Navigating the Road Ahead: Your Ultimate Guide on How to Remove a Name From a Car Loan

Navigating the Road Ahead: Your Ultimate Guide on How to Remove a Name From a Car Loan Carloan.Guidemechanic.com

Life throws curveballs, and sometimes, financial agreements made with the best intentions need to be unraveled. Whether it’s a relationship ending, a shift in financial circumstances, or simply a desire for greater independence, removing a name from a car loan can seem like a daunting task. It’s a common situation, and understanding your options is the first step towards a smoother journey.

As an expert blogger and professional SEO content writer, I’ve seen countless individuals grapple with this exact challenge. This comprehensive guide is designed to demystify the process, providing you with clear, actionable steps and expert insights to navigate the complexities of removing a name from a car loan. Our goal is to empower you with the knowledge to make informed decisions and secure your financial future.

Navigating the Road Ahead: Your Ultimate Guide on How to Remove a Name From a Car Loan

Why Would You Need to Remove a Name From a Car Loan? Understanding the Common Scenarios

Before we dive into the "how," let’s explore the "why." Based on my experience, people seek to remove a name from a car loan for a variety of very valid reasons. Understanding these common scenarios can help you identify with the situation and confirm you’re on the right path.

1. Divorce or Separation:

This is perhaps the most frequent reason. When a marriage or significant relationship ends, jointly held assets and debts, including car loans, need to be reallocated. A divorce decree might stipulate who gets the car, but it doesn’t automatically remove the other party from the loan. The lender’s agreement still stands.

2. Relationship Changes (Beyond Marriage):

Partners who bought a car together, siblings, or even friends might find themselves in a situation where one party no longer wishes to be financially responsible for the vehicle. Life circumstances change, and what made sense once might not make sense now.

3. Shifting Financial Responsibility:

Sometimes, one person’s financial situation improves dramatically, or perhaps the other party needs to reduce their debt burden for other goals, like buying a home. Removing a name allows for a clear division of financial responsibility. This can be a proactive step to help one party qualify for other loans or simply streamline their personal finances.

4. Improving One Party’s Credit Score:

Having a joint loan means both parties’ credit scores are affected by payment history. If one person has a stronger financial standing or needs to improve their debt-to-income ratio for a significant purchase, removing them from a car loan can be a strategic move. It can free up their credit capacity.

5. Death of a Co-Borrower:

While a somber reason, it’s a critical one. If a co-borrower passes away, the remaining borrower might need to formalize the loan solely in their name, especially if the estate needs to be settled without lingering joint debts. This often involves navigating specific legal and financial procedures with the lender.

Understanding Your Current Car Loan Agreement: Co-Borrower vs. Co-Signer

Before you make any moves, it’s crucial to understand the specifics of your current car loan. There’s a significant difference between a co-borrower and a co-signer, and this distinction impacts how you can proceed.

Co-Borrower:

A co-borrower is typically someone who shares equal ownership of the car and equal responsibility for the loan. Both names are on the car’s title, and both are equally liable for making payments. Lenders consider both co-borrowers’ income and credit when approving the loan. Removing a co-borrower often involves a more complex process because they are a primary party to the agreement.

Co-Signer:

A co-signer, on the other hand, does not typically have an ownership stake in the car itself (their name isn’t on the title), but they are equally responsible for the loan payments if the primary borrower defaults. Their role is to add creditworthiness to the application. Removing a co-signer can sometimes be simpler than removing a co-borrower, but it still requires lender approval and often a demonstration of the primary borrower’s ability to pay alone.

Reviewing Your Loan Documents:

Your original loan agreement is your bible here. It will clearly state who the borrowers are, the terms, and potentially clauses related to name changes or transfers. Take the time to read through it thoroughly. Look for terms like "assumption clause" or "release of liability."

Contacting Your Lender:

Once you’ve reviewed your documents, your next step is to contact your current lender. They are the ultimate authority on what options are available to you. Explain your situation clearly and ask about their specific policies and procedures for removing a name from a car loan. Each financial institution has its own set of rules and requirements.

