Navigating the Road Ahead: Securing a Car Loan with a Charge-Off On Your Credit

Navigating the Road Ahead: Securing a Car Loan with a Charge-Off On Your Credit Carloan.Guidemechanic.com

Getting a car is often a necessity, not just a luxury. Whether it’s for work, family, or personal independence, reliable transportation is key. However, if your credit report shows a "charge-off," the path to securing a car loan with a charge-off on your credit can feel like an uphill battle. It’s a common misconception that a charge-off means the end of your financing hopes.

While a charge-off certainly presents challenges, it doesn’t necessarily close the door to vehicle ownership. This comprehensive guide will walk you through understanding charge-offs, preparing your finances, and identifying the right strategies to significantly increase your chances of getting approved for an auto loan. We’ll provide actionable insights and expert tips to help you navigate this complex financial landscape successfully.

Navigating the Road Ahead: Securing a Car Loan with a Charge-Off On Your Credit

What Exactly is a Charge-Off? And Why It Matters for Car Loans

Before we dive into solutions, it’s crucial to understand what a charge-off truly means for your credit profile. A charge-off occurs when a creditor (like a bank or credit card company) writes off a debt as unlikely to be collected. This typically happens after a long period of missed payments, usually 180 days or more.

From the lender’s perspective, they’ve stopped actively trying to collect the debt and have removed it from their active accounts. However, this doesn’t mean the debt disappears; you still owe the money. It simply signifies that the original creditor has given up on collecting it themselves, often selling it to a debt collection agency.

The Impact of a Charge-Off on Your Credit Score

A charge-off is one of the most severe negative marks that can appear on your credit report. It signals to potential lenders that you’ve failed to repay a significant debt in the past. This severely impacts your credit score, often dropping it by a substantial number of points.

This significant dip in your score makes you appear as a high-risk borrower to future lenders. When you apply for a car loan with a charge-off on your credit, lenders will see this mark and assess your creditworthiness very carefully, often leading to higher interest rates or outright denial.

How Lenders View a Charge-Off

When an auto lender reviews your application, a charge-off immediately raises a red flag. It tells them that there’s a history of non-payment. They will likely question your ability and willingness to repay a new loan.

Lenders are in the business of assessing risk. A charge-off indicates a higher probability of default. Understanding this perspective is the first step in addressing their concerns and building a stronger case for your loan approval.

The Reality of Getting a Car Loan with a Charge-Off: Challenging, But Not Impossible

Let’s be upfront: getting an auto loan with a charge-off on your credit history is undoubtedly more challenging than with good credit. You’re swimming against the current. However, it is absolutely not impossible. Many people successfully navigate this situation and secure the financing they need.

The key is to be realistic about your expectations and proactive in your approach. You will likely face different terms than someone with a pristine credit score, but with the right strategy, you can find a solution.

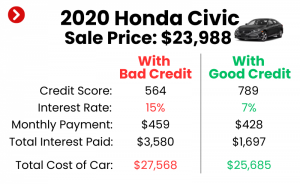

Expect Higher Interest Rates and Potential Fees

One of the most immediate consequences of a charge-off is the likelihood of facing significantly higher interest rates. Lenders mitigate their increased risk by charging more for the loan. This means your monthly payments will be higher, and the total cost of the vehicle will increase over the life of the loan.

Based on my experience in the automotive financing world, it’s common for individuals with charge-offs or other severe credit issues to see rates in the double digits. Don’t be surprised if offers are significantly higher than advertised "prime" rates. Be prepared for this reality and budget accordingly.

A Down Payment Becomes Your Best Friend

Another common expectation when seeking an auto loan after charge-off is the need for a substantial down payment. A larger down payment reduces the loan amount, thereby lowering the lender’s risk. It also demonstrates your commitment and financial stability, making you a more attractive borrower.

Pro tips from us: Aim for at least 10-20% of the vehicle’s purchase price as a down payment. The more you can put down, the better your chances of approval and potentially securing a slightly better interest rate.

Key Strategies to Boost Your Chances of Approval

Successfully getting a car loan with a charge-off requires a strategic, multi-faceted approach. You need to present yourself as the most reliable borrower possible, despite past financial missteps.

1. Understand Your Credit Report Thoroughly

Your credit report is your financial resume. Before you even think about applying for a loan, get copies of your credit report from all three major bureaus: Experian, Equifax, and TransUnion. You can get a free copy from AnnualCreditReport.com once every 12 months.

Review every entry with a fine-tooth comb. Look for:

- Errors: Are there any accounts listed that aren’t yours? Is the charge-off amount correct? Is the date accurate? Disputing errors can sometimes improve your score.

