Navigating the Road Ahead: Your Ultimate Guide to Bad Credit And Repo Car Loans

Navigating the Road Ahead: Your Ultimate Guide to Bad Credit And Repo Car Loans Carloan.Guidemechanic.com

Getting a car loan can feel like climbing a mountain, even for those with stellar credit. But what if your financial history includes the double whammy of bad credit and a prior vehicle repossession? For many, this scenario seems like an insurmountable obstacle, leading to feelings of frustration and hopelessness. However, based on my extensive experience in the auto financing landscape, I can tell you that while challenging, securing a car loan after a repossession with bad credit is absolutely possible. It requires a strategic approach, patience, and a deep understanding of how lenders operate.

This comprehensive guide is designed to be your ultimate resource, breaking down every aspect of obtaining bad credit and repo car loans. We’ll delve into the realities you face, the strategies that work, and how to not only get approved but also use this opportunity to rebuild your financial future. Our goal is to empower you with the knowledge to confidently navigate this complex journey, turning a seemingly impossible situation into a stepping stone towards financial recovery.

Navigating the Road Ahead: Your Ultimate Guide to Bad Credit And Repo Car Loans

Understanding the Landscape: Bad Credit and the Shadow of Repossession

Before we explore solutions, it’s crucial to understand the challenges you’re up against. A prior repossession casts a significant shadow on your credit profile, signaling to lenders a higher risk.

What Exactly is "Bad Credit"?

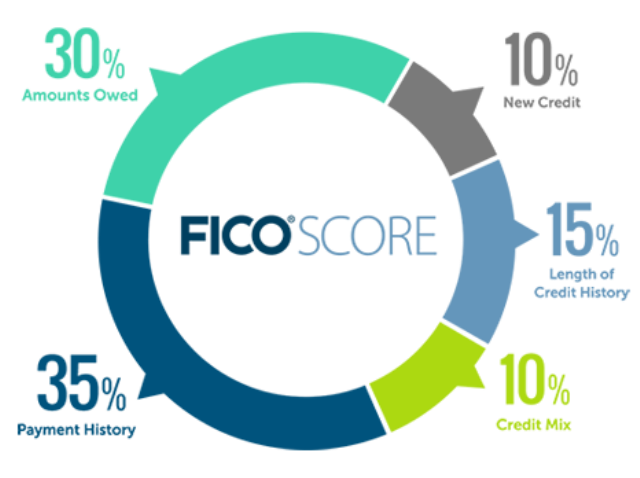

"Bad credit" isn’t a single number; it’s a range. Generally, a FICO score below 600 is considered poor, while anything under 580 is often categorized as very poor. This score is a numerical representation of your creditworthiness, derived from your payment history, amounts owed, length of credit history, new credit, and credit mix. A low score indicates to lenders that you may have a history of missed payments, high debt, or other financial missteps.

This poor credit history tells lenders that extending credit to you carries a higher risk of default. It can make everything from renting an apartment to securing a cell phone contract more difficult and expensive. When it comes to financing a significant purchase like a car, bad credit acts as a major red flag, often leading to loan denials or less favorable terms.

The Profound Impact of a Repossession on Your Credit

A vehicle repossession is one of the most severe negative marks that can appear on your credit report. It signifies that you failed to meet the terms of a previous loan agreement, resulting in the lender seizing the asset. This event has a dramatic and long-lasting effect on your credit score, often causing it to plummet by 100 points or more.

A repossession remains on your credit report for up to seven years from the date of the original delinquency. During this period, it serves as a stark warning to potential lenders, indicating a past inability to manage vehicle financing responsibly. Lenders view this as a direct indicator of future risk, making them extremely cautious about offering new credit, especially another auto loan.

The Psychological and Financial Fallout

Beyond the credit score impact, a repossession can have significant psychological and financial consequences. It can lead to feelings of embarrassment, frustration, and a sense of being stuck. Financially, you might still owe a deficiency balance – the difference between what you owed on the car and what the lender sold it for, plus collection costs. This remaining debt can be pursued by the original lender, further complicating your financial recovery.

Understanding these implications is the first step towards overcoming them. Acknowledging the past without letting it define your future is key. Your goal now is to demonstrate a renewed commitment to financial responsibility.

The Hurdles You Face: Why Lenders Hesitate with Bad Credit and Repo Car Loans

Lenders are in the business of assessing and managing risk. When you approach them with a history of bad credit and a repossession, you represent a higher-risk borrower.

Risk Assessment from a Lender’s Perspective

From a lender’s viewpoint, a repossession history suggests a high probability of future default. They look at your credit report to gauge your reliability. A repossession indicates a past failure to fulfill a payment obligation, making them hesitant to trust you with another substantial loan. They are concerned about their return on investment and the likelihood of recouping their funds.

