Navigating the Road Ahead: Your Expert Guide to Common Car Loan Terms

Navigating the Road Ahead: Your Expert Guide to Common Car Loan Terms Carloan.Guidemechanic.com

Buying a car is an exciting milestone, but for many, the journey involves securing a car loan. Understanding the language of vehicle financing can feel like learning a new dialect, full of jargon and complex concepts. Yet, mastering these common car loan terms is not just about sounding smart; it’s about empowering yourself to make informed decisions, save money, and avoid costly mistakes.

As an expert blogger and professional in the automotive finance space, I’ve seen countless individuals navigate the sometimes-treacherous waters of auto loans. My mission with this comprehensive guide is to demystify these terms, transforming confusion into clarity. We’ll break down everything from the interest rate and APR to negative equity and GAP insurance, ensuring you’re fully equipped to confidently sign on the dotted line.

Navigating the Road Ahead: Your Expert Guide to Common Car Loan Terms

Why Understanding Car Loan Terms is Your Ultimate Power Move

Based on my experience, one of the biggest pitfalls for car buyers is signing a loan agreement without fully grasping its implications. This isn’t just about the monthly payment; it’s about the total cost, the flexibility, and the long-term financial health of your investment. Think of your car loan as a partnership with a lender. To ensure it’s a fair and beneficial partnership, you need to speak the same language.

Without a solid understanding, you might inadvertently agree to unfavorable conditions, pay more than necessary, or find yourself in a difficult financial situation down the line. This article is designed to be your essential roadmap, turning complex vehicle financing concepts into actionable knowledge. Let’s dive in and unlock the secrets to smart auto loan management.

The Absolute Essentials: Core Car Loan Terms You Must Know

Before you even step foot into a dealership or apply for a loan online, familiarizing yourself with these fundamental car loan terms is non-negotiable. They form the bedrock of every loan agreement.

1. Principal: The Heart of Your Loan

At its simplest, the principal is the actual amount of money you borrow to purchase your vehicle. It’s the sticker price of the car, minus any down payment, trade-in value, or rebates. This is the starting figure upon which all interest calculations are made.

When you make your monthly payment, a portion of it goes towards reducing this principal amount, and another portion covers the interest charged by the lender. Early in your loan term, a larger share of your payment often goes to interest, with less applied to the principal. Over time, as the principal balance decreases, more of your payment starts chipping away at the core amount.

Understanding the principal is crucial because it directly impacts the interest you’ll pay over the life of the loan. A higher principal means more interest, assuming the same rate and term. Always aim to reduce your principal as much as possible upfront through a substantial down payment.

2. Interest Rate vs. APR (Annual Percentage Rate): Don’t Get Them Confused!

These two terms are often used interchangeably, but they represent distinct concepts. Knowing the difference is paramount for truly understanding the cost of your vehicle financing.

The interest rate is essentially the percentage a lender charges you for borrowing the principal amount. It’s expressed as a percentage and applies directly to your loan balance. A lower interest rate generally means lower monthly payments and a lower total cost of the loan. Factors like your credit score, the loan term, and market conditions heavily influence the interest rate you’ll be offered.

However, the APR (Annual Percentage Rate) is the true cost of borrowing money, encompassing not just the interest rate but also other fees associated with the loan. This can include origination fees, processing fees, or even certain insurance premiums bundled into the loan. For example, some lenders might offer a seemingly low interest rate but then tack on high fees, making the APR much higher.

Pro tips from us: Always compare loans based on their APR, not just the interest rate. The APR gives you the most accurate picture of the total annual cost of your credit. It’s the most transparent figure for comparing different loan offers side-by-side.

3. Loan Term: How Long Will You Be Paying?

The loan term refers to the length of time, typically expressed in months, over which you agree to repay your auto loan. Common loan terms range from 36 months (3 years) to 84 months (7 years), with 60 or 72 months being very popular.

A shorter loan term generally means higher monthly payments but a lower total amount paid in interest over the life of the loan. This is because the lender has less time to accrue interest. Conversely, a longer loan term will result in lower monthly payments, making the car seem more affordable upfront. However, you’ll end up paying significantly more in total interest charges over the extended period.

Based on my experience, many buyers fall into the trap of solely focusing on the lowest monthly payment. While understandable, extending your loan term too much can lead to negative equity faster and significantly increase the overall cost of the car. It’s a delicate balance between affordability and financial prudence.

4. Monthly Payment: Your Recurring Obligation

Your monthly payment is the fixed amount you agree to pay your lender each month until the loan is fully satisfied. This payment is a combination of a portion of the principal and the accrued interest for that period.

Several factors determine the size of your monthly payment: the principal amount, the interest rate, and the loan term. A higher principal, a higher interest rate, or a shorter loan term will all result in a higher monthly payment. Conversely, a larger down payment reduces the principal, leading to lower monthly payments.

