Navigating the Road Ahead: Your Comprehensive Guide to Personal Car Loans for Poor Credit

Navigating the Road Ahead: Your Comprehensive Guide to Personal Car Loans for Poor Credit Carloan.Guidemechanic.com

Securing a car loan can feel like an uphill battle when your credit score isn’t ideal. Many people find themselves in this challenging situation, where a low credit score seems to shut the door on essential purchases, including a reliable vehicle. But here’s the crucial truth: having poor credit doesn’t automatically disqualify you from getting a personal car loan. It simply means you need a different strategy, more preparation, and a deeper understanding of the process.

As an expert blogger and professional in the financial space, I’ve seen countless individuals navigate this very path successfully. My goal with this comprehensive guide is to empower you with the knowledge, strategies, and confidence needed to secure a personal car loan, even with poor credit. We’ll explore every facet, from understanding your credit to finding the right lender and managing your loan effectively, ensuring you drive away with a car and a plan for a brighter financial future.

Navigating the Road Ahead: Your Comprehensive Guide to Personal Car Loans for Poor Credit

Understanding Poor Credit and the Car Loan Landscape

Before diving into solutions, it’s vital to grasp what "poor credit" means in the eyes of lenders and why it impacts car loan applications. Your credit score is essentially a numerical representation of your creditworthiness – how likely you are to repay borrowed money. Scores typically range from 300 to 850, with anything generally below 600-620 often considered "poor" or "subprime."

Why Lenders Hesitate (and How to Address It)

Lenders assess risk. A low credit score signals to them a higher potential for default, meaning you might not pay back the loan as agreed. This perceived risk is why you’ll often face higher interest rates or stricter terms compared to someone with excellent credit. However, it’s not an outright rejection; it’s an invitation for you to demonstrate your reliability in other ways.

Based on my experience, many people mistakenly believe their low score is a permanent roadblock. This isn’t true. Lenders specializing in subprime loans understand that life happens, and they are designed to work with borrowers who have past credit challenges. The key is to present a strong overall financial picture, even if one aspect – your credit score – is currently weak.

The Indispensable Role of a Car in Daily Life

For many, a car isn’t a luxury; it’s a necessity. It’s the bridge to your job, your children’s school, medical appointments, and essential errands. Without reliable transportation, maintaining employment and a stable household becomes significantly harder. This understanding fuels our mission: to help you secure the financing you need to keep your life moving forward.

Preparing for Your Car Loan Journey: Laying the Groundwork

Success in securing a personal car loan with poor credit heavily relies on preparation. Think of it as building a robust case for yourself. The more prepared you are, the more confidence you’ll project to lenders, and the better terms you’re likely to receive.

1. Check Your Credit Score and Report: Know Thyself

This is the absolute first step. You cannot begin to address a problem if you don’t fully understand its scope. Obtain your credit report from all three major credit bureaus: Equifax, Experian, and TransUnion. You are entitled to a free report from each once every 12 months via AnnualCreditReport.com.

Pro tips from us: Carefully review each report for inaccuracies. Errors are more common than you might think, and disputing them can potentially boost your score. Even a few points can make a difference in loan terms. Understanding what’s on your report also helps you explain any past issues to a potential lender.

2. Determine Your Realistic Budget: Beyond the Monthly Payment

It’s easy to focus solely on the monthly car payment, but a truly responsible budget considers the total cost of ownership. This includes not just the loan principal and interest, but also car insurance, fuel, maintenance, registration fees, and potential repair costs. For someone with poor credit, insurance premiums can be higher, so factor that in.

Create a detailed personal budget that outlines your income and all your expenses. This will show you exactly how much you can comfortably afford each month for a car, preventing you from overextending yourself. Lenders will also appreciate this level of financial foresight.

