Navigating the Road Ahead: Can You Get a Car Loan with a 560 Credit Score?

Navigating the Road Ahead: Can You Get a Car Loan with a 560 Credit Score? Carloan.Guidemechanic.com

Embarking on the journey to purchase a new vehicle is an exciting prospect for many. However, for individuals with a credit score of 560, the path can often seem fraught with obstacles and uncertainty. A 560 credit score falls firmly into the "poor" or "subprime" category, signaling to lenders that there might be a higher risk involved in extending credit.

But here’s the crucial question that often weighs heavily: Can you get a car loan with a 560 credit score? The short answer is yes, it is absolutely possible. However, the longer, more nuanced answer involves understanding the realities of such a loan, preparing strategically, and being ready to navigate specific challenges. This comprehensive guide will equip you with the knowledge, strategies, and insights needed to increase your chances of approval and secure the best possible terms, even with a less-than-stellar credit history.

Navigating the Road Ahead: Can You Get a Car Loan with a 560 Credit Score?

Understanding What a 560 Credit Score Means for Lenders

Before diving into the "how-to," it’s vital to grasp the implications of your 560 credit score. In the eyes of most traditional lenders, a 560 FICO score places you squarely in the "high-risk" bracket. This score indicates a history that may include late payments, collections, high credit utilization, or even past bankruptcies, making lenders cautious about your ability to repay new debt.

Lenders use credit scores to assess the likelihood of a borrower defaulting on a loan. A lower score suggests a higher probability of default, which means they will either deny your application or offer terms that reflect this elevated risk. These terms typically include significantly higher interest rates and potentially shorter loan durations, leading to higher monthly payments.

The Reality: Getting a Car Loan with a 560 Score is Possible, But With Caveats

Let’s be clear: getting a car loan with a 560 credit score is not a pipe dream. Many people in similar situations successfully secure auto financing every day. The key difference lies in managing your expectations and understanding that the terms will likely be less favorable than those offered to borrowers with excellent credit.

You will almost certainly face higher Annual Percentage Rates (APRs), which translate to a greater total cost over the life of the loan. Furthermore, lenders might approve you for a lower loan amount, requiring you to consider more affordable vehicle options. It’s a trade-off, but with the right approach, you can still drive away in a reliable vehicle.

Key Strategies to Significantly Improve Your Chances of Approval

Securing a car loan with a 560 credit score requires a proactive and strategic approach. You need to present yourself as the most reliable borrower possible, despite your credit history. Here are some proven strategies to help you tip the scales in your favor.

1. Build a Strong Down Payment

This is arguably one of the most impactful steps you can take. A substantial down payment directly reduces the amount you need to borrow, which in turn lowers the lender’s risk. When a lender sees that you’re willing to put a significant amount of your own money upfront, it demonstrates commitment and financial responsibility, even with a challenging credit score.

Based on my experience working with countless individuals, aiming for at least 15-20% of the vehicle’s purchase price as a down payment can dramatically improve your approval odds. For example, on a $15,000 car, a $2,250 to $3,000 down payment makes a powerful statement. It tells the lender that you have skin in the game and are less likely to default on the remaining loan balance.

A larger down payment also has the added benefit of reducing your monthly payments and the total interest paid over the life of the loan. It can even help you secure a slightly better interest rate, as the loan-to-value (LTV) ratio becomes more attractive to lenders. Start saving early and aggressively; every dollar you put down lessens your future burden.

2. Find a Reliable Cosigner

Having a cosigner with excellent credit can be a game-changer when you have a 560 credit score. A cosigner essentially guarantees the loan, promising to make payments if you default. This significantly reduces the risk for the lender, as they now have two individuals legally responsible for the debt.

A good cosigner should have a strong credit score (typically 700+), a stable income, and a low debt-to-income ratio. This individual acts as a financial safeguard, making your application much more appealing to lenders who might otherwise hesitate due to your credit history. The presence of a financially secure cosigner can unlock better interest rates and more favorable loan terms.

Pro tips from us: Choosing a cosigner is a serious decision that carries significant responsibility for both parties. Ensure you have an open and honest conversation about the commitment involved, the risks to their credit, and your plan for making timely payments. Remember, if you miss payments, it negatively impacts both your credit and theirs.

