Navigating the Road Ahead: Your Expert Guide to Car Loans After Chapter 7 Bankruptcy

Navigating the Road Ahead: Your Expert Guide to Car Loans After Chapter 7 Bankruptcy Carloan.Guidemechanic.com

For many, owning a reliable vehicle isn’t a luxury; it’s a necessity for work, family, and daily life. The thought of needing a car after experiencing the financial upheaval of Chapter 7 bankruptcy can feel daunting, even impossible. You’ve been through a challenging time, and now you’re wondering if a fresh start truly extends to getting back on the road.

The good news is that obtaining car loans with Chapter 7 bankruptcy on your record is absolutely achievable. While it presents unique hurdles, understanding the process, preparing diligently, and adopting strategic approaches can pave your way to securing the financing you need. This comprehensive guide, informed by years of financial insight, will walk you through every step, helping you regain your financial footing and drive away in a new (or new-to-you) car.

Navigating the Road Ahead: Your Expert Guide to Car Loans After Chapter 7 Bankruptcy

Understanding Chapter 7 Bankruptcy and Its Impact on Car Loans

Chapter 7 bankruptcy, often referred to as "liquidation bankruptcy," provides individuals with a clean slate by discharging most unsecured debts. This process typically moves quite quickly, usually concluding within a few months of filing. It’s designed to offer a fresh financial start, freeing you from overwhelming debt burdens.

However, this fresh start comes with a significant mark on your credit report. A Chapter 7 bankruptcy filing remains on your credit history for up to 10 years from the filing date. During this period, your credit score will experience a substantial drop, often falling into the "poor" or "very poor" categories.

This reduced credit score directly impacts a lender’s perception of your creditworthiness. They see a higher risk when lending to someone with a recent bankruptcy. Consequently, securing any type of loan, including a car loan, becomes more challenging immediately after discharge.

It’s crucial to understand that while your credit score takes a hit, bankruptcy also signals that you are no longer burdened by the discharged debts. In some ways, this can be seen as a positive for future lenders, as it indicates you have more disposable income available to manage new obligations responsibly.

The Waiting Period: When Can You Apply for a Car Loan?

One of the most common questions individuals have is, "How soon can I get a car loan after Chapter 7?" There’s no single, universally mandated waiting period. However, practical considerations and lender policies typically dictate the timing.

Most conventional lenders, such as large banks and credit unions, prefer to see some time pass after a bankruptcy discharge. This waiting period allows you to demonstrate renewed financial stability and responsible credit habits. It provides evidence that your financial situation has stabilized.

Based on my experience, many lenders are more willing to consider applications once your Chapter 7 bankruptcy has been officially discharged. The discharge date is critical because it signifies the legal completion of your bankruptcy case. Applying before this date is often futile, as your financial obligations are still in flux.

While some specialized lenders might offer financing even before discharge (though this is rare for Chapter 7 and often comes with extremely unfavorable terms), waiting until after discharge is generally advisable. A few months of demonstrating responsible financial behavior post-discharge can significantly improve your chances and lead to better loan terms.

Rebuilding Your Credit Score: A Crucial First Step

Before you even think about stepping onto a car lot, your absolute priority should be actively rebuilding your credit score. A higher score, even a modest improvement, can unlock better interest rates and more favorable loan terms. This isn’t just about getting a loan; it’s about getting a manageable loan.

There are several effective strategies you can employ to start mending your credit. One excellent option is to obtain a secured credit card. With a secured card, you provide a cash deposit that acts as your credit limit, reducing the risk for the lender.

Another powerful tool is a credit builder loan. These loans involve a financial institution holding the loan amount in a savings account while you make regular payments. Once the loan is paid off, you receive the money, and your on-time payments are reported to credit bureaus. Both of these methods allow you to establish a positive payment history, which is paramount after bankruptcy.

Pro tips from us: Always pay all your bills on time, every time. This includes utilities, rent, and any new credit accounts. Payment history is the single most influential factor in your credit score. Additionally, regularly monitor your credit reports from all three major bureaus (Experian, Equifax, and TransUnion) to ensure accuracy and identify any errors. You can get free copies annually from AnnualCreditReport.com.

