Navigating the Road Ahead: Your Comprehensive Guide to Multiple Car Loans

Navigating the Road Ahead: Your Comprehensive Guide to Multiple Car Loans Carloan.Guidemechanic.com

The open road often calls for more than one set of wheels. Perhaps your growing family needs a spacious SUV alongside your daily commuter, or your new business venture requires a reliable work truck in addition to your personal vehicle. The idea of juggling multiple car loans might seem daunting, even impossible, to some. Yet, for many, it’s a practical solution to diverse transportation needs.

As an expert blogger and professional SEO content writer with years of experience dissecting the complexities of automotive finance, I’m here to tell you that obtaining and managing multiple car loans is indeed possible. However, it requires a strategic approach, a solid understanding of financial principles, and a meticulous eye for detail. This ultimate guide will demystify the process, offer invaluable insights, and equip you with the knowledge to make informed decisions, ensuring your financial journey remains smooth and sustainable.

Navigating the Road Ahead: Your Comprehensive Guide to Multiple Car Loans

What Exactly Are Multiple Car Loans?

Simply put, multiple car loans refer to a scenario where an individual or entity has two or more active financing agreements for separate vehicles running concurrently. This isn’t about refinancing one loan; it’s about taking on new debt for additional cars while existing car loans are still being paid off.

This situation can arise for various reasons, from expanding personal utility to supporting business operations. It’s a financial decision that significantly impacts your monthly budget and overall debt profile, making careful consideration absolutely crucial. Understanding the implications is the first step toward successful management.

Is Getting Approved for Multiple Car Loans Possible? The Short Answer is "Yes, But…"

The possibility of securing multiple car loans is not a myth. Many people successfully manage two, or even more, vehicle financing agreements simultaneously. However, it’s far from a straightforward process for everyone. Lenders assess your financial health with an even more critical eye when you apply for a second or third car loan.

Their primary concern is your ability to comfortably repay all your debts without undue strain. This means demonstrating exceptional financial stability, a strong payment history, and a clear capacity to take on additional financial obligations. It’s a testament to your creditworthiness and responsible financial behavior.

The "Why" Behind the Wheel: Common Reasons for Multiple Car Loans

People consider multiple car loans for a variety of legitimate and often essential reasons. It’s rarely a frivolous decision but rather a calculated move to meet specific needs.

One of the most common scenarios involves practical necessity. A family might need a larger vehicle for school runs and family trips, while a smaller, fuel-efficient car serves as a commuter for work. Another frequent reason is business expansion. A small business owner might finance a delivery van or a specialized work truck in addition to their personal car, directly contributing to their livelihood and growth.

Furthermore, hobby or passion projects can also lead to multiple loans. An enthusiast might finance a classic car or a performance vehicle for weekend drives, separate from their daily driver. In some cases, it could even be an investment opportunity, such as purchasing vehicles for a ride-sharing service or a small rental fleet. Each of these scenarios presents a compelling reason, but also a unique set of financial considerations.

The Lender’s Lens: Key Factors for Approval

When you apply for an additional car loan, lenders don’t just look at the new application in isolation. They evaluate your entire financial picture, scrutinizing several critical factors to gauge your risk profile. Understanding these elements is paramount to increasing your chances of approval.

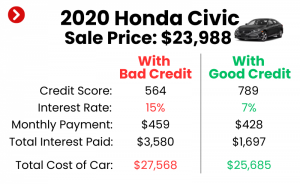

Firstly, your credit score is the cornerstone of any lending decision. For multiple car loans, an excellent credit score (typically 700+) is often a prerequisite. A high score signals to lenders that you are a reliable borrower with a history of responsible debt management. Any significant dips or negative marks could severely hinder your application.

Secondly, and arguably most important, is your Debt-to-Income (DTI) ratio. This metric compares your total monthly debt payments to your gross monthly income. Lenders use it to assess how much of your income is already allocated to debt. A high DTI ratio suggests you might be overextended, making it difficult to take on additional payments. Generally, a DTI of 36% or lower is preferred, though some lenders might go higher for well-qualified applicants. Pro tips from us: Before applying, calculate your DTI meticulously. If it’s on the higher side, consider reducing other debts first.

Thirdly, income stability and level play a crucial role. Lenders want to see a consistent, verifiable income stream that is more than sufficient to cover all your existing debts plus the new car loan payments. Self-employed individuals might need to provide more extensive documentation, such as tax returns, to prove income consistency.

Your payment history on existing loans and credit cards is also heavily weighted. A spotless record of on-time payments demonstrates reliability. Conversely, any late payments, defaults, or collections will raise red flags and significantly diminish your chances of approval.

