Navigating the Road Ahead: A Comprehensive Guide to Subprime Car Loan Lenders

Navigating the Road Ahead: A Comprehensive Guide to Subprime Car Loan Lenders Carloan.Guidemechanic.com

Embarking on the journey to purchase a car is an exciting prospect, offering freedom and convenience. However, for many individuals, the path to vehicle ownership can seem blocked by the formidable hurdle of a less-than-perfect credit score. This is where subprime car loan lenders step in, providing a vital lifeline for those who might otherwise be denied traditional financing.

This comprehensive guide is designed to demystify the world of subprime auto loans. We’ll explore what these loans entail, how to find reputable lenders, navigate the application process, and ultimately, use this financial tool to not only secure a vehicle but also rebuild your credit for a stronger financial future. Our goal is to equip you with the knowledge and confidence needed to make informed decisions, transforming what can be a stressful experience into a strategic step forward.

Navigating the Road Ahead: A Comprehensive Guide to Subprime Car Loan Lenders

Understanding Subprime Car Loans: A Deep Dive

A "subprime" car loan might sound intimidating, but at its core, it’s a financing option specifically tailored for individuals with a credit score that falls below what traditional lenders consider "prime." Generally, this means a FICO score below 660, often ranging from 580 to 660, or even lower. These loans are a crucial segment of the auto financing market, recognizing that financial challenges don’t negate the need for reliable transportation.

The existence of subprime car loans acknowledges a significant demographic who, for various reasons, may have experienced credit difficulties. These could include past bankruptcies, foreclosures, late payments, or simply a limited credit history. Traditional lenders often view these factors as too high a risk, leading to automatic denials for conventional loans.

Based on my experience, many people mistakenly believe that having a bad credit score means car ownership is impossible. This simply isn’t true. While the terms may differ from those offered to individuals with excellent credit, subprime lenders are specifically structured to assess and mitigate these perceived risks, making car ownership a reality for millions. They understand that life happens, and a credit score is a snapshot, not a life sentence.

Identifying Reputable Subprime Car Loan Lenders

Finding the right lender is perhaps the most critical step in securing a subprime car loan. The market is vast, comprising various types of financial institutions, and not all are created equal. Knowing where to look and what to look for can significantly impact your loan terms and overall experience.

Types of Subprime Lenders:

- Dealership Financing (Buy Here, Pay Here): Many dealerships offer in-house financing, especially for subprime borrowers. This can be convenient, as you can shop for a car and arrange financing in one place. However, it’s essential to scrutinize their terms carefully, as rates can sometimes be higher, and selection might be limited.

- Traditional Banks and Credit Unions: While primarily serving prime borrowers, some larger banks and many credit unions have specialized departments or programs for subprime auto loans. Credit unions, in particular, are member-focused and might offer more flexible terms or slightly lower rates to their members, even with a challenging credit history.

- Online Lenders and Finance Companies: A growing number of online platforms and finance companies specialize exclusively in subprime auto loans. These lenders often have streamlined application processes and can provide multiple offers quickly. They can be an excellent option for comparing rates and terms from various providers without leaving your home.

Pro tips from us: Always prioritize lenders who are transparent about their rates, fees, and terms. A reputable lender will be upfront about all costs involved and won’t pressure you into signing anything you don’t fully understand. Check their reviews and ratings with organizations like the Better Business Bureau.

Common mistakes to avoid are falling for "guaranteed approval" promises without any credit check. While some lenders specialize in bad credit, no legitimate lender can guarantee approval without assessing your financial situation. This is often a red flag for predatory lending practices. Be wary of any lender that asks for upfront fees before approving your loan or doesn’t clearly disclose all charges.

The Application Process: What to Expect

Applying for a subprime car loan involves a process that is both similar to and distinct from a traditional auto loan application. While the core steps remain, subprime lenders often look at a broader range of factors beyond just your credit score. Preparing thoroughly can significantly improve your chances of approval and help you secure better terms.

Required Documents and Information:

Lenders will typically ask for documentation to verify your identity, income, and residency. This usually includes:

- Proof of Identity: A valid driver’s license or state ID.

- Proof of Income: Recent pay stubs (usually 1-3 months), tax returns if self-employed, or bank statements showing consistent deposits. This is crucial as it demonstrates your ability to repay the loan.

- Proof of Residence: Utility bills, a lease agreement, or mortgage statements with your current address.

- Proof of Insurance: You’ll need to show you have adequate car insurance before driving off the lot.

- References: Sometimes, personal or professional references may be requested.

What lenders look for goes beyond just the numbers on your credit report. They are trying to assess your overall financial stability and repayment capacity. They’ll consider your debt-to-income ratio, employment history, and even the stability of your residence. A long, stable employment history, for example, can offset a lower credit score in their eyes.

Pre-approval is a powerful tool in the subprime lending world. It allows you to get an estimate of how much you can borrow and at what interest rate before you even step foot in a dealership. This empowers you to shop for a car with a clear budget in mind, giving you leverage in negotiations. Once pre-approved, the full application involves submitting all your documentation for final verification.

