Navigating the Road Ahead: A Deep Dive into High Risk Car Loan Companies

Navigating the Road Ahead: A Deep Dive into High Risk Car Loan Companies Carloan.Guidemechanic.com

For many, a car isn’t just a luxury; it’s a necessity, a lifeline connecting you to work, family, and daily life. But what happens when past financial hurdles, like a low credit score or a history of missed payments, stand between you and reliable transportation? This is where the world of High Risk Car Loan Companies comes into play.

Navigating this terrain can feel daunting, filled with skepticism and confusing terms. However, understanding how these specialized lenders operate and what they offer can unlock the door to vehicle ownership and, potentially, a path to financial recovery. This comprehensive guide will peel back the layers, offering an in-depth look at high-risk auto loans, equipping you with the knowledge to make informed decisions and secure the car you need.

Navigating the Road Ahead: A Deep Dive into High Risk Car Loan Companies

Understanding the Landscape: What Exactly Are High-Risk Car Loans?

Before diving into specific companies, it’s crucial to grasp the fundamental concept of a high-risk car loan. Traditional lenders, such as major banks and credit unions, often prefer borrowers with excellent or good credit histories, as these individuals present a lower perceived risk of default. They see a consistent track record of on-time payments and responsible financial behavior.

However, life happens. Financial setbacks, unexpected emergencies, or even just a lack of credit history can leave individuals with what lenders classify as "high-risk" profiles. This isn’t a judgment on your character, but rather an assessment of the statistical likelihood of you repaying a loan based on your credit report. A high-risk car loan, often referred to as a subprime auto loan or bad credit car loan, is specifically designed to cater to these borrowers.

The core difference lies in the lender’s approach to risk. High-risk lenders are willing to take on borrowers that traditional institutions might reject. They understand that a low credit score doesn’t always equate to an inability or unwillingness to pay, but rather a need for a second chance or a different financing structure. These loans come with their own set of characteristics, primarily higher interest rates, to compensate the lender for the increased risk they are undertaking.

Who Qualifies as "High Risk" in the Eyes of a Lender?

Lenders use various metrics to determine a borrower’s risk profile. While the exact criteria can vary, several common scenarios typically place an individual into the "high-risk" category. Understanding these can help you anticipate how a lender might view your application.

Firstly, a low credit score is the most obvious indicator. Typically, a FICO score below 620 is considered subprime, with scores below 580 often falling into the "very poor" category. This signals to lenders that there have been past payment issues or a limited credit history, making future payment reliability uncertain.

Secondly, a history of significant financial distress, such as bankruptcy, foreclosure, or vehicle repossession, will immediately flag an applicant as high risk. These events demonstrate a past inability to meet financial obligations, even if circumstances have since improved. Lenders will look closely at the timing and details of these events.

Lastly, a thin credit file – meaning very little or no credit history – can also place you in this category. While it doesn’t indicate past financial mismanagement, it offers no data for a lender to assess your repayment habits. This makes it difficult for them to predict your future behavior, categorizing you similarly to someone with poor credit. High-risk car loan companies are specifically equipped to evaluate these complex profiles, often looking beyond just the credit score to other factors like current income and stability.

The Key Players: Who Are High Risk Car Loan Companies?

When you’re searching for car loans for bad credit, you’ll encounter various types of lenders specializing in this niche. These aren’t always the big banks you see on every corner; often, they are specialized financial institutions or even specific departments within dealerships. Based on my experience in the auto finance industry, knowing the different types of bad credit auto lenders is crucial for finding the right fit.

1. Subprime Lenders (Direct & Indirect)

These are arguably the most common type of High Risk Car Loan Companies. Subprime lenders specialize in providing financing to individuals with lower credit scores. They have underwriting criteria specifically designed for borrowers who might not qualify for conventional loans.

- Direct Subprime Lenders: Some companies exclusively operate as direct lenders, meaning you apply directly to them for the loan. These are often online lenders or specialized finance companies. They assess your application, approve the loan, and fund it themselves.

- Indirect Subprime Lenders: More commonly, subprime lenders work through dealerships. When you apply for financing at a dealership, and your credit isn’t prime, the dealership will submit your application to a network of subprime lenders they partner with. The dealership then acts as the intermediary, facilitating the loan process. This is a very common route for individuals seeking auto loans for poor credit.

2. Buy Here Pay Here (BHPH) Dealerships

BHPH dealerships represent a distinct segment of the high-risk auto loan market. They are unique because the dealership itself is the lender. Instead of arranging financing through a third party, you buy the car and make your payments directly to the dealership.

- Characteristics: BHPH dealerships are often willing to approve loans for individuals with very low credit scores, bankruptcies, or repossessions. They tend to focus more on your current income and ability to make regular payments rather than solely on your credit history. The approval process can be quicker, and the down payment requirements might be flexible.

