Navigating the Road Ahead: How Long Are Used Car Loans, and What’s Right for You?

Navigating the Road Ahead: How Long Are Used Car Loans, and What’s Right for You? Carloan.Guidemechanic.com

Embarking on the journey to purchase a used car is an exciting prospect, offering fantastic value and a wide array of choices. However, for many, the path to ownership involves securing a used car loan, and one of the most critical questions that arises is: "How long are used car loans typically, and what loan term makes the most sense for my financial situation?"

As an expert blogger and someone deeply entrenched in the automotive finance world, I can tell you that understanding used car loan lengths isn’t just about the monthly payment. It’s about the total cost, your financial flexibility, and the long-term health of your wallet. This comprehensive guide will demystify used car loan terms, helping you make an informed decision that drives you towards financial success. We’ll explore the common lengths, the factors that influence them, and crucial insights to help you choose wisely.

Navigating the Road Ahead: How Long Are Used Car Loans, and What’s Right for You?

What Exactly Is a Used Car Loan Term?

Before we dive into the specifics of duration, let’s clarify what a "loan term" actually means. Simply put, the loan term is the length of time you have to repay the money you’ve borrowed to purchase your used vehicle. This period is typically expressed in months, such as 36, 48, 60, or even 72 months.

Each month, you’ll make a scheduled payment that includes both a portion of the principal (the original amount borrowed) and the interest accrued. The longer the loan term, the more months you have to spread out these payments, which generally results in lower individual monthly installments. Conversely, a shorter term means higher monthly payments but fewer months of interest accumulation.

The "Standard" Landscape: Common Used Car Loan Lengths

Unlike new car loans, which often stretch to 72 or even 84 months, used car loan terms tend to be a bit shorter. This is primarily due to the depreciation rate and the expected lifespan of a pre-owned vehicle. Lenders are more cautious with older cars, as their value can decline more rapidly, and they might have a higher risk of mechanical issues.

Based on my experience working with countless car buyers, the most common loan terms for used vehicles typically fall into a few key categories. While there’s no single "standard," you’ll most frequently encounter options ranging from 36 to 72 months. Occasionally, for very recent models or certified pre-owned vehicles, an 84-month term might be available, but this is less common and often comes with stricter requirements.

Key Factors Influencing Your Used Car Loan Length

The length of the used car loan you qualify for, and ultimately choose, isn’t a random number. Several critical factors come into play, influencing both what lenders offer and what makes financial sense for you. Understanding these elements is crucial for navigating the loan application process effectively.

1. The Age and Mileage of the Used Car

This is arguably the most significant factor affecting used car loan terms. Lenders evaluate the risk associated with the vehicle itself. An older car with high mileage is generally perceived as a higher risk because it has a shorter expected lifespan, higher potential for mechanical problems, and will likely depreciate faster.

Consequently, lenders are often reluctant to offer very long loan terms for these vehicles. You might find that a car over, say, eight years old or with more than 100,000 miles, will be capped at a 36 or 48-month loan. Newer used cars, perhaps 1-3 years old, with lower mileage, will typically qualify for longer terms, mirroring options available for new vehicles.

2. The Total Loan Amount

Naturally, the amount of money you need to borrow plays a role. A smaller loan amount, perhaps for an inexpensive used car, might encourage a shorter loan term to minimize the total interest paid. Conversely, if you’re financing a significant portion of a higher-value used vehicle, a longer term might be necessary to make the monthly payments affordable.

However, lenders also have minimum and maximum loan amounts they are willing to finance for certain terms. Always ensure the loan amount aligns with the car’s actual value to avoid being upside down on your loan.

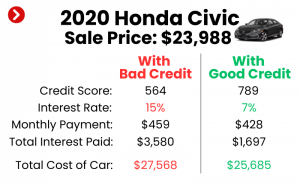

3. Your Credit Score

Your creditworthiness is a cornerstone of any loan application. A strong credit score signals to lenders that you are a reliable borrower with a history of responsible debt management. Borrowers with excellent credit (generally FICO scores of 720+) will have access to the best interest rates and the widest range of loan terms, including the longest options available.

Conversely, a lower credit score might limit your options, forcing you into shorter terms or higher interest rates, or both. Lenders might view you as a higher risk, and a shorter term helps them recover their investment more quickly. for more detailed advice on boosting your credit.

4. Your Down Payment

The amount of money you put down upfront significantly impacts your loan. A larger down payment reduces the total amount you need to borrow, which can open up more flexible loan term options. It also demonstrates your commitment to the purchase and reduces the lender’s risk.

Based on my experience, a substantial down payment can often help you secure a longer term with a better interest rate, or conversely, allow you to choose a shorter term with a very manageable monthly payment. It’s a powerful tool in your financing arsenal.

