Navigating the Road Ahead: Your Expert Guide to Getting a Small Car Loan with Bad Credit

Navigating the Road Ahead: Your Expert Guide to Getting a Small Car Loan with Bad Credit Carloan.Guidemechanic.com

Embarking on the journey to purchase a car can be exciting, but for many, the path is often complicated by a less-than-perfect credit score. If you’re wondering how to get a small car loan with bad credit, you’re not alone. Millions of individuals face this challenge, and the good news is, it’s absolutely possible to secure the financing you need, especially for a more affordable vehicle.

As an expert in auto financing and credit, I understand the frustrations and anxieties that come with a low credit score. Based on my experience, while it requires a strategic approach and a bit more legwork, finding a suitable loan for a small car is within reach. This comprehensive guide will walk you through every step, offering actionable advice and pro tips to help you drive away in your new-to-you car.

Navigating the Road Ahead: Your Expert Guide to Getting a Small Car Loan with Bad Credit

Understanding Bad Credit and Its Impact on Car Loans

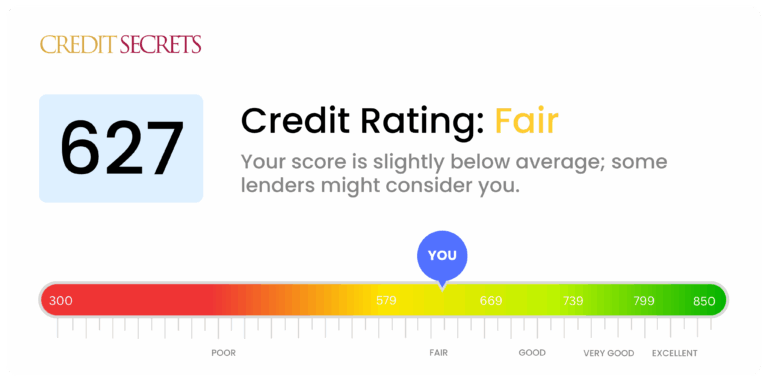

Before diving into solutions, it’s crucial to understand what "bad credit" means in the eyes of a lender and why it poses a challenge. Generally, a FICO score below 600-620 is considered "subprime" or "bad credit." This range signals to lenders that there might be a higher risk of you defaulting on your payments.

Lenders use your credit score as a primary indicator of your financial reliability. A lower score suggests a history of missed payments, high debt, or even bankruptcy, making them more hesitant to approve a loan. However, the exact definition can vary slightly between different financial institutions.

The good news is that the risk associated with lending for a small car is often lower for the lender. A smaller loan amount means less capital at stake, which can make them more willing to consider applicants with bad credit. This is a key advantage to keep in mind throughout your search.

Step 1: Know Your Credit Score and Understand Your Report

The very first step on your journey is to face your credit head-on. You cannot effectively seek a loan if you don’t know where you stand. Obtaining your credit score and a full copy of your credit report is paramount.

You are legally entitled to a free copy of your credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) once every 12 months. Visit AnnualCreditReport.com – it’s the only truly free and authorized source. Reviewing your report allows you to see exactly what lenders see.

Pro tips from us: Carefully scrutinize every entry on your report. Look for any inaccuracies or errors, such as accounts that aren’t yours, incorrect payment statuses, or outdated information. Even a small error can negatively impact your score and approval chances. Disputing these errors promptly can often lead to a quick bump in your score.

Step 2: Assess Your Financial Reality and Create a Realistic Budget

Before you even think about looking at cars, you need to understand what you can genuinely afford. This goes beyond just the monthly car payment. Consider insurance, fuel, maintenance, and potential repair costs for a used vehicle.

Create a detailed budget that outlines all your income and expenses. This will help you determine a comfortable monthly car payment that won’t strain your finances. Remember, missing future payments will only worsen your credit.

Based on my experience: Many people make the mistake of focusing solely on the monthly payment without considering the total cost of the loan over its lifetime. A smaller, more affordable car naturally leads to a smaller loan amount, which is much more manageable with bad credit. This also signals to lenders that you are being responsible.

