Navigating the Road Ahead: Your Expert Guide to Getting a Car Loan After Chapter 7 Bankruptcy

Navigating the Road Ahead: Your Expert Guide to Getting a Car Loan After Chapter 7 Bankruptcy Carloan.Guidemechanic.com

Filing for Chapter 7 bankruptcy can feel like hitting a financial reset button, offering a fresh start from overwhelming debt. However, the path forward often comes with new challenges, particularly when it comes to securing credit for major purchases like a car. Many people assume that getting a car loan after Chapter 7 is impossible, or at best, an uphill battle with predatory lenders.

Based on my experience as a financial expert and observing countless individuals navigate this very situation, I can tell you that it’s absolutely possible to get a car loan after Chapter 7. It requires strategic planning, patience, and a deep understanding of how lenders view your financial situation post-bankruptcy. This comprehensive guide will illuminate the path, providing you with the knowledge and actionable steps needed to confidently secure an auto loan and rebuild your financial future.

Navigating the Road Ahead: Your Expert Guide to Getting a Car Loan After Chapter 7 Bankruptcy

Understanding Chapter 7 and Its Immediate Impact on Your Credit

Before we delve into the "how-to," it’s crucial to grasp what Chapter 7 bankruptcy means for your financial standing and, specifically, your credit score. This understanding forms the foundation of your recovery strategy.

What Chapter 7 Means for Your Financial Standing

Chapter 7 bankruptcy, often referred to as "liquidation bankruptcy," involves selling non-exempt assets to pay off creditors. Once the process is complete, most unsecured debts are discharged, providing a significant fresh start. While it offers immense relief from debt, it also leaves a prominent mark on your credit report.

This bankruptcy will remain on your credit report for ten years from the filing date. During this period, lenders will be aware of your past financial struggles, which naturally makes them more cautious. Your ability to get new credit will be impacted, but not permanently destroyed.

The Credit Score Hit: Reality and Recovery

A Chapter 7 bankruptcy filing typically causes a substantial drop in your credit score, often by 100-200 points or more, depending on your score before filing. This immediate decline is due to the severe negative impact bankruptcy has on your credit history. Lenders use credit scores to assess risk, and a low score indicates a higher risk.

However, it’s important to remember that a credit score is not static. It’s a dynamic number that reflects your most recent financial behaviors. The moment you file for bankruptcy, your old debts are discharged, meaning you have less debt burden. This reduction in debt, combined with responsible financial habits moving forward, becomes the cornerstone of your credit recovery.

The Waiting Game: How Long Until You Can Apply?

While there’s no official "waiting period" mandated by law before you can apply for a car loan after Chapter 7, most lenders prefer to see some time pass. Many conventional lenders look for a minimum of 1-2 years post-discharge before considering an auto loan application. This waiting period allows them to observe your financial behavior and see if you’ve established new, positive credit habits.

Some subprime lenders, however, might consider applications much sooner, even immediately after discharge. These lenders specialize in working with individuals who have challenging credit histories. The key is understanding that the longer you wait and the more diligently you work on rebuilding your credit, the better your loan terms and interest rates are likely to be.

The First Steps: Rebuilding Your Financial Foundation

Successfully getting a car loan after Chapter 7 isn’t just about finding a lender; it’s fundamentally about rebuilding your credit and demonstrating renewed financial responsibility. This phase is critical and sets the stage for future financial success.

Secured Credit Cards: A Powerful Tool

One of the most effective ways to start rebuilding your credit is by using a secured credit card. Unlike traditional credit cards, a secured card requires you to put down a deposit, which often becomes your credit limit. This deposit minimizes the risk for the lender.

By using this card responsibly – making small purchases and paying the balance in full and on time every month – you’ll establish a positive payment history. Lenders report this activity to the credit bureaus, gradually improving your credit score. From a professional perspective, secured cards are an invaluable first step.

Credit Builder Loans: An Often Overlooked Strategy

Another excellent tool in your credit rebuilding arsenal is a credit builder loan. With this type of loan, a bank or credit union lends you a small amount, but instead of giving you the money upfront, they hold it in a savings account or certificate of deposit. You then make regular payments on the loan over a set period.

Once the loan is fully paid, you receive the money. The significant benefit is that your timely payments are reported to the credit bureaus, showing a consistent, positive payment history. It’s a unique way to save money while simultaneously building your credit score.

