Navigating the Road Ahead: Car Loan Lenders With Bad Credit – Your Ultimate Guide to Approval

Navigating the Road Ahead: Car Loan Lenders With Bad Credit – Your Ultimate Guide to Approval Carloan.Guidemechanic.com

Finding yourself in need of a car but facing the hurdle of bad credit can feel like staring down a dead-end street. The modern world demands mobility, whether for work, family responsibilities, or simply maintaining your independence. Many people believe that a low credit score automatically disqualifies them from securing an auto loan. This couldn’t be further from the truth.

While challenging, getting a car loan with bad credit is absolutely achievable. It requires understanding your options, knowing what lenders look for, and approaching the process strategically. This comprehensive guide will illuminate the path, providing you with the knowledge and tools to confidently navigate the landscape of car loan lenders with bad credit, ensuring you drive away with a vehicle that meets your needs and a loan that helps rebuild your financial future.

Navigating the Road Ahead: Car Loan Lenders With Bad Credit – Your Ultimate Guide to Approval

Understanding Bad Credit and Its Impact on Car Loans

Before diving into solutions, it’s crucial to understand what "bad credit" typically means in the eyes of a lender. Your credit score, primarily FICO or VantageScore, is a three-digit number that summarizes your creditworthiness. Scores generally range from 300 to 850.

A "bad" credit score usually falls below 600, often even below 580, categorizing you as a "subprime" borrower. This indicates to lenders a higher risk of default, making them more hesitant to lend or compelling them to charge higher interest rates to offset that perceived risk. Common reasons for bad credit include missed payments, high credit card balances, collections, bankruptcies, or a limited credit history.

Why Getting a Car Loan with Bad Credit is a Unique Challenge

Lenders assess risk. When you apply for a car loan, they want to be confident that you will make your payments on time and in full. A history of financial difficulties suggests a higher likelihood of missed payments, which directly impacts their bottom line. This doesn’t mean you’re a lost cause, but it does mean you’ll likely encounter different loan terms and types of lenders than someone with excellent credit.

The good news is that many lenders specialize in working with individuals who have less-than-perfect credit. They understand that life happens and that a past financial stumble shouldn’t permanently bar someone from essential transportation. Our goal here is to help you identify these lenders and present yourself as the most attractive borrower possible, despite your credit history.

Dispelling Common Myths About Bad Credit Car Loans

The topic of bad credit often comes with a host of misconceptions. Let’s tackle a few head-on to ensure you approach this process with a clear and realistic mindset.

Myth 1: It’s Impossible to Get a Car Loan with Bad Credit.

This is simply untrue. While more difficult, it’s far from impossible. Many financial institutions and dealerships specialize in these types of loans, recognizing the vast market of individuals working to improve their credit.

Myth 2: All Lenders for Bad Credit Are Predatory.

While caution is always advised, and some less reputable lenders exist, many legitimate lenders offer fair, albeit higher-interest, loans to bad credit borrowers. The key is knowing how to identify reputable lenders and understand the terms.

Myth 3: You’ll Be Stuck with Exorbitant Interest Rates Forever.

While initial rates will likely be higher, successfully managing a bad credit car loan can significantly improve your credit score over time. This opens the door to refinancing at a lower rate in the future or securing better terms on subsequent loans. It’s an opportunity to rebuild.

Types of Lenders for Bad Credit Car Loans

Navigating the various types of lenders is perhaps the most crucial step for anyone seeking a car loan with bad credit. Not all lenders are created equal, and understanding their unique approaches can save you time and money.

1. Subprime Lenders (Specialty Auto Finance Companies)

These are financial institutions specifically designed to work with borrowers who have lower credit scores. They often have more flexible underwriting criteria compared to traditional banks. They understand that a low credit score might not tell the whole story and will look at other factors like income stability and employment history more closely.

- How they operate: Subprime lenders assess a higher risk and therefore typically charge higher interest rates. However, they are more willing to approve loans that traditional banks would deny. They often have established relationships with a network of dealerships.