Step 3: Strategically Improve Your Credit Score (Even Slightly)

While a complete credit overhaul takes time, there are immediate steps you can take to make your profile more appealing to lenders. Even a slight improvement can lead to better loan terms.

Start by paying all your bills on time, every time. Payment history is the most significant factor in your credit score. If you have any outstanding small debts, like medical bills or old credit card balances, try to pay them down or settle them. Reducing your credit utilization (the amount of credit you’re using compared to your total available credit) can also provide a quick boost.

For more in-depth strategies on repairing your credit, you might want to explore our detailed guide on credit repair strategies on our blog (Internal Link). Every point counts when you’re seeking a loan with bad credit.

Step 4: Gather All Necessary Documents

Being prepared can significantly streamline the application process and show lenders you are serious and organized. Before you even speak to a lender, compile all the documents they are likely to request.

This typically includes proof of income (pay stubs, tax returns if self-employed), proof of residency (utility bills, lease agreement), a valid driver’s license, and references. Some lenders might also ask for bank statements or a list of your monthly expenses.

Having everything readily available demonstrates responsibility and expedites the approval process. It also reduces the back-and-forth, making the experience less stressful for you.

Step 5: Explore Your Loan Options for Bad Credit Car Loans

This is where your strategic approach truly comes into play. Not all lenders are created equal when it comes to bad credit. You need to know where to look and what to expect.

A. Dealership Financing (Specializing in Subprime Loans)

Many dealerships work with a network of lenders, some of whom specialize in subprime auto loans. These dealerships are often more accustomed to dealing with challenging credit situations.

- "Buy Here, Pay Here" Dealerships: These dealerships act as both the seller and the lender. They can be a viable option if other avenues fail, as they often have very lenient credit requirements. However, common mistakes to avoid include high interest rates, limited car selection, and sometimes less transparent terms. Always read the fine print carefully.

- Traditional Dealerships with Subprime Lenders: Many larger dealerships have finance departments that partner with various banks and finance companies, including those that cater to bad credit borrowers. They can often shop your application around to find you the best possible rate among their partners. This is often a better option than "Buy Here, Pay Here" if available.

B. Banks and Credit Unions

While often more challenging for bad credit borrowers, don’t dismiss traditional banks and credit unions entirely.

- Credit Unions: These member-owned financial institutions are often more flexible and willing to work with members who have less-than-perfect credit, especially if you have an existing relationship with them. They may offer more favorable interest rates than subprime lenders.

- Banks: If you have an existing checking or savings account with a bank, they might be more inclined to offer you a loan, even with bad credit. It’s always worth applying, but be prepared for potentially stricter criteria. Applying for pre-approval can give you an idea of their willingness without multiple hard inquiries impacting your score.

C. Online Lenders Specializing in Bad Credit

The digital age has brought forth a host of online lenders who specifically cater to individuals with bad credit. These platforms often have streamlined application processes and quick approval times.

- Pros: Convenience, quick decisions, and often a higher likelihood of approval compared to traditional banks. They might also offer competitive rates for bad credit borrowers.

- Cons: You need to be diligent in researching their reputation. Look for lenders with positive reviews and transparent terms. Some online lenders may have higher interest rates than credit unions.

D. Finding a Co-signer

If you have a trusted friend or family member with good credit who is willing to co-sign your loan, this can significantly improve your chances of approval and secure a better interest rate.

- Pros: A co-signer essentially guarantees the loan, making it much less risky for the lender. This can open doors to more conventional lenders and lower interest rates.

- Cons: The co-signer is equally responsible for the loan. If you miss payments, their credit score will be negatively affected, and they could be liable for the debt. This decision should never be taken lightly, as it impacts a personal relationship.

Based on my experience: A co-signer can be a powerful tool, but it’s crucial to have an open and honest conversation with them about the responsibilities and potential risks involved. Ensure you are absolutely confident in your ability to make all payments on time.

