Navigating the Road Ahead: Your Comprehensive Guide to Getting a Car Loan with a 598 Credit Score

Navigating the Road Ahead: Your Comprehensive Guide to Getting a Car Loan with a 598 Credit Score Carloan.Guidemechanic.com

Finding yourself with a 598 credit score when you need a car can feel like hitting a major roadblock. Many people assume that a credit score in this range automatically disqualifies them from securing a car loan. However, based on my experience in the financial landscape, this isn’t necessarily true. While a 598 credit score presents challenges, it certainly doesn’t close the door entirely.

This comprehensive guide is designed to empower you with the knowledge and strategies needed to secure a car loan, even with a subprime credit score. We’ll explore what a 598 score means for lenders, how to prepare effectively, where to find the right financing, and crucial steps to take for a successful outcome. Our ultimate goal is to help you drive away in the car you need, armed with confidence and a clear path forward.

Navigating the Road Ahead: Your Comprehensive Guide to Getting a Car Loan with a 598 Credit Score

Understanding Your 598 Credit Score: What It Really Means for Lenders

A 598 credit score falls into what is typically known as the "Fair" or "Subprime" category. On the FICO scale, which ranges from 300 to 850, scores below 620 are generally considered subprime. This classification signals to lenders that you might carry a higher risk of defaulting on a loan compared to borrowers with higher scores.

Lenders use your credit score as a quick snapshot of your creditworthiness. A 598 score suggests a history that might include late payments, high credit utilization, or limited credit history. While it’s not ideal, it’s also not the lowest score possible, indicating there’s room for improvement and a chance for approval. It simply means you’ll need to approach the car loan process more strategically.

The Real-World Implications of a Subprime Score

The most significant implication of a 598 credit score is the interest rate you’ll likely be offered. Lenders compensate for the perceived higher risk by charging a higher Annual Percentage Rate (APR). This means your monthly payments will be higher, and the total cost of the car over the loan term will be significantly greater than for someone with excellent credit.

Additionally, lenders might impose stricter terms, such as requiring a larger down payment or a shorter loan term. They might also limit the amount you can borrow or the type of vehicle you can finance. Understanding these realities upfront helps set realistic expectations and guides your preparation.

Is a Car Loan with a 598 Credit Score Really Possible? The Good News

Yes, getting a car loan with a 598 credit score is absolutely possible. Many lenders specialize in working with individuals who have subprime credit. They understand that life happens, and a credit score doesn’t always tell the whole story of someone’s financial capability or intent.

The key is to demonstrate to these lenders that, despite your credit score, you are a responsible borrower. This involves showcasing financial stability through steady income, a reasonable debt-to-income ratio, and a commitment to making timely payments. It’s about building a compelling case beyond just your credit score.

Demonstrating Your Financial Responsibility

Lenders want to see evidence that you can and will repay the loan. Even with a lower credit score, strong mitigating factors can sway their decision. A stable job history, a good income relative to your debts, and a substantial down payment can all paint a more favorable picture. These elements reduce the lender’s risk and make them more comfortable extending credit to you.

Remember, a 598 credit score indicates a need for careful planning and execution. It’s not a barrier, but rather a prompt to be exceptionally well-prepared. With the right approach, you can turn a challenging situation into a successful car purchase.

Essential Preparation Steps Before You Apply

Preparation is your most powerful tool when seeking a car loan with a 598 credit score. Approaching lenders without proper groundwork can lead to multiple rejections, which can further negatively impact your credit score. Taking these steps seriously will significantly increase your chances of approval and help you secure more favorable terms.

1. Check Your Credit Report Thoroughly and Dispute Errors

Before anything else, obtain copies of your credit reports from all three major bureaus: Experian, Equifax, and TransUnion. You can get free copies annually from AnnualCreditReport.com. Carefully review each report for any inaccuracies or outdated information.

Pro tips from us: Errors on your credit report are surprisingly common and can unfairly drag down your score. Disputing these errors can lead to a quick bump in your score, potentially pushing you into a slightly better credit tier. This small step can make a big difference in the interest rate you qualify for. For detailed information on disputing errors, you can refer to trusted sources like the Consumer Financial Protection Bureau for guidance.

2. Save for a Significant Down Payment

A substantial down payment is one of the most effective ways to offset a lower credit score. Lenders view a large down payment as a sign of your commitment and reduces the amount they need to finance. This lowers their risk significantly.

Aim for at least 10-20% of the car’s purchase price, if not more. Not only does it make you a more attractive borrower, but it also reduces your monthly payments and the total interest paid over the life of the loan. This is a powerful leverage point you control.

3. Establish a Realistic Budget

Before you even start looking at cars, determine exactly how much you can comfortably afford each month for a car payment, insurance, fuel, and maintenance. Many people overlook the true cost of car ownership beyond just the loan payment.