- Pros: Higher approval rates for bad credit, often quick decisions, access to a wider range of vehicles through their dealer networks.

- Cons: Higher interest rates, potentially longer loan terms (leading to more interest paid overall), some may have less flexible terms.

- Pro Tip from us: When dealing with subprime lenders, always scrutinize the Annual Percentage Rate (APR) and the total cost of the loan. Don’t just focus on the monthly payment.

2. Dealership Financing (Including "Buy Here, Pay Here" Lots)

Many dealerships offer in-house financing, acting as the lender themselves or working with a network of external lenders, including subprime ones. "Buy Here, Pay Here" (BHPH) lots are a specific type of dealership where the dealer is also the lender, and you make your payments directly to them.

- How they operate: Dealerships can often provide convenience, offering a "one-stop shop" experience where you can select a car and secure financing at the same location. BHPH lots are often seen as a last resort due to their typically very high interest rates and often older, less reliable inventory.

- Pros: Convenience, high approval rates (especially BHPH), can often work with very poor credit, may not perform a hard credit inquiry initially.

- Cons: Often much higher interest rates, limited car selection (especially BHPH), less transparent terms, BHPH loans sometimes don’t report to credit bureaus (meaning it won’t help rebuild your credit).

- Based on my experience: While convenient, BHPH lots should be approached with extreme caution. Always try to explore other options first. If you do go this route, ensure they report payments to all three major credit bureaus so your on-time payments can actually help your credit score.

3. Online Lenders and Marketplaces

The digital age has brought a new wave of lenders and platforms that specialize in connecting borrowers with various financing options, including those for bad credit. These platforms often work with a network of lenders and can provide multiple offers for comparison.

- How they operate: You fill out one application online, and the platform then matches you with lenders who are likely to approve your loan based on your credit profile. This allows for quick comparisons without multiple hard inquiries on your credit report.

- Pros: Convenience (apply from home), ability to compare multiple offers easily, potentially faster approval process, often a wider range of lenders to choose from.

- Cons: Requires careful reading of terms and conditions for each offer, some online lenders may have less personalized service.

- Internal Link: To learn more about how online applications impact your credit score, you might find our article on "Understanding Credit Inquiries: Soft vs. Hard Pulls" helpful.

4. Credit Unions

Credit unions are non-profit financial cooperatives owned by their members. They are known for their member-centric approach and often offer more flexible lending criteria than traditional banks, especially to existing members.

- How they operate: If you’re already a member of a credit union, or if you can join one (often based on location, employer, or association), they may be more willing to work with you even with bad credit. They tend to look at the "whole picture" of your financial situation.

- Pros: Often lower interest rates than other bad credit lenders, more personalized service, potential for more flexible terms, may be more understanding of past financial issues.

- Cons: Requires membership, may have stricter approval criteria than dedicated subprime lenders, less prevalent than banks or dealerships.

- Pro Tip from us: Check with any credit unions you are already a member of first. They often have the best rates and most understanding policies for their members.

5. Traditional Banks (with specific conditions)

Major banks like Chase, Wells Fargo, or Bank of America typically have stricter lending criteria and prefer borrowers with good to excellent credit. However, it’s not entirely impossible to secure a loan from them with bad credit, especially if certain conditions are met.

- How they operate: They might consider you if you have a significant down payment, a reliable co-signer with excellent credit, or a long-standing positive banking relationship with them.

- Pros: Potentially lower interest rates than subprime lenders if approved, established and reputable institutions.

- Cons: Very difficult to get approved with bad credit alone, often requires a strong co-signer or substantial collateral/down payment.

Key Factors Lenders Consider (Even with Bad Credit)

Even with bad credit, lenders are looking for indicators that you can and will repay your loan. Understanding these factors allows you to present yourself as the best possible candidate.

- Income Stability: Lenders want to see a steady source of income. This demonstrates your ability to make regular payments. They’ll look for consistent employment history, pay stubs, and sometimes bank statements.

