Navigating the Road Ahead: Unpacking the Average New Car Loan Length and Its True Cost

Navigating the Road Ahead: Unpacking the Average New Car Loan Length and Its True Cost Carloan.Guidemechanic.com

Buying a new car is an exciting milestone. The scent of fresh upholstery, the gleam of untouched paint, the promise of reliable journeys – it’s a significant investment. Yet, amidst the thrill of a test drive and the allure of a new model, many prospective buyers often overlook one of the most critical financial decisions they’ll make: the length of their car loan.

Understanding the "average new car loan length" isn’t just about knowing a statistic; it’s about grasping the profound impact this choice has on your monthly budget, the total amount you pay, and your long-term financial health. As an expert in automotive finance and a seasoned content writer, I’ve seen firsthand how a well-informed decision here can save you thousands of dollars and countless headaches. This comprehensive guide will peel back the layers, offering you the insights needed to navigate this crucial aspect of car ownership with confidence.

Navigating the Road Ahead: Unpacking the Average New Car Loan Length and Its True Cost

What Exactly is a Car Loan Term, and Why Does It Matter?

Before we dive into averages, let’s establish the fundamentals. A car loan term refers to the duration, typically measured in months, over which you agree to repay the money borrowed to purchase your vehicle. Common terms range from 36 months (3 years) to 84 months (7 years), and sometimes even longer.

This seemingly simple number dictates two major aspects of your loan: your monthly payment and the total interest you’ll pay over the life of the loan. A shorter term means higher monthly payments but less interest overall. Conversely, a longer term offers lower monthly payments but significantly increases the total cost of your vehicle. It’s a delicate balance that requires careful consideration.

Based on my experience, many buyers focus almost exclusively on the monthly payment, often stretching the loan term to its maximum to achieve a "manageable" figure. While this approach provides immediate relief, it can lead to considerable financial strain in the long run.

The Current Landscape: What is the Average New Car Loan Length Today?

The automotive finance world is dynamic, constantly shifting with economic trends, interest rates, and consumer behavior. Over the past decade, we’ve observed a clear trend: the average new car loan length has been steadily increasing. What was once predominantly a 60-month (5-year) standard has now stretched considerably.

According to recent financial analyses and industry reports, the average new car loan length often hovers around 69 to 72 months, and in some cases, even longer. This upward trend is not accidental. It’s largely a response to the rising cost of new vehicles. As car prices escalate, lenders and dealerships offer longer terms to keep monthly payments "affordable" for a wider range of buyers.

Pro tips from us: Don’t just accept the average as your personal ideal. While it reflects market conditions, it doesn’t necessarily reflect the financially smartest choice for your situation. Always question whether a longer term is genuinely beneficial or merely a way to mask a purchase that might be beyond your comfortable budget.

Deconstructing Loan Lengths: Pros and Cons of Different Terms

Understanding the general trends is helpful, but applying it to your own purchase requires a deeper dive into the specific advantages and disadvantages of various loan lengths. Let’s break down the implications of both shorter and longer terms.

Shorter Loan Terms (e.g., 36-60 Months)

Opting for a shorter loan term is often lauded by financial experts, and for good reason. While it presents a higher immediate financial commitment, the long-term benefits are substantial.

-

Less Total Interest Paid: This is perhaps the most significant advantage. Because you’re paying off the principal balance faster, the amount of time interest accrues is dramatically reduced. Over several years, this can translate into thousands of dollars saved, money that stays in your pocket or can be invested elsewhere.

Based on my experience, this saving alone is often enough to convince buyers to stretch their budget slightly for a shorter term. It’s a tangible, quantifiable benefit that directly impacts your wealth.

-

Faster Equity Build-Up: When you make larger monthly payments, you’re paying down the principal more aggressively. This means you build equity in your vehicle much faster. Equity is the difference between what your car is worth and what you still owe on it.

Having positive equity quickly protects you from being "upside down" on your loan, a common problem with longer terms.

-

Lower Risk of Negative Equity: Negative equity, also known as being "upside down" or "underwater," occurs when you owe more on your car than it’s currently worth. Since cars depreciate rapidly, especially in the first few years, a shorter loan term significantly reduces the window in which you’re likely to experience negative equity.