Common mistakes to avoid are applying to too many lenders at once, which can further ding your credit score with multiple hard inquiries. Instead, research and select a few reputable lenders, perhaps three to four, and apply to them strategically. Also, never inflate your income or provide inaccurate information on your application; this can lead to loan denial or even legal repercussions.

Navigating the Terms: Interest Rates, Fees, and Loan Structures

Understanding the specific terms of a subprime car loan is paramount to making a sound financial decision. While these loans offer a necessary pathway to vehicle ownership, they often come with different structures and costs compared to prime loans. Being well-informed about these elements will protect you from unexpected expenses and help you manage your budget effectively.

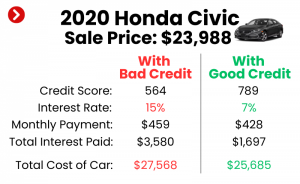

The primary difference you’ll encounter with subprime loans is generally higher interest rates. This isn’t arbitrary; it reflects the increased risk lenders perceive when financing individuals with lower credit scores. From the lender’s perspective, there’s a greater likelihood of default, and the higher interest rate serves as compensation for taking on that elevated risk. It’s crucial to understand that these rates can vary significantly depending on your specific credit profile, the lender, and the current market conditions.

When comparing loan offers, pay close attention to the Annual Percentage Rate (APR), not just the stated interest rate. The APR provides a more complete picture of the total cost of borrowing, as it includes not only the interest rate but also any additional fees associated with the loan, expressed as a yearly percentage. A lower interest rate might look appealing, but if it comes with high origination fees, the APR could still be substantial.

Common fees associated with subprime auto loans can include:

- Origination Fees: A charge for processing the loan application.

- Documentation Fees: Fees for preparing the loan paperwork.

- Late Payment Fees: Penalties for payments made after the due date.

- Prepayment Penalties: Some loans may charge a fee if you pay off the loan early. Based on my experience, these are less common with auto loans than other types of debt, but it’s always wise to check the fine print.

The loan term length also plays a significant role in the overall cost. While extending the loan term (e.g., to 72 or 84 months) can lower your monthly payments, it dramatically increases the total amount of interest you’ll pay over the life of the loan. This is a common strategy used by some lenders to make a loan seem more affordable upfront, but it costs you more in the long run. It’s a balance between managing monthly cash flow and minimizing the total cost of the vehicle.

Strategies for Securing the Best Possible Subprime Loan

Even with a less-than-perfect credit score, you’re not entirely without leverage. Several proactive strategies can significantly improve your chances of approval and help you secure more favorable terms on a subprime car loan. Taking these steps can save you thousands of dollars over the life of your loan.

One of the most impactful strategies is to improve your credit score before you apply. Even small improvements can make a difference. Start by checking your credit report for errors and disputing any inaccuracies. Pay down any outstanding credit card balances to lower your credit utilization ratio. Make sure all your current bills are paid on time. Even a few months of diligent effort can nudge your score into a better tier, potentially unlocking lower interest rates.

Saving for a larger down payment is another powerful move. A substantial down payment reduces the amount you need to borrow, which in turn lowers the lender’s risk. Lenders see a larger down payment as a sign of financial commitment and stability. It can also lead to smaller monthly payments and less interest paid over the loan term. Aim for at least 10-20% of the car’s purchase price if possible.

Having a co-signer with good credit can dramatically strengthen your application. A co-signer essentially guarantees the loan, promising to make payments if you default. This significantly reduces the lender’s risk and can help you qualify for a loan you might not otherwise get, often at a much better interest rate. However, ensure both you and your co-signer understand the full responsibility involved, as their credit will also be impacted by your payment history.

Shopping around and getting multiple quotes is non-negotiable. Do not accept the first offer you receive, especially from a dealership. Apply to a few different online lenders, credit unions, and banks. Most credit scoring models will treat multiple inquiries for the same type of loan within a specific period (usually 14-45 days) as a single inquiry, minimizing the impact on your score. This allows you to compare offers side-by-side and choose the best one.

Finally, remember that you are negotiating for two things: the car’s price and the loan terms. Negotiate the price of the car first, before discussing financing. A lower car price means you’ll need to borrow less, reducing your overall costs regardless of the interest rate. Once the car price is settled, then you can focus on securing the best financing. For more tips on this, you might find our article on Tips for Negotiating Car Prices helpful.

The Long-Term Game: Using a Subprime Loan to Rebuild Credit

Securing a subprime car loan isn’t just about getting a vehicle; it’s also a significant opportunity to improve your financial standing. When managed responsibly, a subprime auto loan can serve as a powerful tool for rebuilding your credit and opening doors to better financial opportunities in the future.

The most crucial aspect of rebuilding credit with a subprime loan is making every single payment on time, every month. Payment history is the largest factor in your credit score, accounting for 35% of your FICO score. Consistent, timely payments demonstrate financial responsibility to credit bureaus and lenders. Each on-time payment reported to the credit bureaus will gradually contribute to a positive payment history, slowly but surely elevating your credit score.

