Navigating the Road Ahead: Can I Get a Car Loan with a 530 Credit Score?

Navigating the Road Ahead: Can I Get a Car Loan with a 530 Credit Score? Carloan.Guidemechanic.com

Facing the challenge of securing a car loan with a 530 credit score can feel like staring down a daunting, uphill battle. Many people find themselves in this exact position, wondering if their dream of owning a reliable vehicle is simply out of reach. The good news? While a 530 credit score is indeed categorized as "Very Poor" by FICO and VantageScore models, getting approved for a car loan isn’t entirely impossible. It requires a strategic approach, realistic expectations, and a willingness to put in the effort.

Based on my experience in the financial and automotive sectors, securing a car loan with a low credit score isn’t about finding a magic wand; it’s about understanding the landscape, mitigating risks for lenders, and demonstrating your commitment to financial responsibility. This comprehensive guide will walk you through the realities, reveal actionable strategies, and equip you with the knowledge to increase your chances of approval, even with a 530 credit score.

Navigating the Road Ahead: Can I Get a Car Loan with a 530 Credit Score?

Understanding Your 530 Credit Score: What It Really Means

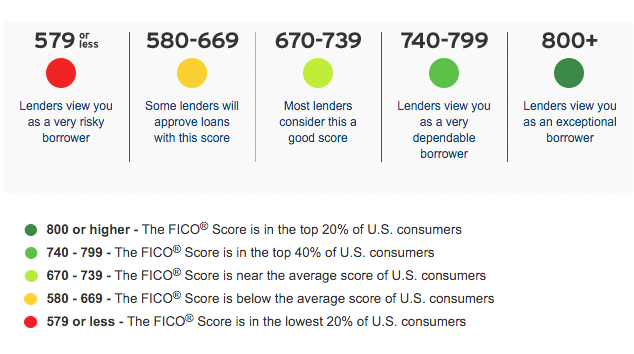

Before we dive into loan strategies, let’s get a clear picture of what a 530 credit score signifies. Credit scores, primarily FICO and VantageScore, range from 300 to 850. A score of 530 places you firmly in the "Very Poor" or "Bad" credit category.

This rating tells potential lenders that you’ve likely had a history of financial challenges. These could include missed payments, high credit utilization, collections, bankruptcies, or a short credit history. From a lender’s perspective, a 530 score indicates a higher risk of default, meaning there’s a greater chance you might not repay the loan as agreed. This perception of risk directly impacts their willingness to lend and the terms they’ll offer.

The Reality Check: What to Expect When Seeking a Car Loan with Bad Credit

Let’s be upfront: securing a car loan with a 530 credit score will be more challenging than for someone with good or excellent credit. You’ll encounter a different set of expectations and limitations.

Firstly, your lender options will be more restricted. Traditional banks and prime lenders typically prefer applicants with scores above 660. You’ll likely need to explore subprime lenders, credit unions, or specific dealership financing programs that specialize in bad credit auto loans.

Secondly, expect higher interest rates (APR). Because you represent a higher risk, lenders will charge more to compensate for that risk. This means your monthly payments will be higher, and the total cost of the car over the loan term will be significantly more than for a borrower with a good credit score. It’s crucial to understand that while an approval might be possible, the terms might not be ideal.

Strategic Moves: Key Steps to Improve Your Chances of Approval

Even with a 530 credit score, there are proactive steps you can take to make your application more attractive to lenders. These strategies focus on reducing the lender’s perceived risk and demonstrating your capacity to repay.

1. Secure a Substantial Down Payment

This is, hands down, one of the most impactful steps you can take. A significant down payment immediately reduces the amount you need to borrow, which in turn lowers the lender’s risk. If you put down 10-20% or more of the vehicle’s price, you show a strong commitment to the purchase and a greater likelihood of repaying the loan.

Pro tips from us: Aim for at least 10% of the car’s value, but 20% is even better. This not only increases your approval chances but also reduces your monthly payments and the total interest paid over the life of the loan. It also helps prevent you from being "upside down" on your loan (owing more than the car is worth) early on.