This offers peace of mind and more financial flexibility if you need to sell or trade in your car sooner than expected.

-

Quicker Debt Freedom: Imagine paying off your car in three or five years instead of seven or eight. That’s several years where you’re free from a car payment, freeing up a significant portion of your budget for other goals like saving for a down payment on a home, investing, or simply enjoying more disposable income.

This psychological benefit of being debt-free sooner is often underestimated but profoundly impactful.

Longer Loan Terms (e.g., 72-84+ Months)

While they offer immediate relief in the form of lower monthly payments, longer loan terms come with a host of financial drawbacks that deserve careful consideration.

-

Significantly More Total Interest Paid: This is the primary pitfall. Spreading payments over a longer period means interest has more time to compound, leading to a much higher overall cost for the same vehicle. What looks like an "affordable" monthly payment can quickly become a very expensive car.

Common mistakes to avoid are not calculating the total cost of the loan. Many buyers are shocked when they see the full amount of interest paid on an 84-month loan compared to a 60-month loan.

-

Slower Equity Build-Up and Higher Risk of Negative Equity: With smaller monthly payments, less of your payment goes toward the principal in the early years. Combined with rapid depreciation, this almost guarantees you’ll be upside down on your loan for a significant period.

This means if your car is totaled or stolen, your insurance payout might not cover the full loan amount, leaving you to pay the difference. It also makes trading in or selling your car difficult without rolling negative equity into a new loan, a cycle best avoided.

-

Longer Period of Debt: Seven or even eight years is a long time to be tied to a single debt, especially for a depreciating asset. Life circumstances can change dramatically over such a long period – job loss, family expansion, unexpected expenses.

A long-term car payment can become a financial burden that limits your flexibility and ability to adapt to new situations.

-

Potential for Higher Maintenance Costs While Still Making Payments: As a car ages, maintenance costs typically increase. With an 84-month loan, you could still be making payments on a six or seven-year-old car that requires more frequent and expensive repairs.

This double financial hit – a car payment and significant repair bills – is a situation many buyers regret entering.

The Critical Impact of Loan Length on Your Finances

The length of your car loan isn’t just a number; it’s a financial lever that profoundly influences several key aspects of your personal economy. Understanding these impacts is crucial for making an informed decision.

Monthly Payments

This is the most obvious and immediate effect. A longer loan term spreads the total cost (principal + interest) over more months, resulting in a lower monthly payment. Conversely, a shorter term concentrates that cost into fewer months, leading to a higher monthly payment.

For example, a $30,000 loan at 5% APR might have a monthly payment of around $566 over 60 months, but only about $429 over 84 months. While the latter looks more attractive on the surface, it hides a significant cost increase over time.

Total Interest Paid

This is where the real financial implications of loan length become starkly clear. Even a seemingly small difference in interest rate can be amplified over a longer term. The longer you take to repay the loan, the more opportunities the interest has to accrue.

Using our previous example:

- 60 months at 5% APR: Total interest paid ≈ $3,975

- 84 months at 5% APR: Total interest paid ≈ $6,069

That’s over $2,000 in additional interest for the exact same car, simply by extending the loan by two years. This money could have gone into savings, investments, or paying down other debts.

Equity vs. Negative Equity

As mentioned, loan length directly impacts your equity position. Cars lose a significant portion of their value the moment they’re driven off the lot, and depreciation continues rapidly in the first few years.

With a shorter loan, your payments outpace depreciation, allowing you to build positive equity faster. With a longer loan, especially one with a low down payment, depreciation often outruns your principal payments. This leaves you in a state of negative equity for an extended period, meaning you owe more than the car is worth.

Common mistakes to avoid are ignoring the impact of depreciation. Many buyers assume their car will hold its value, but for most new vehicles, this isn’t the case, especially in the early years. Always consider the potential for negative equity.

Resale Value and Trade-in Options

If you plan to sell or trade in your vehicle before the loan is paid off, your loan length plays a critical role. If you have positive equity, selling or trading in is relatively straightforward. You can use the equity towards your next purchase or simply walk away without debt.

