Navigating the Road Ahead: Your Expert Guide to Huntington Bank Used Car Loans

Navigating the Road Ahead: Your Expert Guide to Huntington Bank Used Car Loans Carloan.Guidemechanic.com

Driving away in a used car can be an incredibly rewarding experience. It offers the thrill of a "new" ride without the steep depreciation hit of a brand-new vehicle. However, securing the right financing is often the most critical step in making that dream a reality. This is where a reliable lender like Huntington Bank comes into play.

As an expert in auto financing, I’ve seen firsthand how the right loan can transform a stressful purchase into a smooth, exciting journey. This comprehensive guide will walk you through everything you need to know about Huntington Bank used car loans, ensuring you’re well-equipped to make informed decisions and drive off the lot with confidence. We’ll delve deep into their offerings, the application process, and expert tips to secure the best possible terms.

Navigating the Road Ahead: Your Expert Guide to Huntington Bank Used Car Loans

Why a Used Car Makes Smart Financial Sense

Before we dive into the specifics of Huntington Bank, let’s briefly touch upon why choosing a used car is often a brilliant financial move. It’s not just about saving money upfront; it’s about long-term value.

New cars depreciate rapidly the moment they leave the dealership, often losing 20-30% of their value in the first year alone. Used cars, on the other hand, have already absorbed the brunt of this depreciation, meaning your investment holds its value much better over time. This financial advantage frees up more of your budget for other important things.

Huntington Bank: A Trusted Partner in Your Car Buying Journey

Huntington Bank has a long-standing reputation for providing accessible and competitive financial products, including auto loans. They understand that buying a car, whether new or used, is a significant decision. Their approach is often characterized by customer-centric services and a commitment to making the financing process as clear as possible.

Based on my experience, choosing a reputable bank like Huntington offers several advantages. You’ll typically find transparent terms, dedicated support, and the peace of mind that comes with working with a well-established financial institution. This reliability is especially crucial when navigating the complexities of used car financing.

Understanding Huntington Bank’s Used Car Loan Options

Huntington Bank offers a range of auto loan solutions designed to fit various needs, specifically catering to those looking to finance a used vehicle. It’s essential to understand these options to determine which best aligns with your financial situation and car buying goals. They don’t just offer a one-size-fits-all solution; instead, they provide flexibility.

New Purchase Loans for Used Vehicles

This is the most common type of loan for individuals buying a used car from a dealership or even a private seller. Huntington Bank provides financing to cover the purchase price of the vehicle, allowing you to pay it back over a set period. These loans are structured with fixed interest rates, meaning your monthly payment remains consistent throughout the loan term.

The specific terms, such as the interest rate and repayment period, will depend on factors like your creditworthiness, the age and mileage of the vehicle, and the overall economic climate. Huntington aims to offer competitive rates that make used car ownership affordable.

Refinancing Your Existing Used Car Loan

Many people overlook the opportunity to refinance their current auto loan, but it can be a powerful financial tool. If your credit score has improved since you first purchased your used car, or if interest rates have dropped, refinancing with Huntington Bank could save you a significant amount of money. This process involves taking out a new loan with better terms to pay off your old loan.

We’ll delve deeper into refinancing later, but it’s important to know that Huntington offers this service. It allows you to potentially lower your monthly payments, reduce your interest rate, or even shorten your loan term, leading to substantial savings over the life of the loan.

Loan Features That Matter

When considering any auto loan, it’s crucial to look beyond just the interest rate. Huntington Bank’s used car loans often come with features designed to benefit the borrower. For example, they typically offer flexible repayment terms, allowing you to choose a loan duration that fits your budget, ranging from shorter terms with higher payments to longer terms with lower payments.

Furthermore, many of their loans do not carry prepayment penalties. This means you have the freedom to pay off your loan earlier than scheduled without incurring additional fees, which can save you a considerable amount in interest over time. From years of analyzing auto loans, I can confirm that the absence of prepayment penalties is a significant advantage, providing you with financial agility.

