Navigating the Road Ahead: A Deep Dive into the 63-Month Car Loan

Navigating the Road Ahead: A Deep Dive into the 63-Month Car Loan Carloan.Guidemechanic.com

Buying a car is a significant financial decision, and choosing the right loan term can dramatically impact your budget and overall financial health. While 60-month (5-year) and 72-month (6-year) car loans are common, the 63-month car loan often emerges as a unique option that deserves a closer look. It’s not just an arbitrary number; for many, it represents a strategic sweet spot in auto financing.

As an expert blogger and SEO content writer with years of experience dissecting financial topics, I understand the nuances of auto loans. My goal today is to provide you with a comprehensive, in-depth guide to the 63-month car loan. We’ll explore its advantages, potential pitfalls, and how to determine if this specific term is the right path for your next vehicle purchase. By the end of this article, you’ll be equipped with the knowledge to make an informed decision, ensuring a smoother ride for your finances.

Navigating the Road Ahead: A Deep Dive into the 63-Month Car Loan

What Exactly is a 63-Month Car Loan?

At its core, a 63-month car loan is an agreement to repay the principal amount borrowed for a vehicle, plus interest, over a period of 63 months – which equates to five years and three months. This term sits comfortably between the more traditional 60-month and 72-month options, offering a distinct set of characteristics that appeal to a particular segment of car buyers.

This specific loan duration isn’t as widely advertised as its even-numbered counterparts, but it’s a legitimate option offered by many lenders. It’s often presented when a borrower is looking to slightly reduce their monthly payments compared to a 60-month loan, without committing to the full six years of a 72-month term. Think of it as a finely tuned adjustment to your repayment schedule.

The Allure of a Longer Loan Term: Why 63 Months Appeals

The primary draw of any longer loan term, including 63 months, is the reduction in your monthly payment. Spreading the total cost of the vehicle over a longer period means each individual payment becomes smaller and more manageable. This can be a game-changer for budgeting.

Lower Monthly Payments: This is arguably the biggest benefit. A slightly longer term like 63 months, compared to 60 months, can shave a few dollars off your monthly obligation. This difference, while seemingly small, can free up cash flow for other expenses or savings goals. It makes higher-priced vehicles more accessible without straining your immediate budget.

Affordability for Higher-Priced Vehicles: For many, a 63-month loan makes a dream car or a necessary upgrade more financially viable. If you need a more reliable family car or a vehicle with specific features, but the monthly payments on a shorter term are too high, stretching it out to 63 months can bring it within reach. This allows you to drive the car you need or want sooner.

Budgeting Flexibility: Lower payments provide greater flexibility in your personal finances. You might use the extra funds to build an emergency fund, pay down other debts, or invest. Based on my experience, many buyers appreciate this breathing room, especially when unexpected expenses arise. It’s about creating a sustainable financial plan that accommodates car ownership without undue stress.

Understanding the Potential Downsides

While the appeal of lower monthly payments is strong, it’s crucial to understand that longer loan terms, including 63 months, come with their own set of financial trade-offs. Overlooking these can lead to significant long-term costs. Responsible car ownership involves balancing immediate affordability with future financial health.

Higher Total Interest Paid: This is the most significant drawback. The longer you take to repay a loan, the more interest accrues over the life of that loan. Even if the interest rate is the same, those extra three months compared to a 60-month loan, or even just the extension from a much shorter term, mean you’re paying interest for a longer duration. This results in a higher overall cost for the vehicle.

Risk of Negative Equity (Upside Down Loan): When you have negative equity, it means you owe more on your car than its current market value. Longer loan terms increase the likelihood of this happening, especially during the initial years of ownership. Cars depreciate rapidly, and if your payments are spread too thin, your loan balance might decrease slower than the car’s value. This becomes a major issue if you need to sell or trade in the vehicle early. Common mistakes to avoid are underestimating depreciation and over-financing.

