Navigating the Road Ahead: Your Expert Guide to Getting a Car Loan with Little Credit History

Navigating the Road Ahead: Your Expert Guide to Getting a Car Loan with Little Credit History Carloan.Guidemechanic.com

Getting your first car is an exciting milestone, a symbol of independence and new possibilities. But for many, especially those just starting out, the path to auto loan approval can seem daunting, particularly when faced with a limited or non-existent credit history. Lenders often rely on a robust credit profile to assess risk, making it a common hurdle for first-time buyers or recent graduates.

Based on my extensive experience in personal finance and automotive lending, I can assure you that securing a car loan with little credit history is absolutely achievable. It requires a strategic approach, a clear understanding of the lending landscape, and a commitment to responsible financial planning. This comprehensive guide will walk you through every step, offering actionable advice and insights to help you drive away in your new vehicle.

Navigating the Road Ahead: Your Expert Guide to Getting a Car Loan with Little Credit History

Understanding the Credit Landscape: Why Lenders Care So Much

Before diving into strategies, it’s crucial to understand why lenders place such emphasis on your credit history. Your credit report and score are essentially your financial resume. They tell lenders how reliably you’ve managed past debts, indicating your likelihood of repaying a new loan.

When you have little to no credit history, lenders view you as an unknown quantity. They lack the data points—like previous loan payments, credit card usage, or account longevity—to confidently assess your risk. This doesn’t mean you’re a bad borrower; it simply means you haven’t had the opportunity to prove yourself yet. Our goal here is to bridge that gap and present yourself as a low-risk applicant, even with a blank slate.

Laying the Foundation: Preparing for Your Car Loan Journey

Success in securing a car loan with limited credit begins long before you even step foot in a dealership or bank. Thorough preparation is your most powerful tool.

Know Your Financial Limits: Crafting a Realistic Budget

One of the most common mistakes aspiring car owners make is not having a clear, realistic budget. Before you even think about car models, sit down and map out your finances. How much can you truly afford each month for a car payment, insurance, fuel, and maintenance?

Pro tips from us: Factor in all potential costs, not just the monthly loan payment. Insurance premiums for new drivers can be surprisingly high, and maintenance, while less frequent for newer cars, is still a vital consideration. Overestimating your affordability can lead to financial strain down the road.

The Power of a Down Payment: Your First Impression

A significant down payment is perhaps the single most impactful step you can take when applying for a car loan with little credit. When you put down a substantial sum, you reduce the amount you need to borrow, which in turn lowers the lender’s risk.

A larger down payment also shows financial responsibility and commitment. It signals to the lender that you are serious about this purchase and have the discipline to save. Aim for at least 10-20% of the car’s purchase price if possible. Even a smaller down payment is better than none.

Gathering Your Documents: Be Prepared

Lenders will require various documents to verify your identity, income, and residence. Having these ready in advance demonstrates organization and can expedite the application process.

Common documents include:

- Government-issued identification (driver’s license, passport).

- Proof of income (recent pay stubs, tax returns if self-employed, employment verification letter).

- Proof of residence (utility bill, lease agreement).

- Bank statements.

Having these prepared helps present you as a responsible and organized individual, making the lender’s job easier and your application smoother.

Researching Car Options: Realistic Choices

With little credit, your first car might not be your dream car. Focus on reliable, affordable vehicles that fit your budget. Lenders are more likely to approve loans for less expensive cars, as the loan amount is smaller and the risk is reduced.

Consider certified pre-owned (CPO) vehicles, which offer a good balance of reliability and value. They typically come with warranties and have undergone thorough inspections, providing peace of mind.

Strategic Approaches: How to Get Approved

Now, let’s explore the specific strategies you can employ to strengthen your car loan application when your credit history is thin.

1. The Co-Signer Advantage: Sharing the Responsibility

One of the most effective ways to secure a car loan with little credit is to apply with a co-signer. A co-signer is someone with a strong credit history who agrees to be equally responsible for the loan. If you fail to make payments, the co-signer is obligated to pay.

Benefits of a Co-Signer:

- Increased Approval Odds: The lender views the loan as less risky because there’s a financially stable individual backing it.