Finally, the loan-to-value (LTV) ratio for each vehicle and the down payment you’re willing to make are considered. A substantial down payment reduces the lender’s risk and can sometimes offset other concerns. It shows your commitment and reduces the amount you need to finance.

The Ups and Downs: Pros and Cons of Multiple Car Loans

Like any significant financial decision, taking on multiple car loans comes with a set of advantages and disadvantages that warrant careful consideration. Weighing these points is essential for making a choice that aligns with your financial goals and capabilities.

On the positive side, the primary benefit is flexibility and utility. You gain the ability to meet diverse transportation needs without compromise. This could mean having a reliable vehicle for work and a separate one for family, or a practical daily driver alongside a specialized vehicle for a hobby or business. This flexibility can significantly enhance convenience and productivity in your daily life. For businesses, it can mean expanding operations and increasing revenue potential.

However, the downsides are substantial and demand careful attention. The most obvious is the increased financial burden. You’ll have multiple monthly payments, potentially higher insurance costs, and more maintenance expenses. This significantly reduces your disposable income and can strain your budget. Common mistakes to avoid are underestimating these cumulative costs.

Another significant risk is the impact on your credit score. While managing multiple loans responsibly can positively affect your credit mix and payment history, any missed payments or defaults will severely damage your score. Furthermore, having a higher overall debt load can make it harder to qualify for other loans in the future, such as a mortgage, as your DTI ratio will be elevated. Your financial flexibility will naturally be reduced, as a larger portion of your income is committed to debt.

Strategies for Successfully Managing Multiple Car Loans

Once you’ve secured multiple car loans, the journey isn’t over; it’s just beginning. Effective management is key to avoiding financial distress and maintaining a healthy credit profile. Based on my experience working with countless individuals, proactive management is the differentiator between success and struggle.

Budgeting becomes your best friend. A meticulous, detailed budget that accounts for every single expense, including all loan payments, insurance, fuel, and maintenance for each vehicle, is non-negotiable. Track your income and outflow rigorously to ensure you always have enough funds.

Building and maintaining a robust emergency fund is absolutely essential. Life happens, and unexpected expenses or income disruptions can quickly derail your ability to make multiple payments. Aim for at least 3-6 months of living expenses saved up as a buffer.

Consider automating your payments. Setting up automatic transfers from your bank account to your loan providers ensures that payments are never missed. This not only saves you from late fees but also protects your credit score.

Regularly review your financial situation. At least once a quarter, sit down and assess your income, expenses, DTI, and credit score. Are you still comfortable with your debt load? Are there opportunities to pay down principal faster? This ongoing vigilance helps you adapt to changing circumstances.

Finally, explore options like refinancing if interest rates drop or your credit score significantly improves. Refinancing one or more of your loans to a lower interest rate can reduce your monthly payments and free up cash flow. Similarly, if your financial situation becomes overwhelming, debt consolidation could be a future strategy, though it’s less common for multiple secured car loans unless combined with other unsecured debts.

Common Mistakes to Avoid When Considering Multiple Car Loans

The path to multiple car loans is riddled with potential pitfalls that can lead to significant financial stress. Being aware of these common mistakes can help you steer clear of them.

Underestimating the true cost is a frequent error. It’s not just about the monthly payment. Factor in increased insurance premiums for each vehicle, higher fuel costs, more frequent maintenance, and potential depreciation. These hidden costs can quickly add up and overwhelm an unprepared budget.

Ignoring your Debt-to-Income (DTI) ratio is another critical misstep. Many applicants focus solely on their credit score, forgetting that lenders heavily weigh DTI. A strong credit score won’t compensate for an already overstretched income. From years of observing financial trends, I can attest that DTI is often the silent killer of loan applications.

Applying indiscriminately to multiple lenders in a short period can backfire. Each hard inquiry on your credit report can slightly lower your score. Instead, research lenders thoroughly, pre-qualify if possible, and apply only to those where you have the highest chance of approval.

Neglecting to build an emergency fund before taking on additional debt is a recipe for disaster. Without a financial cushion, any unexpected expense—a car repair, a medical bill, or job loss—can quickly lead to missed payments and a spiraling debt problem.

Lastly, failing to read the fine print on loan agreements can lead to unpleasant surprises. Understand all terms, conditions, interest rates, fees, and penalties before signing. Don’t be afraid to ask questions until you fully grasp every detail.