3. Shop Around for Lenders – Don’t Settle for the First Offer

One of the common mistakes to avoid is walking into a dealership and taking the first financing offer presented. With a 560 credit score, you need to be a savvy shopper and explore multiple lending avenues. Different lenders have varying criteria and risk appetites, so what one bank denies, another might approve.

Consider applying to a range of institutions:

- Credit Unions: Often more lenient and community-focused, credit unions may offer better rates and terms to members, even with lower credit scores.

- Online Lenders: Many online platforms specialize in subprime auto loans and can offer quick pre-approvals, allowing you to compare offers without impacting your credit score multiple times (if done within a short shopping window).

- Dealerships with Special Finance Departments: Some dealerships have dedicated teams that work with a network of subprime lenders. While convenient, always compare their offers with those you’ve secured independently.

- Buy Here Pay Here (BHPH) Dealerships: These dealerships finance their own loans in-house. They are often a last resort for those with very poor credit and can come with extremely high interest rates and less consumer protection. Use them cautiously and only after exploring all other options.

Seek pre-approval from several lenders before you even step foot on a car lot. This gives you concrete offers to compare and provides leverage during negotiations. It also separates the financing process from the car selection process, allowing you to focus on getting the best deal for each.

4. Focus on Affordable and Reliable Vehicles

With a 560 credit score, managing your expectations about the type of vehicle you can afford is crucial. Lenders will be less inclined to approve a large loan for a brand-new luxury car. Instead, focus on reliable, used vehicles that fit within a modest budget.

Aim for a car that meets your essential transportation needs without breaking the bank. A lower loan amount means lower monthly payments, which reduces your financial strain and the overall risk for the lender. Avoid unnecessary add-ons or extended warranties that inflate the loan amount, unless they are truly essential and offer exceptional value.

Consider the total cost of ownership, including insurance, maintenance, and fuel. A cheaper car might have higher insurance premiums or be less fuel-efficient. A lower purchase price combined with reasonable running costs makes your loan more sustainable and attractive to lenders.

5. Demonstrate Stability and Income

Lenders want to see evidence that you have the capacity to repay the loan, regardless of your past credit issues. Your current financial stability plays a significant role in their decision. This means showing proof of steady employment, consistent income, and a manageable debt-to-income (DTI) ratio.

Be prepared to provide pay stubs, bank statements, and employment verification. If you’ve been at your current job for a substantial period (e.g., 1-2 years), this demonstrates stability. A low DTI ratio (ideally below 40%) indicates that a reasonable portion of your income is available to cover new loan payments, making you a more attractive borrower.

If you have any side income or additional assets, be ready to present that information as well. The more evidence you can provide of your ability to make consistent payments, the better your chances of approval.

6. Consider a Secured Car Loan (if applicable)

While less common for direct car loans, some lenders might offer secured personal loans where you put up collateral (like savings or another asset) to secure the loan. This reduces the lender’s risk even further. For a car loan specifically, the car itself serves as collateral, but your ability to repay is still paramount.

In some unique cases, if you have another valuable asset, a lender might consider it as additional security, though this is rare for standard auto loans. Focus primarily on the other strategies, as they are more directly applicable to securing auto financing with a 560 credit score.

Navigating the Application Process with Confidence

Once you’ve implemented these strategies, the application process itself requires diligence and transparency.

- Gather Your Documents: Have all necessary paperwork ready: driver’s license, proof of income (pay stubs, tax returns), proof of residence (utility bills), bank statements, and any information about your cosigner (if applicable). Being prepared shows responsibility.

- Be Honest: Don’t try to hide or embellish your financial situation. Lenders will conduct their own checks. Transparency builds trust, and it’s always better to address any concerns upfront.

- Understand the Terms: Read every line of the loan agreement before signing. Pay close attention to the APR, total loan amount, monthly payment, loan term, and any associated fees. If something is unclear, ask questions until you fully understand.

- Beware of Predatory Lending: With a low credit score, you might encounter lenders offering "guaranteed approval" with exorbitant interest rates or hidden fees. If a deal seems too good to be true, or if you feel pressured, walk away.

