Navigating the Road Ahead: Your Comprehensive Guide to Getting a Car Loan With Credit Card Debt

Navigating the Road Ahead: Your Comprehensive Guide to Getting a Car Loan With Credit Card Debt Carloan.Guidemechanic.com

Dreaming of a new car but worried your credit card debt stands in the way? You’re not alone. Many individuals find themselves in a similar situation, balancing the desire for reliable transportation with existing financial commitments. The good news is, getting a car loan with credit card debt isn’t an impossible feat. It requires a strategic approach, a clear understanding of how lenders assess risk, and a commitment to improving your financial standing.

As an expert blogger and professional SEO content writer, I’ve seen countless people navigate these waters successfully. This comprehensive guide will equip you with the knowledge and actionable strategies to increase your chances of approval, secure favorable terms, and drive off with confidence, even with existing credit card debt. Let’s hit the road to financial clarity!

Navigating the Road Ahead: Your Comprehensive Guide to Getting a Car Loan With Credit Card Debt

The Reality of Car Loans with Existing Credit Card Debt

It’s important to acknowledge the elephant in the room: credit card debt can make securing a new loan more challenging. Lenders view your existing debt as a factor that influences your ability to take on new financial obligations. This isn’t to say it’s a brick wall, but rather a hurdle that requires a well-thought-out jump.

Your credit card debt primarily impacts two crucial aspects of your financial profile: your credit score and your debt-to-income (DTI) ratio. Both of these are critical metrics that auto lenders scrutinize when evaluating your loan application. Understanding their importance is the first step toward building a stronger case for yourself.

How Lenders View Your Application: Key Factors at Play

When you apply for a car loan, lenders aren’t just looking at your income. They’re assessing a holistic picture of your financial health to determine your creditworthiness and the risk involved in lending to you. Here’s a breakdown of the key factors they consider:

1. Your Credit Score: The Ultimate Report Card

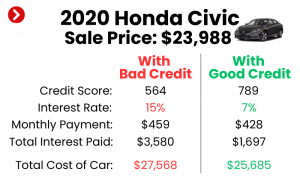

Your credit score is a three-digit number that summarizes your credit history and predicts your likelihood of repaying a loan. Credit card debt, especially high balances or late payments, can significantly lower this score. A lower credit score signals higher risk to lenders, potentially leading to higher interest rates or even loan denial.

Based on my experience, many people underestimate the power of their credit score. It’s not just about getting approved; it’s about getting approved for a good loan. A strong score can save you thousands of dollars in interest over the life of your car loan.

2. Debt-to-Income (DTI) Ratio: Are You Overburdened?

Your DTI ratio compares your total monthly debt payments to your gross monthly income. Lenders use this ratio to determine if you can comfortably afford an additional monthly car payment on top of your existing credit card bills, student loans, mortgage, or rent. A high DTI suggests you might be stretched too thin financially.

For most auto lenders, a DTI ratio of 36% or lower is generally preferred, although some may go higher depending on other factors. This ratio directly shows how much of your income is already committed to debt, which leaves less for a new car payment.

3. Payment History: A Track Record of Responsibility

Lenders want to see consistent, on-time payments across all your existing debts, including credit cards. A history of late or missed payments, even on a small credit card bill, raises red flags. It indicates potential financial instability or a lack of commitment to your obligations.

Pro tips from us: Your payment history is one of the most heavily weighted factors in your credit score. Even if your balances are high, consistently making at least the minimum payments on time demonstrates a level of financial discipline that lenders appreciate.

4. Stability: Employment and Residency

Lenders also look for stability in your life. This includes a consistent employment history, preferably with the same employer for a significant period (e.g., two years or more), and a stable residency. These factors suggest a reliable income stream and a settled lifestyle, which makes you a more dependable borrower.

Frequent job changes or moving every year can sometimes be viewed as indicators of instability, even if they aren’t directly related to your credit card debt. Lenders prefer predictability.

