Navigating the Road Ahead: Your Comprehensive Guide to Getting a Car Loan as a Recent College Graduate

Navigating the Road Ahead: Your Comprehensive Guide to Getting a Car Loan as a Recent College Graduate Carloan.Guidemechanic.com

The ink on your diploma might still be drying, but the open road is calling. For many recent college graduates, a new car represents freedom, independence, and a crucial step into adulthood. Whether it’s for commuting to your first job, visiting family, or simply exploring, reliable transportation is often essential. However, securing an auto loan as a recent grad can feel like navigating a maze without a map. Limited credit history, student loan debt, and new employment status often present unique challenges.

But don’t despair! Based on my extensive experience in personal finance and auto lending, getting a car loan after graduation is absolutely achievable with the right strategy and preparation. This comprehensive guide is designed to empower you with the knowledge, tips, and insights needed to confidently approach the car buying process, secure favorable terms, and drive off in your dream car. We’ll break down every step, from building your financial foundation to understanding the application process, ensuring you’re well-equipped for success.

Navigating the Road Ahead: Your Comprehensive Guide to Getting a Car Loan as a Recent College Graduate

The Reality Check: Why Getting a Car Loan as a Recent Grad Can Be Tricky

Let’s be honest, lenders are in the business of assessing risk. When you’re a recent college graduate, you often present a somewhat unknown quantity. This isn’t a personal judgment; it’s simply how the lending world operates. Understanding these challenges is the first step toward overcoming them.

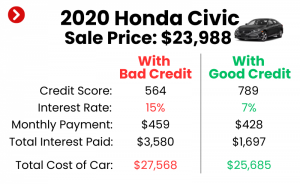

The primary hurdle for most recent grads is a lack of established credit history. Lenders rely heavily on your credit report and score to predict your ability and willingness to repay debt. Without a long track record of responsible borrowing, such as credit card payments or previous loan repayments, they have less data to go on. This can make them hesitant to approve a significant loan like an auto loan, or they might offer higher interest rates to compensate for the perceived risk.

Furthermore, many recent graduates are just starting their careers. While you might have a promising job offer, the short duration of your employment can also be a factor. Lenders prefer to see stable, consistent income over a longer period. Lastly, the shadow of student loan debt, while a common reality, can sometimes impact your debt-to-income (DTI) ratio, another metric lenders use to gauge your financial capacity. These combined factors mean that getting a car loan for a college graduate requires a more strategic approach than for someone with years of established credit and employment.

Building Your Foundation: Essential Steps Before You Apply

Before you even start browsing car lots or online marketplaces, it’s crucial to lay a solid financial groundwork. This preparation will not only increase your chances of loan approval but also help you secure better terms. Think of it as preparing your financial resume for lenders.

Know Your Credit Score (or Lack Thereof)

The very first step is to understand where you stand financially, especially concerning your credit. Even if you’ve never had a credit card or a loan, you might have some entries on your credit report from student loans or utility bills. It’s vital to check your credit report from all three major bureaus – Experian, Equifax, and TransUnion. You are entitled to a free report from each once a year.

Based on my experience, many recent grads are surprised by what they find – or don’t find – on their reports. Look for any errors and dispute them immediately. While you might not have a high FICO score yet, understanding the components of a credit score (payment history, amounts owed, length of credit history, new credit, credit mix) will guide your actions. If you have any existing credit, ensure all payments are on time and in full. This shows immediate responsibility.

Budgeting Like a Pro: What Can You Truly Afford?

This is perhaps the most critical step. It’s incredibly tempting to eye that shiny new car, but the true cost of car ownership extends far beyond the monthly loan payment. You need to create a detailed budget that accounts for everything: the car payment, insurance, fuel, maintenance, registration, and potential repairs. Don’t forget other living expenses like rent, utilities, groceries, and student loan payments.