- Status of the Charge-Off: Is it "paid," "settled," or "unpaid"? A "paid" or "settled" charge-off, even if for less than the full amount, looks better than an "unpaid" one.

- Other Negative Items: Are there other late payments, collections, or judgments? Address these if possible.

Understanding the full scope of your credit history helps you anticipate lender questions and prepare your responses.

2. Pay Down Other Debts & Improve Your Debt-to-Income (DTI) Ratio

Lenders don’t just look at your credit score; they also assess your ability to take on new debt. Your debt-to-income (DTI) ratio is a critical factor. This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI indicates you have more disposable income to cover new loan payments.

Focus on paying down high-interest debts, especially credit card balances. Even small reductions can improve your DTI and make you a more appealing candidate for an auto loan after charge-off. Showing that you are actively managing your current debts demonstrates financial responsibility.

3. Save for a Significant Down Payment

As mentioned earlier, a down payment is incredibly powerful when you have a charge-off. It directly reduces the amount you need to borrow, which in turn lowers the lender’s risk. This makes them more willing to approve your application.

Pro tips from us: Start saving early. Even if it means waiting a few extra months to buy a car, a larger down payment can save you thousands in interest over the life of the loan. It also provides you with immediate equity in the vehicle, which is a strong position to be in.

4. Consider a Co-Signer (with caution)

If you have a trusted friend or family member with excellent credit who is willing to co-sign your loan, this can significantly improve your chances of approval and potentially secure a lower interest rate. A co-signer essentially guarantees the loan, meaning they are legally responsible for repayment if you default.

However, this decision should not be taken lightly. Common mistakes to avoid are not fully understanding the co-signer’s responsibility. If you miss payments, it negatively impacts their credit, not just yours. Ensure you have a clear, honest discussion about the risks and your commitment to repayment before asking someone to co-sign.

5. Explore Different Lender Types

Not all lenders are created equal, especially when it comes to bad credit car financing options. You’ll need to broaden your search beyond traditional banks.

- Subprime Lenders: These lenders specialize in working with borrowers who have less-than-perfect credit. They understand the challenges of a charge-off and are often more willing to approve loans, albeit with higher interest rates.

- Credit Unions: Often more flexible and community-focused than large banks, credit unions may be more understanding of your situation. They sometimes offer better rates to members, even those with credit issues.

- Online Lenders: Many online platforms specialize in "second chance auto loans" for individuals with poor credit. These can offer convenience and a broader range of options, allowing you to compare multiple offers.

- "Buy Here, Pay Here" (BHPH) Dealerships: These dealerships offer in-house financing, meaning they are both the seller and the lender. They are often very lenient with credit requirements, making them a viable option for those with severe credit challenges like a charge-off. However, common mistakes to avoid are not comparing their rates and terms carefully. BHPH loans often come with very high interest rates and restrictive terms. Always read the fine print and compare total costs.

6. Be Prepared for Higher Interest Rates

It’s a harsh truth, but with a charge-off, you will almost certainly be offered higher interest rates. Lenders price their loans based on risk, and a charge-off indicates significant risk. Don’t be discouraged by this; focus on getting approved first.

Pro tips from us: Your goal initially is to get approved and establish a positive payment history. After 12-18 months of on-time payments, you may be able to refinance your car loan with a charge-off on your credit at a lower interest rate, once your credit score has improved.

7. Provide Proof of Income and Stability

Lenders want to see that you have a stable financial situation now, regardless of past issues. Be ready to provide documentation of:

- Consistent Income: Pay stubs, tax returns, bank statements.

- Employment History: A stable job history demonstrates reliability.

- Residency: Proof of long-term residency (e.g., utility bills) can also reassure lenders.

The more evidence you can provide that you are currently stable and capable of repayment, the better your chances.

8. Negotiate Wisely

Even with a charge-off, negotiation is still possible. Don’t just accept the first offer. Focus on the total cost of the loan, not just the monthly payment. A lower monthly payment achieved by extending the loan term might mean paying significantly more in interest over time.

Be wary of unnecessary add-ons like extended warranties or protection plans that inflate the loan amount. While some might be beneficial, others are often overpriced and can be purchased separately later if needed.

Common Mistakes to Avoid When Seeking a Car Loan with a Charge-Off

Navigating the waters of bad credit financing can be tricky. Knowing what not to do is just as important as knowing what to do.

Applying Everywhere Without Caution

A common mistake is submitting multiple loan applications to various lenders in a short period. Each application often results in a "hard inquiry" on your credit report, which can further lower your credit score.

Pro tips from us: Do your research beforehand. Use pre-qualification tools (which often use a "soft inquiry" and don’t affect your score) to get an idea of potential rates before committing to a full application. Apply to 2-3 targeted lenders within a two-week window, as multiple inquiries for the same type of loan within a short timeframe are often grouped as one by credit scoring models.

