Navigating the Road Ahead: Your Expert Guide to Getting the Best Car Loan After Chapter 7 Discharge

Navigating the Road Ahead: Your Expert Guide to Getting the Best Car Loan After Chapter 7 Discharge Carloan.Guidemechanic.com

The dust has settled. Your Chapter 7 bankruptcy has been discharged, and a significant weight has lifted. This marks a fresh start, a clean slate, and an opportunity to rebuild your financial life. However, a common question arises for many in your shoes: "How do I get a car loan after Chapter 7 discharge, and can I even get a good one?"

The answer is a resounding yes! Securing a car loan after bankruptcy is not only possible but often a crucial step in rebuilding your credit and regaining financial independence. It might seem daunting, and some lenders may initially be hesitant, but with the right knowledge, preparation, and strategy, you can absolutely drive away in a reliable vehicle with manageable terms.

Navigating the Road Ahead: Your Expert Guide to Getting the Best Car Loan After Chapter 7 Discharge

This comprehensive guide is designed to empower you with the insights and strategies needed to navigate the post-bankruptcy auto loan landscape successfully. We’ll delve deep into understanding the process, preparing your finances, finding the right lenders, and ultimately securing the best car loan after Chapter 7 discharge for your unique situation.

Understanding Chapter 7 Discharge and Its Credit Impact

Before we dive into loan applications, let’s clarify what a Chapter 7 discharge truly means for your financial standing. A Chapter 7 bankruptcy, often referred to as "liquidation bankruptcy," wipes out most of your unsecured debts, providing you with a fresh start. This discharge legally releases you from the obligation to pay those debts.

While the discharge itself is a huge relief, the bankruptcy filing will remain on your credit report for up to 10 years. Initially, it causes a significant drop in your credit score, as it indicates a past inability to repay debts. Lenders will see this mark, and it often places you in the "subprime" category.

However, based on my experience, this initial credit score drop is not the end of your financial journey. In fact, for many, the period immediately after discharge presents a unique opportunity. With most debts eliminated, your debt-to-income ratio often improves dramatically, and you’re no longer burdened by overwhelming payments. This can make you a more attractive borrower to certain lenders who specialize in post-bankruptcy financing, as you have less existing debt to compete with new obligations.

The New You: Rebuilding Your Financial Foundation

The period immediately following your Chapter 7 discharge is critical for laying a strong financial foundation. Think of it as a reset button; you now have the chance to build positive credit habits from scratch. This proactive approach will significantly improve your chances of securing a favorable car loan.

One of the most effective strategies is to establish new lines of credit and manage them responsibly. Secured credit cards are an excellent starting point. You deposit money into an account, and that amount becomes your credit limit. Using these cards for small, regular purchases and paying the balance in full and on time each month demonstrates your ability to handle credit responsibly.

Another smart move is to consider a credit builder loan from a credit union or community bank. With these loans, the money is held in a savings account while you make regular payments. Once the loan is paid off, you receive the funds, and your consistent payments are reported to credit bureaus, positively impacting your score. Additionally, ensure all your current bills, like rent, utilities, and cell phone payments, are paid on time, as some services now report payment history to credit bureaus. Regularly monitoring your credit reports for accuracy is also crucial during this rebuilding phase.

When to Apply for a Car Loan After Chapter 7

Patience is a virtue, especially when seeking a car loan after Chapter 7 discharge. While it’s technically possible to apply for a loan almost immediately after discharge, waiting a little longer often yields better results and more favorable terms.

Many lenders prefer to see at least 12 to 24 months of consistent, positive payment history post-bankruptcy. This demonstrates a pattern of financial stability and a reduced risk profile. During this waiting period, you can focus on the credit-rebuilding strategies we discussed, allowing your credit score to gradually improve from its post-bankruptcy low.

Pro tip from us: Don’t rush into a car loan. If you can manage with public transport, ride-sharing, or borrowing from a trusted family member for a few months, use that time to strengthen your credit profile. The longer you wait and the more positive financial activity you demonstrate, the better your chances of securing a lower interest rate and more favorable loan terms. Your first post-bankruptcy loan is a stepping stone; make sure it’s a solid one.

Preparing for Your Post-Bankruptcy Car Loan Application

Preparation is key to success, particularly when seeking a car loan with a past bankruptcy on your record. Lenders will scrutinize your application more closely, so presenting yourself as a reliable borrower is paramount.

Know Your Credit Score and Report

Even after a Chapter 7 discharge, your credit score will begin to recover, albeit slowly. It’s essential to know where you stand. Obtain copies of your credit reports from all three major bureaus (Experian, Equifax, and TransUnion) via AnnualCreditReport.com. This is the only source authorized by federal law to provide free credit reports once every 12 months from each bureau. Review them meticulously for any errors or inaccuracies that could further hinder your score.