3. Save for a Down Payment: Your Best Ally

A substantial down payment is one of the most powerful tools you have when seeking a car loan with poor credit. It reduces the amount you need to borrow, which in turn lowers the lender’s risk. A larger down payment also often translates to a lower monthly payment and less interest paid over the life of the loan.

Based on my experience, even 10-20% of the car’s value can significantly improve your chances of approval and lead to better terms. It demonstrates your commitment and financial stability to the lender, signaling that you have skin in the game.

4. Gather Necessary Documents: Be Ready to Impress

Lenders will require various documents to verify your identity, income, and residence. Having these readily available will streamline the application process and show your seriousness. Typically, you’ll need:

- Government-issued ID (driver’s license)

- Proof of residence (utility bill, lease agreement)

- Proof of income (pay stubs, tax returns, bank statements)

- Social Security Number

- References (sometimes required by subprime lenders)

Having everything organized shows responsibility and can speed up your loan approval.

Finding the Right Lender for Personal Car Loans with Poor Credit

Not all lenders are created equal, especially when it comes to borrowers with less-than-perfect credit. It’s crucial to target lenders who specialize in or are open to working with individuals in your situation.

1. Specialized "Bad Credit" Lenders and Dealerships

Many dealerships have financing departments that work with a network of lenders, some of whom specialize in subprime auto loans. These "special finance" departments are designed to help people with credit challenges. Some dealerships also offer "in-house financing," meaning they lend you the money directly.

While convenient, "buy here, pay here" dealerships (a form of in-house financing) often come with higher interest rates and less consumer protection. Pro tips from us: always compare their offers with other lenders before committing. Ensure the car’s price is fair and the terms are transparent.

2. Credit Unions: A Community-Focused Alternative

Credit unions are member-owned financial institutions known for their more personalized approach and often more flexible lending criteria than traditional banks. They may be more willing to look beyond just your credit score and consider your overall financial history, relationship with the credit union, and ability to repay.

If you’re a member of a credit union, or eligible to join one, it’s always worth checking their auto loan options. They might offer more favorable terms, even with poor credit.

3. Online Loan Marketplaces: Comparison Shopping Made Easy

Several online platforms specialize in connecting borrowers with poor credit to a network of lenders. These marketplaces allow you to pre-qualify with multiple lenders using a single application, often with only a "soft inquiry" that doesn’t harm your credit score. This allows you to compare offers without commitment.

This method is excellent for understanding what rates and terms you might qualify for before you even step into a dealership. It empowers you with information, strengthening your negotiating position.

4. Exploring Co-Signers: A Shared Responsibility

If you have a trusted individual with good credit who is willing to co-sign your loan, it can significantly increase your chances of approval and potentially secure a lower interest rate. A co-signer legally agrees to take responsibility for the loan if you fail to make payments.

Common mistakes to avoid are not fully understanding the co-signer’s responsibility. It’s a serious commitment for them, as it impacts their credit if you default. Ensure open communication and a clear understanding of your repayment plan.

Strategies to Improve Your Chances of Approval

Even with poor credit, there are several proactive steps you can take to make your application more attractive to lenders. These go beyond simply finding the right lender; they involve presenting yourself as a reliable borrower.

1. Leverage a Strong Down Payment

As mentioned, a substantial down payment reduces the loan amount and the lender’s risk. It also signals your commitment. If you can save more, do so. Every extra dollar you put down lessens the burden on the loan.

2. Demonstrate Stable Income and Employment History

Lenders want to see that you have a consistent and sufficient income to cover your monthly payments. A steady job history (ideally 1-2 years or more with the same employer) provides reassurance. If you’ve recently changed jobs, be prepared to explain the circumstances.

Provide clear, verifiable proof of income. This might include recent pay stubs, W-2 forms, or tax returns if you’re self-employed.

3. Show Financial Responsibility in Other Areas

While your credit score might be low, you can still highlight positive financial behaviors. Are you consistently paying other bills on time, such as rent, utilities, or phone bills? While these might not always appear on your credit report, you can use them as proof of responsible payment history.

