Navigating the Road Ahead: Securing Car Loans For People With Repos

Navigating the Road Ahead: Securing Car Loans For People With Repos Carloan.Guidemechanic.com

Facing a car repossession can feel like a financial dead end. The sting of losing your vehicle combined with the hit to your credit score often leaves individuals wondering if they’ll ever qualify for a car loan again. But here’s the encouraging truth: while challenging, securing car loans for people with repos is absolutely possible. It requires a strategic approach, a clear understanding of your financial situation, and a commitment to rebuilding.

As an expert blogger and professional SEO content writer, I’ve seen countless individuals navigate these waters successfully. This comprehensive guide is designed to empower you with the knowledge and tools needed to drive off the lot with a new set of wheels, even after a repossession. We’ll delve deep into every facet, from understanding the impact on your credit to finding the right lenders and making smart financial decisions.

Navigating the Road Ahead: Securing Car Loans For People With Repos

The Immediate Aftermath: Understanding Repossession’s Impact

A vehicle repossession is more than just losing your car; it’s a significant financial event that leaves a lasting mark on your credit report. Understanding this impact is the first crucial step toward recovery.

How Repossession Hurts Your Credit Score

When a lender repossesses your car, they report it to the major credit bureaus (Experian, Equifax, and TransUnion). This entry indicates a failure to meet your loan obligations, which is a major red flag for future lenders.

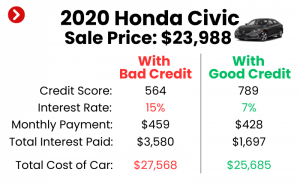

Based on my experience, a repossession can drop your credit score by 50 to 100 points or even more, depending on your credit profile before the event. This immediate reduction makes qualifying for new credit much harder and often results in higher interest rates.

The Long-Term Credit Implications

A repossession typically remains on your credit report for seven years from the original delinquency date. During this period, it serves as a constant reminder of past financial difficulties.

While its impact lessens over time, especially if you start building positive credit history afterward, it remains visible. Lenders will factor this into their decision-making process for various types of loans, not just auto loans.

The Psychological and Practical Hurdles

Beyond the numbers, a repossession carries a heavy psychological toll. It can feel embarrassing, frustrating, and incredibly limiting. Practically, losing a car often means losing a vital mode of transportation, impacting your ability to get to work, run errands, and maintain daily life.

Recognizing these challenges is important, but don’t let them deter you. This article is about moving forward and finding viable solutions for financing after repo.

Is Getting a Car Loan After Repossession Possible? Absolutely!

The short answer is yes, getting an auto loan after repossession is entirely possible. However, it’s crucial to set realistic expectations. You likely won’t walk into a dealership and get the same favorable terms as someone with an excellent credit history.

Your journey will involve demonstrating financial stability and a renewed commitment to responsible borrowing. Many lenders specialize in bad credit car loans and understand that people sometimes face difficult circumstances. They are willing to offer second chance car loans, provided you meet their specific criteria.

Essential Steps Before Applying for a Car Loan

Before you even think about stepping onto a car lot or filling out an application, there are several critical preparatory steps. These actions will not only improve your chances of approval but also help you secure the best possible terms available for your situation.

1. Review Your Credit Report Thoroughly

This is non-negotiable. You need to know exactly what lenders see when they pull your credit. Obtain free copies of your credit report from all three major bureaus through AnnualCreditReport.com.

Scrutinize every detail for inaccuracies. Errors can negatively impact your score, and correcting them can provide a much-needed boost. Dispute any incorrect information immediately with the credit bureau.

Understanding your credit score is also vital. Services like Credit Karma or your bank might offer free scores, giving you a good baseline. Knowing your score helps you understand what types of loans you might qualify for.

2. Understand Why the Repossession Happened

Reflect honestly on the circumstances that led to the repossession. Was it due to job loss, unexpected medical bills, or simply poor financial management? Understanding the root cause is essential for preventing a repeat scenario.

Lenders might ask about the repossession during the application process. Being able to explain what happened, what you learned, and how you’ve changed your financial habits shows maturity and responsibility. This transparency can work in your favor.

3. Actively Work to Improve Your Credit Score

Even a small improvement in your credit score can make a difference in interest rates and loan terms. This isn’t an overnight fix, but consistent effort pays off.

Pro tips from us: Start by making all current payments on time, every time. This is the single most impactful action you can take. Reduce existing credit card debt, as high utilization ratios hurt your score. Consider a secured credit card or a credit-builder loan to demonstrate responsible credit usage.

Every positive action you take will gradually help to mitigate the negative impact of the repossession over time. Patience and discipline are key here.

4. Save for a Substantial Down Payment

For individuals seeking car loans for people with repos, a significant down payment is arguably one of the most powerful tools in your arsenal. It directly reduces the amount you need to borrow, which lowers the lender’s risk.