Understanding your FICO or VantageScore will give you a realistic expectation of what interest rates you might encounter. While a perfect score isn’t expected, showing improvement indicates responsible financial management since your discharge.

Create a Realistic Budget

Before you even think about car models, determine what you can genuinely afford. This isn’t just about the monthly car payment; it includes insurance, fuel, maintenance, and potential repair costs. Based on my experience, common mistakes to avoid are focusing solely on the monthly payment without considering the total cost of ownership. A car that seems affordable on a monthly basis could quickly become a financial burden if you haven’t factored in all associated expenses.

Calculate your debt-to-income ratio (DTI). This ratio compares your total monthly debt payments to your gross monthly income. Lenders use DTI to assess your ability to manage monthly payments. A lower DTI (ideally below 36%) signals less risk to lenders. Understanding your debt-to-income ratio is a critical step in responsible borrowing.

Save for a Substantial Down Payment

Perhaps the single most impactful step you can take to secure a good car loan after Chapter 7 discharge is to save a significant down payment. A larger down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid over the life of the loan.

More importantly, a substantial down payment signals to lenders that you are serious about your financial commitment and have "skin in the game." It significantly reduces their risk. Aim for at least 10-20% of the vehicle’s purchase price. The more you put down, the better your chances of approval and securing a more favorable interest rate, even with a lower credit score.

Demonstrate Income and Employment Stability

Lenders want assurance that you have the consistent income required to make your car payments. They will look for stable employment history. If you’ve recently changed jobs, ensure you can explain the career progression or reasons behind the change.

Be prepared to provide pay stubs, bank statements, and potentially even employment verification letters. Showing a steady work history and a reliable income stream is crucial for convincing lenders of your ability to repay the loan.

Gather All Necessary Documents

Streamline your application process by having all required documents ready. This typically includes:

- Proof of identity (driver’s license, passport)

- Proof of residency (utility bill, lease agreement)

- Proof of income (recent pay stubs, tax returns if self-employed)

- Bank statements

- Your bankruptcy discharge papers

Having these readily available demonstrates your preparedness and can speed up the approval process significantly.

Finding the Right Lender for a Car Loan After Chapter 7

Navigating the lending landscape after bankruptcy requires a strategic approach. Not all lenders are created equal, and some are far more willing to work with individuals who have a Chapter 7 discharge on their record.

Explore Specialized Subprime Lenders

These lenders specifically cater to individuals with lower credit scores, including those with past bankruptcies. They understand that a bankruptcy discharge is a fresh start and are more willing to take on the perceived higher risk.

You can often find these lenders online, through financial aggregators, or at dealerships that advertise "bankruptcy approval" or "fresh start financing." Be aware that while these lenders offer approval, their interest rates will generally be higher than those offered to borrowers with excellent credit. Your goal is to find the most competitive rate among these specialized lenders, not to compare it to prime rates just yet.

Consider Credit Unions

Credit unions are member-owned financial institutions that often have more flexible lending criteria than traditional banks. They tend to be more relationship-focused and may be more willing to work with you if you have a history with them or if you become a member.

Based on my experience, credit unions can sometimes offer slightly better interest rates and more personalized service to borrowers with less-than-perfect credit. It’s always worth checking with local credit unions in your area.

Dealership Financing: Proceed with Caution (Buy Here, Pay Here)

While many dealerships offer in-house financing, often known as "Buy Here, Pay Here" (BHPH), this option should be approached with extreme caution. BHPH dealerships typically approve anyone, regardless of credit history, because they are both the seller and the lender.

The significant downsides often include:

- Exorbitant Interest Rates: These can be much higher than even subprime lenders.

- Limited Vehicle Selection: You’ll often find older, higher-mileage vehicles that may come with mechanical issues.

- Less Favorable Terms: Stricter payment schedules, potential for repossession with minimal missed payments, and sometimes less transparent contract terms.

- Limited Credit Reporting: Some BHPH dealerships do not report payments to all three major credit bureaus, meaning your timely payments may not help rebuild your credit as effectively.

Pro tips from us: Only consider a BHPH dealership as a last resort. If you do, read every single line of the contract, understand all fees, and ensure they report to all three major credit bureaus.

Get Pre-Approved for a Loan

One of the smartest moves you can make is to get pre-approved for a car loan before you step foot on a dealership lot. Pre-approval gives you several significant advantages:

- Know Your Budget: You’ll know exactly how much you can afford, preventing you from falling in love with a car outside your price range.

- Negotiating Power: You become a cash buyer in the eyes of the dealership, giving you leverage to negotiate the car’s price rather than being focused on the monthly payment.