However, if you’re in negative equity, selling your car means you’ll have to come up with the difference out of pocket to pay off the loan. This can severely limit your options and potentially force you to roll the negative equity into your next car loan, perpetuating a cycle of debt.

Factors Influencing Your Ideal Car Loan Length

Choosing the right car loan length isn’t a one-size-fits-all decision. It’s a personal financial choice that should align with your specific circumstances and goals. Several key factors should guide your decision-making process.

1. Your Budget and Monthly Payment Affordability

This is often the primary driver for most buyers. You need to honestly assess how much you can comfortably afford each month without straining your finances. However, remember to balance this with the total cost. Don’t just look for the lowest possible monthly payment if it means paying significantly more in the long run.

Consider all your other expenses and ensure the car payment leaves room for savings, emergencies, and other financial goals.

2. The Interest Rate Offered

Your interest rate is a critical component. A higher interest rate amplifies the total cost, especially on longer loans. Even a small difference in APR can translate to hundreds or thousands of dollars over several years.

Always aim for the lowest possible interest rate by improving your credit score, making a larger down payment, and shopping around for pre-approvals from multiple lenders.

3. Your Down Payment Amount

A larger down payment directly reduces the amount you need to borrow. This not only lowers your monthly payments but also reduces the total interest paid and helps you build equity faster.

Pro tips from us: Aim for at least a 20% down payment on a new car. This significantly cushions the blow of initial depreciation and helps you avoid negative equity from the outset.

4. Your Credit Score

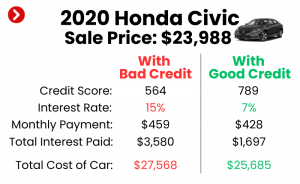

Your credit score is a major determinant of the interest rate you’ll be offered. Borrowers with excellent credit scores (typically 700+) qualify for the best rates, regardless of the loan term. Those with lower scores may face higher rates, making longer terms even more expensive.

Improving your credit score before applying for a loan can save you a substantial amount of money.

5. Vehicle Depreciation Rate

Some vehicles depreciate faster than others. Understanding your chosen car’s typical depreciation curve can help you align your loan term to avoid being underwater for too long. Luxury vehicles, for instance, often depreciate quickly in the early years.

Researching resale values and depreciation trends for specific makes and models is a smart move.

6. Your Financial Goals

Are you aiming for early retirement? Saving for a house? Trying to become debt-free? Your car loan length should align with these broader financial goals. A shorter term supports debt freedom, while a longer term might hinder it.

Consider how this car payment fits into your overall financial roadmap.

7. Planned Ownership Period

How long do you intend to keep the car? If you typically trade in your vehicles every 3-5 years, a 7-year loan makes little sense. You’ll likely be in negative equity when you go to trade it in, creating a financial hurdle.

Match your loan term to your typical car ownership cycle. If you keep cars for a long time (8+ years), a slightly longer loan might be less detrimental, but the interest costs still apply.

Pro Tips for Choosing the Right Car Loan Length

Making the optimal choice requires more than just knowing the numbers; it requires strategic planning and discipline. Here are some actionable tips based on years of observing car buying habits.

- Run the Numbers Thoroughly: Don’t just rely on the dealership’s calculations. Use online car loan calculators to compare monthly payments and, critically, the total cost of the loan across different terms and interest rates. Seeing the full picture will illuminate the true cost of extending your loan.

- Focus on Total Cost, Not Just Monthly Payment: This is the golden rule of car financing. A lower monthly payment feels good in the short term, but if it means paying thousands more over the life of the loan, it’s a false economy. Prioritize minimizing total interest paid.

- Consider Your Lifestyle and Stability: Do you have a stable job with consistent income? Are you planning major life changes like starting a family or buying a home? A long car loan can become a significant burden if your financial situation changes unexpectedly. Choose a term that aligns with your anticipated life stability.