Use a budget planner to track your income and expenses. This will give you a clear picture of your disposable income and prevent you from taking on a loan that stretches your finances too thin. Common mistakes to avoid are focusing solely on the monthly payment without considering the total cost or how it fits into your overall budget.

4. Know What Car You Can Afford (and Need)

With a 598 credit score, it’s crucial to be realistic about the type of car you can finance. While a brand new luxury vehicle might be appealing, a more affordable, reliable used car is often the smarter choice. Look for vehicles that are a few years old, have good mileage, and a strong resale value.

The goal is to get a reliable car that meets your needs without overextending your budget. Remember, you can always upgrade your vehicle in the future once your credit score has improved. Focus on practicality over prestige for now.

5. Understand Your Debt-to-Income Ratio

Your debt-to-income (DTI) ratio is another critical factor lenders consider. This is the percentage of your gross monthly income that goes towards debt payments. Lenders prefer a DTI of 36% or less, though some subprime lenders might approve higher.

A high DTI signals that you’re already heavily burdened with debt, making it riskier to take on a new car loan. If your DTI is high, consider paying down some existing debts before applying for a car loan. This demonstrates proactive financial management.

Navigating the Lender Landscape

Not all lenders are created equal, especially when you have a 598 credit score. Knowing where to look and what to expect from different types of lenders can save you time, frustration, and potentially money. Each option has its own advantages and disadvantages.

Dealership Financing: Convenience with Caveats

Many car dealerships offer in-house financing or work with a network of lenders. This can be convenient, as you can often complete the car shopping and financing in one place. Dealerships often have relationships with subprime lenders who are more willing to approve loans for lower credit scores.

However, be wary of "Buy Here, Pay Here" dealerships. While they often guarantee approval regardless of credit, their interest rates are typically very high, and their loan terms can be unfavorable. Always compare their offers with other lenders.

Online Lenders: Specialists in Subprime Loans

The digital age has brought forth numerous online lenders specializing in car loans for individuals with less-than-perfect credit. These lenders often have more flexible underwriting criteria than traditional banks. They can provide pre-approvals quickly, allowing you to shop with confidence.

Doing your research and reading reviews for online lenders is crucial. Look for reputable companies with transparent terms and good customer service. Applying for pre-approval with a few different online lenders can help you compare offers without impacting your credit score too much.

Credit Unions: Often More Flexible

If you are a member of a credit union, or if you qualify to join one, they can be an excellent option. Credit unions are member-owned financial institutions that often offer more competitive interest rates and more flexible terms than traditional banks. They tend to be more understanding of individual circumstances.

Because they are focused on their members’ financial well-being, credit unions might be more willing to look beyond your credit score if you have a strong relationship with them. It’s definitely worth exploring if you have a credit union connection.

Local Banks: Might Be Tougher Without a Relationship

Traditional banks generally have stricter lending criteria and prefer borrowers with higher credit scores. While you can certainly apply at your local bank, especially if you have an existing banking relationship, be prepared for a higher chance of rejection or less favorable terms.

However, if you have a long-standing history with your bank, a personal loan officer might be able to advocate for you. It never hurts to inquire, but keep your expectations realistic.

The Application Process: What Lenders Look For

When applying for a car loan with a 598 credit score, lenders will scrutinize your application even more closely. Beyond your credit score, they are looking for specific indicators of your ability and willingness to repay the loan. Being prepared with all necessary documentation and understanding their criteria will streamline the process.

Gathering Your Documents

Before you even fill out an application, have all your essential documents organized. This includes:

- Government-issued ID (driver’s license).

- Proof of income (pay stubs, tax returns, bank statements).

- Proof of residence (utility bill, lease agreement).

- Insurance information.

- Trade-in vehicle title (if applicable).

Having these ready demonstrates your seriousness and efficiency, making the application process smoother for both you and the lender.

Income Stability and Employment History

Lenders want to see a stable income source and a consistent employment history. A steady job for at least six months to a year at the same employer indicates reliability. If you’ve recently changed jobs, be prepared to explain the circumstances and demonstrate that your new position is stable.

Your income must be sufficient to cover the car payments, your existing debts, and living expenses. Lenders will carefully assess this, as it directly impacts your ability to make payments.

Current Debts and Expenses

As mentioned with the DTI ratio, lenders will evaluate your current debt obligations. This includes credit card balances, student loans, mortgages, and any other monthly payments. They want to ensure that adding a car loan won’t push you into a financially precarious position.

Being proactive and reducing some of your existing debt before applying can significantly improve your chances of approval. This shows a commitment to financial health.

