Navigating the Road Ahead: What Exactly Is a Co-Applicant on a Car Loan?

Navigating the Road Ahead: What Exactly Is a Co-Applicant on a Car Loan? Carloan.Guidemechanic.com

Buying a car is an exciting milestone, but securing the right financing can often feel like navigating a complex maze. Many prospective car owners encounter terms like "co-applicant" or "co-signer," and understanding these roles is crucial for making informed financial decisions. If you’ve ever wondered how to boost your chances of loan approval, secure better interest rates, or simply share the financial responsibility, then understanding the concept of a co-applicant is your first essential step.

In this comprehensive guide, we’ll strip away the jargon and delve deep into what it means to have a co-applicant on a car loan. We’ll explore the myriad benefits, potential risks, and the critical differences that distinguish a co-applicant from a co-signer. Our goal is to equip you with the knowledge to confidently approach your next car purchase, ensuring a smoother journey from the showroom to your driveway. Let’s hit the road!

Navigating the Road Ahead: What Exactly Is a Co-Applicant on a Car Loan?

Understanding the Core: What Exactly is a Co-Applicant?

When you apply for a car loan, lenders assess your financial health to determine your creditworthiness. A co-applicant on a car loan is essentially another individual who applies for the loan with you. This person shares equal responsibility for the debt, meaning they are just as legally obligated to repay the loan as you are. They are not merely a guarantor; they are an equal partner in the financial commitment.

Think of it like this: both of you are signing the same loan agreement, effectively becoming joint borrowers. This shared responsibility extends beyond just making payments; it encompasses the entire life of the loan. Both names will appear on the loan documents, and often, on the car’s title as well, signifying joint ownership.

From the lender’s perspective, a co-applicant strengthens the loan application. They combine their financial profiles – credit scores, income, and debt-to-income ratios – with yours. This combined financial picture often presents a lower risk to the lender, potentially unlocking more favorable loan terms. Based on my experience in the automotive finance industry, bringing in a financially strong co-applicant is one of the most effective strategies for individuals facing challenges in securing a loan independently.

Why Consider a Co-Applicant for Your Car Loan? The Undeniable Benefits

The decision to include a co-applicant isn’t just about getting approved; it’s about optimizing your loan experience. There are several compelling reasons why this strategy can be highly advantageous. Let’s explore these benefits in detail.

Improved Loan Approval Chances

One of the primary reasons individuals seek a co-applicant is to enhance their eligibility for a car loan. Lenders meticulously scrutinize an applicant’s financial background, looking for indicators of reliability and repayment capacity. If your credit history is limited, you have a lower credit score, or your income alone isn’t robust enough to meet the lender’s requirements, a co-applicant can significantly turn the tide in your favor.

When you apply with a co-applicant, the lender evaluates the combined financial strength of both individuals. A co-applicant with a strong credit score, a stable employment history, and a healthy income can offset any weaknesses in your personal financial profile. This combined strength signals to the lender that there are two parties committed to repayment, effectively reducing the perceived risk of default. It’s like having a safety net, making the lender more comfortable in extending credit.

Better Interest Rates and Loan Terms

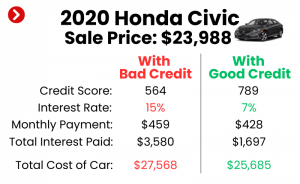

Beyond just getting approved, a strong co-applicant can dramatically impact the cost of your loan. Interest rates are a direct reflection of the lender’s perceived risk; lower risk typically translates to lower interest rates. When the combined credit profile of you and your co-applicant is strong, lenders are more likely to offer competitive rates.

A lower interest rate means you’ll pay less over the life of the loan, saving you hundreds or even thousands of dollars. Moreover, a robust joint application might also open doors to more flexible loan terms, such as a longer repayment period without an exorbitant increase in interest, or lower monthly payments. Pro tips from us: Always shop around with your joint application to see which lenders offer the most attractive rates based on your combined financial strength. Don’t settle for the first offer.

Access to Higher Loan Amounts

Sometimes, your income alone might not qualify you for the car you truly need or desire. If you’re looking to finance a more expensive vehicle, but your individual debt-to-income ratio or overall income doesn’t quite meet the mark, a co-applicant can be the solution. Lenders use income as a critical factor in determining how much debt you can realistically manage.