Monitoring Your Credit: The Importance of Vigilance

As you embark on your credit rebuilding journey, regularly monitoring your credit report is paramount. Errors on your report can hinder your progress and should be disputed immediately. You’re entitled to a free copy of your credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) once every 12 months via AnnualCreditReport.com.

Pro tips from us: Don’t just pull your report once a year. Consider using a reputable credit monitoring service that provides more frequent updates. Understanding what’s on your credit report and how it impacts your score is crucial for making informed financial decisions. For more detailed insights, consider reading our article on Understanding Your Credit Report and Score After Bankruptcy.

Preparing for Your Car Loan Application: Strategy is Key

Approaching the car loan application process strategically can significantly improve your chances of approval and help you secure more favorable terms. This involves more than just filling out a form.

Knowing Your Financial Landscape: Budgeting and Affordability

Before you even think about looking at cars, sit down and create a realistic budget. Understand exactly how much you can comfortably afford for a monthly car payment, insurance, fuel, and maintenance. Overextending yourself on a car loan is a common mistake that can lead to further financial distress.

Based on my experience, many people get caught up in the excitement of a new car and overlook the true cost of ownership. A car loan is a commitment, and ensuring it fits within your budget is the first step to responsible borrowing. Don’t let a lender tell you what you can afford; know it yourself first.

Saving for a Down Payment: Your Best Ally

One of the most powerful tools you have when seeking a car loan after Chapter 7 is a substantial down payment. A larger down payment reduces the amount you need to borrow, which in turn lowers the lender’s risk. It also demonstrates your financial discipline and commitment.

Lenders are more willing to approve loans for applicants who put money down, especially those with a bankruptcy on their record. It shows you have "skin in the game" and are less likely to default. Aim for at least 10-20% of the car’s purchase price, if possible.

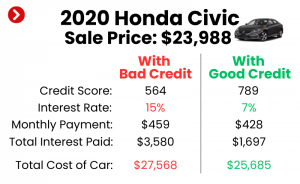

Understanding Interest Rates and Loan Terms

When you have a bankruptcy on your record, you should anticipate higher interest rates compared to borrowers with excellent credit. This is simply how lenders mitigate perceived risk. However, it’s vital to understand that rates can vary significantly between lenders.

Focus not only on the monthly payment but also on the total cost of the loan over its term. A longer loan term might offer lower monthly payments but will result in paying significantly more in interest over the life of the loan. Aim for the shortest term you can comfortably afford to minimize interest charges.

Gathering Your Documents: What Lenders Will Ask For

Being prepared with all necessary documentation can streamline the application process and show your seriousness. Lenders will typically ask for:

- Proof of income (pay stubs, tax returns, bank statements)

- Proof of residence (utility bills, lease agreement)

- Identification (driver’s license, social security card)

- Bankruptcy discharge papers

- Proof of insurance

Having these documents ready demonstrates your organization and transparency, which can positively influence a lender’s decision.

Finding the Right Lender: Where to Look for a Car Loan After Chapter 7

Not all lenders are created equal, especially when it comes to financing after bankruptcy. Knowing where to look can save you time and frustration.

Specialty Lenders for Bad Credit Auto Loans

There are many lenders who specialize in subprime auto loans, catering specifically to individuals with challenging credit histories, including those with past bankruptcies. These lenders understand the unique circumstances of post-bankruptcy borrowers and have underwriting criteria that accommodate this.

While their interest rates might be higher, they offer a viable path to getting approved. Look for reputable subprime lenders online or ask your dealership if they work with such institutions. Always check reviews and their standing with the Better Business Bureau.

Credit Unions: Often More Lenient

Credit unions are member-owned financial institutions known for their community focus and often more flexible lending practices compared to traditional banks. They may be more willing to work with members who have a bankruptcy on their record, especially if you have an established relationship with them.

It’s always a good idea to check with your local credit union first. Their rates and terms can often be more favorable than those offered by other subprime lenders.

Buy Here, Pay Here Dealerships: Pros and Cons

Buy Here, Pay Here (BHPH) dealerships offer in-house financing, meaning they are both the seller and the lender. They often approve applicants regardless of their credit history, which can seem appealing immediately after bankruptcy. However, there are significant downsides.