5. The Interest Rate

While not a direct determinant of loan length, the interest rate you qualify for heavily influences the attractiveness of different loan terms. A low interest rate makes a longer loan term less financially burdensome because the total interest paid doesn’t skyrocket as much. Conversely, a high interest rate makes longer terms very expensive, often pushing borrowers towards shorter terms to minimize overall costs.

Always remember that the interest rate directly impacts the total amount you will pay over the life of the loan. for an in-depth explanation of how interest works.

6. Lender Policies and Programs

Every lender has its own set of criteria, risk assessment models, and specific loan products. Some lenders specialize in longer terms, while others prefer shorter ones, especially for used vehicles. Dealerships often work with multiple lenders, each with different offerings.

Pro tips from us: Always shop around and compare offers from various banks, credit unions, and online lenders. Don’t just accept the first offer you receive; different lenders might have different caps on loan terms for specific vehicle ages or credit profiles.

7. Your Personal Financial Goals

Beyond what lenders offer, your own financial objectives should heavily influence your chosen loan length. Are you looking to minimize monthly expenses at all costs? Or is your priority to pay off debt quickly and reduce total interest? Your personal financial strategy is a crucial, often overlooked, factor.

Consider your future plans: Do you anticipate a pay raise, or a new expense? Will you keep this car for a long time, or upgrade in a few years? These considerations should guide your decision.

Exploring Common Used Car Loan Lengths: Pros and Cons

Now that we understand the influencing factors, let’s break down the most common loan terms you’ll encounter for used cars and weigh their advantages and disadvantages.

1. Short-Term Loans (e.g., 24-48 Months)

These terms are generally preferred by financially savvy buyers who prioritize minimizing interest paid and becoming debt-free quickly.

- Pros:

- Significantly Lower Total Interest Paid: This is the biggest advantage. By paying off the loan faster, you spend less money on interest over the loan’s life.

- Faster Equity Build-Up: You’ll own your car outright sooner, building equity more rapidly. This is beneficial if you plan to trade in the vehicle in a few years.

- Less Risk of Being "Upside Down": You’re less likely to owe more on the car than it’s worth, which is a common problem with longer terms and depreciating assets.

- Peace of Mind: Being debt-free sooner offers significant financial freedom.

- Cons:

- Higher Monthly Payments: This is the trade-off. Shorter terms mean larger installments each month, which might strain tighter budgets.

- Less Financial Flexibility: Higher payments leave less discretionary income, potentially impacting your ability to save or cover unexpected expenses.

2. Medium-Term Loans (e.g., 48-60 Months)

Often considered the "sweet spot" for many used car buyers, medium-term loans offer a balance between affordability and total cost.

- Pros:

- Balanced Monthly Payments: These terms strike a good compromise, making payments manageable for many budgets without drastically increasing total interest.

- Manageable Total Cost: While you’ll pay more interest than a short-term loan, it’s significantly less than a very long-term option.

- Good for Mid-Range Vehicles: This term length often aligns well with the expected lifespan and depreciation of many used cars.

- Cons:

- Still Higher Monthly Payments than Long Terms: If budget is extremely tight, even 60 months might feel like a stretch.

- Slower Equity Build-Up: While better than longer terms, it still takes a few years to build significant equity.

3. Long-Term Loans (e.g., 60-72 Months, sometimes 84 Months for Newer Used Cars)

These terms have become increasingly popular due to their ability to provide the lowest possible monthly payments. However, they come with significant financial considerations.

- Pros:

- Lowest Monthly Payments: This is the primary draw, making higher-priced used cars seem more affordable on a month-to-month basis.

- Greater Financial Flexibility (Monthly): Lower payments free up more cash flow for other expenses or savings each month.

- Cons:

- Highest Total Interest Paid: You will pay significantly more in interest over the life of the loan. This is the biggest hidden cost of long terms.

- High Risk of Being "Upside Down": As cars depreciate, especially used ones, you’re very likely to owe more than the car is worth for a significant portion of the loan term. This becomes a major problem if you need to sell the car or if it’s totaled.

- Longer Debt Period: You’ll be making car payments for many years, tying up a portion of your income that could be used for other financial goals.

- Potential for Mechanical Issues Outlasting Warranty/Loan: With older used cars, a 72-month loan means you could still be paying for the car long after its warranty has expired and potentially when major repairs are needed.

The Trade-Off: Shorter vs. Longer Loan Terms

Understanding the raw pros and cons is one thing; internalizing the core trade-off is another. It boils down to this: monthly affordability versus total cost.

A shorter loan term means you pay more each month, but you pay less overall. This is because you’re accruing interest for a shorter period. Think of it as a sprint – intense but over quickly.