By adding a co-applicant, you essentially combine your incomes. This aggregated income figure provides a larger financial cushion, demonstrating to the lender that the joint applicants have the capacity to handle a larger monthly payment. This can qualify you for a higher loan amount, making that dream car a more attainable reality. It broadens your financial scope, allowing for more purchasing power.

Building Credit for One or Both Applicants

A car loan is a significant credit-building tool. For individuals with a thin credit file – meaning they haven’t had many credit accounts open for long – or those looking to improve a less-than-perfect score, a co-applicant arrangement can be highly beneficial. When payments are made on time, consistently, it positively reflects on both applicants’ credit reports.

This shared positive payment history helps establish or strengthen credit scores for both individuals involved. It demonstrates responsible financial behavior to credit bureaus, which can lead to better opportunities for future loans, credit cards, and even mortgages. It’s a mutual investment in financial health, provided both parties uphold their payment responsibilities.

Shared Financial Burden and Responsibility

Finally, having a co-applicant means the financial responsibility isn’t solely on one person’s shoulders. While both are equally liable, the psychological and practical benefit of sharing the burden can be substantial. This can be particularly helpful for couples or family members who share expenses and often make large purchases together.

It fosters a sense of teamwork and mutual accountability. In situations where unexpected financial challenges arise for one party, the other can step in to ensure payments are not missed. This shared commitment can alleviate stress and make the process of managing a large loan feel more manageable.

The Flip Side: Risks and Responsibilities of a Co-Applicant

While the benefits of a co-applicant are numerous, it’s crucial to approach this decision with a full understanding of the associated risks and responsibilities. Entering a joint loan agreement is a significant commitment that carries long-term implications for both parties.

Equal Legal Obligation

The most critical aspect to grasp is that a co-applicant holds equal legal obligation for the entire debt. This isn’t a partial responsibility; it’s 100% of the loan. If the primary driver or applicant fails to make payments for any reason, the lender has every right to pursue the co-applicant for the full outstanding balance. This includes not just missed payments but also late fees and potential repossession costs.

There is no "primary" and "secondary" in the eyes of the law regarding repayment responsibility for co-applicants. Both are equally liable. Common mistakes to avoid are assuming that because one person drives the car, the other’s responsibility is somehow lesser. That’s a dangerous misconception that can lead to significant financial distress.

Credit Score Impact – For Better or Worse

Just as positive payment history builds credit for both parties, negative payment history can severely damage both credit scores. Every late payment, missed payment, or default will be reported to credit bureaus under both applicants’ names. This can significantly lower credit scores for both individuals, making it harder to secure future loans, credit cards, or even apartments.

A car loan is a substantial debt, and its management has a profound effect on credit. Even if you, as the co-applicant, are diligently paying your other bills, a default on a joint car loan can tarnish your otherwise perfect credit history. This shared credit risk is a primary reason why choosing a co-applicant requires immense trust and confidence in their financial discipline.

Relationship Strain

Money matters are a leading cause of stress in relationships. Entering a joint financial agreement like a car loan can put a significant strain on personal relationships if things go awry. Disagreements over payments, unexpected financial difficulties for one party, or a breakdown in communication can lead to resentment, arguments, and even permanent damage to friendships or family ties.

Imagine a scenario where the primary driver loses their job and can no longer make payments. The co-applicant is then left to cover the entire monthly payment, potentially for a car they don’t even use. This situation can breed frustration and anger, highlighting the importance of having a robust and trusting relationship before entering such an agreement.

Default Consequences and Asset Seizure

In the unfortunate event of a default, both applicants face the consequences. The lender can take legal action against either or both individuals to recover the debt. This could include wage garnishment, bank account levies, or legal judgments that appear on both credit reports. Furthermore, the car itself serves as collateral for the loan.

If payments stop, the lender has the right to repossess the vehicle. Even if the co-applicant has been making payments, if the loan goes into default, the asset can be seized. This means both parties lose their investment in the car, and still might be liable for any remaining balance after the sale of the repossessed vehicle (a "deficiency balance"). Understanding the severity of these consequences is paramount.