Pro tips from us: Use a spreadsheet or a budgeting app to track your income and expenses for a month or two. This gives you a realistic picture of your disposable income. A common mistake to avoid is focusing solely on the monthly car payment without considering the overall impact on your financial health. Aim for your total car expenses (payment, insurance, gas, maintenance) to be no more than 10-15% of your net monthly income. This ensures you’re not "car poor" and have room for other financial goals.

Save for a Down Payment: Your Secret Weapon

A significant down payment is one of the most powerful tools a recent college graduate can wield when seeking a car loan. It instantly reduces the amount you need to borrow, which lowers your monthly payments and the total interest paid over the life of the loan. More importantly, it signals to lenders that you are financially responsible and have "skin in the game."

Aim for at least 10-20% of the car’s purchase price as a down payment. If you’re looking at a $20,000 car, a $2,000 to $4,000 down payment can make a huge difference in how lenders view your application. Even if it means waiting a few extra months to save up, the long-term benefits of a larger down payment – better interest rates, lower monthly payments, and less risk of being upside down on your loan – are well worth it.

Understand Interest Rates and How They Affect Your Wallet

Interest rates are the cost of borrowing money, expressed as a percentage of the loan amount. For recent grads with limited credit, initial interest rates might be higher than average. It’s crucial to understand how they work and their impact on your total loan cost. A 1% difference in interest rate can add hundreds, or even thousands, of dollars to the total cost of your car over a 5-year loan term.

Factors influencing your interest rate include your credit score, loan term (shorter terms usually have lower rates but higher monthly payments), the vehicle’s age, and market conditions. Knowledge is power here. By understanding the typical range of rates for your credit profile, you can better evaluate loan offers and recognize a good deal when you see one. Don’t just look at the monthly payment; focus on the Annual Percentage Rate (APR), which includes fees and other costs, giving you a truer picture of the loan’s expense.

Strategies for Loan Approval: Your Blueprint for Success

Now that your financial foundation is solid, let’s explore specific strategies that can significantly boost your chances of getting a car loan as a recent college graduate. These tactics are designed to mitigate the risks lenders perceive and present you as a reliable borrower.

Strategy 1: The Power of a Co-signer

One of the most effective ways for a recent grad to secure a car loan with favorable terms is to apply with a co-signer. A co-signer is someone, typically a parent or close relative, with excellent credit and stable income, who agrees to be equally responsible for the loan if you fail to make payments. This significantly reduces the risk for the lender.

When you have a co-signer, the lender evaluates both your credit profiles. If your co-signer has a strong credit history, it effectively "lends" their creditworthiness to your application, making you a much more attractive borrower. This can lead to approval for a loan you might not get on your own, often with a much lower interest rate. However, it’s vital to understand the commitment. If you miss payments, it impacts your co-signer’s credit score, and they are legally obligated to pay. This is a big ask, so ensure you both fully understand the responsibility involved.

Strategy 2: Exploring Dealership "New Grad Programs" and Subprime Lenders

Many major car manufacturers recognize the unique challenges recent graduates face and offer special programs designed to help them get into a new vehicle. These "New Grad Programs" often provide benefits like reduced interest rates, waived down payment requirements, or cash back incentives specifically for college graduates. Eligibility typically requires a degree within the last two years, proof of employment, and a minimum income.

While these manufacturer programs are excellent options, they might still require some credit history. If you don’t qualify for these or prime loans, subprime lenders specialize in working with borrowers who have limited or poor credit. Be aware that these loans come with significantly higher interest rates due to the increased risk. While they can provide an entry point to car ownership and credit building, approach them with caution and ensure you can comfortably afford the payments. This can be a viable path to getting a car loan, but it’s crucial to understand the long-term cost.

Strategy 3: Dealership Financing vs. Bank/Credit Union Loans

When it comes to where you get your loan, you essentially have two main avenues: directly from a bank or credit union, or through the dealership. Each has its pros and cons.