Longer Commitment: A 63-month loan means you’re committed to making car payments for over five years. This is a substantial chunk of time in anyone’s financial life. During this period, your financial situation might change, or your vehicle needs could evolve. A longer commitment means less flexibility to adapt to these changes without financial repercussions.

Increased Wear and Tear Beyond Warranty: Most new car warranties typically last around 3 years/36,000 miles or 5 years/60,000 miles. With a 63-month loan, you’ll be making payments for several months, or even a year or more, after your basic warranty expires. This means any repairs that arise during the latter part of your loan term will come directly out of your pocket, adding unexpected costs to your already existing loan payments.

Who is a 63-Month Car Loan Best Suited For?

A 63-month car loan isn’t for everyone, but it can be an excellent fit for specific types of buyers. Understanding if you fall into this category is key to making a smart financial choice. It’s about aligning the loan term with your personal financial situation and car ownership goals.

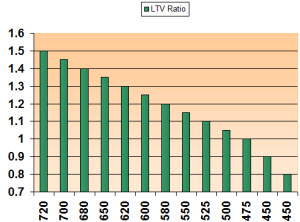

Buyers with Excellent Credit Looking for Specific Benefits: Individuals with strong credit scores (typically 700+) are often offered lower interest rates. This minimizes the impact of paying more interest over a longer term. For these buyers, a 63-month loan can offer slightly reduced payments without a drastically higher total cost compared to shorter terms. They benefit from affordability while still securing favorable loan conditions.

Those Needing Slightly Lower Payments to Fit a Budget: If your budget is tight but you absolutely need a reliable vehicle, a 63-month term can provide that crucial wiggle room. It allows you to manage your cash flow effectively, ensuring you don’t overextend yourself monthly. This is particularly relevant if a 60-month loan pushes your budget past its comfortable limit.

People Who Plan to Keep Their Car for a Long Time: If you’re someone who drives their vehicles until the wheels fall off, a 63-month loan might make sense. By keeping the car for 7-10 years or more, you effectively spread the total cost over a much longer period of actual ownership. This mitigates the impact of being upside down on the loan for a few years, as you’ll eventually own it outright and then enjoy years of payment-free driving.

Individuals with Stable Finances: A consistent income and job security are important for any long-term loan. If your employment is stable and your income reliable, you can comfortably commit to payments for over five years. Any uncertainty in your financial outlook might make a shorter term, or a less expensive vehicle, a more prudent choice.

Factors Influencing Your 63-Month Car Loan

Several key factors will determine the terms and total cost of your 63-month car loan. Understanding these elements empowers you to negotiate effectively and secure the best possible deal. Pro tips from us: always prepare by assessing these factors before approaching a lender or dealership.

Credit Score

Your credit score is paramount. It’s a numerical representation of your creditworthiness, and lenders use it to assess the risk of lending to you. A higher credit score (e.g., FICO Score 700+) signals lower risk, typically resulting in lower Annual Percentage Rates (APRs). Conversely, a lower score will lead to higher interest rates, significantly increasing your total cost over 63 months. For more insights on managing your car budget, check out our article on Budgeting for Your First Car (Internal Link 1 Placeholder).

Down Payment

A down payment is the amount of money you pay upfront for the car. Making a larger down payment directly reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay over the 63-month term. A substantial down payment also helps reduce the risk of negative equity, giving you a cushion against depreciation. Aim for at least 10-20% if possible.

Interest Rate (APR)

The Annual Percentage Rate (APR) is the true cost of borrowing, expressed as a yearly rate. It includes both the interest rate and any additional loan fees. Even a small difference in APR can translate into hundreds or thousands of dollars saved (or spent) over a 63-month period. Always compare APRs from multiple lenders, not just the monthly payment.

Loan Amount

This is the total price of the vehicle you are financing, minus any down payment or trade-in value. The higher the loan amount, the higher your monthly payments will be, and the more interest you will accrue over 63 months. It’s crucial to negotiate the car’s price before discussing financing to ensure you’re not overpaying.