Strategies to Improve Your Chances of Approval

While the presence of credit card debt presents challenges, it doesn’t mean you’re out of options. With strategic planning and effort, you can significantly bolster your application. Here’s how:

1. Pre-Loan Preparations: Laying the Groundwork

Before you even step foot in a dealership or apply online, take these crucial steps to strengthen your financial profile:

-

Review Your Credit Report Meticulously:

- Obtain free copies of your credit report from all three major bureaus (Equifax, Experian, TransUnion) via AnnualCreditReport.com. Scrutinize them for any errors, inaccuracies, or fraudulent activity. Disputing and correcting these can instantly boost your score.

- Common mistakes to avoid are not checking your credit report at all. You might be surprised by incorrect information that is unfairly dragging down your score.

-

Pay Down Existing Credit Card Debt (Even a Little Helps):

- This is perhaps the most impactful step. Reducing your credit card balances lowers your credit utilization ratio (the amount of credit you’re using versus your total available credit). A utilization ratio below 30% is generally recommended, with 10% being ideal for top scores.

- Even paying off one small balance can make a difference. It shows initiative and immediately frees up some of your DTI.

-

Avoid New Credit Applications:

- Resist the urge to apply for new credit cards or other loans in the months leading up to your car loan application. Each hard inquiry can temporarily ding your credit score, and opening new lines of credit increases your overall debt load.

-

Build an Emergency Fund:

- While not directly impacting your credit score, having a small emergency fund (even a few hundred dollars) can provide peace of mind and prevent you from relying on credit cards for unexpected expenses, which could further complicate your debt situation.

2. During the Loan Application Process: Presenting Your Best Self

Once you’ve done your pre-work, these strategies will help you secure the best possible car loan with credit card debt:

-

Shop Around for Lenders:

- Don’t just take the first offer. Banks, credit unions, online lenders, and even dealership financing all have different criteria and rates. Credit unions, in particular, are often more flexible and offer better rates to members, especially if you have an existing relationship with them.

- Submit all your car loan applications within a short timeframe (typically 14-45 days, depending on the scoring model). This allows multiple inquiries for the same type of loan to be counted as a single hard inquiry, minimizing the impact on your credit score.

-

Consider a Co-signer:

- If your credit score or DTI ratio is a major concern, a co-signer with excellent credit can significantly improve your chances of approval and help you secure a lower interest rate. A co-signer essentially pledges their creditworthiness to back your loan.

- However, be aware of the implications: the co-signer is equally responsible for the loan, and any missed payments will affect their credit as well. This should only be considered with someone you trust implicitly and who understands the risks.

-

Make a Larger Down Payment:

- A substantial down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay over the life of the loan. It also signals to lenders that you’re financially committed and serious about the purchase.

- From years of observing lending practices, a larger down payment acts as a buffer against perceived risk from your credit card debt. It shows you have some savings and are willing to put your own money on the line.

-

Opt for a More Affordable Car:

- Be realistic about what you can afford. Instead of stretching for your dream car, choose a vehicle that fits comfortably within your budget, especially when you have existing credit card debt. A lower car price means a smaller loan amount, which is easier to get approved for and more manageable monthly.

-

Debt Consolidation (Pre-Car Loan):

- In some specific cases, consolidating your credit card debt into a personal loan before applying for a car loan might be beneficial. This can sometimes lower your monthly payments, reduce your DTI, and replace multiple revolving credit lines with one installment loan, which can be viewed more favorably by some lenders.

- However, this strategy has risks. You need to ensure the interest rate on the consolidation loan is lower than your credit card rates, and you must avoid racking up new credit card debt after consolidation. If not managed carefully, you could end up with more debt.

Understanding Your Options & Potential Hurdles

Even with the best preparation, navigating a car loan with credit card debt might present a few specific scenarios:

1. Higher Interest Rates Are Likely

If your credit score is on the lower end due to credit card debt, expect to be offered higher interest rates. Lenders charge more to compensate for the increased risk they perceive. This is a common hurdle, but it shouldn’t deter you. Focus on getting approved, and you can always look into refinancing later.