A longer loan term means you pay less each month, but you pay more overall. The extended repayment period gives interest more time to accumulate, significantly increasing the total amount you hand over to the lender. This is more like a marathon – less intense monthly, but a much longer journey with a higher cumulative effort.

Common mistakes to avoid are focusing solely on the monthly payment. While it’s important for your budget, it doesn’t tell the whole story. Always ask for the total cost of the loan, including all interest and fees, for different term lengths. You might be surprised at the difference.

How to Choose the Right Used Car Loan Length for YOU

With all this information, how do you pinpoint the best loan term for your specific situation? It requires a careful assessment of your personal finances and future plans.

1. Assess Your Current Budget Realistically

Start by creating a detailed budget. How much disposable income do you truly have each month for a car payment, insurance, fuel, and maintenance? Don’t just look at what you can afford, but what you should afford without feeling financially strained.

Pro tips from us: Aim for a car payment that is no more than 10-15% of your net monthly income. This leaves room for other essentials and unexpected costs.

2. Consider the Car’s Expected Longevity and Your Ownership Plans

How long do you realistically plan to keep this used car? If you typically upgrade every 3-4 years, a 72-month loan makes little sense, as you’ll likely still owe money when you want to trade it in. If you plan to drive the car until its wheels fall off, a slightly longer term might be acceptable if it means a significantly lower interest rate.

Match your loan term to your ownership horizon. Ideally, you want to pay off the car before its major components start failing or before you’re ready for an upgrade.

3. Evaluate Your Financial Stability and Future Outlook

Are you in a stable job? Do you anticipate major life changes soon, such as starting a family, buying a house, or going back to school? Your financial stability should play a huge role. If your income is variable or uncertain, opting for a shorter term with higher payments could be risky.

From years of advising car buyers, I’ve seen that unexpected life events can quickly turn an "affordable" long-term payment into a burden. Build in a buffer.

4. Calculate the Total Cost for Different Scenarios

Don’t guess. Use online loan calculators to compare the total cost (principal + interest) for various loan terms at the interest rate you’re likely to qualify for. Seeing the numbers laid out clearly can be a powerful motivator.

For example, a $20,000 loan at 6% interest over 48 months might cost you around $22,500 total, while the same loan over 72 months could cost over $23,800. That’s a significant difference for the same car.

Pro Tips for Securing the Best Used Car Loan Term

Beyond choosing the right length, there are strategic moves you can make to improve your overall loan experience.

- Improve Your Credit Score: As mentioned, a higher credit score unlocks better rates and more favorable terms. Pay bills on time, reduce outstanding debt, and check your credit report for errors before applying.

- Save for a Larger Down Payment: A substantial down payment reduces the loan amount, lowers your monthly payments, and often helps you secure a better interest rate and more flexible terms.

- Shop Around for Lenders (Get Pre-Approved): Don’t limit yourself to the dealership’s financing options. Get pre-approved by a few different banks and credit unions before you even step onto the lot. This gives you leverage and a benchmark to compare against.

- Negotiate the Car Price, Not Just the Payment: Always negotiate the total price of the car first. A lower purchase price means you need to borrow less, which naturally improves your loan options.

- Understand All Terms and Conditions: Read the fine print! Be aware of any prepayment penalties, late fees, or other clauses in the loan agreement.

Common Mistakes to Avoid When Taking Out a Used Car Loan

Many car buyers fall into common traps that can lead to financial regret. Avoid these pitfalls:

- Focusing Only on the Monthly Payment: This is the most prevalent mistake. A low monthly payment can mask a very expensive long-term loan. Always look at the total cost.

- Ignoring the Total Cost of the Loan: As discussed, the total interest paid can add thousands to the price of your car. This hidden cost is crucial.

- Not Checking Your Credit Score Beforehand: Going into loan applications blind can lead to disappointment and multiple credit inquiries, which can temporarily ding your score.

- Buying More Car Than You Can Afford: It’s easy to get caught up in the excitement of a nicer car, but don’t stretch your budget to the breaking point. The stress isn’t worth it.

- Skipping Pre-Approval: Without pre-approval, you lose significant negotiation power at the dealership and might end up with a less favorable loan.

Conclusion: Driving Towards a Smart Financial Future

Determining "how long are used car loans" is more than just a quick answer; it’s a decision that profoundly impacts your financial well-being for years to come. While common terms range from 36 to 72 months, the ideal length for you will depend on a careful balance of your budget, the car’s characteristics, your credit profile, and your personal financial goals.

By understanding the factors at play, weighing the pros and cons of different terms, and avoiding common mistakes, you can make a choice that not only gets you behind the wheel of your desired used car but also sets you on a path to a smarter, more secure financial future. Drive confidently, and drive wisely!