Common mistakes to avoid are jumping into a BHPH loan without fully understanding the terms. BHPH loans typically come with very high interest rates, short loan terms, and often require frequent payments (weekly or bi-weekly). The vehicles themselves might also be older, higher mileage, and come with fewer guarantees. Use these as a last resort, and only after thoroughly exploring all other options.

Online Loan Marketplaces

Several online platforms act as marketplaces, connecting borrowers with multiple lenders. These platforms can be particularly useful for those with challenging credit, as they allow you to submit one application and receive offers from various lenders specializing in different credit tiers. This can help you compare offers without impacting your credit score multiple times.

Using these platforms can save you time and potentially lead to a better deal by fostering competition among lenders. Ensure the platform is reputable and secure before submitting your personal information.

Avoiding Predatory Lenders

Our pro tips for you include being extremely wary of any lender that guarantees approval without checking your credit, charges excessive upfront fees, or pressure you into signing immediately. These are red flags for predatory lending practices. Reputable lenders will always review your credit and income.

Avoid any deal that feels too good to be true or puts undue pressure on you. The goal is to get a car, but also to continue rebuilding your financial health, not to fall into another debt trap.

The Application Process: What to Expect and How to Succeed

Once you’ve done your homework and found potential lenders, the application process itself requires a strategic approach.

Being Honest About Your Bankruptcy

There’s no point in trying to hide your bankruptcy; lenders will see it on your credit report. Being upfront and honest about your past financial challenges demonstrates integrity and transparency. It also allows you to frame your narrative positively.

Explain what you’ve learned and how you’ve changed your financial habits since the bankruptcy. This honesty can build trust with the lender.

Explaining Your Financial Situation (The "Why")

Lenders want to understand the story behind your bankruptcy. Was it due to medical bills, job loss, divorce, or something else? More importantly, they want to know what steps you’ve taken to prevent a recurrence. Be prepared to articulate:

- The cause of your bankruptcy.

- The positive changes you’ve made (e.g., budgeting, new job, secured credit cards).

- Your current stable income and living situation.

This narrative helps humanize your application beyond just a credit score.

The Role of a Co-Signer

A co-signer with good credit can significantly improve your chances of approval and potentially secure a lower interest rate. When someone co-signs, they agree to be equally responsible for the loan if you default. This reduces the risk for the lender.

However, consider this option carefully. A co-signer’s credit will be affected by your payments, and if you default, their credit will suffer, and they will be responsible for the debt. Only use a co-signer if you are absolutely confident in your ability to make timely payments. It’s a significant favor to ask.

Negotiating the Deal: Focusing Beyond Just the Monthly Payment

When negotiating your car loan, resist the urge to focus solely on the monthly payment. Dealerships often try to stretch out loan terms to lower monthly payments, which results in you paying much more interest over time. Instead, focus on:

- The total price of the car: Negotiate this first.

- The interest rate (APR): A lower APR saves you thousands.

- The loan term: Aim for the shortest term you can afford.

- Any additional fees or add-ons: Question everything.

Based on my experience, negotiating holistically will lead to a better overall deal and prevent you from overpaying in the long run.

Pro Tips for Boosting Your Chances of Approval and Getting Better Terms

Beyond the standard steps, there are specific strategies you can employ to further enhance your application.

Showcasing Financial Stability Post-Bankruptcy

Lenders are looking for evidence that your financial situation has stabilized since your bankruptcy discharge. This includes:

- Consistent employment: A steady job with a reliable income is crucial.

- Stable residence: Living in the same place for an extended period shows stability.

- Low debt-to-income ratio: Demonstrate that your current income can comfortably cover your existing debts plus the new car payment.

Any evidence you can provide to illustrate your financial reliability will be a significant plus.

The Power of a Larger Down Payment

As mentioned earlier, a larger down payment signals reduced risk to the lender and your commitment to the purchase. It also means you’ll borrow less, resulting in lower monthly payments and less interest paid over the life of the loan. From a professional perspective, this is one of the most impactful actions you can take.

If you can save an extra few thousand dollars, it will make a noticeable difference in the terms you’re offered.

Choosing the Right Vehicle: Practicality Over Luxury

When your credit is still recovering, opting for a modest, reliable, and affordable used car is a far wiser choice than a brand-new luxury vehicle. Lenders are more likely to approve loans for less expensive cars, as the risk is lower for them.

A practical choice also means lower insurance costs and less depreciation, further aiding your financial recovery. You can always upgrade once your credit is fully restored.