It’s crucial to ensure your monthly payment fits comfortably within your budget, not just now, but for the entire duration of the loan. Don’t stretch your finances too thin, as missing payments can severely damage your credit score.

5. Down Payment: Your Upfront Investment

A down payment is the initial sum of money you pay towards the purchase of the vehicle, reducing the amount you need to borrow. It’s your direct equity in the car from day one.

Making a substantial down payment offers several significant advantages. Firstly, it lowers your principal loan amount, which in turn reduces your monthly payments and the total interest you’ll pay over the loan term. Secondly, it can help you secure a better interest rate because lenders view borrowers with more skin in the game as less risky. Finally, a larger down payment helps prevent you from going "upside down" on your loan, a concept we’ll discuss shortly.

Common mistakes to avoid are skimping on the down payment just to drive off the lot. While 0% down loans exist, they often come with higher interest rates or other less favorable terms, ultimately costing you more. Aim for at least 10-20% of the vehicle’s purchase price if possible.

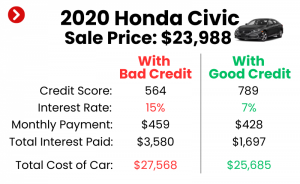

6. Credit Score: Your Financial Reputation

Your credit score is a numerical representation of your creditworthiness, essentially a report card on how well you’ve managed borrowed money in the past. It’s one of the most critical factors lenders consider when evaluating your auto loan application.

Lenders use your credit score to assess the risk of lending you money. A high credit score (generally 700+) indicates a responsible borrower, making you eligible for the best interest rates and most favorable car loan terms. A lower credit score (below 620) suggests a higher risk, which can result in higher interest rates, stricter loan terms, or even loan denial.

Pro tips from us: Check your credit score and report well before you start shopping for a car. This allows you time to correct any errors and potentially improve your score, which could save you thousands of dollars in interest over the life of the loan. You can often get a free credit report from AnnualCreditReport.com.

7. Collateral: The Security for Your Loan

In the context of a car loan, the vehicle itself serves as collateral. This means that if you fail to make your monthly payments as agreed (default on the loan), the lender has the legal right to repossess the car to recover their losses.

This is why car loans are considered "secured" loans. The collateral provides a safety net for the lender, which is why they are often more willing to offer competitive interest rates compared to unsecured loans (like personal loans). Understanding that your car is collateral reinforces the importance of consistent and timely loan payments.

Beyond the Basics: Advanced & Important Car Loan Terms

Once you’ve got the core concepts down, it’s time to delve into some more nuanced vehicle financing terms that can significantly impact your financial situation.

8. Debt-to-Income Ratio (DTI): Are You Overburdened?

Your Debt-to-Income Ratio (DTI) is a key metric lenders use to assess your ability to manage monthly payments and repay debt. It’s calculated by dividing your total monthly debt payments (including the prospective car loan payment) by your gross monthly income.

Lenders typically prefer a DTI ratio below a certain threshold, often 36% or 43%, though this can vary. A low DTI indicates that you have sufficient income to cover your existing debts and the new car loan without undue financial strain. A high DTI might signal to lenders that you’re already overextended, making them less likely to approve your loan or offering less favorable car loan terms.

9. Equity & Negative Equity (Upside Down): Your Car’s Value vs. Your Debt

Equity in a car refers to the difference between the car’s current market value and the amount you still owe on your loan. If your car is worth more than what you owe, you have positive equity. This is a desirable position, especially if you plan to trade in or sell your vehicle.

Conversely, negative equity, also known as being "upside down" or "underwater" on your loan, occurs when you owe more on your car than its current market value. This is a common problem, especially with new cars that depreciate rapidly in the first few years. If your car is totaled or stolen while you have negative equity, your insurance payout might not cover the full amount you still owe the lender, leaving you to pay the difference out of pocket.

Common mistakes to avoid are putting very little down and opting for a very long loan term. Both can accelerate negative equity.

10. Refinancing: A Second Chance at Better Terms

Refinancing an auto loan means taking out a new loan to pay off your existing car loan, often with different (and hopefully better) car loan terms. People typically refinance to secure a lower interest rate, reduce their monthly payments, or shorten/lengthen their loan term.

You might consider refinancing if your credit score has significantly improved since you first took out the loan, if market interest rates have dropped, or if your financial situation has changed and you need a more manageable monthly payment. Refinancing can potentially save you a substantial amount of money over the life of the loan.

For more insights on when refinancing makes sense, check out our related article: Is Car Loan Refinancing Right for You? (Internal Link Placeholder)

11. Prepayment Penalty: Freedom to Pay Early?

A prepayment penalty is a fee charged by some lenders if you pay off your car loan earlier than the agreed-upon loan term. Lenders impose these penalties to recoup some of the interest income they would have earned if the loan had run its full course.