- Employment History: A long, stable employment history signals reliability. Frequent job changes can be a red flag, but if you have a good reason (e.g., career advancement), be prepared to explain it.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI indicates you have more disposable income to cover a new car payment. Lenders prefer a DTI below 43%, though subprime lenders might be more flexible.

- Down Payment: A significant down payment is one of the most powerful tools for a bad credit borrower. It reduces the amount you need to borrow, thereby lowering the lender’s risk. It also shows your commitment and ability to save.

- Co-signer: Having a co-signer with good credit significantly boosts your chances of approval and can lead to better loan terms. The co-signer essentially guarantees the loan, making them equally responsible if you default.

- Vehicle Choice: Lenders view less expensive, reliable used cars as lower risk. Trying to finance a brand-new, high-value luxury car with bad credit is far more challenging than securing a loan for a more modest vehicle.

Strategies to Improve Your Chances of Approval

Don’t just apply blindly. Proactive steps can significantly enhance your approval odds and potentially secure better terms.

- Check Your Credit Report Thoroughly: Before applying anywhere, obtain copies of your credit reports from all three major bureaus (Experian, Equifax, TransUnion) via AnnualCreditReport.com. Review them for errors or inaccuracies and dispute any you find. Correcting mistakes can sometimes boost your score surprisingly quickly.

- Save for a Substantial Down Payment: As mentioned, a larger down payment (aim for at least 10-20% of the car’s value) reduces the loan amount and the lender’s risk. This can often sway a lender who might otherwise hesitate.

- Find a Reliable Co-signer: If possible, ask a trusted family member or friend with good credit to co-sign. Ensure they understand the responsibility, as any missed payments will affect their credit too.

- Get Pre-Approved: Seek pre-approval from multiple lenders. This allows you to compare offers without committing and gives you leverage at the dealership. Pre-approvals usually involve a soft credit inquiry, which doesn’t harm your score.

- Choose the Right Car: Be realistic about what you can afford and what lenders are willing to finance. Focus on reliable, used vehicles that fit within your budget.

- Gather All Necessary Documents: Be prepared with proof of income (pay stubs, bank statements), proof of residence (utility bills), driver’s license, and any other requested documents. Being organized shows you’re serious.

- Explain Your Situation (When Appropriate): If there’s a specific, explainable reason for your bad credit (e.g., medical emergency, temporary job loss), be prepared to briefly and honestly explain it to the lender. Sometimes, a human touch can make a difference.

The Application Process for a Bad Credit Car Loan

The journey to securing your car loan can be broken down into manageable steps:

Step 1: Research Lenders.

Based on the types of lenders discussed, identify a few that seem like a good fit. Look for lenders specializing in bad credit or those with good reviews for their subprime lending.

Step 2: Gather Your Documents.

Collect all necessary financial and personal documents. This includes recent pay stubs, bank statements, utility bills, driver’s license, and insurance information.

Step 3: Apply for Pre-Approval.

Start with pre-approval applications. This provides you with an estimated loan amount, interest rate, and terms without impacting your credit score significantly. This step is invaluable for setting realistic expectations.

Step 4: Compare Offers.

Once you have a few pre-approval offers, compare them carefully. Look beyond just the monthly payment. Focus on the APR, the total cost of the loan over its lifetime, and any associated fees.

Step 5: Choose Your Car.

With a clear understanding of your approved loan amount, you can confidently shop for a car that fits your budget. Avoid the temptation to buy more car than you can afford.

Step 6: Finalize the Loan.

Once you’ve found the right car, you’ll finalize the loan with your chosen lender, complete all paperwork, and drive away. Ensure you understand every clause before signing.

Understanding Your Loan Terms (Crucial for Bad Credit)

When you have bad credit, understanding the fine print of your loan agreement is paramount. Higher risk often means different terms, and you need to be fully aware of what you’re agreeing to.

