Navigating the Road Ahead: Securing a Car Loan with a 450 Credit Score

Navigating the Road Ahead: Securing a Car Loan with a 450 Credit Score Carloan.Guidemechanic.com

Embarking on the journey to purchase a car is an exciting prospect for many. However, for those with a credit score hovering around 450, the path can seem daunting, riddled with uncertainty and potential rejections. A 450 credit score places you firmly in the "Very Poor" category, signaling a significant challenge when seeking traditional financing. Yet, the dream of car ownership doesn’t have to be out of reach.

As an expert blogger and professional SEO content writer, I understand the complexities of bad credit auto loans. My mission with this comprehensive guide is to provide you with an honest, in-depth, and actionable roadmap to navigate the landscape of securing a 450 credit score car loan. We will explore realistic expectations, uncover practical strategies, and empower you with the knowledge to make informed decisions, ultimately setting you on a path not just to car ownership, but to financial recovery.

Navigating the Road Ahead: Securing a Car Loan with a 450 Credit Score

Understanding What a 450 Credit Score Truly Means

Before we delve into financing options, it’s crucial to grasp the gravity of a 450 credit score. In the FICO scoring model, scores range from 300 to 850. A score of 450 sits at the very low end, indicating a substantial history of financial difficulties. This isn’t just a number; it’s a summary of your past financial behavior.

Lenders view a 450 credit score as a high-risk indicator. It suggests a borrower who has struggled to meet financial obligations in the past, potentially due to multiple late payments, defaults, collections, or even bankruptcy. From a lender’s perspective, this history raises concerns about your ability and willingness to repay a new loan. Consequently, they anticipate a higher likelihood of default, which significantly impacts their lending decisions.

Based on my experience in the financial landscape, a 450 credit score often stems from a series of unfortunate events or a prolonged period of financial mismanagement. It’s not uncommon to see individuals in this range who have faced job loss, medical emergencies, or significant life changes that led to missed payments. Understanding the root cause of your low score can be the first step towards addressing it and building a stronger financial future.

Is a Car Loan with a 450 Credit Score Even Possible? The Reality Check

Let’s be upfront: securing a traditional car loan with a 450 credit score is exceedingly difficult, if not impossible, through conventional banks and credit unions. These institutions typically cater to borrowers with good to excellent credit, as their business model is built on low-risk lending. However, this doesn’t mean all hope is lost.

The good news is that specialized lenders exist who focus specifically on subprime auto loans. These are financial institutions and dealerships that are willing to take on the higher risk associated with borrowers who have less-than-perfect credit. They understand that everyone deserves a second chance and that life events can impact credit scores beyond a borrower’s control. Their lending criteria are different, often placing more emphasis on your current income and stability rather than solely on your past credit history.

Common mistakes to avoid are believing that "guaranteed approval" advertisements are always legitimate or that you’ll qualify for prime interest rates. These are often misleading. While some lenders specialize in bad credit, there’s no such thing as truly "guaranteed" approval without any qualification. Furthermore, due to the increased risk, any loan you do secure will likely come with significantly higher interest rates and less favorable terms than what someone with good credit would receive. Managing these expectations from the outset is vital for a successful outcome.

Key Strategies to Dramatically Improve Your Chances of Approval

While a 450 credit score presents challenges, there are powerful strategies you can employ to significantly boost your likelihood of approval. These methods are designed to mitigate the perceived risk for lenders and demonstrate your commitment to repayment.

The Undeniable Power of a Substantial Down Payment

One of the most effective ways to make yourself a more attractive borrower, even with a low credit score, is to offer a significant down payment. A down payment reduces the amount of money you need to borrow, which in turn reduces the lender’s risk. If you default on the loan, the lender has less to lose because a larger portion of the car’s value has already been paid.

Based on my experience, lenders look favorably upon a strong down payment because it shows financial commitment and capability. It signals that you have some savings, indicating a degree of financial stability. Aim for at least 10-20% of the car’s purchase price, or even more if possible. The larger your down payment, the lower your monthly payments will be, and the less interest you’ll pay over the life of the loan. This also creates immediate equity in the vehicle, which can be a safety net.

Leveraging the Advantage of a Co-Signer

Another highly effective strategy is to apply for the loan with a co-signer who has good credit. A co-signer essentially acts as a guarantor for your loan. They agree to be legally responsible for the debt if you fail to make payments. This significantly reduces the lender’s risk because they have another creditworthy individual to pursue if you default.

A strong co-signer, ideally someone with an excellent credit score and stable income, can make all the difference. Their credit profile can help you qualify for a loan you otherwise wouldn’t, and potentially even secure a lower interest rate. However, it’s crucial to understand the responsibilities involved. Your co-signer is equally liable for the debt, and any missed payments will negatively impact their credit score as well as yours. Choose someone you trust implicitly and who understands the full implications of their commitment. This is a serious financial decision for both parties.