Applying for a loan directly with a bank or credit union (often called getting "pre-approved") is highly recommended. Based on my experience, this gives you a strong negotiating position at the dealership because you walk in with your own financing already secured. You know the maximum amount you can borrow and your interest rate, allowing you to focus solely on negotiating the car’s price. Credit unions, in particular, often offer more competitive rates and a more personalized approach, which can be beneficial for recent grads.

Dealership financing can be convenient, as it’s a one-stop shop. They work with multiple lenders to find you a loan. However, without a pre-approval, you might not know if you’re getting the best rate. Always compare any offers from the dealership with your pre-approved loan. Sometimes, dealerships can beat your pre-approval, especially if they are trying to move specific inventory, but having your own financing empowers you to make an informed decision and avoid potential markups.

Strategy 4: The Art of Negotiation

Once you have your financing in order, the next step is negotiating the car’s price. Remember, the dealer wants to sell a car, and you want to buy one at a fair price. Don’t be afraid to negotiate. Focus on the total purchase price of the car, not just the monthly payment. A common mistake is getting fixated on a low monthly payment, which can often be achieved by extending the loan term, leading to more interest paid over time.

Do your research on the car’s value using sites like Kelley Blue Book (KBB) or Edmunds. Be prepared to walk away if the deal isn’t right. Pro tips from us: Consider buying at the end of the month or quarter when sales quotas are a factor, which might give you more leverage. Also, be mindful of add-ons and extended warranties; while some might be valuable, many are high-profit items for the dealership and can often be negotiated down or purchased separately.

Strategy 5: Consider a Reliable Used Car

While the allure of a brand-new car is strong, a reliable used car can be a much more financially sensible option for a recent college graduate. Used cars are generally less expensive, which means you’ll need to borrow less, making loan approval easier and your monthly payments more manageable. They also depreciate slower than new cars, retaining their value better over the first few years.

Lower car value often translates to lower insurance premiums as well, which is another significant cost saving. When choosing a used car, focus on models known for their reliability and good resale value. Get a pre-purchase inspection from an independent mechanic to ensure there are no hidden issues. This approach can help you build credit responsibly while minimizing your financial burden, setting you up for a new car purchase down the line when your credit history is more robust.

Navigating the Application Process: What to Expect

Once you’ve identified a car and chosen your preferred lending strategy, it’s time to complete the loan application. This isn’t as daunting as it sounds, especially with proper preparation. Knowing what to expect will help you feel more confident and less stressed.

Gathering Your Documents

Lenders require specific documentation to verify your identity, income, and employment. Having these ready will significantly speed up the application process. Based on my experience, the more organized you are, the smoother this step will be.

You’ll typically need:

- Proof of Identity: Driver’s license, passport.

- Proof of Income: Recent pay stubs (usually 2-3 months), offer letter if you’ve just started a new job, bank statements.

- Proof of Employment: Contact information for your employer, possibly an employment verification letter.

- Proof of Residence: Utility bill, lease agreement, or bank statement with your current address.

- Vehicle Information: If you’ve already chosen a car, you’ll need its VIN (Vehicle Identification Number) and purchase price.

- Graduation Verification: Your diploma or official transcripts for new grad programs.

Filling Out the Application

Whether online or in person, take your time to fill out the application accurately and completely. Be honest about your financial situation. Lenders will verify the information you provide, and any discrepancies can lead to delays or denial.

One crucial point: avoid applying for multiple loans simultaneously within a short period. Each loan application results in a "hard inquiry" on your credit report, which can temporarily lower your credit score. If you’re shopping for the best rate, try to do all your applications within a 14-45 day window, as credit scoring models often count these as a single inquiry for rate shopping purposes. This allows you to compare offers without unnecessarily harming your credit.

Understanding Loan Offers

Once approved, you’ll receive a loan offer detailing the terms. Don’t just glance at the monthly payment. Pay close attention to the Annual Percentage Rate (APR), the loan term (e.g., 60 months, 72 months), and any associated fees. A lower monthly payment often means a longer loan term, which translates to more interest paid over time.