The Primary Methods to Remove a Name from a Car Loan: A Deep Dive

There isn’t a single "easy button" to remove a name from a car loan. Instead, there are several distinct methods, each with its own requirements, benefits, and drawbacks. Let’s explore them in detail.

Method 1: Refinancing the Car Loan

Refinancing is, by far, the most common and often the most practical method for removing a name from a car loan. It essentially means taking out a brand-new loan to pay off the existing one, with only the desired party listed as the borrower.

What it is and How it Works:

When you refinance, a new lender (or even your current one) offers you a new loan with new terms (interest rate, payment schedule, etc.). This new loan pays off your old loan entirely. If only one person applies for the new loan, the other person’s name is automatically removed from the financial obligation. The new loan is then solely in the name of the applicant.

Eligibility Requirements:

To successfully refinance, the remaining borrower must qualify for the new loan on their own. Lenders will assess:

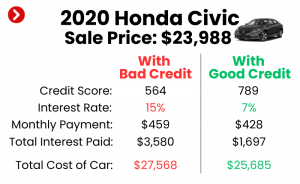

- Credit Score: A good credit score (typically 670+) is crucial. The higher your score, the better interest rate you’ll likely receive.

- Income: You must demonstrate sufficient income to comfortably cover the new monthly payments, along with your other financial obligations.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. Lenders prefer a DTI below 43%, though it can vary.

- Car’s Value and Age: Lenders also consider the car itself. It needs to be worth enough to secure the loan, and older, high-mileage vehicles can be harder to refinance.

The Application Process:

- Gather Documents: You’ll need proof of income (pay stubs, tax returns), identification, the car’s title, and your current loan information.

- Shop Around: Don’t just go with your current lender. Check rates from multiple banks, credit unions, and online lenders. This is where you can potentially secure a better interest rate or terms.

- Submit Application: Fill out the application with only the name you wish to keep on the loan.

- Credit Check: The lender will perform a hard credit inquiry, which will temporarily ding your credit score by a few points.

- Approval and Closing: If approved, you’ll sign new loan documents, and the new lender will pay off your old loan. The car’s title will then be updated to reflect the new loan and borrower(s).

Pros and Cons of Refinancing:

- Pros: It cleanly separates financial responsibility, can potentially lead to a lower interest rate or monthly payment, and allows one party to retain the vehicle.

- Cons: Requires the remaining borrower to qualify on their own, can temporarily impact credit scores, and might not be an option if credit or income has declined.

Pro Tips from Us:

Before you even apply, pull your credit report from all three major bureaus (Experian, Equifax, TransUnion) and review it for accuracy. Address any errors. Also, consider pre-qualification offers from lenders; these give you an idea of potential rates without a hard credit pull. Prepare all your financial documents in advance to streamline the application process.

Common Mistakes to Avoid:

A common mistake is assuming you’ll qualify without checking your credit score and DTI first. Another is accepting the first offer you receive without shopping around; you could be leaving money on the table. Neglecting to update the car’s title after refinancing is also a critical oversight that can cause issues down the road.

Method 2: Selling the Car

If refinancing isn’t an option, or if neither party wants to keep the car, selling it is a straightforward way to remove both names from the loan. The proceeds from the sale are used to pay off the outstanding balance.

When This is a Viable Option:

Selling the car is a good choice if:

- Neither party needs or wants the vehicle.

- The car’s market value is equal to or greater than the loan balance (no negative equity).

- You need a quick resolution to the shared debt.

Process of Selling:

- Determine Market Value: Use resources like Kelley Blue Book (KBB) or Edmunds to get an accurate estimate of your car’s value.

- Contact Lender: Get the exact payoff amount from your lender, as this includes any accrued interest up to the day you plan to pay it off.

- Private Sale vs. Dealership Trade-in:

- Private Sale: Generally yields a higher price but requires more effort (advertising, showing the car, handling paperwork). You’ll need to coordinate with your lender to release the title once the loan is paid off.

- Dealership: Less hassle, but you’ll likely get less for your car. The dealership handles the payoff and title transfer directly.