2. Find a Reliable Co-signer

A co-signer with good credit can be a game-changer. When someone with a strong credit history co-signs your loan, they essentially promise to take over payments if you default. This provides an additional layer of security for the lender, significantly increasing your approval chances and potentially securing you a lower interest rate.

However, choosing a co-signer requires careful consideration. The co-signer is equally responsible for the debt, and any missed payments will negatively impact their credit score as well as yours. Common mistakes to avoid are not discussing the responsibilities thoroughly with your co-signer or taking advantage of their good faith. Ensure both parties understand the full implications.

3. Explore Dealership Financing, Including "Buy Here Pay Here" (BHPH) Options

Many dealerships have their own financing departments or work with a network of lenders, including subprime lenders who specialize in bad credit loans. These lenders are often more willing to work with individuals with lower credit scores.

"Buy Here Pay Here" (BHPH) dealerships are another option, particularly for those with very low scores. These dealerships typically finance the loan in-house, making the approval process quicker and often less stringent regarding credit checks. However, BHPH loans often come with significantly higher interest rates and less favorable terms. It’s crucial to approach BHPH dealers with caution, thoroughly review all terms, and only consider them if other options are exhausted.

4. Consider Credit Unions Over Traditional Banks

Credit unions are member-owned financial institutions known for their more personalized approach and often more flexible lending criteria compared to large commercial banks. Because they prioritize their members’ financial well-being, they might be more willing to work with you, even with a 530 credit score, especially if you have an existing relationship with them.

It’s worth exploring local credit unions, as they sometimes offer better rates and terms for bad credit car loans. They may look beyond just your credit score and consider your overall financial picture, including your income stability and relationship with the institution.

5. Get Pre-Approved Before You Shop

Getting pre-approved for a car loan means a lender has reviewed your financial information and determined how much they are willing to lend you, along with an estimated interest rate. This step is incredibly beneficial for several reasons.

Firstly, it gives you a clear budget, so you know exactly what price range of vehicles you can afford. Secondly, it empowers you to negotiate with dealerships more effectively, as you walk in with your own financing in hand. Thirdly, it usually involves a "soft inquiry" on your credit (which doesn’t hurt your score) before a "hard inquiry" for the final loan. This allows you to compare offers without multiple hits to your credit.

6. Opt for a More Affordable, Used Vehicle

While a brand new car might be tempting, choosing a reliable, less expensive used vehicle is a smart move when you have a 530 credit score. A lower overall loan amount reduces the risk for the lender, making them more likely to approve your application.

Additionally, a lower purchase price means lower monthly payments, which is crucial for ensuring you can consistently make payments on time. This consistency is vital for rebuilding your credit score moving forward. Focus on reliability and affordability over luxury.

7. Provide Proof of Stable Income and Employment

Lenders want to see evidence that you have a consistent and sufficient income to cover your car payments. Bring recent pay stubs, bank statements, and employment verification letters to your loan application.

Demonstrating stability in your employment and income history helps to offset the risk associated with your low credit score. The longer you’ve been at your current job, the better it looks to lenders.

8. Scrutinize and Correct Your Credit Report

Based on my experience, one of the most overlooked first steps for anyone with bad credit is to thoroughly review their credit report. Errors on your credit report are surprisingly common and can drag down your score unfairly. You are entitled to a free credit report from each of the three major bureaus (Experian, Equifax, and TransUnion) once a year via AnnualCreditReport.com.

Carefully examine every entry for inaccuracies: incorrect account balances, accounts you don’t recognize, or late payments that were actually on time. Dispute any errors immediately with the credit bureau and the creditor. Removing even one significant error can sometimes bump your score up enough to improve your loan terms.

What to Expect During the Loan Process and Beyond

Even with strategic preparation, the lending process with a 530 credit score will have specific characteristics you need to be aware of.

Higher Interest Rates (APR)

As mentioned, higher Annual Percentage Rates (APRs) are a given. While someone with excellent credit might get an APR of 3-5%, you could be looking at rates in the double digits, sometimes even 15-25% or higher, depending on the lender and market conditions. This is the cost of borrowing with a higher risk profile. Focus on getting approved, making timely payments, and then refinancing once your credit improves.