Finding the Right Lender for Post-Bankruptcy Car Loans

Not all lenders are created equal, especially when you’re seeking car loans with Chapter 7 bankruptcy on your record. It’s essential to target lenders who specialize in or are accustomed to working with individuals rebuilding their credit.

Specialized lenders, often referred to as "subprime" lenders, are a common route. These institutions have specific programs and underwriting criteria designed for borrowers with less-than-perfect credit histories, including recent bankruptcies. They understand the nuances of post-bankruptcy financing and may be more willing to approve your application.

Credit unions are another excellent option to explore. They are member-owned and often more flexible and understanding than traditional banks. If you have an existing relationship with a credit union, or qualify for membership, their rates and terms can sometimes be more competitive, even for borrowers with past bankruptcy.

Buy Here Pay Here (BHPH) dealerships also offer financing directly. While they can be a last resort, be extremely cautious. These dealerships often charge very high interest rates and may have less favorable terms. Always read the fine print and compare their offers thoroughly before committing.

Finally, a growing number of online lenders specialize in bad credit auto loans. Many offer pre-qualification processes that don’t impact your credit score, allowing you to compare offers from various lenders before making a decision. This can be a convenient way to gauge your options from home.

Preparing Your Application: What Lenders Look For

When applying for a car loan after Chapter 7, thorough preparation is key. Lenders will be looking for stability and a clear ability to repay the loan, even more so given your financial history. Having all your documents in order will streamline the process and demonstrate your seriousness.

You’ll need solid proof of income, typically through recent pay stubs (at least two to three months) or tax returns if you’re self-employed. Lenders want to see a consistent and reliable income stream that clearly supports your proposed monthly car payment, alongside your other living expenses. This is non-negotiable for demonstrating repayment capacity.

Proof of residency is also required, usually in the form of utility bills, a lease agreement, or mortgage statements. This helps lenders verify your address and stability. A stable residence indicates a more reliable borrower.

A significant down payment is perhaps one of the most impactful elements you can bring to the table. It demonstrates your commitment to the purchase and immediately reduces the loan amount, thereby lowering the lender’s risk. We’ll delve deeper into down payments shortly, but start saving now.

If you have a trade-in vehicle, its value can also act like a down payment, further reducing the amount you need to borrow. Make sure to have its title and registration ready. Lastly, and crucially, you must provide your official bankruptcy discharge papers. This document confirms the completion of your Chapter 7 case and is essential for any lender considering a post-bankruptcy loan.

Understanding Loan Terms and Interest Rates

One of the realities of securing car loans with Chapter 7 bankruptcy on your record is that you will likely face higher interest rates. Lenders view borrowers with recent bankruptcies as higher risk, and higher interest rates compensate them for that perceived risk.

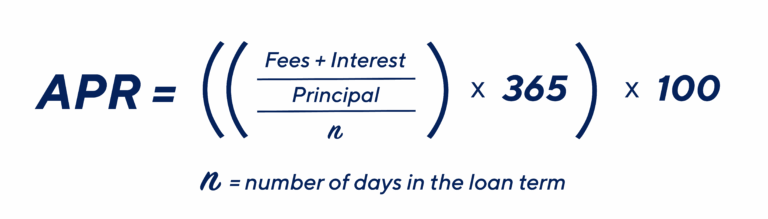

It’s absolutely critical to understand every aspect of your loan terms. Don’t just focus on the monthly payment. Look closely at the Annual Percentage Rate (APR), which includes the interest rate plus any other fees associated with the loan, giving you the true cost of borrowing. A higher APR means you’ll pay significantly more over the life of the loan.

The loan term length is another vital consideration. While a longer loan term (e.g., 72 or 84 months) might result in lower monthly payments, it dramatically increases the total interest you’ll pay over time. For instance, extending a loan by just 12-24 months can add thousands of dollars to the overall cost, even if the monthly payment seems more affordable.

Common mistakes to avoid are focusing solely on the monthly payment without considering the total cost of the loan. Always ask about prepayment penalties. Some lenders charge a fee if you pay off your loan early. While you might not plan to, having the flexibility to refinance or pay off sooner without penalty can be beneficial if your financial situation improves.

The Importance of a Down Payment

As touched upon earlier, a substantial down payment is one of your most powerful assets when seeking a car loan after Chapter 7. It significantly improves your chances of approval and can lead to more favorable loan terms.