Exploring Specialized Lenders and Dealerships

Traditional banks are unlikely to approve a 450 credit score car loan. Your best bet lies with lenders who specialize in subprime auto financing. These include:

- Subprime Lenders: These are financial institutions specifically designed to work with borrowers who have poor credit. They assess applications differently, often focusing on your current income, employment history, and debt-to-income ratio more than your past credit score alone. You can often find these lenders through online search, or by asking dealerships which lenders they work with for challenged credit.

- Buy Here, Pay Here (BHPH) Dealerships: These dealerships act as both the car seller and the lender. They often offer easier approval for bad credit borrowers, as they control the entire financing process in-house. While convenient, BHPH loans typically come with very high interest rates and short repayment terms. Pro tips from us: While BHPH can be a last resort, always compare their offers carefully. Understand the total cost, not just the monthly payment, and be wary of extremely high APRs.

- Credit Unions: Sometimes, credit unions can be more flexible than large banks, especially if you have an existing relationship with them. They might be more willing to consider your overall financial situation rather than just your credit score. It’s always worth checking with your local credit union to see if they have options for members with lower credit scores.

Managing Your Expectations for the Vehicle

With a 450 credit score, it’s essential to manage your expectations regarding the type of vehicle you can finance. This is likely not the time to pursue a brand-new luxury SUV. Your focus should be on securing reliable transportation that meets your essential needs.

Prioritize an affordable, used car that fits within a realistic budget. A lower-priced vehicle means a smaller loan amount, which reduces the lender’s risk and your monthly payment burden. The goal at this stage is to get approved, establish a positive payment history, and start rebuilding your credit. You can always upgrade to your dream car later, once your credit score has significantly improved. Think of this as a stepping stone rather than your ultimate destination.

Preparing Meticulously for Your Loan Application

Preparation is key to increasing your chances of approval and securing the best possible terms for a 450 credit score car loan. Don’t walk into a dealership or lender unprepared.

Gathering All Necessary Documents

Lenders will want to verify your identity, income, and residency. Having all your documents ready can streamline the process and show you are organized and serious. Typically, you’ll need:

- Proof of Income: Recent pay stubs (at least 2-3 months), tax returns (if self-employed), or bank statements showing regular deposits.

- Proof of Residency: Utility bills, lease agreements, or mortgage statements with your current address.

- Identification: Valid driver’s license or state-issued ID.

- Proof of Insurance: You’ll need to secure full coverage insurance before driving off the lot.

- References: Some lenders, especially subprime ones, may ask for personal or professional references.

Knowing Your True Budget

Before you even start looking at cars, determine what you can truly afford. This goes beyond just the monthly car payment. Factor in:

- Loan Payment: The principal and interest.

- Car Insurance: Bad credit often means higher insurance premiums, especially for full coverage required by lenders.

- Fuel Costs: Estimate your weekly or monthly fuel expenses.

- Maintenance and Repairs: Used cars, especially older ones, will require maintenance. Budget for unexpected repairs.

- Registration and Taxes: Initial and annual costs.

A common mistake is to only consider the monthly payment. Pro tips from us: Create a detailed budget that includes all your existing expenses and potential car-related costs. Be conservative in your estimates. Over-stretching your budget can lead to missed payments, further damaging your credit, and potentially repossession.

Obtaining and Reviewing Your Credit Report

Even with a 450 score, it’s vital to know exactly what’s on your credit report. You are entitled to a free credit report from each of the three major bureaus (Equifax, Experian, TransUnion) once every 12 months via AnnualCreditReport.com.

Review your reports meticulously for any inaccuracies or errors. Incorrect information, such as accounts that aren’t yours or debts that have already been paid, can unfairly depress your score. If you find errors, dispute them immediately with the credit bureau. Correcting these could potentially give your score a slight boost, which might make a small difference in lending decisions. Understanding the negative items on your report also helps you explain your situation to a lender, if necessary, and demonstrates that you are taking responsibility.

The Application Process and What to Scrutinize

Once you’ve prepared, the next step is to apply. This phase requires careful attention to detail and a critical eye for loan terms.

Pre-Qualification vs. Full Application

Many lenders offer a pre-qualification process, which involves a "soft inquiry" on your credit report. This doesn’t affect your credit score and gives you an idea of the loan amount and interest rate you might qualify for. This is an excellent way to shop around without damaging your credit further.

A full application, however, involves a "hard inquiry," which can temporarily ding your credit score by a few points. It’s wise to get pre-qualified with several lenders first, then proceed with a full application only for the most promising offers. Try to complete all your hard inquiries within a short window (typically 14-45 days) so they count as a single inquiry for scoring purposes. This minimizes the negative impact on your credit.

Understanding the Loan Offer: APR, Term, and Total Cost

When presented with a loan offer, do not simply look at the monthly payment. You need to understand the full scope of the loan:

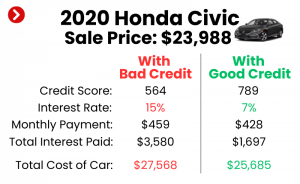

- Annual Percentage Rate (APR): This is the true cost of borrowing, including interest and any fees. For a 450 credit score, expect a very high APR, potentially in the double digits or even higher. Even a small difference in APR can mean thousands of dollars over the life of the loan.

