Navigating the Road Ahead: Your Comprehensive Guide to the 60 Months Car Loan

Navigating the Road Ahead: Your Comprehensive Guide to the 60 Months Car Loan Carloan.Guidemechanic.com

Buying a car is a significant milestone for many, a blend of excitement and financial consideration. For most, financing is a necessity, and among the myriad options available, the 60 months car loan stands out as a popular choice. This five-year repayment plan offers a unique balance between manageable monthly payments and a reasonable repayment period.

However, choosing a 60-month auto loan isn’t merely about securing the lowest monthly payment. It’s a strategic financial decision with long-term implications for your budget, your credit, and your overall financial health. As an expert in car financing, my goal here is to provide you with an incredibly detailed, unique, and actionable guide. We’ll delve deep into every facet of the 60-month car loan, equipping you with the knowledge to make an informed choice that truly benefits you.

Navigating the Road Ahead: Your Comprehensive Guide to the 60 Months Car Loan

What Exactly is a 60-Month Car Loan? Unpacking the Five-Year Commitment

A 60 months car loan is, at its core, an installment loan designed to help you finance the purchase of a vehicle over a period of five years. This means you commit to making 60 equal monthly payments until the principal amount borrowed, plus accrued interest, is fully repaid. It’s one of the most common loan terms available for both new and used vehicles.

Compared to shorter terms, like 36 or 48 months, a 60-month loan stretches out your repayment period. This extension directly impacts your monthly financial obligation. While the total cost of the car remains the same, spreading payments over a longer duration typically results in lower individual monthly installments. This makes more expensive vehicles seem more accessible within a fixed budget.

However, this extended period isn’t without its trade-offs. The total interest paid over the life of the loan generally increases with longer terms. This is a crucial point that many borrowers overlook when focusing solely on the monthly payment figure. Understanding this fundamental dynamic is the first step towards mastering your car financing journey.

The Allure of a 60-Month Car Loan: Why Borrowers Choose It

The popularity of the 60 months car loan isn’t accidental. It offers several compelling advantages that align with the financial realities of many car buyers. Based on my experience in the auto finance industry, these are the primary drivers behind its widespread adoption.

1. Lower Monthly Payments:

This is arguably the most significant draw. By extending the repayment period to five years, lenders can offer significantly lower monthly payments compared to shorter terms. For many households, this translates into immediate budgetary relief. It allows them to fit a new car payment comfortably into their existing expenses without feeling overly strained.

2. Access to More Expensive Vehicles:

Lower monthly payments can open doors to vehicles that might otherwise be out of reach. A buyer with a fixed budget for car payments might find that a 60-month loan allows them to afford a higher trim level, a newer model, or a vehicle with more desired features. This can significantly enhance the car buying experience and lead to greater satisfaction with the purchase.

3. Enhanced Financial Flexibility:

The reduced monthly financial burden often provides a buffer in a household budget. This flexibility can be crucial for covering unexpected expenses, contributing to savings, or allocating funds to other financial goals. It prevents the car payment from becoming an overwhelming obligation, allowing for a more balanced financial life.

4. Predictability in Budgeting:

A fixed 60-month auto loan provides a clear, predictable monthly expense. This stability is invaluable for financial planning, allowing individuals and families to budget accurately for the next five years. Knowing exactly what your car payment will be each month eliminates uncertainty and simplifies overall financial management.

Understanding the Financial Implications: Beyond the Monthly Payment

While the allure of lower monthly payments is strong, a truly informed decision about a 60 months car loan requires a deeper dive into its financial implications. Pro tips from us emphasize looking at the bigger picture.

1. The Role of Interest Rates:

Interest is the cost of borrowing money, and it’s a critical component of any loan. With a 60-month term, you’re paying interest for a longer duration. Even if the interest rate itself is competitive, the cumulative effect over five years can be substantial. Factors like your credit score, the lender you choose, and current market conditions all influence the interest rate you’ll receive. A higher rate on a longer term can add thousands to the total cost.

2. Total Cost of Ownership:

Many focus solely on the monthly payment or the sticker price. However, the true cost of a car includes not just the purchase price and interest, but also insurance, maintenance, fuel, and potential repairs. A longer loan term means you’ll own the car for a greater portion of its lifespan, potentially incurring more maintenance costs after the manufacturer’s warranty expires. When you opt for a 60-month auto loan, you need to budget for these ongoing expenses.

3. The Impact of Depreciation and Negative Equity:

Cars begin to depreciate the moment they leave the dealership lot. Over five years, a vehicle can lose a significant portion of its value. With a longer loan term, there’s a higher risk of entering a state of "negative equity," especially in the early years. Negative equity occurs when you owe more on your car loan than the car is actually worth. This can become problematic if you need to sell or trade in the vehicle before the loan is paid off, as you’ll still be responsible for the difference. This is a common mistake to avoid: not considering the car’s depreciating value against the loan balance.