- Pay Off the Existing Loan: Once the car is sold, you use the proceeds to pay off the loan immediately. The lender will then release the lien and send you the clear title.

Dealing with Negative Equity:

A common challenge is negative equity, meaning you owe more on the car than it’s worth. If this is the case, you’ll need to come up with the difference out-of-pocket to pay off the loan completely. This is a crucial financial consideration. Based on my experience, underestimating the payoff amount is a common pitfall; always get an official payoff quote from your lender, not just your current balance.

Legal Issues and Paperwork:

Ensure all sales agreements are in writing. For a private sale, the buyer typically pays you, and you then pay the lender. The lender will then mail the title. Make sure you get proof of the loan payoff from your lender.

Method 3: Loan Assumption

Loan assumption is a less common but sometimes viable option. This is where a new borrower (or the remaining borrower) takes over the existing loan, with the original terms, and the original borrower is released from liability.

What it Means:

Instead of taking out a new loan (refinancing), the lender agrees to transfer the current loan to another party. The original terms, interest rate, and payment schedule generally remain the same.

When Lenders Allow It:

Most car loans are not assumable. This is much more common with mortgages. However, some lenders, particularly smaller ones or credit unions, might consider it, especially if the new borrower has excellent credit and the car’s value supports the loan. You absolutely must ask your specific lender if this is an option.

Requirements for the Assuming Party:

The party assuming the loan must meet the lender’s credit and income requirements, just as if they were applying for a new loan. The lender needs to be confident that the new borrower can handle the payments.

Challenges and Limitations:

The biggest challenge is that most auto loan agreements do not include an assumption clause. Even if they do, the process can be lengthy and involves significant paperwork. It’s often easier and quicker to refinance or sell the vehicle.

Method 4: Paying Off the Loan Completely

This is the most straightforward method, provided you have the financial means. If you can pay off the entire outstanding balance of the car loan, both names are immediately removed from the financial obligation.

Sources of Funds:

This could come from savings, a bonus, a settlement, or even a personal loan (though this means replacing one loan with another).

Benefits:

- Instant relief from the debt.

- No credit checks or complex applications.

- Immediate release of the lien and clear title.

- Both parties are completely free from the obligation.

Important Considerations and Potential Challenges

Removing a name from a car loan isn’t just about paperwork; it involves significant financial and legal considerations. Understanding these can help you avoid pitfalls.

1. Credit Score Impact:

When one person is removed from a joint loan (especially through refinancing), the loan disappears from their credit report, which can be positive or negative depending on their overall credit history. For the remaining borrower, taking on the loan solely might initially increase their debt-to-income ratio, but consistent on-time payments will build their credit.

2. Lender Requirements:

As mentioned, every lender has unique policies. Don’t assume what worked for a friend will work for you. Always get specific requirements directly from your loan provider. Pro tip: Document every conversation with your lender, including names, dates, and what was discussed.

3. Negative Equity:

This is a major stumbling block. If you owe more than the car is worth, you’ll need to cover the difference out-of-pocket if you sell the car. For refinancing, negative equity can make it harder to qualify, as lenders are hesitant to lend more than the car’s value.

4. Legal Implications, Especially in Divorce:

A divorce decree might state that one party is responsible for the car loan. However, this decree is a separate legal agreement between you and your ex-spouse; it does not automatically release the other party from the loan obligation in the eyes of the lender. If the designated party defaults, the lender can still pursue the other party for payment. Always seek legal counsel if your situation involves a divorce decree.

5. Consent of All Parties:

In most cases, especially for refinancing or selling, all parties named on the original loan will need to consent to the change and sign new documents. If one party is uncooperative, the process becomes significantly more challenging, often requiring legal intervention.

Common Mistakes to Avoid:

One common mistake is neglecting to get legal advice, especially in complex divorce situations. Another is not getting everything in writing; verbal agreements with lenders or co-borrowers are rarely enforceable. Always confirm the name removal in writing from the lender.