Step 6: The Application Process and Negotiation Strategies

Once you’ve identified potential lenders, it’s time to apply and negotiate. Don’t simply accept the first offer you receive. Shopping around is key.

Start by applying for pre-approval from a few different lenders. Pre-approvals usually involve a "soft inquiry" on your credit, which doesn’t hurt your score. This gives you an idea of the loan amount and interest rate you might qualify for.

When you’re ready to apply, consolidate your applications within a short timeframe (usually 14-45 days). Multiple inquiries for the same type of loan within this window are typically treated as a single inquiry by credit bureaus, minimizing the impact on your score.

Pro tips from us: Always negotiate! Don’t be afraid to ask for a lower interest rate, a shorter loan term (if it fits your budget), or fewer fees. Focus on the total cost of the loan, not just the monthly payment. A lower interest rate over a shorter term can save you thousands.

Common mistakes to avoid are: accepting a loan with an excessively long term (e.g., 72 or 84 months) just to get a low monthly payment. While it seems appealing, you’ll pay significantly more in interest over the life of the loan and your car will depreciate faster than you pay it off, leading to negative equity.

Step 7: Choose the Right Small Car

The type of car you choose is incredibly important when dealing with bad credit. Opting for a "small car" is not just about preference; it’s a strategic financial move.

A smaller, more affordable vehicle means you’ll be seeking a lower loan amount. This reduces the risk for the lender, making them more likely to approve your application. It also makes your monthly payments more manageable, increasing your chances of successfully paying off the loan.

Consider reliable, fuel-efficient used cars rather than brand-new models. Used cars have already taken the steepest depreciation hit, and their lower price point aligns perfectly with your goal of securing a small car loan with bad credit. Focus on models known for their longevity and low maintenance costs to avoid unexpected expenses down the line.

Pro Tips for Maximizing Your Approval Chances

Here are some additional insights to bolster your application:

- Be Realistic: Understand that with bad credit, your interest rates will likely be higher than someone with excellent credit. Focus on getting approved for a reliable car you can afford, and plan to refinance later.

- Offer a Down Payment: Even a small down payment can make a significant difference. It reduces the amount you need to borrow, shows the lender your commitment, and reduces their risk. The more you put down, the better your chances and potentially your terms.

- Don’t Lie on Your Application: Transparency is crucial. Providing false information can lead to immediate denial and potentially legal trouble. Be honest about your financial situation.

- Understand All Fees: Beyond the interest rate, be aware of any origination fees, documentation fees, or prepayment penalties. Read the loan agreement thoroughly before signing. For more information on understanding loan terms, you can refer to reputable sources like the Consumer Financial Protection Bureau’s auto loan guide (External Link).

After Approval: Rebuilding Your Credit with Your New Loan

Congratulations, you’ve secured your small car loan with bad credit! This is not just about getting a car; it’s a golden opportunity to rebuild your credit score.

Making consistent, on-time payments on your auto loan is one of the most effective ways to improve your credit. Each on-time payment demonstrates financial responsibility to the credit bureaus. Over time, as your payment history improves, your credit score will gradually increase.

Once your credit score has significantly improved (typically after 12-24 months of on-time payments), you might be eligible to refinance your car loan at a lower interest rate. This can save you a substantial amount of money over the remaining life of the loan. To learn more about how a car loan impacts your credit and strategies for improvement, check out our article on leveraging loans for credit building (Internal Link).

Drive Away with Confidence

Getting a small car loan with bad credit may seem like an uphill battle, but it’s a challenge that can be overcome with the right knowledge and strategy. By understanding your credit, budgeting wisely, exploring all your financing options, and negotiating effectively, you can secure the transportation you need.

Remember, this isn’t just about a car; it’s about taking control of your financial future. Use this opportunity to make consistent payments, improve your credit score, and open doors to better financial opportunities down the road. Your journey to a reliable small car starts now, and with these steps, you’re well-equipped to navigate it successfully.