Understanding the Cost: Interest Rates with a 560 Credit Score

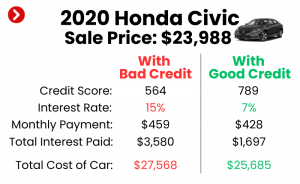

This is perhaps the most significant reality check for borrowers with a 560 credit score. You should expect significantly higher interest rates compared to those with excellent credit. While someone with a 720+ score might qualify for an APR below 5-7%, a borrower with a 560 score could face rates ranging from 15% to 25% or even higher, depending on the market, the lender, and other factors.

These higher rates mean that a substantial portion of your monthly payment will go towards interest, especially in the early stages of the loan. Over the life of a 5-year loan, this can add thousands of dollars to the total cost of the vehicle. For example, a $15,000 loan at 20% APR over 60 months results in approximately $8,800 in interest alone, whereas at 7% APR, it’s about $2,800.

While high, these rates might be your only option for immediate transportation. The good news is that by making on-time payments, you can gradually improve your credit score. After 12-18 months of responsible payment history, you might be able to refinance your car loan at a lower interest rate, saving you a considerable amount of money in the long run.

The Path to Rebuilding Your Credit with a Car Loan

Ironically, securing and responsibly managing a car loan can be a powerful tool for rebuilding your credit score. This is where the long-term value truly lies. By consistently making your car loan payments on time, every month, you demonstrate financial reliability to credit bureaus.

Each on-time payment contributes positively to your payment history, which is the single most important factor in your credit score (accounting for 35%). Over time, this positive activity will gradually lift your score, opening doors to better financial opportunities in the future, including lower interest rates on other loans and credit cards.

Pro tips from us: Set up automatic payments to avoid missing due dates. Consider making bi-weekly payments if your budget allows; this can sometimes help reduce the total interest paid and ensures you’re always ahead. For more tips on improving your credit score, check out our comprehensive guide on .

What to Watch Out For: Red Flags and Pitfalls

When your credit score is 560, you’re more vulnerable to less ethical lending practices. Be vigilant and aware of common red flags:

- "Guaranteed Approval" Scams: No legitimate lender can truly guarantee approval without reviewing your financial situation. These are often traps leading to extremely high interest rates, hidden fees, or unfavorable terms.

- Excessive Fees: Scrutinize all fees listed on the loan agreement. Some lenders might try to pile on unnecessary origination fees, processing fees, or administrative charges.

- Balloon Payments: Be wary of loans that have very low monthly payments initially but end with a massive "balloon" payment. If you can’t afford this final payment, you could lose your vehicle.

- Long Loan Terms for Older Cars: While a longer term means lower monthly payments, it also means paying more interest over time, especially with a high APR. Avoid extending a loan too far past the expected lifespan of the vehicle.

- Pressure Tactics: Never feel rushed or pressured into signing anything. A reputable lender will give you time to review documents and ask questions. Common mistakes to avoid include making an impulsive decision just to get a car.

Making the Right Decision for Your Future

While it’s possible to get a car loan with a 560 credit score, it’s important to ask yourself if it’s the best decision for your long-term financial health. Weigh your immediate need for transportation against the financial implications of a high-interest loan.

Could you wait a few months, save more for a down payment, and work on improving your credit score even slightly? Even a 30-50 point increase could make a difference in the interest rate offered. Alternatively, consider temporary solutions like public transport, ride-sharing, or borrowing from family if your need isn’t urgent.

The goal is not just to get a car loan, but to get a car loan that you can comfortably afford and that contributes positively to your financial future, rather than trapping you in a cycle of debt.

Conclusion: Your Roadmap to Auto Financing with a 560 Credit Score

Navigating the landscape of auto financing with a 560 credit score is undoubtedly challenging, but it is far from impossible. By understanding the nuances of subprime lending and strategically employing the tactics outlined in this guide, you can significantly increase your chances of approval.

Remember to prioritize a substantial down payment, explore the possibility of a reliable cosigner, meticulously shop around for the best lenders, and focus on affordable, practical vehicles. Your financial stability, demonstrated through consistent income and a manageable debt-to-income ratio, will also play a critical role. While you should prepare for higher interest rates, view this loan as an opportunity to rebuild your credit and unlock better financial prospects down the road.

Armed with knowledge and a proactive mindset, you can successfully secure the transportation you need while simultaneously paving the way for a stronger financial future. If you’re ready to start your car buying journey, read our article on . For a deeper understanding of how credit scores are calculated and what impacts them, visit External Link: FICO’s official website.