Navigating the Road Ahead: The Definitive Guide to Car Loan Age Limits

Navigating the Road Ahead: The Definitive Guide to Car Loan Age Limits Carloan.Guidemechanic.com

The dream of owning a reliable car, whether it’s a brand-new model or a dependable used vehicle, knows no age. From fresh-faced young adults eager for their first set of wheels to seasoned drivers seeking comfort and independence in their golden years, a car represents freedom and necessity. Yet, a common concern often surfaces, particularly among older applicants: "Is there a car loan age limit?"

This question, while perfectly valid, stems from a pervasive misconception. As an expert blogger and professional SEO content writer who has spent years demystifying complex financial topics, I’m here to tell you that the truth is far more nuanced than a simple "yes" or "no." In this comprehensive guide, we’ll delve deep into the real factors lenders consider, debunk myths surrounding age restrictions, and equip you with the knowledge to confidently secure your next car loan, no matter your age.

Navigating the Road Ahead: The Definitive Guide to Car Loan Age Limits

Our ultimate goal is to provide a pillar of content that doesn’t just scratch the surface but offers genuine, actionable value. So, buckle up as we navigate the ins and outs of car financing, ensuring you’re well-prepared for your journey.

Is There a Strict Car Loan Age Limit? The Truth Revealed

Let’s address the elephant in the room right away: there is no legal maximum age limit for obtaining a car loan in the United States or most other developed countries. This is a critical point that often gets overlooked. Lenders are legally prohibited from discriminating against applicants based solely on age, thanks to regulations like the Equal Credit Opportunity Act (ECOA) in the U.S.

However, while there isn’t a hard age cutoff, it’s equally important to understand why this concern arises. Lenders, at their core, are assessing risk. They want to be confident that you can and will repay the loan according to the agreed terms. Certain factors often associated with age – such as changes in income stability, health considerations, or the duration of a loan term – can subtly influence their assessment, but age itself isn’t the direct barrier.

Based on my experience working with countless individuals and analyzing lender criteria, the focus is always on your financial profile, not your birth year. The perceived "car loan age limit" isn’t about how old you are; it’s about how your age might impact the core elements of your financial health that lenders scrutinize. Understanding this distinction is the first step toward a successful application.

Beyond Birthdays: What Lenders Really Evaluate for Car Loan Approval

Since age isn’t the direct hurdle, what truly matters to lenders? They employ a holistic approach, examining several key financial indicators to gauge your creditworthiness and ability to repay. These factors are universal, applying equally to a 20-year-old as they do to an 80-year-old.

Let’s break down these critical components in detail.

Credit Score and History: Your Financial Report Card

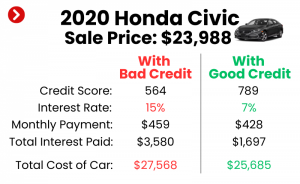

Your credit score is arguably the single most important factor in securing any loan, and car loans are no exception. This three-digit number, primarily FICO or VantageScore, acts as a summary of your financial reliability. It tells lenders how well you’ve managed past debts.

A higher credit score signals to lenders that you are a responsible borrower with a proven track record of timely payments. This can translate into better loan terms, including lower interest rates and more flexible repayment options. Conversely, a lower score suggests a higher risk, potentially leading to higher interest rates or even loan denial.

Pro tips from us: Regularly review your credit report from all three major bureaus (Experian, Equifax, TransUnion) via AnnualCreditReport.com. Look for any errors or discrepancies that could be dragging down your score. Actively work to pay bills on time, keep credit utilization low, and avoid opening too many new credit lines simultaneously.

Income and Debt-to-Income Ratio: Can You Afford It?

Lenders need assurance that you have a stable and sufficient income stream to comfortably cover your monthly car loan payments, along with all your other financial obligations. They aren’t just looking at the number; they’re assessing its consistency and reliability.

For older borrowers, income sources might diversify beyond traditional employment. Pensions, Social Security benefits, retirement account distributions (like 401k or IRA withdrawals), investment income, and even rental income are all valid forms of verifiable income. The key is that these sources must be regular, predictable, and provable through bank statements, tax returns, or benefit letters.