- Considerations: While offering accessibility, BHPH loans typically come with significantly higher interest rates than even other subprime loans. The vehicle selection might be older models, and the terms can sometimes be less flexible. Pro tips from us: Always read the fine print carefully and understand the total cost of the loan over its entire term when dealing with BHPH dealerships.

3. Credit Unions

While many credit unions prioritize members with good credit, some offer second chance auto loans or programs specifically for members with less-than-perfect credit. Credit unions are member-owned, non-profit organizations, which means they sometimes offer more flexible terms and lower rates than traditional banks or even some subprime lenders, especially to their existing members.

- Benefits: If you’re already a member, or willing to become one, it’s worth inquiring about their bad credit auto loan options. They often take a more holistic view of your financial situation.

- Limitations: Their high-risk offerings might still be more restrictive than dedicated subprime lenders, and approval isn’t guaranteed for all applicants.

4. Online Loan Aggregators and Networks

These platforms aren’t direct lenders themselves but act as a bridge, connecting you with a network of lenders, including many specializing in high-risk car loans. You fill out one application, and it gets submitted to multiple lenders who then pre-qualify you or send you offers.

- Advantages: This can save significant time and effort compared to applying to individual lenders one by one. It also allows you to compare multiple offers without impacting your credit score with numerous hard inquiries.

- How it works: They typically partner with both subprime lenders and special finance car dealerships that have robust bad credit auto loan programs.

Understanding these different types of High Risk Car Loan Companies will empower you to target your search more effectively and choose the lender type that best suits your financial situation and needs.

Debunking the Myths: "Guaranteed Approval" and "No Credit Check" Loans

The terms "guaranteed approval car loans" and "no credit check car loans" frequently appear in advertising for high-risk financing. It’s essential to approach these claims with a healthy dose of skepticism. Based on my expertise, true "guaranteed approval" or "no credit check" loans are extremely rare, if not entirely misleading.

No reputable lender will ever truly guarantee approval without some form of financial assessment. Even lenders specializing in bad credit car loans need to ensure you have the income and ability to repay the loan. They might not weigh your credit score as heavily as traditional banks, but they will look at other factors like your employment history, debt-to-income ratio, and residency stability. The "guaranteed" aspect often comes with significant caveats, such as requiring a very large down payment, or it might refer to a pre-qualification, not a final approval.

Similarly, "no credit check" loans are almost exclusively associated with Buy Here Pay Here (BHPH) dealerships. While these dealerships might not pull a traditional credit report from Experian, Equifax, or TransUnion, they will absolutely perform their own assessment of your financial standing. This often involves verifying your income, employment, and banking history to gauge your ability to make payments. They are, in essence, doing their own form of "credit check," just not the kind that impacts your FICO score.

The danger in believing these myths is that borrowers might overlook crucial details, such as exorbitant interest rates, hidden fees, or unfavorable loan terms. Always remember that if something sounds too good to be true in the world of financing, it very likely is. Focus instead on finding lenders who are transparent about their criteria and offer fair terms, even if they are for a higher-risk profile.

Navigating the High-Risk Car Loan Process: Preparation is Power

Securing an auto loan when you have bad credit doesn’t have to be an ordeal. With the right preparation, you can approach High Risk Car Loan Companies with confidence and increase your chances of approval on favorable terms. This proactive approach is a cornerstone of responsible borrowing.

1. Know Your Credit Score and Report

The very first step is to understand where you stand. Obtain a copy of your credit report from all three major bureaus (Experian, Equifax, and TransUnion) and check your credit score. Many services offer this for free.

- What to look for: Scrutinize your report for any errors or inaccuracies that could be unfairly dragging down your score. Disputing these can sometimes boost your score relatively quickly. Understanding the negative marks will also help you explain your situation to a potential lender. For more details on improving your score, consider reading our guide on How to Improve Your Credit Score Before Applying for a Loan (Internal Link 1).

2. Create a Realistic Budget

Before even looking at cars, determine how much you can truly afford to pay each month. This isn’t just about the car payment; it includes insurance, fuel, maintenance, and registration fees.

- Affordability: Lenders will look at your debt-to-income ratio (DTI), which compares your total monthly debt payments to your gross monthly income. A lower DTI indicates you have more disposable income to cover new loan payments, making you a less risky borrower. Aim for a DTI below 40% if possible.

3. Save for a Down Payment

A significant down payment is one of the most powerful tools you have when applying for a high-risk car loan. It directly reduces the amount you need to borrow, which lowers your monthly payments and the total interest paid over the life of the loan.

