Navigating the Road Ahead: Your Expert Guide to Getting a Car Loan with Poor Credit

Navigating the Road Ahead: Your Expert Guide to Getting a Car Loan with Poor Credit Carloan.Guidemechanic.com

Securing a car loan can feel like an uphill battle, especially when your credit score isn’t where you want it to be. Many people believe that poor credit automatically slams the door shut on vehicle ownership. However, based on my extensive experience in the financial and automotive sectors, I can tell you this isn’t necessarily true. While it presents unique challenges, getting a car loan with poor credit is absolutely possible with the right strategy and preparation.

This comprehensive guide is designed to empower you with the knowledge, strategies, and confidence needed to navigate the car loan landscape, even with a less-than-perfect credit history. We’ll dive deep into understanding your credit, preparing for the application, finding the right lenders, and ultimately, driving away in your new (or new-to-you) car. Let’s hit the road!

Navigating the Road Ahead: Your Expert Guide to Getting a Car Loan with Poor Credit

Understanding Poor Credit and Its Real Impact on Car Loans

Before we explore solutions, it’s crucial to understand what "poor credit" means in the eyes of a lender and why it matters. Your credit score is essentially a numerical representation of your creditworthiness, indicating how likely you are to repay borrowed money.

What Defines "Poor Credit"?

Credit scores, like FICO and VantageScore, typically range from 300 to 850. While the exact cutoffs can vary slightly between scoring models and lenders, a score generally below 600-620 is often considered "poor" or "subprime." This range signals a higher risk to lenders, primarily because it suggests a history of missed payments, high debt utilization, or other financial challenges.

Lenders use this score, alongside your credit report, to assess the risk of lending to you. A lower score translates to a higher perceived risk. This doesn’t mean you’re a bad person; it simply means lenders will approach your application with more caution.

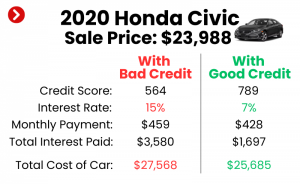

The Real Impact: Higher Costs and Specific Terms

The primary consequence of poor credit on a car loan is typically a higher interest rate. Lenders compensate for the increased risk by charging more for the money they lend. This can significantly increase the total cost of your vehicle over the life of the loan.

Furthermore, you might encounter less favorable loan terms, such as shorter repayment periods (leading to higher monthly payments) or a requirement for a larger down payment. Understanding these realities upfront will help you set realistic expectations and prepare effectively. It’s not about finding a "no credit check" loan, which are often predatory, but about finding legitimate lenders willing to work with your current financial standing.

Laying the Groundwork: Essential Preparation Before You Apply

Preparation is your most powerful tool when seeking a car loan with poor credit. Approaching lenders armed with knowledge and a clear plan dramatically increases your chances of approval and helps you secure better terms.

Step 1: Know Your Credit Score and Report Inside Out

This is the absolute first step. You cannot begin to address your credit situation without knowing exactly what’s on your credit report. It’s like trying to navigate a new city without a map.

- Why it’s crucial: Your credit report details your borrowing history, payment patterns, and any public records like bankruptcies. Lenders will pull this exact report.

- How to get it: You are entitled to a free copy of your credit report from each of the three major bureaus (Experian, Equifax, and TransUnion) once every 12 months. Visit AnnualCreditReport.com to access yours. This is the only authorized website for free reports.

- What to look for: Scrutinize every detail for inaccuracies. Errors can negatively impact your score. If you find mistakes, dispute them immediately with the relevant credit bureau. Even a small correction could boost your score slightly.

- Understand negative marks: Identify what’s contributing to your low score. Is it a history of late payments, high credit card balances, or collections? Knowing the root cause helps you explain your situation to lenders and demonstrates awareness.

Based on my experience, many individuals are surprised by what they find on their credit report. Sometimes, a simple error correction can make a meaningful difference.

Step 2: Craft a Realistic Budget (Beyond Just the Car Payment)

A car loan is just one piece of the puzzle. Owning a car involves numerous ongoing expenses that you must factor into your budget. Lenders want to see that you can afford the entire financial commitment, not just the monthly loan payment.

- Calculate all costs: This includes car insurance (which can be higher for newer cars or for drivers with a history of claims), fuel, maintenance, registration fees, and potential repair costs.

- Determine your affordability: Use a budget planner to understand how much you can truly afford each month for total car-related expenses without stretching yourself too thin. Remember, missing future car payments will only worsen your credit.

- Pro tips from us: Aim for a total car expense (loan payment + insurance + fuel + maintenance savings) that doesn’t exceed 10-15% of your net monthly income. For a deeper dive into budgeting, you might find our article on Budgeting for Your First Car: What You Need to Know (Internal Link) particularly helpful.

Step 3: Save for a Significant Down Payment

A substantial down payment is one of the most effective ways to offset poor credit. It reduces the amount you need to borrow, which in turn lowers the lender’s risk.

- Why it helps:

- Reduces loan amount: Less money borrowed means lower monthly payments and less interest paid over time.