Equally important is your debt-to-income (DTI) ratio. This ratio compares your total monthly debt payments to your gross monthly income. Lenders prefer a lower DTI, typically below 36-43%, as it indicates you have enough disposable income to handle additional debt without becoming overextended. A high DTI, regardless of your age, is a significant red flag.

Down Payment: Reducing Lender Risk, Boosting Your Chances

A substantial down payment is a powerful tool in your car loan application, especially if other aspects of your financial profile are less than perfect. When you put down a significant amount of money upfront, you immediately reduce the amount you need to borrow, which in turn lowers the lender’s risk.

A larger down payment also has direct benefits for you, the borrower. It results in lower monthly payments, less interest paid over the life of the loan, and reduces the likelihood of being "upside down" on your loan (owing more than the car is worth). This financial prudence demonstrates your commitment and financial stability.

Common mistakes to avoid are underestimating the power of a solid down payment. Even a 10-20% down payment can make a significant difference in securing favorable terms and showing lenders you’re serious. If you have savings, consider allocating a good portion towards your down payment.

Loan Term and Vehicle Age: The Lifecycle of the Loan

The length of your loan term (e.g., 36, 48, 60, or 72 months) directly impacts your monthly payment and the total interest you’ll pay. While longer terms offer lower monthly payments, they also mean more interest accrues over time and you’ll be paying for the car for a longer duration.

For older borrowers, lenders might prefer shorter loan terms. This isn’t an age restriction, but rather a practical assessment of risk. A shorter term reduces the likelihood of unforeseen life events impacting repayment ability over a prolonged period. It also aligns the loan duration more closely with the typical lifespan of a vehicle.

On a related note, the vehicle’s age also plays a role. While distinct from the "car loan age limit" for borrowers, some lenders impose limits on how old a car can be or how many miles it can have to qualify for financing. Very old or high-mileage vehicles are considered higher risk due to potential mechanical issues and rapid depreciation.

Collateral (The Car Itself): What’s the Asset Worth?

Remember, a car loan is a secured loan, meaning the vehicle itself serves as collateral. If you default on the loan, the lender can repossess the car to recoup their losses. Therefore, lenders will assess the value and marketability of the car you intend to purchase.

Newer, more reliable vehicles with good resale value are generally easier to finance because they represent stronger collateral. A car that holds its value well reduces the lender’s potential loss in case of default. This is why financing a brand-new car can sometimes be easier than financing a very old, high-mileage vehicle, regardless of the borrower’s age.

Navigating Car Loans as an Older Adult: Your Winning Strategies

Understanding what lenders look for is the first step; the next is strategically positioning yourself as an ideal borrower. For older adults, this often means highlighting financial strengths and mitigating perceived risks.

Here are some winning strategies to help you secure the best possible car loan terms.

1. Build and Maintain Excellent Credit

This cannot be stressed enough. A strong credit score is your most powerful asset. Continue to make all payments on time, keep credit card balances low, and avoid unnecessary new credit applications. If your score isn’t ideal, dedicate time to improving it before applying for a car loan. Even small improvements can lead to significant savings on interest.

2. Demonstrate Stable and Verifiable Income

Gather documentation for all your income sources. This includes pension statements, Social Security award letters, investment income summaries, and recent bank statements. Presenting a clear, consistent picture of your financial inflows will instill confidence in lenders, demonstrating your capacity to meet monthly obligations.

3. Opt for a Larger Down Payment

As discussed, a substantial down payment reduces your loan amount and the lender’s risk. If you have savings or equity from a trade-in vehicle, leveraging these funds can significantly improve your loan application’s strength. It’s a clear signal of financial stability and commitment.

4. Consider a Co-signer (Carefully)

If your income or credit score isn’t as strong as you’d like, adding a co-signer with excellent credit and stable income can dramatically boost your chances of approval and secure better terms. This is often a child or another trusted family member.