- Lender Confidence: A larger down payment also signals to bad credit auto lenders that you are serious about the purchase and have some financial stability. It mitigates their risk, potentially leading to better interest rates. Pro tips from us: Aim for at least 10-20% of the vehicle’s purchase price.

4. Gather Necessary Documents

Being prepared with all your paperwork can streamline the application process. Lenders will typically require:

- Proof of income (pay stubs, bank statements, tax returns).

- Proof of residency (utility bill, lease agreement).

- Proof of identity (driver’s license, passport).

- References (sometimes required by subprime lenders).

5. Consider a Cosigner

If you have a trusted friend or family member with good credit who is willing to cosign your loan, it can significantly improve your chances of approval and potentially secure a lower interest rate.

- Cosigner Responsibilities: A cosigner takes on equal responsibility for the loan. If you miss payments, their credit will be negatively affected, and they will be legally obligated to make the payments. This is a serious commitment for both parties.

The Application Steps with High-Risk Lenders

Once you’ve done your homework, the application process itself is fairly straightforward:

- Pre-qualification: Many online High Risk Car Loan Companies and aggregators offer pre-qualification forms. This allows you to see potential loan terms without a hard credit inquiry, which won’t impact your credit score.

- Full Application: Once you find a lender you like, you’ll complete a full application, which will involve a hard credit inquiry.

- Review Offers: Compare interest rates, loan terms, and any fees. Don’t feel pressured to take the first offer.

- Finalize & Purchase: Once approved, you’ll finalize the loan documents and proceed with purchasing your vehicle.

By preparing thoroughly, you not only improve your chances of approval but also empower yourself to negotiate for the best possible terms.

The Cost of High-Risk Car Loans: Understanding the Numbers

One of the most significant aspects of obtaining a loan from High Risk Car Loan Companies is the cost associated with it. Due to the increased risk lenders assume, these loans typically come with higher expenses compared to traditional financing. Understanding these costs is paramount to making an informed decision. For more information on interest rates, check out our article on Understanding Car Loan Interest Rates (Internal Link 2).

1. Higher Interest Rates

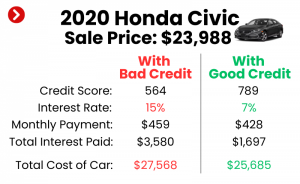

This is the most direct consequence of a low credit score. Lenders charge a higher interest rate to compensate for the greater likelihood of default. While someone with excellent credit might get an annual percentage rate (APR) in the low single digits, a high-risk borrower could face rates anywhere from 10% to 25% or even higher, depending on their credit profile and the specific lender.

- Impact: Over the life of the loan, even a few percentage points difference in interest can add thousands of dollars to the total cost of the vehicle. This is why a larger down payment and a shorter loan term become even more crucial for high-risk borrowers.

2. Longer Loan Terms

To make monthly payments more "affordable" given the higher interest rates, High Risk Car Loan Companies often offer longer loan terms, stretching out payments over 60, 72, or even 84 months. While this reduces the monthly burden, it has a significant downside.

- Drawback: A longer loan term means you’ll be paying interest for a longer period, dramatically increasing the total amount you pay for the car. You also run the risk of becoming "upside down" on your loan – owing more than the car is worth – for a longer duration, especially with depreciation.

3. Fees and Charges

Be vigilant about potential fees. These can include origination fees, documentation fees, or even charges for specific services. While some fees are standard, ensure they are clearly disclosed and reasonable.

- Transparency: Reputable bad credit auto lenders will be transparent about all fees. Common mistakes to avoid are not asking for a full breakdown of all costs and only focusing on the monthly payment.

Strategies to Mitigate High Costs:

- Maximize Your Down Payment: As discussed, a larger down payment reduces the principal amount borrowed, directly cutting down on interest paid.

- Choose a Shorter Loan Term: If your budget allows, opt for the shortest loan term possible. This will increase your monthly payment but drastically reduce the total interest paid.

- Improve Your Credit First: If your need for a car isn’t immediate, dedicating a few months to improving your credit score can make a substantial difference in the interest rates you’re offered. Pay down existing debts, make all payments on time, and correct any errors on your credit report.

- Consider a Cosigner: A cosigner with good credit can help you secure a lower interest rate, as their creditworthiness balances out your higher risk.

- Shop Around: Get quotes from multiple High Risk Car Loan Companies and compare their offers meticulously. Don’t settle for the first approval you receive.

- Negotiate: Even with bad credit, there might be some room for negotiation on the vehicle price or loan terms, especially at special finance car dealerships.

Understanding these costs and employing mitigation strategies are essential steps towards securing a manageable and responsible high-risk auto loan.

Finding Reputable High Risk Car Loan Companies: Your Due Diligence

With so many options, how do you distinguish between legitimate High Risk Car Loan Companies and those that might take advantage of your situation? Finding a trustworthy lender requires careful research and a critical eye. This step is as important as the application itself.