Who Makes a Good Co-Applicant? Choosing Wisely

The decision of who to ask to be your co-applicant is not one to be taken lightly. It requires careful consideration and a deep understanding of trust, financial stability, and shared responsibility. Not everyone is suitable for this role, and selecting the wrong person can lead to significant headaches for both parties.

Trust and Reliability

At the very core, a good co-applicant is someone you trust implicitly. This isn’t just about personal trust, but financial trust. You must be confident in their commitment to the loan, their financial discipline, and their ability to uphold their end of the bargain. This person should be reliable, responsible, and someone with whom you can have open, honest conversations about finances.

Based on my experience, the strongest co-applicant relationships are built on transparency. Both parties should openly discuss their financial situations, expectations, and any potential challenges before signing any documents. A lack of trust or clear communication can quickly turn a beneficial arrangement into a nightmare.

Strong Credit History

The primary financial benefit of a co-applicant often comes from their strong credit history. A good co-applicant will have a high credit score, a proven track record of on-time payments, and a low debt-to-income ratio. Their excellent credit profile will help offset any weaknesses in your own, leading to better loan terms.

Lenders look for a history of responsible borrowing. If your potential co-applicant has a patchy credit history or significant outstanding debt, they may not be the best choice. In fact, a co-applicant with poor credit could actually hinder your application rather than help it, making it even harder to secure approval or favorable terms.

Stable Income and Employment

Lenders prioritize a steady and verifiable income when assessing loan applications. A good co-applicant will have stable employment and a consistent income stream that demonstrates their ability to contribute to or cover the monthly payments if necessary. They should ideally have been in their current job for a reasonable period, indicating stability.

An unstable income, frequent job changes, or reliance on unpredictable income sources can raise red flags for lenders, even if their credit score is decent. The goal is to present the most financially secure picture possible to the lender.

Understanding of Commitment

Both you and your co-applicant must have a complete and clear understanding of the commitment involved. This means fully comprehending the legal obligations, the potential credit impacts, and the long-term financial responsibility. There should be no ambiguity about who is responsible for what, and what happens in various scenarios.

Pro tips from us: Sit down with your potential co-applicant and thoroughly review all loan documents and terms before signing. Discuss hypothetical situations like job loss, relationship changes, or disputes. Ensure both parties are 100% on board and informed.

Legal Age and Residency

Finally, a co-applicant must meet basic legal requirements. They must be of legal age to enter into a contract (typically 18 or 21, depending on the jurisdiction) and often be a legal resident of the country or state where the loan is being originated. These are fundamental prerequisites for any loan agreement.

The Application Process with a Co-Applicant

Applying for a car loan with a co-applicant is similar to a single application, but with a few key differences in terms of documentation and evaluation. Understanding these steps can help streamline the process.

Gathering Documents

Just as you would for a solo application, both you and your co-applicant will need to gather a comprehensive set of documents. This typically includes:

- Proof of Identity: Driver’s license, state ID, passport.

- Proof of Residency: Utility bills, lease agreements.

- Proof of Income: Pay stubs (from both employers), W-2s, tax returns (if self-employed).

- Credit Information: While lenders will pull credit reports, it’s good to have an idea of both your scores beforehand.

- Other Financial Information: Bank statements, details of existing debts.

Ensure all documents are current and readily available to avoid delays.

Joint Application Form

Most lenders have specific application forms for joint applicants. These forms will require detailed financial and personal information from both individuals. It’s crucial that both you and your co-applicant fill out your respective sections accurately and completely. Any discrepancies or missing information can cause processing delays or even lead to rejection.

Both parties will need to sign the application, affirming the accuracy of the information provided and their intent to be equally responsible for the loan.

Lender Evaluation

When a lender receives a joint application, they don’t just pick the stronger applicant; they evaluate the combined financial profile. They will look at:

- Combined Credit Scores: Often taking the lower of the two, or an average, but a strong score from one can significantly boost the overall assessment.

- Combined Income: This helps determine the affordability of the loan.

- Combined Debt-to-Income Ratio: The total monthly debt payments of both applicants relative to their combined gross monthly income. A lower ratio is always better.