Hiding Your Financial History

Attempting to conceal your charge-off or other negative credit marks from lenders is futile and counterproductive. Lenders will see everything on your credit report. Being upfront and honest about your financial past, while explaining how you’ve improved your situation, can build trust.

Based on my experience, lenders appreciate honesty. Prepare to discuss the charge-off and explain the circumstances, focusing on what you’ve learned and how your financial habits have changed.

Settling for the First Offer Without Comparison

When you have a charge-off, receiving any approval can feel like a huge win. However, resist the urge to immediately accept the first offer you get. Interest rates and terms can vary significantly between lenders, even for borrowers with similar credit profiles.

Take the time to compare offers from different types of lenders (credit unions, subprime lenders, online platforms). This due diligence can save you a substantial amount of money over the life of the loan.

Buying a Car You Cannot Afford

The excitement of getting approved for a car loan can sometimes lead to making poor decisions. Don’t let a lender push you into a vehicle that stretches your budget too thin. Remember that beyond the monthly payment, you also have to factor in insurance, maintenance, fuel, and registration.

Common mistakes to avoid are overextending your budget. Create a realistic budget before you start shopping. A reliable, affordable used car is often a much wiser choice than a brand-new, expensive vehicle when you’re working to rebuild your credit.

Rebuilding Your Credit for the Future

Getting a car loan with a charge-off on your credit is a significant step, but it’s also an opportunity to actively rebuild your credit for the long term. Your car loan can become a powerful tool for credit improvement if managed responsibly.

Making On-Time Payments is Paramount

Once you secure your car loan, your number one priority should be making every single payment on time, every month. Payment history is the most significant factor in your credit score. Consistent, on-time payments will gradually demonstrate your reliability to credit bureaus and future lenders.

This positive payment history will slowly but surely overshadow the negative impact of the charge-off over time. It’s an investment in your financial future.

Consider Other Credit Building Tools

Beyond your car loan, look into other ways to bolster your credit.

- Secured Credit Cards: These require a deposit, making them less risky for lenders. Use them responsibly for small purchases and pay the balance in full each month.

- Credit Builder Loans: Offered by some credit unions or community banks, these loans are designed specifically to help you build credit. The loan amount is held in an account while you make payments, and you receive the funds once the loan is paid off.

For more in-depth guidance on improving your credit, consider reading our article on Understanding and Improving Your Credit Score (Internal Link 1).

The Car Loan Approval Process with Bad Credit: What to Expect

The process for getting a car loan when you have a charge-off might feel a bit different from a standard application. Being prepared can reduce stress and improve your outcome.

Documentation Needed

Expect lenders to ask for extensive documentation to verify your identity, income, and residency. This might include:

- Government-issued ID

- Proof of residence (utility bill, lease agreement)

- Recent pay stubs or bank statements

- Tax returns (especially if self-employed)

- Contact information for references

Have these documents organized and ready to present. The quicker you can provide what they need, the smoother the process will be.

Potential for Longer Approval Times

While some lenders offer instant approvals, those dealing with challenging credit profiles might take a bit longer. Underwriters will often manually review applications with charge-offs, looking for mitigating factors or additional proof of stability.

Be patient and responsive to any requests for more information. A delay doesn’t necessarily mean a denial; it often just means a more thorough review is underway.

Transparency with Lenders

As previously mentioned, being transparent about your financial situation is crucial. If a lender asks about the charge-off, explain the circumstances briefly and honestly, focusing on what you’ve done to improve your financial habits since then.

You might also find value in consulting resources from the Consumer Financial Protection Bureau (CFPB) for general information on car loan rights and responsibilities: CFPB Auto Loans (External Link).

Conclusion: Your Journey to a Car Loan After a Charge-Off Is Within Reach

Getting a car loan with a charge-off on your credit is a testament to perseverance and strategic planning. While it presents significant hurdles, it is by no means an impossible feat. By understanding the impact of a charge-off, meticulously preparing your finances, and approaching the lending market strategically, you can absolutely secure the financing you need.

Remember to focus on saving a substantial down payment, improving your debt-to-income ratio, and seeking out lenders who specialize in bad credit. Be prepared for higher interest rates, but view this loan as an opportunity to rebuild your credit profile with consistent, on-time payments.

Your financial journey is ongoing. This car loan can be a powerful tool for demonstrating your renewed financial responsibility and paving the way for a stronger credit future. Stay disciplined, stay informed, and drive confidently toward your goals.

For further insights on managing and improving your credit, explore our article on Effective Strategies for Credit Rebuilding (Internal Link 2). We believe in empowering you with the knowledge to make the best financial decisions.