Step-by-Step Guide: How to Navigate the Process

To simplify your journey, here’s a structured approach to removing a name from a car loan:

1. Assess Your Situation Honestly:

Determine why you need to remove a name and which method seems most feasible (refinance, sell, pay off). Check your credit score and current financial standing to gauge your eligibility for refinancing.

2. Gather All Necessary Documents:

Collect your original loan agreement, car title, proof of income, identification, and any relevant legal documents (like a divorce decree). Having these ready will save you time.

3. Contact Your Current Lender:

Explain your goal – removing a name from the car loan. Ask about their specific procedures, required forms, and the options they offer (e.g., "Do you allow refinancing to remove a co-borrower?").

4. Explore Your Options Thoroughly:

- For Refinancing: Apply to multiple lenders. Compare interest rates, loan terms, and any fees. Ensure the new loan will only have the desired name.

- For Selling: Get an accurate appraisal of your car’s value. Obtain an official payoff quote from your current lender. Plan how you’ll handle any negative equity.

- For Paying Off: Confirm the exact payoff amount and ensure you have the funds readily available.

5. Execute the Chosen Method:

Follow through with the refinancing application, the car sale, or the loan payoff. Be diligent with paperwork and deadlines. If refinancing, ensure the new loan is finalized and the old one is paid off.

6. Confirm Name Removal and Title Transfer:

Once the process is complete, get written confirmation from your original lender that your name has been removed from the loan. For refinancing, ensure the car’s title is updated to reflect the new owner(s) and lienholder. For selling, ensure the lien is released and the title transferred to the new owner. Check your credit report a month or two later to ensure the old loan no longer appears as a joint obligation.

What if You Can’t Remove the Name? Alternative Solutions

Sometimes, despite best efforts, you might find it impossible to remove a name from a car loan through traditional methods. This can be frustrating, but there are still paths to explore.

1. Formalizing an Agreement (Not Legally Binding for Lender):

If a name cannot be removed, the parties can draw up a formal, notarized agreement outlining who is responsible for payments, insurance, and maintenance. While this won’t release the other party from the lender’s obligation, it provides a legal framework between the individuals, making it easier to pursue action if one defaults on their promise.

2. Exploring Debt Consolidation (If Applicable):

In some cases, if the remaining borrower has other debts, a personal loan for debt consolidation could potentially include the car loan amount. This would pay off the car loan, but it’s crucial to weigh the new loan’s interest rate and terms carefully. This is a complex financial decision and not always suitable.

3. Seeking Legal Counsel:

If a co-borrower is uncooperative, or if the situation is complicated by divorce decrees that aren’t being followed, legal counsel is essential. An attorney can advise on enforcing agreements or petitioning the court for assistance.

Pro Tips for a Smooth Transition

Based on our extensive experience in financial matters, here are some final pieces of advice to ensure your name removal process goes as smoothly as possible:

- Communicate Openly: Whether it’s with your co-borrower or your lender, clear and honest communication prevents misunderstandings and speeds up the process.

- Get Everything in Writing: Every agreement, every confirmation, every payoff amount should be in writing. Do not rely on verbal assurances.

- Check Your Credit Reports Afterwards: A month or two after the process, pull your credit reports to ensure the loan no longer appears as a joint obligation for the removed party and that the new loan (if refinanced) is correctly reported for the remaining party.

- Consider Professional Advice: For complex situations, particularly those involving divorce or significant financial implications, consult with a financial advisor or legal professional. They can offer tailored guidance and ensure your interests are protected.

Conclusion: Taking Control of Your Financial Journey

Removing a name from a car loan, while challenging, is a common and achievable goal. It requires diligence, understanding your options, and clear communication. By carefully considering refinancing, selling the vehicle, or paying off the loan, and by being aware of the associated financial and legal implications, you can successfully navigate this process.

Remember, taking control of your shared financial obligations is a powerful step towards securing your individual financial future. Don’t let the complexity deter you. With this guide, you now have the knowledge and strategies to confidently move forward and remove a name from a car loan, paving the way for a smoother, more independent financial journey.