- Potentially Better Terms: You might qualify for a lower interest rate than you would on your own, saving you money over the life of the loan.

- Credit Building Opportunity: Making on-time payments will positively impact both your credit and your co-signer’s.

Choosing a Co-Signer:

A co-signer should be someone you trust implicitly and who trusts you. This is often a parent, guardian, or close family member with excellent credit. Ensure both parties fully understand the responsibilities and risks involved. Common mistakes to avoid are choosing someone who isn’t financially stable or not having a clear agreement about payment responsibilities.

2. Dealership Financing vs. Bank/Credit Union Loans: Exploring Your Options

Where you apply for your loan can significantly impact your chances of approval.

Banks and Credit Unions:

These institutions often offer competitive interest rates and a range of loan products. However, they typically have stricter credit requirements. If you have an existing relationship with a bank or credit union (e.g., a checking or savings account), they might be more willing to work with you. It’s always a good idea to check with them first.

Dealership Financing:

Many dealerships offer in-house financing or work with a network of lenders. They often have programs specifically designed for first-time buyers or those with limited credit. These loans might come with slightly higher interest rates, but they can be a viable path to approval. Some dealerships also offer "subprime" lending, which caters to higher-risk borrowers.

- "Buy Here, Pay Here" Dealerships: These are direct lenders who finance the car themselves. While they are often a last resort for those with very poor credit, they typically come with much higher interest rates and less favorable terms. Based on my experience, it’s generally best to exhaust other options before considering "Buy Here, Pay Here" lots, as they can be very costly in the long run.

3. Building Your Credit Proactively: Small Steps, Big Impact

If you have some time before you absolutely need a car, consider taking steps to build a thin credit file. Even a few months of responsible credit use can make a difference.

- Secured Credit Card: This type of credit card requires a cash deposit, which acts as your credit limit. Use it for small, regular purchases and pay the balance in full each month. This demonstrates responsible credit behavior to credit bureaus.

- Small Personal Loan: Some credit unions offer "credit-builder" loans designed to help individuals establish credit. The loan amount is typically held in a savings account until you’ve made all your payments, after which the funds are released to you.

- Become an Authorized User: If a trusted family member with excellent credit adds you as an authorized user on one of their credit cards, their positive payment history can sometimes appear on your credit report, helping to establish your own. Ensure they are a responsible credit user.

4. Start Small: Consider a Less Expensive Vehicle

As mentioned earlier, opting for a more affordable car significantly reduces the risk for the lender. A $10,000 loan is much less of a commitment than a $30,000 loan. This can increase your chances of approval and give you an opportunity to build a positive payment history.

Once you’ve established a good credit history with your first car loan, upgrading to your dream car later will be much easier and likely come with better interest rates.

5. Be Prepared for Higher Interest Rates

With little credit history, lenders view you as a higher risk. This often translates to a higher interest rate on your loan. While it might be frustrating, understand that this is the cost of borrowing when you haven’t yet proven your creditworthiness.

Focus on getting approved and making your payments consistently. After a year or two of on-time payments, you might be able to refinance your loan at a lower interest rate. This is a common strategy for building credit and reducing overall costs.

The Application Process: Navigating the Details

Once you’ve done your homework and chosen your strategy, it’s time to apply.

Filling Out the Application Accurately

Provide accurate and complete information on your loan application. Any discrepancies can raise red flags and delay or even deny your application. Be honest about your income, employment history, and residence.

What Lenders Look For (Beyond Just Credit Score)

While credit history is crucial, lenders also consider other factors, especially for applicants with limited credit:

- Stable Income: Consistent employment and a reliable income source are key indicators of your ability to repay.

- Debt-to-Income Ratio: Lenders will look at how much of your monthly income goes towards existing debt payments. A lower ratio is always better.

- Length of Employment/Residency: Stability in your job and living situation suggests reliability.

- Banking Relationship: If you have an established checking or savings account with the lending institution, it can work in your favor.

Negotiating Terms: Don’t Be Afraid to Ask

Even with limited credit, there might be some room for negotiation, particularly regarding the down payment or the loan term. If you have multiple offers, use them to your advantage.