From a lender’s perspective, a large down payment reduces their exposure to risk. If you default on the loan, they stand to lose less money because you’ve already invested a significant portion upfront. This makes you a more attractive borrower.

For you, a down payment immediately lowers the total amount you need to finance. This directly translates to lower monthly payments and less interest paid over the life of the loan. Even a small down payment can make a difference, but aiming for 10-20% of the vehicle’s price is often recommended.

Pro tips from us: Start saving aggressively for a down payment as soon as your bankruptcy is discharged. Every dollar saved reduces your reliance on borrowed money and strengthens your position. Consider selling items you no longer need or picking up extra work temporarily to boost your savings fund.

Vehicle Choice: Setting Realistic Expectations

After bankruptcy, it’s vital to adjust your expectations regarding the type of vehicle you can realistically finance. This is not the time to pursue a luxury car or a brand-new model with all the bells and whistles. Your primary goal should be reliable transportation that fits within your newly established budget.

Focus on dependable, affordable cars that serve your immediate needs. A slightly older, well-maintained used car can be an excellent option. They typically have lower purchase prices, which means you’ll need to borrow less and face lower monthly payments. This also translates to lower insurance costs and potentially less depreciation.

While a new car might seem appealing, its rapid depreciation in the first few years means you could quickly owe more than the car is worth (be "upside down" on your loan). This situation can be particularly problematic if you need to sell or trade in the car unexpectedly. For now, prioritize function over flash.

Your aim is to secure a car loan that you can comfortably afford, make all payments on time, and use this positive payment history to rebuild your credit. Once your credit score improves significantly, and your financial situation is rock-solid, you can then consider upgrading to a newer or more luxurious vehicle.

Navigating Dealerships: Tips for Success

Walking into a dealership after bankruptcy can feel intimidating, but armed with knowledge and preparation, you can approach the process with confidence. Being transparent and proactive is crucial.

First, be upfront about your bankruptcy. There’s no benefit in trying to hide it; lenders will discover it during the credit check anyway. Explaining your situation calmly and demonstrating your proactive steps toward financial recovery can actually build trust with a salesperson or finance manager.

Based on my experience, it’s often beneficial to secure pre-approvals from a few different lenders before you even visit a dealership. This gives you concrete offers to compare and provides leverage during negotiations. You’ll know what interest rate and terms you qualify for, empowering you to walk away if a dealership tries to push a less favorable deal.

When you’re at the dealership, negotiate wisely. Don’t feel pressured to make an immediate decision. Focus on the total price of the car, not just the monthly payment. Be wary of additional products or services (like extended warranties or rust proofing) that significantly inflate the loan amount, unless you genuinely need and understand them.

Pro tips from us: If possible, bring a trusted friend or family member with you. A second set of eyes and ears can help you stay objective and avoid impulsive decisions. They can also ask questions you might overlook and provide emotional support during a potentially stressful process.

The Role of a Co-Signer (and its risks)

A co-signer can significantly improve your chances of getting approved for a car loan after Chapter 7, especially with more favorable terms. A co-signer, typically someone with excellent credit, essentially guarantees the loan. Their good credit score offsets the risk associated with your bankruptcy.

If you default on the loan, the co-signer becomes legally responsible for the entire debt. This is a massive responsibility, and it highlights the inherent risks involved. The co-signer’s credit score will also be impacted by the loan, whether positively (if you pay on time) or negatively (if you miss payments).

While a co-signer can open doors, it should be approached with extreme caution and only with someone you trust implicitly, like a close family member. Both parties need to fully understand the legal and financial implications.

Common mistakes to avoid are asking someone to co-sign without a clear plan for consistent, on-time payments. A missed payment not only harms your credit but also damages your co-signer’s credit and potentially your relationship. Ensure you can absolutely meet the financial obligation before involving another person.

Refinancing Your Car Loan After Improving Credit

Securing your initial car loan after bankruptcy might come with a higher interest rate, which is often a necessary step on the road to credit recovery. However, this doesn’t have to be a permanent situation. Refinancing your car loan is a smart long-term strategy once your credit score has significantly improved.