Alternative Solutions to Consider Before Committing

Before you fully commit to the path of multiple car loans, it’s wise to explore alternative solutions that might better suit your needs and financial situation. Sometimes, a different approach can provide the desired outcome with less financial burden.

Leasing a second vehicle is a popular alternative. Leasing often comes with lower monthly payments compared to financing, and you avoid the long-term commitment of ownership. It’s ideal if you only need a second car for a few years or prefer always driving a newer model.

For those with occasional needs for an additional vehicle, ride-sharing services or car rental might be more cost-effective. If your second car is only used on weekends or for specific trips, the cost of ownership (payments, insurance, maintenance) might far outweigh the cost of renting when needed.

Another option is to consider if one versatile vehicle could serve multiple purposes. Perhaps a larger SUV or a truck with good passenger capacity could replace the need for two separate cars. This simplifies finances significantly.

Finally, think about the type of vehicle for your secondary need. Instead of financing another brand-new car, opting for a reliable used car with a lower price tag can drastically reduce your loan amount and monthly payments. This is a common strategy to minimize financial exposure.

Pro Tips for Getting Approved for Multiple Car Loans

Securing approval for multiple car loans demands a strategic and proactive approach. Here are some expert tips to boost your chances significantly:

First and foremost, prioritize improving your credit score. Pay down existing debts, especially credit card balances, to lower your credit utilization. Dispute any inaccuracies on your credit report. A higher score translates to better terms and higher approval odds.

Next, focus on reducing existing debt. The lower your DTI ratio, the more attractive you are to lenders. If possible, pay off a small personal loan or credit card entirely before applying for the second car loan.

Increase your verifiable income if possible. This could mean taking on a side hustle, working overtime, or providing proof of recent raises. A higher income directly improves your DTI and demonstrates greater repayment capacity.

Save for larger down payments. As mentioned earlier, a substantial down payment on the second vehicle reduces the loan amount and the lender’s risk. It shows financial prudence and commitment.

Shop around for lenders meticulously. Don’t just go to your primary bank. Credit unions often offer more flexible terms, and online lenders specialize in various niches. Compare interest rates, terms, and fees from multiple sources. Based on my experience, a difference of even half a percentage point can save you hundreds over the life of the loan.

Lastly, be transparent and prepared with documentation. Have all your financial records organized: income statements, tax returns, bank statements, and details of all existing debts. Being forthcoming with lenders builds trust and streamlines the application process.

The Impact on Your Credit Score: A Closer Look

Obtaining multiple car loans can have a multifaceted impact on your credit score, both immediate and long-term. Understanding these effects is vital for managing your financial health.

Initially, each application for a new car loan will result in a hard inquiry on your credit report. A hard inquiry can temporarily dip your credit score by a few points, typically lasting for a few months. While a single inquiry isn’t usually a major concern, multiple inquiries in a short period can signal higher risk to lenders.

Once approved, the increased debt load will be reflected on your credit report. This can raise your overall credit utilization (though usually less impactful than credit card utilization) and, more significantly, increase your DTI ratio. This higher debt burden can make it harder to qualify for other forms of credit in the future.

However, the most profound impact comes from your payment history. Consistently making on-time payments on multiple car loans demonstrates excellent financial responsibility. This positive payment history will contribute significantly to building and maintaining a strong credit score over time. Conversely, even a single missed payment on any of your loans can have a severe and lasting negative impact.

Finally, having a diverse credit mix can be beneficial. Managing different types of credit (e.g., credit cards, mortgage, multiple auto loans) can show lenders that you are capable of handling various financial obligations responsibly. This aspect can positively influence your credit score, provided all accounts are managed perfectly. For more insights into managing your credit, check out our guide on .

Conclusion: Driving Towards a Thoughtful Decision

Navigating the landscape of multiple car loans is a journey that requires careful planning, a deep understanding of financial principles, and unwavering discipline. While it offers undeniable benefits in terms of flexibility and meeting diverse needs, it also comes with significant responsibilities and potential risks.

As an expert in this field, I cannot stress enough the importance of thorough self-assessment. Evaluate your financial health, consider your true needs versus wants, and meticulously plan for every eventuality. Do your homework on lenders, understand the fine print, and always prioritize building a robust emergency fund. To better understand your debt-to-income ratio, a key metric for lenders, you can find more information from the Consumer Financial Protection Bureau.

Ultimately, the decision to pursue multiple car loans should be a well-informed one, based on a clear understanding of your capacity to manage the increased financial burden. With the right strategy and responsible financial habits, you can successfully navigate this path and achieve your transportation goals without compromising your financial well-being. Drive safe, and drive smart!