Potentially Shorter or Longer Loan Terms

Some subprime lenders might offer shorter loan terms (e.g., 36-48 months) to reduce their risk exposure, leading to higher monthly payments. Others might extend the term (e.g., 72 months) to make monthly payments more affordable, but this means you’ll pay significantly more interest over the life of the loan. Carefully evaluate the total cost of the loan, not just the monthly payment.

Additional Fees

Be prepared for potential origination fees, document fees, or other charges that might be added to your loan. Always ask for a full breakdown of all costs associated with the loan.

The Importance of Reading the Fine Print

This cannot be stressed enough. Common mistakes to avoid are rushing through the loan documents and signing without fully understanding every clause. Pay close attention to the APR, total loan amount, loan term, any prepayment penalties, and late payment fees. If anything is unclear, ask for clarification.

Beyond the Loan: Rebuilding Your Credit for a Brighter Future

Getting a car loan with a 530 credit score isn’t just about getting the car; it’s a golden opportunity to begin rebuilding your credit history. This loan, if managed responsibly, can be a powerful tool for financial recovery.

1. Make Every Payment On Time, Every Time

This is the single most important action you can take. Payment history accounts for 35% of your FICO score. Consistent, on-time payments demonstrate reliability to credit bureaus and future lenders. Set up automatic payments or calendar reminders to ensure you never miss a due date.

2. Keep Your Credit Utilization Low (on other credit products)

While your car loan doesn’t directly impact utilization in the same way revolving credit does, maintaining low balances on any credit cards you might have is crucial. High utilization (using a large percentage of your available credit) can drag down your score.

3. Monitor Your Credit Report Regularly

Continue to check your credit reports periodically for any new errors or suspicious activity. As your score begins to improve, you’ll want to track that progress.

4. Consider Refinancing When Your Credit Improves

Once you’ve made 6-12 months of on-time payments, and your credit score has seen some improvement (even 50-100 points can make a difference), consider refinancing your car loan. A better credit score can qualify you for a significantly lower interest rate, reducing your monthly payment and the total cost of the loan. This is a pro tip that many people overlook!

Common Mistakes to Avoid When Seeking a Car Loan with Bad Credit

Navigating the subprime lending market requires vigilance. Avoiding these common pitfalls can save you money and protect your credit score.

- Applying to Too Many Lenders: Each "hard inquiry" on your credit report can slightly lower your score. While credit scoring models often treat multiple auto loan inquiries within a short period (typically 14-45 days) as a single inquiry, it’s still best to be strategic. Use pre-qualification tools that use soft inquiries first.

- Not Budgeting for the Total Cost of Ownership: Beyond the monthly car payment, remember to factor in insurance, fuel, maintenance, and potential repair costs. A car is an ongoing expense, and neglecting these can lead to financial strain and missed payments.

- Settling for the First Offer: Even with bad credit, it’s wise to compare offers from a few different lenders if possible. Don’t feel pressured to take the very first deal presented to you.

- Buying More Car Than You Can Afford: This is perhaps the biggest mistake. Stretching your budget to get a fancier car puts you at a higher risk of default, which will further damage your credit. Focus on a reliable vehicle that fits comfortably within your budget.

Conclusion: Your Path to Car Ownership and Improved Credit

While securing a car loan with a 530 credit score presents considerable challenges, it is by no means an impossible feat. It requires a well-thought-out strategy, a clear understanding of your financial situation, and a proactive approach to addressing lender concerns. By focusing on a substantial down payment, exploring co-signer options, researching subprime lenders and credit unions, and being diligent about your credit report, you significantly enhance your chances of approval.

Remember, this car loan isn’t just about getting from point A to point B; it’s an opportunity to rebuild your financial standing. By making consistent, on-time payments, you’re not only fulfilling your loan obligation but actively paving the way for a healthier credit score. This improved score will open doors to better financial opportunities in the future, including lower interest rates on subsequent loans and credit products.

So, take a deep breath, gather your documents, and approach this process with patience and determination. Your journey to car ownership and improved credit starts now. For more tips on how to boost your credit score, check out our guide on . You might also find our article on helpful in navigating the terms you’re offered. For official guidance on managing your finances, the Consumer Financial Protection Bureau offers excellent resources at .