Refinancing involves taking out a new loan to pay off your existing car loan. The goal is typically to secure a lower interest rate, which can dramatically reduce your monthly payments and the total amount of interest you pay over the life of the loan. It’s a powerful way to save money once you’ve proven your creditworthiness.

When should you consider refinancing? Typically, after 12-18 months of consistent, on-time payments on your current car loan. By this point, your credit score should have improved considerably, demonstrating a solid track record of responsible borrowing. A lower debt-to-income ratio and a higher credit score will make you a more attractive candidate for new lenders.

Pro tips from us: Shop around for refinancing offers just as you would for an initial loan. Compare rates from multiple banks, credit unions, and online lenders. Make sure to factor in any fees associated with the new loan to ensure the refinancing truly saves you money in the long run.

Common Mistakes to Avoid When Getting a Car Loan After Chapter 7

Navigating the post-bankruptcy landscape for a car loan is tricky, and it’s easy to fall into common pitfalls. Being aware of these can save you significant time, money, and stress.

First, not checking your credit reports regularly is a major oversight. Errors on your report can unfairly depress your score. Always ensure all accounts are reported accurately, especially your bankruptcy discharge.

Applying for loans everywhere (often called "shotgunning applications") is another common mistake. Each hard inquiry can temporarily ding your credit score. While FICO models typically group multiple auto loan inquiries within a short period (usually 14-45 days) as a single inquiry, spreading them out over months can be detrimental.

Going into the process without a down payment is a significant disadvantage. As we’ve discussed, a down payment is crucial for reducing risk and improving terms. Common mistakes to avoid are assuming you can get approved without one, or neglecting to save up enough cash.

Another critical error is buying more car than you can truly afford. High monthly payments can quickly become overwhelming, potentially leading to missed payments and further credit damage. Stick to your budget, even if it means compromising on features.

Finally, ignoring the fine print of loan terms can lead to expensive surprises. Don’t sign anything until you fully understand the APR, loan term, any fees, and prepayment penalties. Based on my experience, many individuals get caught by unexpected clauses because they didn’t take the time to read the agreement thoroughly.

Life After Bankruptcy: Maintaining Good Financial Habits

Getting a car loan after Chapter 7 is a significant step, but it’s just one part of your broader financial recovery journey. Sustaining good financial habits is paramount to prevent future challenges and continue building a strong financial future.

Effective budgeting is the cornerstone of financial health. Create a realistic budget that tracks all your income and expenses. This ensures you know exactly where your money is going and can allocate funds for your car payments, savings, and other necessities without stress. For more on managing your finances post-bankruptcy, check out our guide on "Rebuilding Your Credit Score Effectively."

Building an emergency fund is another non-negotiable step. Life is unpredictable, and having a financial cushion for unexpected expenses (like car repairs, medical bills, or job loss) prevents you from relying on credit or going into debt again. Aim for at least three to six months’ worth of living expenses.

Responsible credit use, post-bankruptcy, means making all payments on time, keeping credit utilization low on any new credit cards, and avoiding taking on unnecessary debt. Your car loan, with its consistent payments, will be a powerful tool in rebuilding your credit, but only if you manage it responsibly.

Embrace continuous financial literacy. The more you understand about personal finance, investing, and debt management, the better equipped you’ll be to make sound decisions and protect your newly found financial stability. Understanding how to manage your credit effectively is a lifelong skill. If you’re weighing your options, you might also find our article "Understanding Different Types of Car Loans" helpful. For external resources on financial literacy, the Consumer Financial Protection Bureau (CFPB) offers excellent, unbiased information.

Conclusion: Driving Towards a Brighter Financial Future

Navigating the path to securing car loans with Chapter 7 bankruptcy on your record requires patience, strategic planning, and a commitment to rebuilding your financial life. While the initial challenges may seem formidable, remember that bankruptcy is a fresh start, not a permanent roadblock.

By understanding the impact of bankruptcy, diligently rebuilding your credit, choosing the right lenders, and preparing thoroughly for your application, you can absolutely secure the transportation you need. Focus on realistic vehicle choices, save for a substantial down payment, and meticulously review all loan terms.

This journey is about more than just a car; it’s about demonstrating your renewed financial responsibility and paving the way for a brighter future. With discipline and informed decision-making, you’ll not only get back on the road but also continue building a strong, stable financial foundation for years to come.