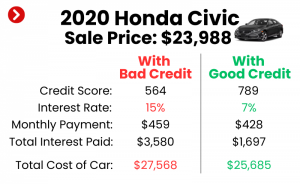

- Interest Rates (APR): For bad credit borrowers, interest rates (Annual Percentage Rate) will be significantly higher than for those with good credit. This is how lenders compensate for the increased risk. A 20%+ APR is not uncommon. Understand that a higher APR means you pay much more over the life of the loan. Use an online calculator to see the total interest paid.

- Loan Term (Length): While longer loan terms (e.g., 72 or 84 months) result in lower monthly payments, they also mean you pay more interest over time and potentially risk being "upside down" on your loan (owing more than the car is worth). Based on my experience, aim for the shortest loan term you can comfortably afford.

- Fees: Be aware of any origination fees, documentation fees, or other charges that might be added to the loan. These can subtly increase your total cost.

- Prepayment Penalties: Some loans include penalties for paying off your loan early. While less common now, always check for this. You want the flexibility to pay it off faster if your financial situation improves.

Pro Tip from us: Never sign a loan agreement you don’t fully understand. Ask questions until you are completely clear on every term. Don’t be pressured into signing quickly.

Common Mistakes to Avoid When Seeking a Bad Credit Car Loan

Making the wrong moves can set you back further. Be aware of these common pitfalls:

- Applying Everywhere: Each hard credit inquiry can slightly lower your credit score. Bunch your applications within a 14-45 day window so they count as a single inquiry for scoring purposes.

- Not Checking Your Credit Report: Blindly applying without knowing your credit standing is a missed opportunity to correct errors and understand your position.

- Ignoring the Total Cost of the Loan: Focusing solely on the monthly payment can be deceptive. A low monthly payment over a very long term can mean paying significantly more in interest.

- Buying More Car Than You Can Afford: It’s tempting to stretch your budget, but an unaffordable car payment is a direct path to defaulting and worsening your credit.

- Rushing the Decision: Take your time to compare offers, read reviews, and understand terms. A car loan is a significant financial commitment.

- Falling for Predatory Offers: If an offer seems too good to be true, it probably is. Be wary of lenders promising guaranteed approval without any credit check or those demanding excessive fees upfront.

- Neglecting Insurance Costs: Remember to factor in car insurance, which can be higher for newer vehicles and for drivers with a history of bad credit.

Beyond the Loan: Building Better Credit for the Future

Securing and successfully managing a bad credit car loan is a golden opportunity to rebuild your credit and improve your financial standing. This isn’t just about getting a car now; it’s about setting yourself up for a better financial future.

- Make On-Time Payments, Every Time: This is the single most important factor in improving your credit score. Set up automatic payments to ensure you never miss a due date.

- Reduce Other Debts: As you manage your car loan, also work on reducing other high-interest debts like credit card balances. A lower debt-to-income ratio is always favorable.

- Monitor Your Credit: Keep an eye on your credit score and report regularly. You can often get free scores from your bank or credit card companies.

- Consider Credit-Builder Tools: Once your car loan is stable, you might explore secured credit cards or credit-builder loans to further diversify your credit mix.

- The Future Benefit: A successfully paid-off car loan will be a positive entry on your credit report for years, demonstrating your reliability to future lenders. This can lead to lower interest rates on mortgages, personal loans, and even future auto loans.

External Link: For more detailed guidance on improving your credit score, the Consumer Financial Protection Bureau (CFPB) offers excellent resources at consumerfinance.gov.

Conclusion: Your Road to Car Ownership with Bad Credit is Open

Having bad credit doesn’t mean you’re permanently sidelined from car ownership. It simply means you need a more informed and strategic approach. By understanding the types of car loan lenders with bad credit, preparing yourself thoroughly, and diligently comparing offers, you can secure the financing you need.

Remember to prioritize your financial stability, choose a car that fits your budget, and use this opportunity to build a stronger credit future. The road ahead may have a few more turns, but with this guide, you’re well-equipped to navigate them successfully and drive towards your goals. Don’t let past financial challenges define your future mobility. Start your research today, empower yourself with knowledge, and take the first step towards securing your next vehicle.