The Huntington Bank Auto Loan Application Process: A Step-by-Step Guide

Securing a used car loan with Huntington Bank is a structured process designed to be straightforward. Understanding each step can help you prepare thoroughly and ensure a smooth experience. Preparation is key to a successful application.

Step 1: Get Pre-Approved – Your Power Play

One of the most valuable pieces of advice I can offer is to get pre-approved for a loan before you even start serious car shopping. Huntington Bank offers a pre-approval process that provides you with a clear understanding of how much you can borrow and at what interest rate. This acts as a powerful financial weapon in your car buying arsenal.

Why pre-approval is crucial:

- Budget Clarity: You’ll know your exact spending limit, preventing you from falling in love with a car outside your financial reach.

- Negotiation Power: Dealers view pre-approved buyers as serious purchasers, which can give you leverage in negotiating the car’s price. You’re walking in with your own financing already secured.

- Time Savings: It streamlines the purchase process at the dealership, as the financing is largely handled beforehand.

The pre-approval process typically involves a soft credit pull, which won’t impact your credit score. If you proceed with the loan, a hard inquiry will be made.

Step 2: Gather Your Essential Documentation

Once you decide to apply, whether for pre-approval or a full loan, you’ll need to provide certain documents. Having these ready beforehand will significantly speed up the process. Huntington Bank, like all lenders, needs to verify your identity, income, and financial stability.

Commonly required documents include:

- Personal Identification: Government-issued ID (driver’s license, state ID).

- Proof of Income: Recent pay stubs (usually 2-3 months), tax returns (W-2s or 1099s for self-employed), or bank statements.

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Social Security Number: For credit verification.

- Vehicle Information: Once you’ve chosen a car, you’ll need its VIN, mileage, and purchase price.

A common mistake to avoid is waiting until the last minute to gather these documents. Based on my experience, having everything organized upfront prevents delays and frustration.

Step 3: Choose Your Application Method

Huntington Bank offers multiple convenient ways to apply for a used car loan:

- Online Application: This is often the quickest and most popular method. You can complete the application from the comfort of your home, any time of day.

- In-Branch: If you prefer face-to-face interaction and personalized assistance, visiting a Huntington Bank branch allows you to speak directly with a loan officer.

- Over the Phone: You can also initiate or complete an application by calling their customer service line.

Each method has its advantages, so choose the one that best suits your comfort level and schedule.

Step 4: Understanding Credit Score and Its Impact

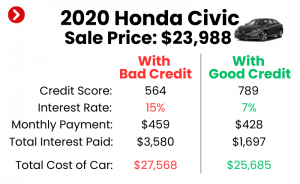

Your credit score is arguably the most significant factor influencing the interest rate you’ll receive on a Huntington Bank used car loan. Lenders use your score to assess your creditworthiness and the risk associated with lending you money. A higher credit score generally translates to a lower interest rate, saving you thousands over the life of the loan.

Here’s a general breakdown:

- Excellent Credit (720+): You’ll likely qualify for the best rates and terms.

- Good Credit (660-719): Still very good, you’ll get competitive rates.

- Fair Credit (600-659): You may qualify, but rates could be higher.

- Poor Credit (<600): Approval might be challenging, or rates could be significantly higher.

Pro tips from us: Always check your credit score before applying for any loan. You can get free credit reports annually from the three major bureaus (Equifax, Experian, TransUnion). This allows you to identify and dispute any errors that could negatively impact your score. For more tips on understanding your credit score, check out our article on .

Step 5: Decision and Funding

After submitting your application, Huntington Bank will review your information, including your credit history and income. You’ll typically receive a decision relatively quickly, especially with online applications. If approved, you’ll receive your loan offer detailing the interest rate, loan term, and monthly payment.

Once you accept the terms, Huntington Bank will disburse the funds directly to the dealership or, in some cases, to you if it’s a private party sale. The entire process, from application to funding, is designed to be efficient so you can drive away in your chosen used vehicle without undue delay.

What Influences Your Huntington Bank Used Car Loan Rate?

Understanding the factors that shape your interest rate is crucial for securing the most favorable terms. It’s not just a random number; several elements play a significant role. From years of experience in the lending landscape, these are the critical levers that impact your Huntington auto loan rates.