- Employment History: Stability of employment for both individuals.

Lenders aim to assess the overall risk presented by the joint application. The stronger the combined profile, the more favorable the loan terms are likely to be.

Approval and Loan Disbursement

Once the lender has thoroughly reviewed the application and performed their due diligence, they will either approve, deny, or offer conditional approval. If approved, both you and your co-applicant will be required to sign the final loan agreement. This document legally binds both of you to the terms and conditions of the loan.

The loan funds will then be disbursed, typically directly to the car dealership. Remember, once signed, both parties are fully responsible for every aspect of the loan. This includes not just the payments, but also any fees, insurance requirements, and adherence to the loan’s covenants. For more details on the general car loan process, you might find our article on helpful.

Co-Applicant vs. Co-Signer: A Crucial Distinction

While often used interchangeably in casual conversation, the terms "co-applicant" and "co-signer" have distinct legal and financial implications that are critical to understand. Misinterpreting these roles can lead to significant misunderstandings and unforeseen consequences.

Ownership Rights

The most significant difference lies in ownership rights. A co-applicant (or co-borrower) is typically listed on the vehicle’s title, meaning they have an ownership stake in the car itself. Both names appear on the title, granting both individuals legal rights to the asset. This shared ownership is a hallmark of a true joint loan.

A co-signer, on the other hand, does not have an ownership stake in the vehicle. Their name does not appear on the title. A co-signer merely guarantees the loan; they pledge to repay the debt if the primary borrower defaults. They are essentially a guarantor, providing their creditworthiness as security, but without any claim to the asset.

Primary vs. Secondary Borrower

In a co-applicant scenario, both individuals are considered primary borrowers from the lender’s perspective. There is no hierarchical distinction; both are equally responsible for the debt and have equal rights to the financed asset.

For a co-signer, there is a clear distinction: one is the primary borrower (who drives and owns the car), and the other is the co-signer (who guarantees the loan). The lender will first pursue the primary borrower for payments. Only if the primary borrower fails to pay will the lender turn to the co-signer. However, it’s important to note that many lenders can pursue either party immediately upon default, so the distinction can be subtle in practice.

When to Choose Which Option

Choose a co-applicant when:

- You want to share ownership of the car.

- Both parties intend to use the car, or it’s a shared family asset.

- Both parties want to benefit from building credit together.

- The combined financial strength is needed to secure approval or better terms, and shared ownership is desired.

Choose a co-signer when:

- The primary borrower wants sole ownership of the vehicle.

- The co-signer’s primary role is simply to provide credit enhancement without taking on ownership rights.

- The co-signer trusts the primary borrower implicitly to make payments but doesn’t want any legal claim to the car.

Understanding this fundamental difference is vital for both parties involved. For a deeper dive into the nuances of joint credit and its impact, you can refer to resources from trusted financial institutions like the Consumer Financial Protection Bureau (CFPB) or major credit bureaus. .

Managing a Joint Car Loan: Best Practices

Securing a car loan with a co-applicant is just the beginning. Effective management of the loan throughout its term is crucial for maintaining financial health and preserving relationships. Here are some best practices to ensure a smooth journey.

Open Communication

Communication is the bedrock of any successful joint financial endeavor. Both parties must maintain open and honest dialogue about the loan, payment schedules, and any potential financial difficulties. Regular check-ins, even informal ones, can prevent misunderstandings and ensure both are on the same page.

If one party experiences a financial setback, it’s imperative to communicate this immediately to the other co-applicant. This allows for proactive planning and prevents missed payments, which can harm both credit scores.

Clear Payment Plan

Before the first payment is due, establish a clear and agreed-upon payment plan. Decide who will be responsible for making the monthly payment, or if it will be split. If splitting, determine the exact amounts and how funds will be transferred. Some couples might opt for one person to make the full payment, with the other reimbursing them for their share.

Automating payments from a joint account or setting up reminders can help ensure consistency. Having a written agreement, even a simple one, can provide clarity and prevent disputes down the line.

Monitoring Credit Reports

Both co-applicants should regularly monitor their credit reports. Since the loan appears on both credit files, it’s essential to ensure that payments are being reported accurately and that no unauthorized activity occurs. You are entitled to a free credit report from each of the three major bureaus annually.