- Shows commitment: A large down payment demonstrates to lenders that you are serious about your purchase and have a financial stake in the vehicle.

- Increases approval odds: With less risk involved, lenders are more likely to approve your application, even with a lower credit score.

- How much is enough? While 10-20% of the car’s value is often recommended, with poor credit, aiming for 25% or more can significantly improve your chances and terms. Every dollar you put down is a dollar you don’t have to borrow and pay interest on.

Step 4: Consider a Co-signer (With Caution)

If you have a trusted friend or family member with good credit, asking them to co-sign your loan can be a game-changer. A co-signer essentially guarantees the loan, promising to make payments if you default.

- Benefits:

- Higher approval chances: The lender sees the co-signer’s good credit as a backup, reducing their risk.

- Potentially better terms: You might qualify for a lower interest rate than you would on your own.

- Risks:

- Impact on co-signer’s credit: If you miss payments, it negatively affects both your credit scores.

- Financial responsibility: The co-signer is legally obligated to repay the loan if you don’t. This is a serious commitment that can strain relationships if not handled responsibly.

- Common mistakes to avoid are: Co-signing without fully understanding the implications for both parties. Always have a clear, honest conversation about responsibilities and potential scenarios.

Step 5: Be Realistic About Your Vehicle Choice

With poor credit, your options for luxury or brand-new vehicles might be limited. Focus on reliability, affordability, and practical needs rather than wants.

- Prioritize a dependable used car: A less expensive, reliable used car will be easier to finance and keep insured. It also allows you to make consistent payments, which will start to rebuild your credit.

- Avoid overspending: Don’t let the excitement of a new car push you into a loan you can’t comfortably afford. Remember the total cost of ownership.

Navigating the Loan Application Process with Poor Credit

Once you’ve done your homework and prepared financially, it’s time to approach lenders. This phase requires strategic thinking and careful consideration of your options.

Step 1: Research and Target Subprime Lenders

Not all lenders are created equal, especially when it comes to poor credit. Traditional banks often have stricter lending criteria. Instead, focus your initial search on lenders specializing in "subprime" auto loans.

- What are subprime lenders? These are financial institutions, including certain banks, credit unions, and finance companies, that are more willing to lend to individuals with lower credit scores. They understand the challenges and structure their loans accordingly, though often with higher interest rates.

- Where to find them:

- Online auto loan marketplaces: Many online platforms connect borrowers with a network of lenders, including subprime specialists.

- Credit unions: Often more flexible and community-focused than large banks, credit unions may offer better rates and terms even for those with poor credit.

- Dealerships with special finance departments: Many larger dealerships have departments specifically designed to help customers with challenging credit histories.

- Pro tips from us: Avoid applying to too many lenders at once. Each hard inquiry can temporarily ding your credit score. Try to consolidate your applications within a short timeframe (usually 14-45 days), as credit bureaus often group these inquiries as a single event for rate shopping.

Step 2: Get Pre-Approved for a Loan

Pre-approval is a powerful tool. It means a lender has provisionally agreed to lend you a certain amount of money at a specific interest rate, before you even pick out a car.

- Benefits:

- Know your budget: You’ll walk into the dealership knowing exactly how much you can spend, acting like a cash buyer.

- Negotiating power: With pre-approval in hand, you can negotiate the car’s price based on its value, rather than being pressured into a payment plan that might not be ideal.

- Saves time: Streamlines the car-buying process at the dealership.

- Less stress: Reduces the anxiety of not knowing if you’ll be approved.

- What to expect: Pre-approval usually involves a "soft" credit pull initially, which doesn’t affect your score. A "hard" pull will occur when you finalize the loan.

Step 3: Explore Dealership Financing vs. Direct Lenders

You have two main avenues for financing: getting a loan directly from a bank or credit union (direct lending) or using the financing options offered by the car dealership.

- Direct Lenders (Banks, Credit Unions):

- Pros: Often offer competitive rates, especially credit unions. You have a loan in hand before car shopping.

- Cons: Might have stricter eligibility for poor credit.

- Dealership Financing:

- Pros: Convenient, as they handle the paperwork. They work with multiple lenders (including subprime ones) and might find a deal you couldn’t on your own.

- Cons: May mark up interest rates to earn a profit. Can sometimes feel pressured to accept less favorable terms.

- Based on my experience: It’s always best to secure a pre-approval from a direct lender before visiting a dealership. This gives you a benchmark. If the dealership can beat your pre-approved rate, great! If not, you have a solid backup.

Step 4: Understand Secured Car Loans

A secured car loan means the car itself serves as collateral for the loan. This is the standard for most auto loans. If you default on payments, the lender can repossess the vehicle.

- Why it’s relevant for poor credit: Because the loan is secured by an asset, lenders perceive less risk, making them more willing to approve borrowers with poor credit. This is generally a better option than unsecured personal loans for car purchases, which typically have even higher interest rates for bad credit.

Step 5: Exercise Caution with "Buy Here, Pay Here" Dealerships

"Buy Here, Pay Here" (BHPH) dealerships offer in-house financing, meaning they are both the seller and the lender. While they often advertise "guaranteed approval," they come with significant drawbacks.