1. Your Credit Score and History

As mentioned, this is paramount. A robust credit history demonstrating responsible borrowing and timely payments signals lower risk to Huntington Bank. Conversely, a history of late payments or defaults will likely result in a higher interest rate to compensate for the perceived increased risk.

2. Loan Term Length

The duration over which you choose to repay your loan directly impacts your interest rate. Shorter loan terms (e.g., 36 or 48 months) generally come with lower interest rates because the bank gets its money back faster. Longer terms (e.g., 60 or 72 months) often have higher rates, as the bank carries the risk for a longer period. While longer terms mean lower monthly payments, they usually mean more interest paid overall.

3. Loan Amount and Down Payment

The total amount you borrow and the size of your down payment also influence your rate. A larger down payment reduces the loan amount, thereby lowering the bank’s risk and potentially earning you a better rate. Huntington Bank appreciates borrowers who show a commitment by putting money down upfront.

4. Debt-to-Income (DTI) Ratio

Your DTI ratio compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates that you have more disposable income to cover your loan payments, making you a more attractive borrower. Huntington Bank assesses this to ensure you can comfortably afford the new loan.

5. Age and Mileage of the Used Vehicle

The car itself plays a role. Older used vehicles or those with very high mileage are sometimes considered higher risk by lenders. This is because their value might depreciate faster, and they could require more maintenance, potentially impacting your ability to make payments. Newer used cars (e.g., 1-3 years old) typically qualify for better rates.

6. Market Interest Rates

Beyond your personal financial profile, the general economic environment and prevailing interest rates set by the Federal Reserve influence all lending rates, including auto loans. If market rates are high, your auto loan rate will likely be higher, regardless of your credit score.

Refinancing Your Used Car Loan with Huntington Bank

Refinancing can be a game-changer for many used car owners. It’s a strategic move that could significantly improve your financial standing. Huntington Bank provides robust refinancing options, and understanding when and why to consider them is crucial.

Why Consider Refinancing?

- Lower Interest Rate: If your credit score has improved since you first took out the loan, or if current market rates are lower, you could qualify for a much better interest rate. This directly translates to less money spent on interest over the loan’s life.

- Reduced Monthly Payments: By securing a lower interest rate or extending your loan term (though extending the term might mean more interest overall), you can decrease your monthly outlay, freeing up cash flow.

- Shorten Loan Term: If you’re in a better financial position, you might choose to refinance into a shorter term. While this increases your monthly payment, it drastically reduces the total interest paid and gets you out of debt faster.

- Remove a Co-signer: If you initially needed a co-signer but your credit has since improved, refinancing can allow you to remove them from the loan, relieving them of their financial obligation.

When to Consider Refinancing with Huntington Bank

It’s wise to explore refinancing if any of the following apply to you:

- Your credit score has improved by 50 points or more since your original loan.

- Interest rates in the market have fallen significantly.

- You’re struggling with your current monthly payments and need relief.

- Your current loan has a very high interest rate.

- You want to pay off your car faster.

Huntington’s refinancing process is very similar to applying for a new loan. They will assess your credit, income, and the vehicle’s value. Pro tip from us: Don’t just look at the monthly payment when refinancing; consider the total cost over the loan’s life to ensure you’re truly saving money.

Navigating Challenges: Bad Credit and Used Car Loans

For many, the dream of a used car can seem out of reach due to a less-than-perfect credit score. While Huntington Bank, as a traditional financial institution, primarily serves borrowers with good to excellent credit, there are still avenues to explore. It’s important to set realistic expectations and understand strategies that can improve your chances.

If your credit score is on the lower side, direct approval for a Huntington Bank used car loan might be more challenging than for someone with pristine credit. However, this doesn’t mean it’s impossible.

Strategies to improve your chances with Huntington Bank or similar lenders:

- Substantial Down Payment: Offering a larger down payment reduces the amount you need to borrow, which in turn lowers the bank’s risk. This can sometimes offset a weaker credit profile.

- Apply with a Co-signer: A co-signer with excellent credit can significantly boost your application. They share responsibility for the loan, providing the bank with additional assurance.