4. Insurance Requirements:

Lenders typically require full comprehensive and collision insurance coverage for the duration of your car loan. While this is good practice for any new car owner, the longer term of a 60-month loan means you’ll be paying for this potentially more expensive coverage for an extended period. This needs to be factored into your overall budget.

Key Factors Influencing Your 60-Month Car Loan Approval & Terms

Securing a favorable 60 months car loan isn’t just about finding a car; it’s about proving your creditworthiness to lenders. Several crucial factors come into play, each impacting your chances of approval and the interest rate you’ll be offered. Based on my experience, understanding these elements can significantly improve your position.

1. Your Credit Score: The Paramount Factor:

Your credit score is the single most important determinant. Lenders use it to assess your reliability in repaying debts.

- Excellent Credit (750+): You’ll typically qualify for the lowest interest rates and most favorable terms.

- Good Credit (700-749): Still very strong, offering competitive rates.

- Fair Credit (650-699): You might face slightly higher interest rates, but approval is still likely.

- Poor Credit (below 650): Approval for a 60-month auto loan can be challenging, often coming with significantly higher interest rates or requiring a larger down payment or a co-signer.

2. Your Down Payment: Reducing Risk, Saving Money:

A substantial down payment signals financial stability to lenders and reduces their risk. It also directly lowers the amount you need to borrow, which means lower monthly payments and less interest paid over the life of the loan. Pro tips from us: Aim for at least 10-20% of the car’s purchase price if possible. This also helps mitigate the risk of negative equity.

3. Debt-to-Income Ratio (DTI): Are You Overextended?

Lenders look at your DTI to determine if you can comfortably afford another monthly payment. This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI (ideally below 36%) indicates you have sufficient income to manage your existing debts plus the new car loan. A high DTI can be a red flag for lenders.

4. Loan-to-Value Ratio (LTV): Borrowing Wisely:

The LTV ratio compares the amount you’re borrowing to the car’s actual market value. Lenders prefer an LTV of 100% or less, meaning you’re not borrowing more than the car is worth. A large down payment helps achieve a favorable LTV. Borrowing more than the car’s value (e.g., rolling in taxes, fees, or negative equity from a trade-in) increases risk for the lender and can lead to higher rates.

5. Vehicle Age and Mileage (Especially for Used Cars):

For used cars, the age and mileage of the vehicle play a role. Older cars with high mileage are seen as higher risk because they are more prone to mechanical issues. Some lenders have limits on the age or mileage of vehicles they will finance for a 60 months car loan term.

6. Income Stability and Employment History:

Lenders want assurance that you have a steady and reliable source of income to make your payments. They will typically ask for proof of employment, such as pay stubs, W-2s, or tax returns. A consistent work history demonstrates stability.

Pros and Cons of a 60-Month Car Loan: A Balanced View

To truly make an informed decision, it’s essential to weigh the advantages against the disadvantages of a 60 months car loan. This balanced perspective will help you determine if this particular auto loan structure aligns with your financial goals and lifestyle.

The Pros:

- Affordable Monthly Payments: This is the primary benefit, making car ownership more accessible and freeing up cash flow for other expenses or savings.

- Access to Better Vehicles: With lower monthly payments, you might be able to afford a car that better suits your needs or desires, perhaps with more features or a higher safety rating.

- Fixed Budgeting: Knowing your exact payment for five years allows for predictable financial planning and simplifies monthly budgeting.

- Building Credit History: Consistently making on-time payments on a 60-month auto loan can significantly improve your credit score over time, opening doors to better financial products in the future.

The Cons:

- Higher Total Interest Paid: The longer the loan term, the more interest accrues over time. You will almost certainly pay more overall for the same car compared to a 36- or 48-month loan.

- Increased Risk of Negative Equity: As discussed, depreciation outpaces loan repayment in the early years. This can leave you "upside down" on your loan, owing more than the car is worth.

- Longer Period of Debt: You’ll be making car payments for five years. This can feel like a long commitment, especially if your financial situation changes or you wish to upgrade your vehicle sooner.

- Potential for Out-of-Warranty Repairs: By the time a 60-month loan is paid off, especially for a new car, the vehicle may be approaching or beyond its manufacturer’s warranty period. This means any major repairs will come directly out of your pocket while you are still making payments.

Navigating the Application Process: A Step-by-Step Guide

Securing a 60 months car loan involves more than just walking into a dealership. A strategic approach can save you money and stress. Based on my experience, following these steps will empower you during the process.

1. Preparation is Key: Know Your Financial Standing:

Before you even look at cars, check your credit score and history. This will give you a realistic idea of the interest rates you can expect. Gather necessary documents like proof of income (pay stubs, W-2s), proof of residence, and identification. Understanding your budget – not just for the monthly payment, but for total ownership costs – is paramount.