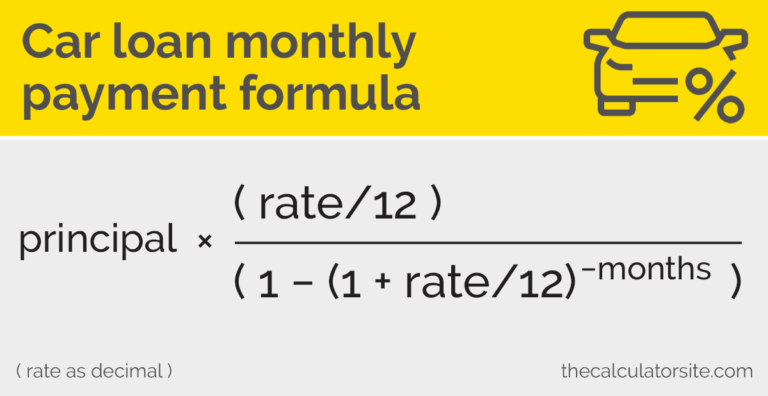

Understand the total cost of the loan. Focus on the overall interest paid over the life of the loan, not just the monthly payment. A longer loan term (e.g., 72 months) might result in lower monthly payments but significantly higher interest paid overall. Pro tips from us: Aim for the shortest loan term you can comfortably afford to minimize interest charges.

Understanding the Fine Print

Before signing any documents, read the loan agreement thoroughly. Understand all the terms and conditions, including:

- The annual percentage rate (APR).

- The total amount financed.

- The total cost of the loan (principal + interest).

- Any fees or penalties for late payments or early payoff.

- The loan term.

If anything is unclear, ask questions until you fully understand. This is a legally binding contract, and it’s essential to be fully informed.

Post-Approval: Building Your Credit for the Future

Congratulations! You’ve secured your car loan. Now, the real work begins: using this opportunity to build a strong credit history for your financial future.

Make Payments On Time, Every Time

This is the most critical step. Your car loan is a significant tradeline on your credit report. Each on-time payment contributes positively to your credit score.

Consider setting up automatic payments from your checking account to avoid missing due dates. Even a single late payment can significantly damage your newly forming credit history.

Monitor Your Credit Report

Regularly check your credit report (you can get a free report annually from each of the three major credit bureaus: Experian, Equifax, and TransUnion via AnnualCreditReport.com). Ensure all information is accurate and that your car loan payments are being reported correctly. This helps you catch any errors and track your progress. External Link: Learn more about getting your free credit report at AnnualCreditReport.com

Responsible Borrowing Habits

Your car loan is just the beginning. As your credit grows, continue to practice responsible borrowing habits. Avoid taking on too much debt, keep credit utilization low on any credit cards, and always pay bills on time. This foundation will serve you well for future financial endeavors, from buying a home to securing personal loans.

Common Mistakes to Avoid When Seeking a Car Loan with Little Credit

Based on my experience, there are several pitfalls new borrowers often encounter:

- Applying Everywhere: Each loan application can result in a "hard inquiry" on your credit report. Too many hard inquiries in a short period can negatively impact your score. Group your applications within a 14-45 day window to have them count as a single inquiry for credit scoring models.

- Not Knowing Your Budget: As discussed, overestimating what you can afford leads to financial stress and potential default.

- Ignoring the Total Cost of Ownership: Beyond the loan payment, remember insurance, fuel, maintenance, and registration. These can add hundreds of dollars to your monthly expenses.

- Skipping the Test Drive and Inspection: Don’t get so caught up in the financing that you forget to thoroughly vet the car itself. A reliable vehicle saves you money on repairs.

- Not Reading the Loan Agreement: Never sign something you don’t fully understand. Ask questions!

Final Thoughts: Your Path to Automotive Independence

Getting a car loan with little credit history might seem like an uphill battle, but with careful planning, strategic execution, and a commitment to financial responsibility, it’s a perfectly achievable goal. Remember, this first loan is not just about getting a car; it’s about establishing a positive financial track record that will open doors to greater opportunities in the future.

By understanding the lending process, leveraging strategies like a co-signer or a strong down payment, and diligently making your payments, you’ll not only drive away in your new vehicle but also build the credit foundation necessary for a secure financial future. Your journey starts here, and with this guide, you’re well-equipped to navigate it successfully.