The Importance of Pre-Approval

Seeking pre-approval from a few different lenders is a smart strategy. Pre-approval involves a soft credit inquiry, which doesn’t hurt your credit score, and gives you an idea of the loan amount and interest rate you might qualify for. This allows you to shop for a car with a clear budget in mind.

It also gives you leverage at the dealership. You walk in as a cash buyer, knowing exactly how much financing you have. This prevents you from being pressured into unfavorable dealership financing options. For more information on navigating the car buying process with less-than-perfect credit, you might find our article on Securing a Car Loan with Bad Credit helpful. (Replace with actual internal link).

Deciphering Your Loan Offer: Key Terms to Understand

Once you start receiving loan offers, it’s critical to understand the fine print. Don’t just focus on the monthly payment. Several key terms will dictate the true cost of your car loan, especially with a 598 credit score. Common mistakes to avoid are rushing through this stage or failing to compare offers thoroughly.

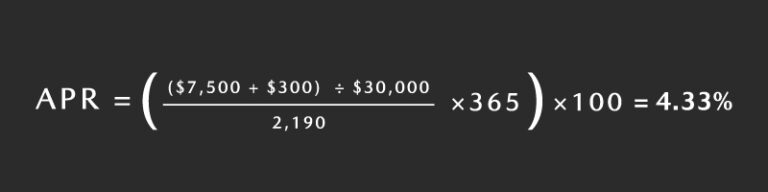

Annual Percentage Rate (APR)

The APR is the most crucial number to look at. It represents the total cost of borrowing money annually, including the interest rate and any associated fees. With a 598 credit score, expect your APR to be significantly higher than prime borrowers. For instance, while someone with excellent credit might get an APR of 5-7%, you might see offers in the 15-25% range, or even higher.

A higher APR means you’ll pay substantially more over the life of the loan. Always compare APRs from different lenders to find the most competitive offer. Even a difference of a few percentage points can save you thousands.

Loan Term Length

The loan term is the duration over which you will repay the loan, typically measured in months (e.g., 36, 48, 60, 72 months). A longer loan term results in lower monthly payments, but it also means you’ll pay more in total interest over time.

For borrowers with a 598 credit score, it’s often tempting to choose the longest term for lower monthly payments. However, this dramatically increases the total cost of the car. Try to opt for the shortest loan term you can comfortably afford to minimize interest payments.

Total Cost of the Loan

Beyond the monthly payment and APR, calculate the total cost of the loan. Multiply your monthly payment by the number of months in the loan term. This will give you the principal plus the total interest paid. Compare this figure across different offers.

Sometimes, a slightly higher monthly payment over a shorter term can lead to a much lower total cost in the long run. Don’t let a low monthly payment obscure the overall financial impact.

Beware of Add-ons and Fees

Dealerships often try to sell you various add-ons like extended warranties, GAP insurance, paint protection, or VIN etching. While some of these might have value, they significantly increase the total amount you finance, which means more interest paid.

Carefully evaluate each add-on and decline anything you don’t genuinely need or can get cheaper elsewhere. Negotiate these items separately, and never feel pressured to accept them.

Strategies for Improving Your Credit Score (Even After Getting the Loan)

Securing a car loan with a 598 credit score is a significant achievement, but it’s also an opportunity to start rebuilding your credit. Improving your score will open doors to better financial products and lower interest rates in the future. This journey doesn’t end when you drive off the lot; it’s just beginning.

Payment History is Paramount

Your payment history accounts for 35% of your FICO score, making it the most critical factor. Making every car loan payment on time, every single month, is crucial. Set up automatic payments or calendar reminders to ensure you never miss a due date.

Consistent on-time payments will steadily improve your credit score over time, demonstrating responsible financial behavior to future lenders. This positive payment history will be a cornerstone of your credit rebuilding efforts.

Reduce Credit Utilization

Your credit utilization ratio (the amount of credit you’re using compared to your total available credit) makes up 30% of your FICO score. Keep your credit card balances as low as possible, ideally below 30% of your credit limit.

Paying down credit card debt not only improves your DTI ratio but also boosts your credit score significantly. This shows lenders that you’re not over-reliant on credit.

Avoid New Debt

While you’re working on improving your credit, try to avoid opening new credit accounts. Each new application can result in a hard inquiry on your credit report, temporarily lowering your score. Focus on managing your existing debt and your new car loan responsibly.

Allow your credit history to stabilize and grow stronger before seeking additional credit. Patience is key in credit building.

Consider a Secured Credit Card

If you don’t have many active credit lines, a secured credit card can be a great tool for credit building. You provide a cash deposit that acts as your credit limit, making it low-risk for lenders. Use it for small, regular purchases and pay the balance in full each month.

This establishes a positive payment history and diversifies your credit mix, both of which contribute to a higher credit score. For further strategies on rebuilding your credit, you might find our article on Quick Ways to Boost Your Credit Score helpful. (Replace with actual internal link).