1. Research Lenders Thoroughly

Start by creating a list of potential lenders. This can include:

- Online Subprime Lenders: Many reputable companies operate entirely online, specializing in car loans for bad credit.

- Dealerships with Special Finance Departments: These dealerships have dedicated teams and relationships with bad credit auto lenders to help customers with challenging credit histories. They often advertise "second chance auto loans."

- Local Credit Unions: As mentioned, some credit unions offer programs for members with less-than-perfect credit.

2. Check Reviews and Ratings

Once you have a list, delve into their reputation.

- Online Reviews: Look at customer reviews on independent sites like Google Reviews, Yelp, and Trustpilot. Pay attention to consistent complaints about hidden fees, poor customer service, or aggressive collection practices.

- Better Business Bureau (BBB): Check the lender’s rating with the BBB. A good rating (A+ to B) and few unresolved complaints are positive indicators.

- Consumer Financial Protection Bureau (CFPB): This government agency tracks consumer complaints against financial institutions. Searching for a lender here can reveal significant issues.

3. Compare Offers Meticulously

Do not accept the first offer you receive. Get pre-qualified with several different High Risk Car Loan Companies or through an online aggregator. This allows you to compare:

- Interest Rates (APR): The annual percentage rate is the most critical figure, as it reflects the true cost of borrowing.

- Loan Terms: Compare the length of the loan and how it impacts your total cost.

- Fees: Ensure all fees are disclosed and compare their amounts.

- Total Cost of Loan: Calculate the total amount you will pay over the life of each loan offer (principal + interest + fees).

4. Look for Transparency

Reputable lenders are transparent about their terms and conditions. They should clearly explain:

- Their eligibility criteria.

- All interest rates, fees, and charges upfront.

- The full amortization schedule of your loan.

Common mistakes to avoid are feeling rushed or pressured into signing without fully understanding every aspect of the loan agreement. If a lender is vague, unwilling to answer questions, or pushes you to sign immediately, consider it a red flag. Take your time, ask questions, and don’t be afraid to walk away if something feels off.

Rebuilding Your Credit Through a High-Risk Car Loan: A Stepping Stone to Financial Health

While the primary goal of securing a high-risk car loan is to get reliable transportation, it also presents a unique opportunity: the chance to actively rebuild your credit. This often overlooked benefit can transform a necessary expense into a powerful tool for improving your financial future.

When you obtain a loan from High Risk Car Loan Companies and make consistent, on-time payments, this positive activity is reported to the major credit bureaus. Every payment made on time demonstrates to lenders that you are a responsible borrower capable of managing debt. This positive reporting will gradually, but steadily, improve your credit score over time.

As your credit score improves, doors that were previously closed will begin to open. You might qualify for better interest rates on future loans, secure more favorable terms on credit cards, or even find it easier to rent an apartment or get lower insurance premiums. A high-risk auto loan, when managed properly, serves as a crucial stepping stone.

The Path to Refinancing

As your credit score improves, you might also qualify for refinancing your existing high-risk car loan. Refinancing involves taking out a new loan, typically with a lower interest rate, to pay off your current loan. This can significantly reduce your monthly payments and the total amount of interest you pay over the remaining term.

- Timing: It’s generally advisable to wait at least 6-12 months of consistent, on-time payments before exploring refinancing options. This gives your credit score enough time to reflect your improved payment habits.

- Benefits: A lower interest rate means more of your payment goes towards the principal, accelerating your path to ownership and saving you money.

Think of your high-risk car loan not just as a means to an end, but as an active component of your credit repair strategy. By diligently making payments and understanding the terms, you’re not just buying a car; you’re investing in your financial recovery.

Conclusion: Driving Towards a Brighter Financial Future

Navigating the landscape of High Risk Car Loan Companies can seem complex, but with the right knowledge and a strategic approach, it’s an entirely achievable goal. We’ve explored what defines a high-risk loan, identified the key types of lenders, debunked common myths, and provided a comprehensive roadmap for preparation and application.

Remember, a high-risk car loan is often more than just a means to acquire a vehicle; it’s a valuable opportunity to demonstrate financial responsibility and rebuild your creditworthiness. While the interest rates may be higher, and the terms might require careful scrutiny, these loans provide essential access to transportation for millions who are working to overcome past financial challenges.

By understanding the costs, meticulously researching reputable bad credit auto lenders, and committing to consistent, on-time payments, you can leverage this experience to your advantage. You’re not just securing a ride; you’re paving the way for a more stable and promising financial future. Don’t let past setbacks define your journey. Start your research today, prepare diligently, and take that empowered step towards the vehicle and financial freedom you deserve.