Trade-in Value

If you’re trading in your old vehicle, its value can act like an additional down payment. The trade-in amount reduces the principal balance of your new loan, leading to lower monthly payments and less interest over the 63-month term. Ensure you research your car’s trade-in value beforehand to get a fair deal.

Calculating Your 63-Month Car Loan Payments

Understanding how your monthly payments are calculated is essential for budgeting. While complex formulas exist, the easiest way to estimate is using online car loan calculators. These tools allow you to input the loan amount, interest rate, and term (63 months) to instantly see your estimated monthly payment and total interest.

Let’s consider a hypothetical example:

- Loan Amount: $25,000

- APR: 5.0%

- Loan Term: 63 months

Using a standard loan calculator, your estimated monthly payment would be approximately $446.00. Over the 63-month term, the total amount paid back would be around $28,098, meaning you’d pay roughly $3,098 in interest. This illustrates the importance of understanding total cost. Pro tips from us: Always calculate the total cost over the life of the loan, not just the monthly payment, to truly understand your financial commitment.

The Application Process for a 63-Month Car Loan

Applying for a car loan, regardless of the term, involves several steps. Being prepared and understanding the process can save you time and potentially secure better terms. This is where informed decision-making truly comes into play.

Gathering Documents: Before you even step foot in a dealership, gather necessary documentation. This typically includes proof of income (pay stubs, tax returns), proof of residence (utility bill), identification (driver’s license), and details of your trade-in if applicable. Having these ready streamlines the application.

Pre-approval vs. Dealership Financing: Based on my experience, getting pre-approved by your bank, credit union, or an online lender before visiting a dealership is a powerful strategy. Pre-approval gives you a clear understanding of what interest rate and loan amount you qualify for, effectively giving you a "cash offer" in hand. This allows you to negotiate the car price separately from the financing, often leading to a better overall deal. Dealership financing can sometimes offer competitive rates, but it’s always best to have an alternative offer.

Understanding the Fine Print: Never sign a loan agreement without thoroughly reading and understanding every clause. Pay close attention to the APR, any fees (origination fees, documentation fees), and specifically look for prepayment penalties. These penalties could negate the benefits if you decide to pay off your 63-month loan early.

Common mistakes to avoid are:

- Not shopping around for loans: Always compare offers from at least three different lenders.

- Focusing solely on the monthly payment: As discussed, the total cost matters more.

- Rushing the process: Take your time to review all documents and ask questions.

Strategies to Optimize Your 63-Month Car Loan

Even with a longer loan term, there are proactive steps you can take to make your 63-month car loan as financially advantageous as possible. These strategies aim to reduce your overall cost and improve your financial flexibility.

Boost Your Credit Score: Prior to applying, take steps to improve your credit score. Pay off outstanding debts, correct any errors on your credit report, and make all payments on time. A higher score translates directly to a lower interest rate, saving you significant money over 63 months. If you’re curious about improving your credit, read our guide on Steps to Boost Your Credit Score (Internal Link 2 Placeholder).

Make a Larger Down Payment: As discussed, the more you put down upfront, the less you borrow. This directly reduces your monthly payments and the total interest accrued. It also provides immediate equity in your vehicle, protecting you against becoming upside down on your loan.

Shop for the Best Interest Rates: Don’t settle for the first offer. Contact multiple banks, credit unions, and online lenders to compare their APRs. Even a quarter-point difference can save you hundreds over five years. Use your pre-approval offer to leverage better rates from other lenders or the dealership.

Consider a Co-signer (If Necessary and Understood): If your credit isn’t ideal, a co-signer with excellent credit can help you secure a lower interest rate. However, understand that a co-signer is equally responsible for the loan. If you miss payments, their credit will be negatively impacted, and they could be held liable for the debt. This decision should not be taken lightly.

Negotiate the Car Price First: Always negotiate the purchase price of the vehicle before discussing financing. Dealers sometimes try to distract buyers with attractive monthly payment figures, masking an inflated car price or unfavorable loan terms. Get the best car price, then work on the best loan.