- Loan Term: This is the length of the repayment period (e.g., 36, 48, 60 months). Longer terms mean lower monthly payments but significantly more interest paid over time. Common mistakes to avoid are stretching out the loan term just to get a lower monthly payment, as this drastically increases the total cost of the car.

- Total Cost of the Loan: Multiply your monthly payment by the number of months in the loan term, then add your down payment. This will give you the total amount you will pay for the car. Compare this across different offers.

Beware of Predatory Practices and Read the Fine Print

Unfortunately, the subprime lending market can attract less scrupulous lenders. Be vigilant for:

- Excessive Fees: Watch out for hidden fees, origination fees, or exorbitant processing charges.

- Loan Packing: This is when a lender tries to add unnecessary products (like extended warranties or rust protection) into your loan, inflating the total amount you owe. Politely decline any add-ons you don’t explicitly want or need.

- Balloon Payments: Ensure there are no unexpected large payments due at the end of the loan term.

- Prepayment Penalties: Check if there are penalties for paying off your loan early. Ideally, you want to pay it off as quickly as possible to save on interest.

Always read every line of the loan agreement before signing. If anything is unclear, ask questions until you fully understand. Don’t feel pressured to sign on the spot. It’s perfectly acceptable to take the documents home to review them carefully or even have a trusted advisor look them over. For more detailed information on understanding auto loan terms, you might find our guide on Decoding Your Auto Loan Agreement helpful.

Rebuilding Your Credit Through a Car Loan

One of the most significant benefits of successfully securing and managing a 450 credit score car loan is the opportunity it provides to rebuild your credit. This isn’t just about getting a car; it’s about setting a foundation for a stronger financial future.

The Power of Consistent On-Time Payments

Making every single car payment on time, every month, is paramount. Payment history is the single most important factor in your credit score, accounting for 35% of your FICO score. Each on-time payment demonstrates to credit bureaus and future lenders that you are a responsible borrower. Set up automatic payments to ensure you never miss a due date.

Even if you can only make the minimum payment, consistency is key. Over time, a consistent record of timely payments will start to chip away at the negative items on your credit report, slowly but surely improving your score. This isn’t an overnight fix, but a steady journey.

Ensure Payments Are Reported to Credit Bureaus

Confirm with your lender that they report your payment history to all three major credit bureaus (Equifax, Experian, and TransUnion). Most legitimate auto lenders do, but it’s always good to verify. If your payments aren’t being reported, they won’t help you build credit. This step is crucial for transforming your car loan into a credit-building tool.

Long-Term Benefits of Credit Improvement

As your credit score improves, doors will begin to open. You’ll qualify for better interest rates on future loans (another car, a mortgage, personal loans), lower insurance premiums, and even better terms on credit cards. A car loan can be the catalyst that transforms your financial standing, moving you from a 450 score to a more respectable and advantageous credit tier. For more in-depth strategies, check out our article on Practical Steps to Improve Your Credit Score.

Exploring Alternatives to a Traditional Car Loan

While a 450 credit score car loan is achievable, it’s not always the only or best option. Sometimes, alternative transportation solutions can be more financially prudent, especially in the short term.

Saving Up and Paying Cash

If your need for a car isn’t immediate, consider saving up to pay cash for an affordable used vehicle. This eliminates the need for a loan entirely, saving you thousands in interest and fees. It also removes the pressure of monthly payments, allowing you to focus on rebuilding your credit through other means. This might require patience, but it offers ultimate financial freedom.

Public Transportation, Ride-Sharing, or Borrowing

Depending on where you live, public transportation might be a viable option. Buses, trains, and subways can be significantly cheaper than car ownership. Ride-sharing services like Uber or Lyft can also fill occasional transportation gaps. In some cases, borrowing a vehicle from a trusted family member or friend for essential trips could be a temporary solution. While these options aren’t always ideal, they can provide breathing room to improve your financial situation before committing to a high-interest car loan.

Conclusion: Your Path to Car Ownership and Credit Recovery

Obtaining a 450 credit score car loan is undoubtedly challenging, but it is not impossible. This comprehensive guide has laid out the realities, strategies, and necessary precautions to help you navigate this complex financial landscape. From understanding the impact of your low score to leveraging down payments and co-signers, and meticulously preparing for your application, every step is crucial.

Remember, the goal isn’t just to get a car; it’s to use this opportunity to responsibly rebuild your credit and pave the way for a more secure financial future. Be realistic about your vehicle choice, diligent in your research, and steadfast in your commitment to on-time payments. With patience, persistence, and the right approach, you can drive away in a reliable vehicle and embark on a journey toward credit recovery. The road ahead may have a few bumps, but with informed decisions, you can certainly reach your destination.