Gather statements or payment confirmations to present to the lender. This can paint a more complete picture of your financial habits beyond just your credit score.

4. Choose an Affordable Car: Be Realistic

It’s tempting to eye that dream car, but with poor credit, realism is your friend. Opt for a reliable, more affordable vehicle that fits comfortably within your budget. A lower loan amount means less risk for the lender and a higher chance of approval for you.

Focus on getting a car that meets your needs, not your wants, at this stage. You can always upgrade once your credit improves.

The Application Process: Navigating the Steps

Once you’ve done your homework and chosen potential lenders, it’s time to apply. Understanding the process will help alleviate anxiety and ensure you’re making informed decisions.

Pre-Qualification vs. Full Application

Many lenders offer a "pre-qualification" option. This is a preliminary assessment based on basic information, and it typically involves a "soft credit inquiry" that doesn’t affect your credit score. Pre-qualification gives you an idea of what loan amount and interest rate you might qualify for.

A full application, however, requires more detailed information and results in a "hard credit inquiry," which can temporarily lower your credit score by a few points. It’s wise to pre-qualify with a few lenders first, then proceed with a full application only for the most promising offers within a short window (usually 14-45 days, depending on the scoring model) to minimize the impact on your credit score.

What to Expect During the Application

Be prepared to answer questions about your employment history, income, existing debts, and housing situation. The lender will review all your submitted documents and assess your overall financial health. They might ask for explanations regarding past credit issues, so be honest and concise.

Based on my experience, transparency is key. Trying to hide or obscure information will only raise red flags. Be upfront about your credit challenges and explain any mitigating circumstances.

Negotiating Your Loan Terms

Even with poor credit, there might be some room for negotiation, especially if you have multiple pre-approvals. Don’t be afraid to ask if the interest rate can be lowered, or if there are any fees that can be waived. Remember, the worst they can say is no.

Focus on the total cost of the loan, not just the monthly payment. A longer loan term might reduce your monthly payment but significantly increase the total interest paid over time.

Understanding Your Loan Terms: The Fine Print Matters

Once approved, carefully review every aspect of your loan agreement before signing. This is where many common mistakes are made, leading to unforeseen financial burdens.

1. Interest Rates: Expect Higher, but Understand Them

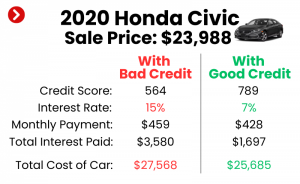

For borrowers with poor credit, interest rates will undoubtedly be higher than for those with excellent credit. This is the lender’s way of compensating for the increased risk. Understand if your rate is fixed (stays the same) or variable (can change).

Calculate the total interest you’ll pay over the life of the loan. A higher interest rate on a long loan term can mean paying significantly more than the car’s actual value.

2. Loan Term (Length): The Double-Edged Sword

The loan term dictates how long you have to repay the loan. Longer terms (e.g., 72 or 84 months) mean lower monthly payments, which can be appealing when budgeting. However, they also mean you pay more interest over time and risk owing more than the car is worth (being "upside down" on your loan) as it depreciates.

Pro tips from us: Aim for the shortest loan term you can comfortably afford. This minimizes interest paid and helps you build equity in your vehicle faster.

3. Total Cost of the Loan: Look Beyond Monthly Payments

Add up the principal loan amount, the total interest, and any associated fees. This figure represents the true cost of your car. Comparing this total cost across different offers is crucial for making an informed decision.

4. Fees and Charges: Read the Fine Print

Be vigilant about any additional fees, such as origination fees, application fees, or prepayment penalties. Some lenders charge extra for administrative costs. Ensure every fee is clearly explained and justified. If a fee seems suspicious, ask for clarification or consider other lenders.

Pro Tips for Managing Your Car Loan and Rebuilding Credit

Getting the loan is just the first step. Successfully managing it is your pathway to rebuilding your credit and achieving greater financial freedom.