2. Shorter Loan Terms May Be Offered

Some lenders might offer shorter loan terms (e.g., 36 or 48 months instead of 60 or 72 months) to mitigate risk. While this means higher monthly payments, it also means you’ll pay off the car faster and accrue less interest overall. Ensure you can comfortably afford these higher payments.

3. Subprime Lenders: When to Consider, When to Be Cautious

If traditional lenders turn you down, you might be approached by subprime auto lenders. These lenders specialize in working with individuals with lower credit scores or higher debt. While they can provide a solution, their interest rates are significantly higher, and terms might be less favorable.

Pro tips from us: Always read the fine print with subprime lenders. Understand all fees, penalties, and the true cost of the loan before signing. It’s often a last resort, but can be a stepping stone if managed responsibly and refinanced when your credit improves.

Pro Tips for Managing Your Finances Post-Car Loan

Securing a car loan with credit card debt is a victory, but the journey doesn’t end there. Effective financial management is crucial to avoid deeper debt and improve your overall financial health.

-

Budgeting for the New Payment:

- Integrate your new car payment seamlessly into your monthly budget. Ensure you have enough disposable income to cover it alongside your existing credit card payments and other expenses.

- Consider using a budgeting app or spreadsheet to track your income and outflows meticulously.

-

Prioritizing Debt Repayment:

- Once your car loan is secured, continue to focus on paying down your high-interest credit card debt. The "debt snowball" or "debt avalanche" methods can be highly effective.

- The debt snowball involves paying off the smallest balance first for psychological wins, while the debt avalanche tackles the highest interest rate debt first to save the most money. Choose the method that best motivates you.

-

Avoiding New Debt:

- Resist the temptation to accumulate new credit card debt. Your goal should be to reduce your overall debt burden, not increase it.

- Based on my experience, many people get into trouble by feeling "financially free" after getting a new loan, only to revert to old spending habits.

-

Refinancing the Car Loan Later:

- As you consistently make on-time payments on your car loan and reduce your credit card debt, your credit score will likely improve. After 6-12 months, you might be eligible to refinance your car loan at a lower interest rate, saving you money.

- This is a smart long-term strategy that many successful borrowers employ.

Common Mistakes to Avoid When Seeking a Car Loan With Credit Card Debt

To ensure a smoother process and better outcomes, steer clear of these common pitfalls:

- Applying Everywhere at Once: While shopping around is good, indiscriminately applying to dozens of lenders within a short period can negatively impact your credit score with too many hard inquiries. Use pre-qualification tools where available, as they often use a soft inquiry that doesn’t affect your score.

- Ignoring Your Credit Report: As mentioned, not checking for errors or understanding your credit history is a major oversight. Your credit report is your financial resume.

- Taking on More Debt Than You Can Afford: It’s easy to get excited about a new car, but overextending yourself financially will lead to stress and potential default. Always prioritize affordability over desire.

- Not Understanding Loan Terms: Don’t just look at the monthly payment. Understand the interest rate (APR), the loan term, any prepayment penalties, and late fees. Pro tips from us: Ask questions until you fully understand every aspect of the loan agreement.

Conclusion: Your Path to a Car Loan is Within Reach

Securing a car loan with credit card debt demands diligence, planning, and a commitment to financial improvement. It’s a journey that many have successfully completed, and with the right strategies, you can too. Focus on improving your credit score, lowering your DTI, making a solid down payment, and shopping wisely for lenders.

Remember, your financial situation is dynamic. By taking proactive steps today, you’re not just getting a car; you’re building a stronger financial future. Start planning, take control of your debt, and soon you’ll be driving towards your goals with confidence.

For a deeper dive into improving your credit score, check out our article on .

If you’re struggling with your current credit card debt, our guide to might offer valuable insights.

To understand more about how your credit score is calculated and its impact, a great resource is FICO’s official website: https://www.fico.com/credit-education (External Link).