A larger down payment also shows lenders that you are serious about this purchase and have a financial stake in the vehicle. Based on my experience, aiming for at least 10-20% of the car’s purchase price can significantly improve your chances of approval and potentially lead to better interest rates.

Common mistakes to avoid are underestimating the power of a down payment or assuming you can get a loan with no money down. While possible in some cases, it’s far less likely and comes with much harsher terms when you have a repossession on your record.

5. Determine Your Realistic Budget

Don’t just think about the monthly car payment. Consider the total cost of car ownership, which includes:

- Loan Payment: Principal and interest.

- Insurance: Expect higher premiums with a bad credit score and for new drivers.

- Maintenance: Routine service, unexpected repairs.

- Fuel: Daily commuting costs.

Use a budget spreadsheet to calculate your monthly income and expenses. This will help you determine how much you can truly afford without stretching your finances too thin. Lenders will also assess your debt-to-income (DTI) ratio, so having a clear budget shows financial prudence.

Where to Find Car Loans After a Repossession

Once you’ve prepared your finances and credit, it’s time to explore your lending options. Not all lenders are created equal when it comes to auto loans after repossession. You’ll need to focus on those who specialize in or are more open to working with individuals with challenging credit histories.

1. Subprime Lenders and Dealership Special Finance Departments

These are often your best bet. Subprime lenders specialize in providing loans to borrowers with lower credit scores, including those with past bankruptcies or repossessions. They understand that life happens and are willing to take on higher risk, albeit with higher interest rates.

Many dealerships have "special finance" or "bad credit car loan" departments. These departments have relationships with a network of subprime lenders and can help match you with suitable options. Be prepared for a thorough review of your financial history.

2. Credit Unions

Credit unions are member-owned financial institutions that often offer more flexible lending criteria than traditional banks. They tend to look beyond just your credit score and consider your overall financial situation and relationship with the credit union.

If you are a member of a credit union, or eligible to join one, it’s definitely worth exploring their auto loan options. Their interest rates can sometimes be more competitive than those offered by traditional subprime lenders.

3. Buy Here, Pay Here (BHPH) Dealerships

Buy Here, Pay Here dealerships offer in-house financing, meaning the dealership itself is the lender. This can be a viable option for those struggling to get approved elsewhere, as they often have very lenient approval standards.

Pros: Easier approval, especially for individuals with severe credit issues. They focus more on your income and ability to pay than your credit history.

Cons: This option often comes with significantly higher interest rates, higher vehicle prices, and limited choices of older, higher-mileage vehicles. Pro tips from us: Carefully read the terms and conditions, as some BHPH arrangements may not report payments to credit bureaus, hindering your credit rebuilding efforts.

4. Online Lenders Specializing in Bad Credit

The internet has opened up numerous avenues for second chance car loans. Many online lenders specifically cater to individuals with bad credit. They allow you to apply from home, often provide quick pre-qualification decisions, and enable you to compare multiple offers.

This can be a convenient way to gauge your options without impacting your credit score with multiple hard inquiries. Just ensure any lender you consider is reputable and transparent about their rates and fees.

What to Expect When Applying for a Car Loan

When you’re applying for car loans for people with repos, your experience will differ from someone with excellent credit. Knowing what to expect can help you navigate the process more smoothly.

Higher Interest Rates

This is almost a certainty. Lenders view a past repossession as an indicator of higher risk, and they compensate for that risk by charging higher interest rates. Your goal should be to get approved and then diligently make payments to improve your credit, potentially allowing you to refinance later.

Shorter Loan Terms

Lenders might offer shorter loan terms (e.g., 36-48 months instead of 60-72 months) to reduce their risk exposure. While this means higher monthly payments, it also means you pay less interest over the life of the loan and build equity faster.

Larger Down Payment Requirements

As mentioned earlier, a significant down payment will be expected and highly beneficial. It mitigates risk for the lender and shows your commitment.

Potential for a Co-Signer

A co-signer with good credit can significantly increase your chances of approval and help you secure better terms. However, be aware that a co-signer is equally responsible for the loan. If you miss payments, it impacts their credit, and they are legally obligated to pay.

Discuss the responsibilities thoroughly with any potential co-signer. This is a big ask and requires trust.

Proof of Income and Residence

Lenders will want to see stable income and residency. Be prepared to provide pay stubs, bank statements, and proof of address (utility bills, lease agreements). This demonstrates your current ability to make payments.

Navigating the Loan Approval Process

Once you’ve identified potential lenders, the application process itself requires careful attention.

Be Honest and Transparent

Don’t try to hide your repossession. Lenders will discover it when they pull your credit report. Be upfront about your financial history and, more importantly, explain what you’ve done to improve your situation since the repossession.