1. Make Payments On Time, Every Time

This is the single most important action you can take. Payment history accounts for 35% of your credit score. Every on-time payment reported to the credit bureaus strengthens your credit profile. Set up automatic payments to avoid missing due dates.

Consistent, timely payments on your car loan will demonstrate your reliability and positively impact your credit score over time.

2. Avoid Missed Payments at All Costs

A single missed payment can significantly damage your credit score and trigger late fees. If you anticipate difficulty making a payment, contact your lender immediately. They may be willing to work with you on a temporary solution. Ignoring the problem will only make it worse.

3. Consider Refinancing When Your Credit Improves

Once you’ve made 6-12 months of on-time payments and your credit score has improved, consider refinancing your car loan. Refinancing allows you to replace your existing loan with a new one, potentially with a lower interest rate and more favorable terms. This can save you a substantial amount of money over the life of the loan.

This is a common strategy employed by savvy borrowers who used a bad credit car loan as a stepping stone to better financial standing.

4. Monitor Your Credit Score Regularly

Keep track of your credit score’s progress. Seeing it improve with each on-time payment can be incredibly motivating. Use free credit monitoring services provided by credit card companies or financial apps.

5. Maintain Overall Financial Discipline

Your car loan is one piece of your financial puzzle. Continue to pay all other bills on time, keep credit card balances low, and avoid taking on unnecessary new debt. This holistic approach to financial health will reinforce your positive credit journey.

Common Mistakes to Avoid When Seeking a Car Loan with Poor Credit

Navigating the world of car loans with poor credit can be tricky, and pitfalls are common. Being aware of these missteps can save you significant time, money, and stress.

1. Applying Everywhere (Multiple Hard Inquiries)

Each time a lender pulls your credit for a loan application, it results in a "hard inquiry." Too many hard inquiries in a short period can negatively impact your credit score. Stick to pre-qualifying with a few lenders and only submit full applications to those with the most promising offers.

2. Settling for the First Offer You Receive

Don’t jump at the first approval you get, especially if it’s the only one you’ve explored. Always compare offers from at least two or three different lenders. As discussed, online marketplaces can be invaluable for this.

3. Ignoring the Total Cost of the Loan

As mentioned earlier, focusing solely on the monthly payment can lead to a much higher overall cost. Always calculate the total amount you’ll pay over the loan’s lifetime, including all interest and fees.

4. Buying More Car Than You Can Afford

It’s easy to get caught up in the excitement of a new car. However, purchasing a vehicle that stretches your budget too thin is a recipe for financial stress and potential default. Stick to your pre-determined affordable budget.

5. Not Reading the Fine Print (All of It)

Loan agreements are legally binding documents. Before you sign anything, read every single clause, no matter how small. Understand the interest rate, term, fees, penalties for late payments, and any other conditions. If something is unclear, ask for clarification. Don’t be rushed.

Conclusion: Driving Towards a Brighter Financial Future

Securing a personal car loan with poor credit is undeniably a challenge, but it is far from impossible. By understanding your credit situation, diligently preparing, seeking out the right lenders, and committing to responsible loan management, you can successfully navigate this journey. This isn’t just about getting a car; it’s about taking a significant step towards rebuilding your financial health and proving your creditworthiness.

Remember, this loan can be a powerful tool for credit rehabilitation. Every on-time payment helps mend your credit score, opening doors to better financial opportunities in the future. Embrace this opportunity, stay disciplined, and you’ll soon find yourself on a smoother, more financially secure road.

Your journey to a reliable vehicle and improved credit starts now. Take these steps, empower yourself with knowledge, and drive confidently into your future.

External Resource: For more information on understanding and improving your credit score, you can visit the Consumer Financial Protection Bureau (CFPB) website: https://www.consumerfinance.gov/consumer-tools/credit-reports-and-scores/