While not as common with auto loans as with mortgages, it’s crucial to check your loan agreement for any such clauses before signing. If you anticipate having the ability to pay off your loan early, ensure your loan doesn’t penalize you for doing so. Most standard vehicle financing agreements for cars do not include prepayment penalties, but it’s always wise to confirm.

12. Guaranteed Asset Protection (GAP) Insurance: Your Safety Net

GAP insurance is an optional add-on that protects you in the event your car is stolen or totaled and you have negative equity. As we discussed, if your car is worth less than what you owe, your standard auto insurance policy will only pay out the car’s actual cash value, leaving you responsible for the remaining balance.

GAP insurance covers this "gap" between what your primary insurance pays and the outstanding balance on your car loan. It’s particularly valuable if you made a small down payment, opted for a long loan term, or bought a car that depreciates quickly.

Pro tips from us: While often offered by dealerships, you can frequently find GAP insurance for a lower price through your own auto insurance provider or a third-party insurer. Always compare prices before committing.

13. Balloon Payment: A Final, Large Sum

A balloon payment loan structure is less common for typical consumer auto loans but exists, particularly for luxury cars or commercial vehicles. With a balloon payment loan, your monthly payments are lower throughout the loan term because a significant portion of the principal is deferred until the very end.

At the end of the loan term, you face a single, large lump-sum payment – the "balloon" – to pay off the remaining balance. While this offers lower monthly payments, it requires careful financial planning to ensure you can afford the large final payment or arrange for refinancing at that time. Failing to make the balloon payment can lead to repossession.

14. Loan Agreement / Contract: The Fine Print That Matters Most

The loan agreement, or contract, is the legally binding document that outlines all the car loan terms and conditions between you and the lender. It details the principal amount, interest rate, APR, loan term, monthly payment schedule, any fees, and what constitutes a default.

This document is where all the concepts we’ve discussed come together. It’s imperative to read every line of this contract before signing. Don’t be afraid to ask questions about anything you don’t understand. Once signed, you are legally bound by its terms.

Pro Tips for Navigating Car Loans Like a Pro

Understanding the jargon is just the first step. Here are some seasoned tips to ensure you secure the best possible vehicle financing.

- Get Pre-Approved: Before you even set foot on a dealership lot, get pre-approved for an auto loan from a bank or credit union. This gives you a clear budget, an idea of the interest rate you qualify for, and empowers you to negotiate with confidence. You’ll know exactly what car loan terms are acceptable.

- Shop Around for Lenders: Don’t just take the first loan offer. Compare offers from multiple banks, credit unions, and online lenders. Even a small difference in APR can save you hundreds, if not thousands, over the loan term.

- Read the Fine Print, Seriously: As mentioned, the loan agreement is your ultimate guide. Don’t rush through it. Look for any hidden fees, prepayment penalties, or unusual clauses. Your future financial well-being depends on it.

- Understand Your Budget Beyond the Monthly Payment: Factor in insurance, fuel, maintenance, and potential repair costs when determining how much car you can truly afford. The monthly payment is only one piece of the puzzle.

- Focus on the Total Cost, Not Just Monthly Payments: While lower monthly payments are attractive, they often come with longer loan terms and higher overall interest paid. Calculate the total amount you’ll pay back over the life of the loan to make a truly informed decision.

Common Mistakes to Avoid When Securing Your Auto Loan

Even with all this knowledge, it’s easy to make missteps. Here are some of the most frequent vehicle financing mistakes I’ve observed.

- Not Checking Your Credit Score: Going into negotiations blind without knowing your credit score puts you at a disadvantage. Lenders may offer you higher rates than you deserve.

- Ignoring the APR: Focusing solely on the advertised interest rate and overlooking the APR can lead to paying more in fees than you realize. Always compare the APR.

- Extending the Loan Term Too Much: While it lowers monthly payments, a very long loan term (e.g., 72 or 84 months) significantly increases the total interest paid and puts you at higher risk of negative equity.

- Forgetting About Hidden Fees: Be vigilant for documentation fees, administrative charges, or other add-ons that can inflate the total cost of your car loan. Always ask for a full breakdown.

- Buying More Car Than You Can Afford: It’s tempting to get the latest model, but overspending on a car loan can strain your finances, making it difficult to meet other financial obligations or save for the future. Remember your DTI!

For further reading on smart car buying strategies, consider our article: Smart Car Buying Strategies: Beyond the Loan (Internal Link Placeholder)

The Road to Smart Car Ownership Starts Here

Navigating the world of common car loan terms doesn’t have to be intimidating. By understanding the definitions and implications of each term – from principal and interest rate to GAP insurance and negative equity – you empower yourself to make intelligent decisions. This knowledge is your shield against unfavorable deals and your sword for securing the best possible vehicle financing for your needs.

Remember, a car loan is a significant financial commitment. Take your time, do your research, and don’t hesitate to ask questions. With this comprehensive guide in hand, you are now well-equipped to drive away with confidence, knowing you’ve secured a loan that truly works for you. Happy driving!