Checking your credit reports allows you to catch any errors or missed payments promptly and address them before they cause significant damage. It also provides peace of mind that the loan is being managed responsibly by both parties. For tips on improving your credit score, check out our guide on .

Refinancing Options

Life circumstances can change. If your financial situation improves, or if interest rates drop, consider exploring refinancing options. Refinancing can potentially lead to a lower interest rate, a smaller monthly payment, or allow one co-applicant to be removed from the loan (if the remaining applicant qualifies on their own).

Discuss refinancing as a joint decision. If one party wishes to be removed, the remaining applicant must be strong enough financially to qualify for the new loan independently. This process requires a new credit check and application.

Handling Disputes

Despite best intentions, disputes can arise. If there are disagreements over payments, usage of the vehicle, or other aspects of the loan, it’s vital to address them constructively. Start with open communication. If an agreement cannot be reached, consider mediation or legal advice.

While hopefully never needed, understanding the legal implications of a default or a dispute can help in navigating difficult situations. It reinforces the importance of choosing a co-applicant with whom you have a strong, trusting relationship.

When Might a Co-Applicant NOT Be the Best Idea?

While the benefits are clear, there are specific scenarios where adding a co-applicant might not be the most prudent choice. It’s important to recognize these situations to avoid potential pitfalls.

Strained Relationships

If your relationship with the potential co-applicant is already strained, unstable, or lacks a strong foundation of trust, involving them in a long-term financial commitment like a car loan is highly risky. Financial stress can exacerbate existing relationship problems, leading to further conflict and potential legal complications.

A loan is a multi-year commitment, and if the relationship sours, you could be left with significant financial and emotional burdens. Always prioritize the stability of your relationship over the perceived convenience of a co-applicant.

One Party Has Bad Credit

The purpose of a co-applicant is often to strengthen a loan application. If your potential co-applicant has a poor credit history, a high debt-to-income ratio, or a history of missed payments, they will not help your application. In fact, their negative financial profile could actually hinder your chances of approval or lead to even higher interest rates.

Lenders consider the combined risk. If one applicant presents a significant risk, it often outweighs the strengths of the other. In such cases, it might be better to work on improving the weaker credit score first before considering a joint application.

Lack of Understanding or Commitment

If either party doesn’t fully grasp the implications of being a co-applicant or isn’t genuinely committed to the shared responsibility, it’s a recipe for disaster. A casual approach to such a significant financial obligation can lead to missed payments, credit score damage, and fractured relationships.

Both individuals must be fully informed, willing, and able to fulfill their obligations. If there’s any hesitation or lack of clarity, it’s a sign to reconsider the joint application.

Ability to Qualify Alone

If you are financially stable, have a good credit score, and can comfortably qualify for a car loan on your own, then adding a co-applicant might be an unnecessary complication. While it could potentially secure a slightly lower interest rate, the added risk to another person’s financial well-being might not be worth the marginal benefit.

Evaluate whether you truly need a co-applicant. If you can manage the loan independently, it might be simpler and less risky to do so. This protects both your financial autonomy and your relationship with a potential co-applicant.

Conclusion: Driving Forward with Confidence

Understanding what a co-applicant on a car loan entails is more than just learning a definition; it’s about making a well-informed financial decision that can significantly impact your future. We’ve explored the profound benefits, from improving your chances of approval and securing better rates to building credit and sharing the financial burden. Yet, we’ve also shone a light on the critical risks, emphasizing the equal legal obligation, potential credit damage, and strain on relationships.

Choosing a co-applicant is a deeply personal and financial decision that demands careful consideration, open communication, and absolute trust. It’s about combining strengths to achieve a common goal, but it requires both parties to fully comprehend their responsibilities and the potential consequences.

As an expert blogger in this field, my ultimate advice is always to educate yourself thoroughly. Weigh the pros and cons meticulously, have candid conversations with your potential co-applicant, and ensure both of you are fully prepared for the commitment ahead. By doing so, you can navigate the complexities of car financing with confidence, secure the best possible terms, and drive away knowing you’ve made a smart, responsible choice. Happy driving!