- Prioritize Building Equity Quickly: Aim to pay off your car faster than it depreciates. This means making a substantial down payment and choosing the shortest loan term you can comfortably afford. Building equity gives you financial flexibility and peace of mind.

- The "20/4/10" Rule (A Guideline, Not a Strict Rule): While not universally applicable, a commonly cited guideline suggests a good approach to car buying is to:

- Make at least a 20% down payment.

- Finance the car for no more than four years (48 months).

- Keep your total monthly car expenses (payment, insurance, fuel, maintenance) to no more than 10% of your gross monthly income.

This guideline promotes responsible car ownership and helps avoid overspending.

- Get Pre-Approved from Multiple Lenders: Before you even step foot in a dealership, secure pre-approvals from banks, credit unions, and online lenders. This not only gives you a benchmark interest rate but also lets you compare various loan terms and their associated costs without pressure.

- Negotiate the Out-the-Door Price, Not Just the Monthly Payment: A savvy salesperson might manipulate the loan term to give you a desired monthly payment, even if it means you’re paying more for the car overall. Always negotiate the total price of the vehicle first, then discuss financing terms.

Beyond the Purchase: What If Your Loan Length Isn’t Working?

Sometimes, despite the best planning, circumstances change, or you realize you made a less-than-ideal choice regarding your loan length. All is not lost. There are strategies you can employ to regain control.

Refinancing Your Car Loan

Refinancing involves taking out a new loan to pay off your existing car loan, often with different terms. This can be an excellent option if:

- Interest rates have dropped since you took out your original loan.

- Your credit score has improved, qualifying you for a lower rate.

- You want to shorten your loan term to pay off the car faster and save on interest.

- You want to lengthen your loan term (though generally not recommended) to lower monthly payments during a temporary financial hardship.

Before refinancing, compare the new interest rate, any associated fees, and the total cost of the new loan versus sticking with your current one.

Making Extra Payments or Rounding Up

One of the simplest yet most effective strategies is to pay more than your minimum monthly payment. Even rounding up to the nearest $50 or $100 can significantly reduce the principal balance over time, thereby shortening your loan term and saving you interest.

Ensure any extra payments are applied directly to the principal balance to maximize their impact. Check with your lender to confirm how extra payments are allocated.

Common Mistakes to Avoid When Choosing a Car Loan Length

As an expert, I’ve observed recurring patterns of errors that buyers make. Being aware of these common pitfalls can help you steer clear of them.

- Focusing Solely on the Monthly Payment: This is by far the biggest mistake. The monthly payment is just one piece of the puzzle; the total cost of the loan is the true measure of affordability.

- Ignoring the Total Cost of the Loan: Many buyers don’t bother to calculate how much they’ll pay in interest over the full loan term. This oversight can lead to significant financial regret.

- Not Considering Depreciation: The rapid decline in a new car’s value is a fact of life. Ignoring it when choosing a loan length can leave you in negative equity for years.

- Taking the Longest Term Just Because It’s Offered: Just because a lender offers an 84-month loan doesn’t mean it’s the right choice for you. It’s often offered because it makes an otherwise unaffordable car seem within reach.

- Underestimating Future Financial Changes: Life is unpredictable. A long-term commitment like a car loan can become a burden if your income changes or unexpected expenses arise. Build some financial wiggle room into your budget.

Conclusion: Your Informed Choice for the Road Ahead

The average new car loan length continues to trend upwards, reflecting the rising cost of vehicles and the desire for "affordable" monthly payments. However, as we’ve thoroughly explored, what seems affordable in the short term can become a costly burden over the long haul.

Making an informed decision about your car loan length is about balancing your immediate budget with your long-term financial health. It requires looking beyond the monthly payment to understand the total cost, the impact on your equity, and your overall financial goals. By carefully considering all the factors, leveraging expert tips, and avoiding common mistakes, you can drive off the lot with not only a new car but also a smart financial decision that serves you well for years to come.

Remember, your car loan is more than just a means to an end; it’s a significant financial commitment. Choose wisely, and enjoy the journey! For up-to-date information on auto loan trends and consumer protection, consult reputable financial analysis sites like the Consumer Financial Protection Bureau (CFPB).