- Compare Offers: You can shop around with multiple lenders for pre-approval. These initial inquiries are often "soft pulls" on your credit, which don’t negatively impact your score. This allows you to compare interest rates and terms without committing.

Consider a Co-Signer

If you’re struggling to get approved or are only offered very high interest rates, a co-signer with good credit could be a viable option. A co-signer essentially guarantees the loan, promising to make payments if you default.

Having a co-signer significantly reduces the lender’s risk, often leading to better approval odds and more favorable interest rates. However, this is a serious commitment for your co-signer. They are fully responsible for the debt if you can’t pay, and it will appear on their credit report. Ensure you and your co-signer fully understand the risks and responsibilities involved before pursuing this path. Choose someone you trust implicitly, and make sure you are confident in your ability to make all payments on time.

Understanding Loan Terms and Avoiding Pitfalls

Once you’ve found a potential lender, it’s crucial to understand the loan terms fully and protect yourself from common pitfalls. This is where attention to detail pays off.

Interest Rates

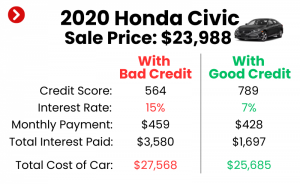

Expect higher interest rates when getting a car loan after Chapter 7 discharge. This is simply a reflection of the perceived risk associated with your credit history. While you should aim for the lowest rate possible, focus more on the overall cost of the loan and whether the monthly payments are truly affordable within your budget. Don’t be swayed solely by a low monthly payment if it comes with an excessively long loan term and a high interest rate.

Loan Term (Length)

The loan term refers to how long you have to repay the loan. Shorter terms (e.g., 36-48 months) mean higher monthly payments but significantly less interest paid over the life of the loan. Longer terms (e.g., 60-72 months or even longer) result in lower monthly payments, which might seem appealing, but you’ll pay substantially more in interest over time.

Pro tips from us: Strive for the shortest term you can comfortably afford. This minimizes the total cost of the loan and gets you out of debt faster.

Beware of Hidden Fees and Upselling

Carefully review the entire loan agreement for any hidden fees such as origination fees, document fees, or prepayment penalties. Ensure you understand every charge. Additionally, dealerships are notorious for upselling additional products like extended warranties, GAP insurance, paint protection, or undercoating. While some of these might have value (GAP insurance can be wise if you have a small down payment), others are often overpriced and unnecessary.

Common mistakes to avoid are signing without fully understanding all fees and feeling pressured into purchasing add-ons you don’t need. Read the fine print meticulously and ask questions about anything you don’t understand before signing.

Strategies for Improving Your Loan Terms Over Time

Securing your first car loan after Chapter 7 discharge is a significant achievement, but it’s often just the beginning of your journey to better credit and more favorable financial terms. Your initial loan might come with a higher interest rate, but there are strategies to improve your situation down the road.

Refinancing Your Loan

One of the most effective strategies is to refinance your car loan after you’ve established a solid payment history. After 6 to 12 months of making all your car payments on time, your credit score will likely have improved. This makes you a more attractive borrower to a wider range of lenders.

You can then apply to refinance your loan at a lower interest rate, potentially saving you thousands of dollars over the remaining term of the loan. This is a common and smart move for individuals rebuilding credit, as your first loan serves as a stepping stone to demonstrate your reliability.

Accelerated Payments

If your budget allows, consider paying more than your minimum monthly payment. Even an extra $25 or $50 each month can significantly reduce the principal balance faster, thereby reducing the total interest you’ll pay and shortening the loan term. Ensure your lender applies these extra payments directly to the principal.

Continued Credit Building

Don’t let your car loan be the only positive entry on your credit report. Continue to practice good financial habits: pay all bills on time, keep your secured credit card balances low (or paid off), and monitor your credit reports for any discrepancies. The more positive financial activity you have, the stronger your credit profile will become, opening doors to even better financial products in the future.

Conclusion: Driving Towards a Brighter Financial Future

Getting a car loan after Chapter 7 discharge is not only achievable but also a powerful tool for rebuilding your credit and regaining financial independence. It requires patience, meticulous preparation, and a strategic approach to finding the right lender and understanding your loan terms.

Remember, your bankruptcy discharge is a fresh start, not a permanent roadblock. By focusing on rebuilding your credit, saving a substantial down payment, demonstrating income stability, and carefully vetting lenders, you can secure a reliable vehicle that meets your needs. Don’t be discouraged by higher initial interest rates; view your first post-bankruptcy car loan as a stepping stone. With consistent, on-time payments, you’ll soon be in a position to refinance and enjoy even better terms.

The road ahead may have a few bumps, but with the right guidance and a commitment to responsible financial management, you’ll be driving towards a brighter, more secure financial future in no time. Start planning today, prepare thoroughly, and confidently take the wheel of your financial destiny.