Avoid Multiple Hard Inquiries

Applying for loans at too many places in a short period can further ding your credit score. Try to get pre-qualified with a few lenders first, which usually involves a soft credit pull that doesn’t affect your score. Once you have pre-approvals, then proceed with full applications for the best offers.

Most credit scoring models will count multiple auto loan inquiries within a specific timeframe (usually 14-45 days) as a single inquiry, recognizing you’re shopping for one loan. However, spreading them out over months is detrimental.

Compare Loan Offers Carefully

Don’t jump at the first offer you receive. Compare interest rates, loan terms, and any associated fees from different lenders. Even a slight difference in interest rate can save you hundreds or thousands of dollars over the life of the loan.

Read the Fine Print

Common mistakes to avoid are signing a loan agreement without fully understanding all the terms. Pay close attention to:

- Annual Percentage Rate (APR): This includes the interest rate and any fees, giving you the true cost of borrowing.

- Total Amount Paid: Understand the total cost over the loan’s lifetime.

- Prepayment Penalties: Check if there are penalties for paying off the loan early.

- Late Payment Fees: Know the consequences of missed or late payments.

If anything is unclear, ask questions until you fully understand.

Rebuilding Your Credit with Your New Car Loan

Getting approved for a car loan after a repossession is a significant achievement. But it’s also an opportunity to actively rebuild your credit and prove your financial responsibility.

Make Timely Payments – Every Single Time

This cannot be stressed enough. Your new car loan is a powerful tool for credit rehabilitation. Every on-time payment you make will be reported to the credit bureaus as positive activity, gradually improving your credit score.

Consistency is key. Set up automatic payments if possible, or create reminders to ensure you never miss a due date. This demonstrates a reliable payment history, which is critical for future lending opportunities.

Your Car Loan as a Stepping Stone

View this car loan as a stepping stone. It might come with less-than-ideal terms, but it’s a way to re-establish trust with lenders. As your credit score improves over 12-24 months of consistent payments, you may be able to refinance your loan at a lower interest rate, saving you money.

This strategic approach turns a potentially difficult situation into a pathway toward a stronger financial future.

Pro Tips for Long-Term Success

Beyond securing the loan, consider these additional tips to ensure your long-term financial health and prevent future issues.

- Start Small and Affordable: Don’t overextend yourself. Choose a reliable, affordable car that meets your needs without straining your budget. A lower loan amount means less risk and easier payments.

- Consider a Co-signer Carefully: While a co-signer can help, remember the shared responsibility. Only pursue this option if you are absolutely confident in your ability to make payments and protect their credit.

- Understand Total Cost of Ownership: Beyond the loan, factor in fuel, insurance, maintenance, and potential repairs. Having a financial buffer for these costs is crucial.

- Explore Refinancing Down the Line: Once you’ve made 12-18 months of on-time payments and your credit score has improved, look into refinancing your car loan. You might qualify for a significantly lower interest rate, reducing your monthly payments and total interest paid.

- Maintain a Detailed Budget: Continue to track your income and expenses rigorously. This practice is fundamental to financial stability and ensures you can comfortably meet all your financial obligations.

Common Mistakes to Avoid When Seeking Car Loans After Repossession

Knowing what not to do is just as important as knowing what to do.

- Not Checking Your Credit Report: Blindly applying without knowing your credit standing and correcting errors is a recipe for disappointment.

- Settling for the First Offer: Don’t feel pressured to accept the very first loan offer you receive. Shop around, compare, and negotiate for better terms.

- Buying More Car Than You Can Afford: It’s tempting to get the newest model, but with bad credit, financial stability is paramount. Prioritize affordability over luxury.

- Ignoring the Fine Print: As mentioned, understanding every clause of your loan agreement is crucial to avoid hidden fees or unfavorable terms.

- Falling for "Guaranteed Approval" Scams: Be extremely wary of lenders promising "guaranteed approval" regardless of credit history. These are often predatory lenders with exorbitant interest rates and fees, or outright scams. No legitimate lender can guarantee approval without reviewing your financial situation.

Conclusion: Your Road to Recovery and a New Car

A repossession is undoubtedly a setback, but it is not the end of your journey toward vehicle ownership. Car loans for people with repos are a reality, requiring diligence, preparation, and a smart strategy. By understanding the impact on your credit, taking proactive steps to improve your financial standing, and knowing where to look for appropriate lenders, you can successfully navigate this challenge.

Remember, this process is about more than just getting a car; it’s about rebuilding your financial foundation and demonstrating renewed responsibility. With patience, persistence, and the right approach, you can drive away with a new car and a clearer path to a healthier financial future. Your journey starts now, armed with the knowledge to make informed decisions and secure the financing you need.