2. Get Pre-Approved: Your Negotiating Power:

One of the most valuable pro tips from us is to get pre-approved for a loan before you visit a dealership. Contact your bank, credit union, or reputable online lenders. Pre-approval gives you:

- A clear understanding of the interest rate you qualify for.

- A maximum loan amount, setting your budget.

- Leverage at the dealership, as you already have financing secured. You can then compare their offer to your pre-approval.

3. Shop Around for Lenders:

Don’t settle for the first offer. Banks, credit unions, online lenders, and dealership financing all have different rates and terms. Compare at least three to five offers to ensure you’re getting the most competitive interest rate for your 60 months car loan. Credit unions often offer very competitive rates.

4. Negotiate the Car Price Separately:

Keep the car price negotiation distinct from the financing. First, agree on the lowest possible price for the vehicle. Only after you’ve settled on the price should you discuss financing options. Common mistakes to avoid include letting the dealer combine these two, making it harder to see where you might be getting a less favorable deal.

5. Read the Fine Print, Every Word:

Before signing any documents, thoroughly review the loan agreement. Pay close attention to:

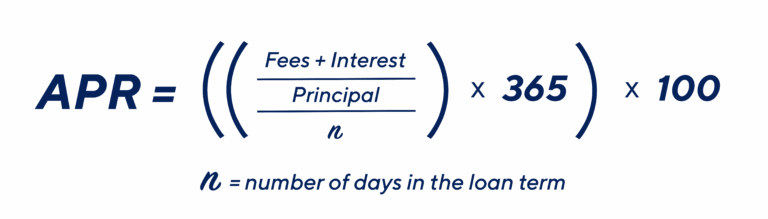

- Annual Percentage Rate (APR): This includes the interest rate plus any fees, giving you the true cost of borrowing.

- Total amount financed: Ensure it matches your agreed-upon price.

- Any additional fees or charges: Understand what each fee is for.

- Prepayment penalties: Confirm if there are any charges for paying off your loan early. Most car loans don’t have these, but it’s crucial to verify.

Pro Tips for Securing the Best 60-Month Car Loan

Based on my extensive experience in auto financing, these strategies will give you a significant advantage when seeking a 60 months car loan.

- Boost Your Credit Score: If you have time before buying, focus on improving your credit score. Pay down existing debts, make all payments on time, and avoid opening new lines of credit. Even a 20-point increase can lead to a lower interest rate.

- Save a Substantial Down Payment: The more you put down, the less you borrow, which means lower monthly payments and less interest paid overall. Aim for 10-20% if possible.

- Shop Around Aggressively for Rates: Don’t just accept the first offer. Get pre-approved with multiple lenders (banks, credit unions, online platforms) within a short window (typically 14-45 days) so it counts as a single inquiry on your credit report. This allows you to compare and leverage the best rate.

- Consider a Co-Signer (with caution): If your credit isn’t ideal, a co-signer with excellent credit can help you qualify for a better rate. However, remember that the co-signer is equally responsible for the debt, so choose wisely and ensure they understand the commitment.

- Negotiate the Car Price First, Then the Financing: As mentioned, separate these two processes. Get the best deal on the car itself before discussing your 60 months car loan options.

- Don’t Just Focus on the Monthly Payment: Always look at the total cost of the loan, including all interest and fees. A lower monthly payment can sometimes mask a much higher overall cost.

- Be Wary of Add-Ons: Dealerships often offer extended warranties, GAP insurance, or other add-ons. While some may be valuable, research them thoroughly. Do not feel pressured to accept them as part of your loan agreement, especially if you can get them cheaper elsewhere.

- Keep Refinancing in Mind: Your current interest rate isn’t necessarily permanent. If your credit score improves or market rates drop after you’ve taken out your 60 months car loan, you might be able to refinance to a lower rate, saving you money over the remaining term.

Common Mistakes to Avoid When Taking a 60-Month Car Loan

Even with the best intentions, borrowers often fall into common traps. Recognizing these pitfalls can save you from costly errors. Based on my observations, these are common mistakes to avoid:

- Focusing Solely on the Monthly Payment: This is the most prevalent mistake. While important for budgeting, fixating only on the monthly figure can lead you to accept a longer term with a higher interest rate, ultimately paying much more over the life of the loan. Always ask for the total loan cost.

- Skipping the Pre-Approval Step: Not getting pre-approved leaves you vulnerable at the dealership. You lose negotiating power and might accept a higher interest rate than you qualify for.

- Not Budgeting for Total Ownership Costs: Beyond the loan payment, remember to factor in insurance, fuel, maintenance, and potential repairs. A beautiful car that breaks your budget for everyday running costs quickly loses its appeal.