- Demonstrate Stable Income: Even with bad credit, a long history of stable employment and verifiable income can make a positive impression. Lenders want to see your ability to repay.

- Improve Your Credit Score First: If time permits, focus on improving your credit score before applying. Pay down existing debts, make all payments on time, and dispute any errors on your credit report. Even a slight increase can make a difference.

- Consider a Secured Loan: While Huntington’s primary auto loans are typically unsecured against the borrower’s general credit, for those with very poor credit, some lenders offer secured personal loans that might be used for a car purchase. This is less common with large banks for auto-specific loans but worth noting in the broader context of financing.

Based on my experience, being transparent about your financial situation and demonstrating a commitment to improving it can go a long way. While Huntington might have stricter criteria than some subprime lenders, their competitive rates for qualified borrowers make it worth exploring.

Pro Tips for a Smooth Huntington Bank Used Car Loan Experience

Securing a used car loan doesn’t have to be a daunting task. With a little preparation and insider knowledge, you can navigate the process with ease and confidence. Here are some expert tips to ensure your experience with Huntington Bank is as smooth as possible.

- Gather Documents Early: Don’t wait until the last minute. Have all your identification, income verification, and residence proof ready before you even start the application. This prevents unnecessary delays.

- Know Your Budget Inside Out: Understand not just what you can afford for a monthly payment, but also the total cost of the car, including insurance, maintenance, and fuel. For more tips on budgeting for your next car, check out our article on .

- Shop Around for Rates: While Huntington Bank offers competitive rates, it’s always wise to compare offers from a few different lenders. This ensures you’re getting the best possible deal for your financial profile.

- Read the Fine Print: Before signing any loan agreement, meticulously read all the terms and conditions. Understand the interest rate, loan term, any fees, and the total amount you’ll repay. Don’t hesitate to ask questions.

- Consider Gap Insurance: If you’re financing a significant portion of your used car, gap insurance can be a smart investment. It covers the "gap" between what your car is worth and what you still owe on the loan if your car is totaled or stolen.

- Communicate Clearly: Maintain open and honest communication with your Huntington Bank loan officer. If you have questions or encounter any issues, reach out promptly. Clear communication fosters a better lending relationship.

Common Mistakes to Avoid When Getting a Used Car Loan

Based on my years in the industry, these are the pitfalls I’ve seen countless people stumble into. Avoiding them can save you significant money and stress.

- Not Getting Pre-Approved: As discussed, skipping pre-approval means you’re shopping blind and lose significant negotiation power at the dealership.

- Focusing Only on Monthly Payments: While a low monthly payment sounds appealing, it often means a longer loan term and more interest paid over time. Always consider the total cost of the loan.

- Ignoring the Total Cost of the Loan: Factor in all fees, interest, and any optional add-ons. The lowest monthly payment isn’t always the cheapest option overall.

- Skipping a Vehicle Inspection: For used cars, a pre-purchase inspection by an independent mechanic is non-negotiable. This can uncover hidden issues that could cost you thousands later.

- Falling for Dealer Financing Without Comparing: Dealers often have strong financing departments, but their first offer might not be the best. Always compare it with your pre-approved Huntington Bank offer.

- Not Understanding Your Credit Report: Errors on your credit report can negatively impact your loan terms. Review it regularly and dispute any inaccuracies.

Conclusion: Drive Forward with Confidence

Securing a used car loan from Huntington Bank can be a straightforward and rewarding experience when approached with knowledge and preparation. From understanding their diverse loan options to meticulously navigating the application process, every step you take can contribute to a more favorable outcome. By leveraging pre-approval, understanding the factors that influence your interest rate, and being mindful of common pitfalls, you position yourself for success.

Huntington Bank’s commitment to customer service and competitive offerings makes them a strong contender for your used car financing needs. With the insights provided in this guide, you are now well-equipped to make informed decisions, secure the best possible terms, and ultimately, drive away in your desired used vehicle with confidence and peace of mind. Your journey to car ownership is an exciting one, and with the right financial partner, it can be a smooth ride from start to finish.