Compare offers side-by-side. Calculate the total cost of each loan by multiplying the monthly payment by the loan term and adding any upfront fees. This comprehensive view will help you choose the loan that best fits your budget and financial goals. If you have questions about any part of the loan agreement, ask! It’s your right to understand every clause before you sign.

Common Mistakes Recent Grads Make (and How to Avoid Them)

Navigating your first major loan can be daunting, and it’s easy to fall into common traps. Being aware of these pitfalls will help you make smarter decisions.

- Not Checking Credit (or Lack Thereof): As discussed, this is foundational. Don’t go into the process blind. Understand your starting point.

- Buying Too Much Car: This is perhaps the biggest mistake. The excitement of a new purchase can overshadow financial prudence. Stick to your budget, even if a lender approves you for a higher amount. Remember, just because you can borrow it doesn’t mean you should.

- Ignoring Insurance Costs: Auto insurance can be a significant expense, especially for younger drivers. Get insurance quotes before you finalize your car purchase. A car that’s affordable in payments might become unaffordable with high insurance premiums.

- Applying Everywhere (Multiple Hard Inquiries): Resist the urge to submit applications to every lender you see. Strategically target a few lenders within the rate-shopping window to minimize credit score impact.

- Skipping the Down Payment: While some loans might allow this, it’s almost always a bad idea. A down payment provides equity, reduces your loan amount, and protects you from being "upside down" on your loan (owing more than the car is worth).

- Not Understanding the Full Loan Terms: Don’t just focus on the monthly payment. Understand the APR, total interest paid, and any prepayment penalties.

- Forgetting About Maintenance: Cars need oil changes, tire rotations, and occasional repairs. Factor these ongoing costs into your budget.

Pro Tips for a Smooth Ride (Post-Approval)

Congratulations, you’ve secured your car loan and driven off the lot! But the journey isn’t over. Responsible loan management is crucial for building a strong financial future.

- Make Payments On Time, Every Time: This is non-negotiable. Timely payments are the most critical factor in building a positive credit history. Set up automatic payments to avoid missing due dates.

- Consider Refinancing Later: Once you’ve established a year or two of on-time payments and your credit score has improved, you might qualify for a lower interest rate by refinancing your car loan. This can save you a significant amount of money over the remaining loan term. Keep an eye on market interest rates and your evolving credit profile.

- Build an Emergency Fund: Life happens. A flat tire, an unexpected repair, or even a temporary job loss can impact your ability to make car payments. Having an emergency fund (3-6 months of living expenses) provides a crucial safety net, ensuring you can meet your obligations even when unforeseen circumstances arise. For a deeper dive into managing student loan debt while planning big purchases, check out our guide on .

- Stay within Your Budget: Don’t let new income or lifestyle creep tempt you into taking on more debt. Continue to live within your means and prioritize your financial goals. If you’re looking for more comprehensive budgeting strategies, our article on can provide invaluable insights.

Conclusion: Your Road to Financial Independence Starts Here

Getting a car loan as a recent college graduate might seem like a formidable challenge, but it is entirely within your reach. By understanding the landscape, preparing meticulously, and employing smart strategies, you can secure the financing you need to embark on your next adventure. Remember, this isn’t just about getting a car; it’s about making a significant financial decision that will impact your credit history and future borrowing power.

Embrace the process with diligence, ask questions, and prioritize financial prudence over immediate gratification. Focus on building a strong credit foundation, making informed choices about affordability, and being a responsible borrower. The freedom of the open road awaits, and with this guide, you’re well-equipped to navigate your way to a successful car loan approval and a solid start to your financial independence.

For additional trusted resources on credit and consumer finance, we recommend visiting the Consumer Financial Protection Bureau (CFPB) website at . They offer a wealth of information to help you make informed financial decisions. What are your biggest concerns about getting a car loan after graduation? Share your thoughts and questions in the comments below!