- Risks:

- Exorbitant interest rates: Often the highest rates in the industry, sometimes bordering on predatory.

- Limited vehicle selection: Usually older, higher-mileage vehicles that may have hidden issues.

- Less reporting to credit bureaus: Some BHPH dealers do not report consistent payment history to all three major credit bureaus, hindering your credit rebuilding efforts.

- Aggressive repossession policies: They often have quick trigger fingers when it comes to repossession.

- Pro tips from us: While BHPH might seem like the only option, it should be a last resort. Exhaust all other avenues first. If you must use one, ensure they report to all three major credit bureaus and thoroughly inspect the vehicle with an independent mechanic.

Strategies to Improve Your Chances and Loan Terms

Beyond finding the right lender, there are specific actions you can take during the application and negotiation process to further your cause.

Demonstrate Stability and Responsibility

Lenders want to see a history of stability, even if your credit score is low.

- Proof of Income: Provide documentation of steady employment and sufficient income to cover the loan. Pay stubs, tax returns, and bank statements are crucial.

- Proof of Residency: Stable residency indicates reliability. Utility bills or a lease agreement can serve as proof.

- Low Debt-to-Income Ratio (DTI): If possible, try to pay down other debts before applying. A lower DTI shows you have more disposable income to put towards a car loan.

- Explain your situation: Don’t be afraid to briefly and honestly explain past credit issues (e.g., job loss, medical emergency). Lenders are more understanding if they see you’re now on a stable path.

Be a Savvy Negotiator

Negotiating a car loan with poor credit requires focus. Don’t get fixated solely on the monthly payment.

- Negotiate the car price first: Get the best possible price on the vehicle itself before discussing financing. This ensures you’re not paying more for the car just to get a lower monthly payment by extending the loan term.

- Understand the total cost: Pay attention to the interest rate, the loan term (number of months), and any fees. A lower monthly payment over a longer term often means you pay significantly more in interest overall.

- Common mistakes to avoid are: Letting a salesperson rush you through the finance office. Take your time, ask questions, and don’t sign anything you don’t fully understand.

Read the Fine Print Meticulously

Every loan agreement has terms and conditions that you must understand.

- Interest rates: Confirm the Annual Percentage Rate (APR), which includes the interest rate and other loan fees.

- Prepayment penalties: Some loans charge a fee if you pay off the loan early. This can be important if you plan to refinance later.

- Late fees: Know the charges for missed or late payments.

- Loan term: Be clear on how many months you’ll be making payments.

Post-Loan Approval: Rebuilding Your Credit for a Brighter Future

Getting the car loan is a victory, but it’s also an opportunity. This is your chance to turn your credit around and set yourself up for better financial opportunities down the road.

Make Every Payment On Time, Every Time

This is the single most important action you can take. Payment history accounts for 35% of your FICO score.

- Set up reminders: Use calendar alerts, automatic payments, or a budgeting app to ensure you never miss a due date.

- Pay slightly more than the minimum: If you can afford it, even an extra $10-20 each month can reduce the principal faster, save on interest, and shorten your loan term.

- Pro tips from us: If you anticipate difficulty making a payment, contact your lender immediately. They may be able to offer options like a deferral, which is better than a missed payment.

Keep Your Other Accounts in Good Standing

While focusing on your car loan, don’t neglect your other financial obligations. Continue to pay all credit card bills, utility bills, and other loans on time.

- Reduce credit card debt: High credit utilization (how much credit you’re using compared to your available credit limit) negatively impacts your score. Aim to keep balances below 30% of your limit, ideally even lower.

Regularly Monitor Your Credit Report

Continue to check your credit report annually for accuracy. As you make on-time payments, you should see your score gradually improve.

- Celebrate progress: Watching your credit score rise is incredibly motivating and confirms your efforts are paying off. For more detailed insights, you might find our article on Understanding Your Credit Score: A Beginner’s Guide (Internal Link) quite beneficial.

Avoid Taking on New Debt Unnecessarily

During the period of rebuilding your credit, try to avoid opening new credit accounts or taking on additional loans. Focus on demonstrating responsible management of your current debt.

- Stability is key: Lenders prefer to see a consistent payment history on existing accounts rather than a flurry of new credit inquiries.

Concluding Thoughts: Your Path to a Car Loan with Poor Credit is Clear

Getting a car loan with poor credit might seem daunting at first, but with a strategic approach, thorough preparation, and a commitment to responsible financial habits, it is entirely achievable. Remember, this isn’t just about getting a car; it’s about taking a crucial step towards rebuilding your financial future.

Start by understanding your credit, prepare a solid budget, save for a down payment, and explore all your lending options. Be honest, diligent, and patient. By following the advice outlined in this guide, you can confidently navigate the process, secure the vehicle you need, and begin a positive journey towards improved credit health. Don’t let your past credit define your future mobility. Start preparing today, and soon, you’ll be driving towards a brighter financial horizon.