Regularly Monitor Your Credit

Continue to monitor your credit reports regularly for any new errors or suspicious activity. Identity theft and fraud can severely damage your credit score. Being vigilant allows you to catch and address issues promptly.

Many credit card companies and banks offer free credit monitoring services, making it easier to keep an eye on your credit health.

Alternative Paths and Backup Plans

Sometimes, despite your best efforts, securing a car loan with a 598 credit score on favorable terms might not be immediately possible. It’s always wise to have backup plans in place. These alternatives can still get you where you need to go while you continue to build your credit.

Consider a Co-signer

If a trusted family member or friend with excellent credit is willing to co-sign your loan, this can significantly improve your chances of approval and secure a lower interest rate. A co-signer essentially guarantees the loan, taking on the responsibility if you default.

However, understand the gravity of this decision. If you miss payments, it negatively impacts both your credit and your co-signer’s. This should only be pursued with someone you trust implicitly and after a thorough discussion of the responsibilities involved.

Buy a Cheaper, Older Car Outright

If financing proves too challenging or expensive, consider purchasing a much cheaper, older car with cash. While it might not be your dream vehicle, a reliable used car can provide transportation while you save money and improve your credit score.

This avoids taking on high-interest debt and allows you to build a stronger financial foundation for a better car purchase in the future.

Public Transportation/Ridesharing

Depending on where you live, public transportation or ridesharing services might be a viable temporary solution. This can save you money on car payments, insurance, fuel, and maintenance, which you can then put towards saving for a down payment or paying down existing debt.

It’s not always convenient, but it can be a financially prudent choice until you’re in a better position to finance a car.

Wait and Save More

Sometimes, the best strategy is simply to wait. Use the time to save a larger down payment and actively work on improving your credit score. Even a few months of diligent credit building and saving can make a significant difference in the loan offers you receive.

Patience can save you thousands of dollars in interest and give you more control over your car buying experience.

Common Pitfalls to Sidestep When Seeking a 598 Credit Score Car Loan

Navigating the car loan process with a subprime credit score is fraught with potential missteps. Being aware of these common pitfalls can help you avoid making costly mistakes that could further damage your credit or lead to a financially unsustainable situation.

Applying with Too Many Lenders

Resist the urge to apply for a loan with every lender you encounter. Each hard inquiry on your credit report can temporarily lower your score. Instead, use pre-qualification (which involves a soft inquiry) to gauge your eligibility with a few lenders before submitting full applications.

Aim to get pre-approved by 2-3 reputable lenders and then compare their offers. This strategic approach minimizes negative impacts on your credit score.

Ignoring Your Budget

As mentioned earlier, failing to establish and stick to a realistic budget is a recipe for disaster. It’s easy to get caught up in the excitement of car shopping and agree to payments that are too high. Always remember the total cost of ownership, not just the monthly payment.

Overextending yourself financially can lead to missed payments, repossession, and further damage to your credit score. Be disciplined with your budget.

Falling for "Guaranteed Approval" Scams

Be extremely wary of any lender promising "guaranteed approval" regardless of your credit score. These often come with predatory interest rates, hidden fees, and highly unfavorable terms designed to trap borrowers in a cycle of debt.

Legitimate lenders will always perform some level of credit assessment. If an offer seems too good to be true, it almost certainly is.

Not Reading the Fine Print

Never sign a contract without thoroughly reading and understanding every single clause. This includes the APR, loan term, total cost, late payment penalties, and any additional fees or add-ons. If something isn’t clear, ask questions until you fully comprehend it.

It’s wise to take the contract home to review it calmly or even have a trusted financial advisor look it over. Don’t let pressure from a salesperson rush you.

Focusing Only on Monthly Payments

While a low monthly payment is attractive, it often comes at the cost of a much longer loan term and significantly more interest paid over time. As we discussed, prioritize the overall cost of the loan and choose the shortest term you can comfortably afford.

A seemingly affordable monthly payment can hide a very expensive total loan if you’re not paying attention to the APR and term length.

Driving Towards a Brighter Financial Future

Getting a car loan with a 598 credit score might seem daunting, but it is an achievable goal with the right preparation and strategy. By understanding what your credit score means, meticulously preparing your finances, and carefully selecting your lender and loan terms, you can navigate this process successfully.

Remember, this isn’t just about getting a car; it’s about making a smart financial decision that can pave the way for a stronger credit future. Use this opportunity to demonstrate your reliability, make consistent on-time payments, and actively work towards improving your credit score. The road ahead may have a few bumps, but with informed choices and diligent effort, you’ll be driving towards a brighter financial horizon. Start your preparation today, and take control of your journey!