- Avoid Unnecessary Add-ons: Dealerships often try to upsell warranties, rustproofing, or other extras. Politely decline anything you don’t genuinely need or that isn’t included in your budget.

- Read the Fine Print: This cannot be stressed enough. Understand every clause in your loan agreement before you sign. If anything is unclear, ask for clarification. Don’t be rushed.

Common Mistakes to Avoid When Getting a Car Loan

Being aware of potential pitfalls can save you from financial headaches down the line.

- Ignoring Your Credit Score: Not knowing your credit standing before applying can lead to rejections or unfavorable terms. Check it and work to improve it.

- Not Budgeting Realistically: Don’t just budget for the monthly payment. Remember to include insurance, fuel, maintenance, and potential repair costs. These can add up quickly.

- Rushing the Decision: Feeling pressured to get a car quickly can lead to poor choices. Take your time, research thoroughly, and don’t settle for a deal that doesn’t feel right.

- Falling for High-Pressure Sales Tactics: Dealerships are in the business of selling. Be prepared to say no to offers that don’t align with your budget or needs.

- Overlooking Insurance Costs: Car insurance can be a significant expense. Get insurance quotes before finalizing your car purchase to ensure it fits within your budget.

Life Beyond Loan Approval: Managing Your Car and Finances

Once you’ve secured your car and loan, the journey continues. Responsible ownership is key to long-term financial stability.

Budgeting for Maintenance

Cars require regular upkeep. Create a separate fund for oil changes, tire rotations, and unexpected repairs. Proactive maintenance prevents bigger, more costly issues down the road.

Understanding Insurance Costs

Your car loan often requires full coverage insurance, which is more expensive than liability-only. Shop around for the best rates, and consider increasing your deductible if you have an emergency fund to cover it. You might find our article on "Budgeting for Single Parents: Mastering Your Money for a Brighter Future" helpful for managing these ongoing costs. (Internal Link 1)

Building an Emergency Fund for Car Repairs

Unexpected repairs can derail your budget. Aim to save at least $500-$1000 specifically for car-related emergencies. This small buffer can prevent you from falling back into debt.

Building Good Payment History

Every on-time car loan payment builds your credit history. This can lead to better interest rates on future loans and overall improved financial standing. This is a crucial step towards improving your financial future. If you’re looking for more ways to strengthen your credit, our guide on "Boosting Your Credit Score: A Comprehensive Guide to Financial Health" offers in-depth strategies. (Internal Link 2)

Conclusion: Driving Towards a Brighter Future

Securing car loans for low-income single mothers is a journey that requires patience, research, and strategic planning. While the path may have its challenges, the benefits of reliable transportation—increased employment opportunities, seamless childcare, enhanced safety, and greater independence—are immeasurable.

By understanding your financial situation, diligently working on your credit, exploring all available loan options, and being a savvy negotiator, you can achieve your goal of car ownership. Remember, you are not alone in this process. Utilize community resources, non-profit organizations, and expert advice to empower your decision-making.

The road ahead may seem daunting, but with this comprehensive guide, you’re well-equipped to navigate it successfully. Drive confidently towards a future of greater independence and opportunity for you and your children. For more trusted information on financial literacy and managing debt, consider exploring resources like the Consumer Financial Protection Bureau (CFPB) website. (External Link: https://www.consumerfinance.gov/)