Monitoring your credit report regularly is also essential. You are entitled to a free credit report from each of the three major bureaus (Equifax, Experian, TransUnion) once every 12 months via AnnualCreditReport.com. Reviewing these reports allows you to track your progress, ensure your loan payments are being reported correctly, and identify any errors that could be negatively impacting your score. For more details on understanding your credit score and reports, check out our guide on Understanding Your Credit Score.

As your credit score improves and you build a solid payment history, you may become eligible for refinancing your subprime loan. Refinancing involves taking out a new loan, often with a lower interest rate, to pay off your existing one. This can significantly reduce your monthly payments and the total amount of interest you pay over the remaining term. Pro tips from us: Aim to refinance after 6-12 months of consistent, on-time payments, especially if interest rates have dropped or your credit score has seen a notable improvement.

Common Myths and Misconceptions About Subprime Auto Financing

The world of subprime auto financing is often shrouded in misconceptions and myths that can deter individuals from exploring viable options. Dispelling these falsehoods is crucial for making informed decisions and avoiding unnecessary anxiety or missteps.

One of the most pervasive myths is the idea of "guaranteed approval" car loans for bad credit. While many lenders specialize in working with challenging credit histories, no legitimate lender can guarantee approval without assessing an applicant’s financial situation. Terms like "guaranteed approval" are often marketing ploys designed to attract desperate borrowers, and they can sometimes be associated with predatory lending practices. Always approach such claims with extreme caution and skepticism.

Another common misconception is that if you have bad credit, you’re relegated to buying only old, unreliable, or cheap cars. While it’s wise to be financially prudent and avoid overspending, a subprime loan doesn’t automatically mean you can only afford a clunker. Many lenders offer financing for a wide range of vehicles, both new and used. The key is to find a car that fits your budget, considering not just the monthly payment but also insurance, maintenance, and fuel costs. The goal is reliable transportation that you can comfortably afford, not just the cheapest option.

Finally, some people believe that subprime loans are always a "rip-off" and should be avoided at all costs. While it’s true that subprime loans come with higher interest rates due to increased risk, they are a legitimate and often necessary financial product. For many, they are the only way to secure a reliable vehicle needed for work, school, or family responsibilities. When approached strategically, with careful research and understanding of the terms, a subprime loan can be a stepping stone to better credit and financial stability, rather than a financial trap. They provide a valuable service to a segment of the population that would otherwise be excluded from the auto market.

Checklist Before You Sign: Your Final Safeguards

Before you put your signature on any loan agreement, it’s absolutely critical to conduct a final review. This last-minute diligence can save you from future headaches, unexpected costs, and buyer’s remorse. Treat this as your ultimate safeguard.

First and foremost, read the fine print of the entire loan agreement, not just the parts the loan officer points out. Every clause, every condition, and every number matters. If anything is unclear, do not hesitate to ask for clarification. A reputable lender will be happy to explain everything in detail. Don’t let yourself be rushed or pressured into signing before you fully grasp every aspect of the agreement.

Understand all the costs involved beyond just the monthly payment. This includes the total loan amount, the APR, any origination fees, documentation fees, late payment penalties, and whether there are any prepayment penalties. Ask for an amortization schedule, which shows how your payments will be allocated between principal and interest over the life of the loan. This transparency is crucial for understanding your total financial commitment.

Always ask questions, no matter how trivial they may seem. Inquire about the lender’s policies on missed payments, options for deferment if you face a temporary financial hardship, and the process for refinancing down the line. Understanding these contingencies upfront prepares you for potential future scenarios and demonstrates your thoroughness. Remember, you have the right to fully understand what you are agreeing to.

Finally, never feel rushed or pressured into signing. This is a significant financial commitment, and you deserve time to review the documents, perhaps even take them home to read in a calm environment or have a trusted advisor look them over. If a lender or dealership is pressuring you, it’s a red flag. Walk away if you feel uncomfortable or if your questions are not being adequately answered. Your financial well-being is more important than any immediate car purchase.

Conclusion: Driving Towards Financial Empowerment

Navigating the landscape of subprime car loan lenders can initially feel like a daunting task, especially when dealing with the complexities of a less-than-perfect credit score. However, as we’ve thoroughly explored, these financial tools offer a crucial pathway to vehicle ownership and, more importantly, a powerful opportunity for financial rehabilitation. With the right knowledge and a strategic approach, a subprime auto loan can be far more than just a means to get a car; it can be a significant step toward rebuilding your credit and securing a more stable financial future.

By understanding what subprime loans entail, meticulously researching reputable lenders, preparing thoroughly for the application process, and diligently managing your loan payments, you are not just buying a car – you are investing in your credit health. Remember, every on-time payment contributes positively to your credit history, gradually paving the way for better financial products and opportunities down the road.

Don’t let past financial challenges define your future. Approach the journey with confidence, armed with the insights from this guide, and choose a subprime car loan that genuinely serves your needs and helps you move forward. Start your journey today with careful planning and an informed perspective, and drive towards both your dream car and improved financial well-being.