Pro tips from us: Ensure both parties fully understand the legal implications of co-signing. A co-signer is equally responsible for the loan, and any missed payments will negatively impact both credit scores. It’s a serious commitment that requires open communication and trust.

5. Choose the Right Vehicle for Your Budget

Be realistic about the car you can afford. Opting for a more modest, reliable vehicle that aligns with your income and budget can make your application more attractive to lenders. A brand-new luxury car might be out of reach, but a gently used, dependable model could be perfectly attainable.

6. Explore Different Lenders

Don’t settle for the first offer you receive. Shop around! Banks, credit unions, online lenders, and even dealership financing departments all have different criteria and rates.

Credit unions, in particular, often offer more personalized service and potentially better rates for their members. Online lenders can provide quick pre-approvals without impacting your credit score significantly. Comparing offers within a short window (typically 14-45 days) will count as a single inquiry on your credit report.

7. Shorten Your Loan Term

While longer terms mean lower monthly payments, a shorter loan term signals less risk to the lender. If your budget allows for higher monthly payments, opting for a 36 or 48-month loan instead of 60 or 72 months can make your application more appealing and save you a considerable amount in interest over time.

Unique Aspects of Car Financing for Seniors

While the core principles of car lending remain consistent across age groups, older borrowers sometimes face unique considerations that are worth addressing. Being proactive about these can smooth your path to vehicle ownership.

Estate Planning and Loan Responsibility

It’s a sensitive topic, but important to consider: what happens to your car loan if you pass away? Typically, the loan becomes part of your estate. Your executor would then use assets from your estate to pay off the remaining balance. If there aren’t enough assets, the car might be sold to cover the debt.

Based on my experience, transparency with your financial advisor or estate planner is crucial. They can help you structure your affairs to ensure your wishes are met and your family isn’t burdened. Sometimes, life insurance policies are used to cover outstanding debts.

Insurance Costs: An Often Overlooked Factor

As drivers age, insurance premiums can sometimes increase due to actuarial data linking age to certain risk factors. While this isn’t a direct loan qualification factor, it significantly impacts the total cost of car ownership. Lenders want to see that you can afford the entire package, including insurance.

Always factor in potential insurance costs when budgeting for a new car. Get quotes from multiple providers before finalizing your purchase to avoid any unwelcome surprises.

Health and Driving Ability

While never explicitly asked on a loan application, lenders are making an assessment about your ability to repay over the loan term. If you’re considering a long-term loan, it’s wise to honestly evaluate your current health and driving ability. This is more for your personal planning than for the lender’s direct assessment.

The goal is to ensure you’ll be able to drive and enjoy the vehicle for the duration of the loan. If health concerns are a factor, a shorter loan term might be a more prudent choice.

Understanding Loan Protections and Avoiding Predatory Lending

Unfortunately, older adults can sometimes be targets of predatory lending practices. These might involve excessively high interest rates, hidden fees, or misleading terms. It’s crucial to thoroughly read and understand every document before signing.

Don’t feel rushed or pressured. If something seems too good to be true, or if you don’t understand a clause, ask questions or seek advice from a trusted financial advisor or a family member. The Consumer Financial Protection Bureau (CFPB) offers excellent resources on understanding your rights and avoiding scams. (External Link: https://www.consumerfinance.gov/)

The Open Road Awaits: Your Car Loan Journey

The notion of a "car loan age limit" is largely a myth. What truly matters to lenders is a robust financial profile, characterized by a strong credit history, stable income, a manageable debt-to-income ratio, and a willingness to make a solid down payment. These are the pillars of creditworthiness, regardless of how many candles were on your last birthday cake.

For older borrowers, the strategies are clear: leverage your financial wisdom, demonstrate your stability, and be proactive in presenting a compelling application. Don’t let unfounded concerns about age deter you from securing the vehicle that provides you with freedom and independence. The open road truly awaits.

By focusing on these key factors and employing smart strategies, you can confidently navigate the car loan process and drive away in the vehicle of your dreams. Start preparing your financial documents today, compare lender offers, and embark on your next automotive adventure with peace of mind.