Read the Loan Agreement Carefully: This cannot be stressed enough. Understand all terms, conditions, fees, and penalties. If anything is unclear, ask for clarification. Don’t be pressured into signing anything you don’t fully comprehend.

What if I Want to Pay Off My 63-Month Loan Early?

Life circumstances change, and you might find yourself in a position to pay off your car loan ahead of schedule. Doing so can save you a substantial amount in interest, but it’s important to check for any potential hurdles.

Prepayment Penalties: Some loan agreements include prepayment penalties. These are fees charged by the lender if you pay off your loan before the scheduled term. While less common with auto loans than with mortgages, it’s crucial to verify this in your loan agreement’s fine print. If a penalty exists, weigh the cost of the penalty against the interest you would save by paying off early.

Benefits of Early Payoff: If there are no prepayment penalties, paying off your 63-month loan early is highly beneficial. You’ll save on all the remaining interest that would have accrued over the rest of the term. This also frees up your monthly budget, reduces your debt burden, and allows you to own your car outright sooner.

How to Do It Effectively:

- Make extra payments: Even small additional payments each month can significantly shorten your loan term and reduce total interest.

- Pay bi-weekly: Instead of one payment a month, pay half your payment every two weeks. This results in 13 full payments per year instead of 12, effectively making an extra payment annually.

- Apply windfalls: Use bonuses, tax refunds, or other unexpected income to make a lump-sum payment towards your principal.

Refinancing Your 63-Month Car Loan

Refinancing means taking out a new loan to pay off your existing one, ideally at a better interest rate or with more favorable terms. This can be a smart move for your 63-month car loan under certain conditions.

When it Makes Sense:

- Improved Credit Score: If your credit score has significantly improved since you first took out the loan, you might qualify for a much lower interest rate.

- Lower Interest Rates: General market interest rates might have dropped since your original loan.

- Financial Strain: If you’re struggling with payments, refinancing to a slightly longer term (e.g., from 63 to 72 months) could lower your monthly payment, though it would increase total interest.

- To Remove a Co-signer: If your credit has improved, you might be able to refinance the loan in your name only, releasing your co-signer from their obligation.

The Process: The refinancing process is similar to applying for your initial car loan. You’ll gather documents, shop for new lenders, and compare offers. Once approved, the new lender pays off your old loan, and you begin making payments to the new lender under the new terms.

Benefits: The primary benefit of refinancing is saving money on interest. It can also lead to lower monthly payments or a shorter loan term, depending on your goals. Based on my experience, many people overlook refinancing as a way to optimize their existing loans, potentially missing out on significant savings. For more detailed information on consumer auto financing, a reliable resource like the Consumer Financial Protection Bureau (CFPB) offers valuable insights. (External Link: https://www.consumerfinance.gov/consumer-tools/auto-loans/)

Conclusion: Making an Informed Decision

The 63-month car loan, while not as commonly discussed as other terms, presents a viable and often beneficial option for many car buyers. It offers a unique balance between manageable monthly payments and a reasonable repayment period, sitting squarely between the 60-month and 72-month benchmarks. However, like any financial product, its suitability depends entirely on your individual financial situation, creditworthiness, and long-term goals.

Before committing to a 63-month car loan, it is imperative to conduct thorough research, compare offers from multiple lenders, and meticulously read all loan documentation. Weigh the allure of lower monthly payments against the potential for higher total interest and the risk of negative equity. By understanding all the factors at play – from your credit score and down payment to interest rates and potential prepayment penalties – you empower yourself to make a decision that aligns with your financial well-being.

Remember, the goal is not just to get into a car, but to do so responsibly and sustainably. A 63-month car loan can be an excellent tool for achieving your automotive dreams, provided you approach it with knowledge, caution, and a clear understanding of its implications. Drive smart, and your financial journey will be as smooth as your new ride. Share your experiences or questions about car loans in the comments below – we’d love to hear from you!