Demonstrating Your Commitment to Timely Payments

If you have any new credit accounts opened since your bankruptcy (like a secured credit card or credit builder loan), ensure you have a flawless payment history. Lenders will scrutinize these recent accounts. Showing even a few months of perfect payment behavior can be incredibly impactful.

This demonstrates your renewed commitment to financial responsibility, proving that you’ve learned from past mistakes.

Common Mistakes to Avoid When Seeking an Auto Loan After Bankruptcy

Even with the best intentions, it’s easy to fall into common traps when seeking a car loan after bankruptcy. Being aware of these pitfalls can save you from costly errors.

Applying to Too Many Lenders

Each time you apply for credit, a "hard inquiry" is placed on your credit report, which can slightly lower your score. Applying to too many lenders within a short period can make you appear desperate to lenders and further ding your credit.

Pro tips from us: Do your research beforehand and target a few specific lenders most likely to approve you. If you’re comparing rates, try to do so within a 14-45 day window, as multiple inquiries for the same type of loan within this timeframe are often counted as a single inquiry by credit scoring models.

Ignoring Your Budget

As emphasized earlier, failing to create and stick to a realistic budget is a recipe for disaster. Getting approved for a loan doesn’t mean you can truly afford it. Overspending on a car can lead to missed payments, further damage to your credit, and potentially repossession.

Always prioritize your financial stability over the desire for a specific vehicle. Your budget should be your ultimate guide.

Settling for the First Offer

Because you have a bankruptcy on your record, you might feel pressured to accept the very first loan offer you receive. This is a common mistake. Even with less-than-perfect credit, it’s always worth comparing offers from multiple lenders.

Competition among lenders, even in the subprime market, can result in better terms for you. Never feel obligated to accept an offer on the spot.

Not Reading the Fine Print

Loan agreements can be complex, but it’s crucial to read every line of the contract before signing. Pay close attention to:

- The Annual Percentage Rate (APR)

- Any hidden fees or charges

- Prepayment penalties

- The total cost of the loan

If anything is unclear, ask for clarification. Don’t sign anything you don’t fully understand.

Life After the Loan: Maintaining Good Credit and Financial Health

Getting the car loan is a significant milestone, but your journey doesn’t end there. It’s an opportunity to solidify your financial recovery.

Making Payments On Time, Every Time

This is arguably the most important aspect of maintaining good credit and strengthening your financial health. Your car loan payments are reported to the credit bureaus, and a perfect payment history will steadily rebuild your credit score. Set up automatic payments to avoid missing due dates.

Consistent, on-time payments demonstrate your reliability and will open doors to better financial products in the future.

Avoiding New Debt

While you’re working to rebuild your credit, it’s wise to avoid taking on unnecessary new debt. Each new loan or credit card adds to your financial obligations and can slow down your credit recovery. Focus on managing your current debts responsibly.

The goal is to show a pattern of responsible borrowing and repayment, not to accumulate more debt.

Regularly Reviewing Your Credit Report

Continue to monitor your credit report regularly for accuracy and to track your progress. As your credit score improves, you’ll see the positive impact of your efforts. This ongoing vigilance helps you spot any issues early and celebrate your achievements.

For more guidance on this, check out our in-depth article: A Step-by-Step Guide to Improving Your Credit Score After Bankruptcy.

Considering Refinancing Down the Road

As your credit score improves (typically after 12-24 months of on-time payments on your car loan and other credit accounts), you may become eligible for a lower interest rate. This is known as refinancing.

Refinancing can significantly reduce your monthly payments and the total amount of interest you pay over the life of the loan. It’s a smart financial move once you’ve proven your creditworthiness.

Conclusion: Your Road to Financial Recovery is Clear

Getting a car loan after filing Chapter 7 bankruptcy might seem daunting at first, but it is a thoroughly achievable goal. It requires a clear understanding of the process, strategic planning, and a commitment to rebuilding your financial foundation. By focusing on repairing your credit, saving for a down payment, being honest with lenders, and making informed decisions, you can secure the transportation you need and continue on your path to financial freedom.

Remember, bankruptcy is a fresh start, not a permanent roadblock. With patience and diligence, you can navigate the road ahead successfully and emerge with stronger credit and greater financial stability. Start today by taking those crucial first steps toward rebuilding your credit, and soon, you’ll be driving toward a brighter financial future.