- Rolling Negative Equity into a New Loan: If you’re trading in a car that you still owe money on (negative equity), some dealers might offer to roll that amount into your new 60 months car loan. This inflates your new loan, means you’re paying interest on a depreciated asset, and immediately puts you further underwater. It’s almost always a bad financial move.

- Ignoring the Fine Print: Skipping over the loan agreement’s details can lead to unpleasant surprises later, such as unexpected fees or terms you didn’t anticipate. Take the time to read and understand everything before signing.

- Falling for High-Pressure Sales Tactics: Car buying can be an emotional process. Don’t let a salesperson rush you into a decision. If you feel pressured, step away and take time to think. A good deal will still be there tomorrow.

When a 60-Month Loan Might Not Be Right for You

While a 60 months car loan is a good fit for many, it’s not universally ideal. There are scenarios where a different approach might serve your financial interests better.

- If You Can Afford Shorter Terms: If your budget comfortably allows for higher monthly payments, opting for a 36 or 48-month loan will significantly reduce the total interest you pay. This saves you money in the long run and gets you out of debt faster.

- If You Frequently Trade Cars: If you’re someone who likes to upgrade vehicles every two to three years, a 60-month loan increases the likelihood of being in a negative equity position when you want to trade in. Shorter terms help you build equity faster.

- If You Prioritize Paying Less Interest: For those whose primary financial goal is to minimize interest paid, a 60-month term, by its nature, will accrue more interest than shorter alternatives.

Alternatives to a 60-Month Car Loan

Understanding your options beyond the 60-month term can provide valuable perspective.

- Shorter Loan Terms (36 or 48 Months): These loans come with higher monthly payments but result in significantly less total interest paid. They also help you build equity faster and reduce the risk of negative equity.

- Longer Loan Terms (72 or 84 Months): These offer even lower monthly payments than a 60-month loan, making very expensive cars seem more affordable. However, they come with the highest total interest costs, a prolonged period of debt, and a much higher risk of negative equity, especially with vehicle depreciation. They should be approached with extreme caution.

- Leasing: Leasing involves paying to use a car for a set period (typically 2-4 years) without owning it. Monthly payments are often lower than purchasing, and you usually get to drive a new car more frequently. However, you don’t build equity, have mileage restrictions, and face potential fees for excessive wear and tear.

- Saving Up to Buy Cash: The most financially sound option, if feasible, is to save enough money to buy a car outright. This eliminates interest payments entirely, giving you full ownership from day one and reducing your overall financial burden.

Managing Your 60-Month Car Loan: After the Purchase

Once you’ve signed on the dotted line for your 60 months car loan, the journey isn’t over. Effective management is crucial for a smooth and cost-effective experience.

- Make Payments On Time, Every Time: This might seem obvious, but consistent on-time payments are paramount. They protect your credit score, avoid late fees, and ensure you stay on track to pay off your loan as planned. Set up automatic payments to avoid missing due dates.

- Consider Making Extra Payments: If your financial situation allows, making extra payments can be incredibly beneficial. Even a small additional amount each month or an extra payment once a year can significantly reduce the principal balance, thereby reducing the total interest paid and shortening the loan term. Always ensure extra payments are applied directly to the principal.

- Explore Refinancing Options: Keep an eye on interest rates and your credit score. If rates drop significantly or your credit score improves after a year or two, you might be able to refinance your 60 months car loan to a lower interest rate. This could save you hundreds or even thousands of dollars over the remaining term.

- Budget for Maintenance and Repairs: As your car ages over the five-year loan term, regular maintenance becomes even more critical. Set aside funds specifically for oil changes, tire rotations, and unexpected repairs. Proactive maintenance can prevent larger, more expensive issues down the road. For trusted resources on car maintenance schedules, you can consult sites like Edmunds or Kelley Blue Book.

- Maintain Adequate Insurance Coverage: Continue to carry comprehensive and collision insurance for the life of the loan as required by your lender. Review your policy periodically to ensure it still meets your needs and to check for potentially better rates.

Conclusion: Making an Informed Decision About Your 60 Months Car Loan

A 60 months car loan can be an excellent financing tool, offering the twin benefits of lower monthly payments and access to a wider range of vehicles. However, it’s not a decision to be taken lightly. As we’ve explored in depth, understanding the true financial implications – particularly the total interest paid and the risk of negative equity – is vital.

By taking the time to prepare, getting pre-approved, shopping around for the best rates, and meticulously reviewing all loan documents, you empower yourself to make a decision that aligns with your financial well-being. Remember to look beyond just the monthly payment and consider the entire cost of car ownership over the five-year term.

Ultimately, the best car loan is one that fits comfortably into your budget, minimizes long-term costs, and supports your overall financial goals. Armed with the insights from this comprehensive guide, you are now well-equipped to navigate the world of auto financing and secure a 60 months car loan that truly works for you. Drive informed, drive smart!