This risk assessment dictates the terms they are willing to offer, if they offer any at all. They will scrutinize your current income, employment stability, and debt-to-income ratio even more closely. Your ability to demonstrate stability and a commitment to making payments becomes paramount.

Higher Interest Rates and Stricter Terms

One of the most immediate consequences of being approved for bad credit and repo car loans is facing significantly higher interest rates. Lenders mitigate the increased risk by charging more for the money they lend. This higher interest rate translates into higher monthly payments and a greater overall cost for the vehicle over the life of the loan. It’s not uncommon for subprime auto loans to carry interest rates in the double digits, sometimes even exceeding 20% or 30% APR.

Furthermore, you can expect stricter terms. This might include a requirement for a larger down payment, a shorter loan term to reduce the lender’s exposure, or even mandatory GAP insurance. Lenders might also impose limitations on the type or age of vehicle you can finance, often favoring older, less expensive models that pose less financial risk.

Debunking the "Guaranteed Approval" Myth

You might encounter advertisements promising "guaranteed approval car loans" for individuals with bad credit or a repossession. Based on my experience, it’s crucial to approach these claims with extreme skepticism. Legitimate lenders always perform some level of due diligence and risk assessment. No reputable lender can truly guarantee approval without first evaluating your financial situation.

Often, these "guaranteed approval" offers are from buy-here-pay-here (BHPH) dealerships that act as both the seller and the lender. While they may be more lenient with approvals, their interest rates are typically exorbitant, and their terms can be predatory. Pro tips from us: Always read the fine print and understand the total cost of the loan before signing anything, especially with these types of establishments.

Strategies for Success: Getting Approved for Bad Credit And Repo Car Loans

Despite the challenges, securing a car loan after a repossession is achievable. It requires preparation, a proactive approach, and knowing where to look.

Step 1: Assess Your Current Financial Standing Thoroughly

Your first and most critical step is to get a clear picture of your current financial health. This involves more than just a quick glance at your bank balance.

Obtain Your Credit Reports and Scores:

You are legally entitled to a free copy of your credit report from each of the three major credit bureaus (Experian, Equifax, and TransUnion) once every 12 months. Visit AnnualCreditReport.com, the only federally authorized source, to get yours. Scrutinize these reports for accuracy. Ensure the repossession details are correct and that there are no other erroneous entries dragging down your score.

Identify Errors and Understand Negative Entries:

Common mistakes to avoid are not reviewing your credit reports regularly. Errors, even small ones, can significantly impact your score. If you find discrepancies, dispute them immediately with the credit bureau. Understanding why your credit is bad – whether it’s late payments, high credit utilization, or the repossession itself – is crucial for addressing the issues proactively. This knowledge empowers you to explain your situation to lenders more effectively.

Step 2: Save Up a Significant Down Payment

This is perhaps the single most impactful step you can take to improve your chances of approval.

Why a Down Payment Matters for High-Risk Borrowers:

A substantial down payment directly reduces the amount of money you need to borrow, thereby lowering the lender’s risk. It shows the lender that you have "skin in the game" and are financially committed to the purchase. For borrowers with bad credit and a repossession history, a down payment of 10-20% (or even more) is highly recommended. It also helps to offset the rapid depreciation of a new vehicle, preventing you from being "upside down" on your loan (owing more than the car is worth).

How it Reduces Lender Risk:

The more you put down, the less the lender stands to lose if you default. It also helps secure a more favorable interest rate, even if only slightly, because you’re presenting less risk. Based on my experience, a strong down payment can often be the deciding factor between approval and denial for individuals seeking bad credit and repo car loans.

Step 3: Consider a Co-signer

A co-signer can significantly boost your loan application, but it comes with responsibilities for both parties.

The Benefits and Risks:

A co-signer, ideally someone with excellent credit and a stable financial history, adds their creditworthiness to your application. This reassures the lender that if you fail to make payments, they have another responsible party to pursue. This can lead to approval for a loan you otherwise wouldn’t get, and potentially even a better interest rate. However, the co-signer is equally responsible for the debt. If you default, their credit will be damaged, and they will be legally obligated to make the payments.

Choosing the Right Co-signer:

Select a co-signer who understands the implications and fully trusts you. It should be someone with whom you have an open and honest relationship, as their financial future will be tied to yours. Common mistakes to avoid are entering into this agreement lightly or without a clear understanding of the shared responsibility.

Step 4: Explore Specialized Lenders

Traditional banks might be hesitant, but there are lenders who specialize in subprime auto loans.

Subprime Auto Lenders:

These lenders specialize in working with individuals who have less-than-perfect credit. They understand the challenges of bad credit and repo car loans and have underwriting criteria tailored to these situations. While they offer a lifeline, their interest rates are typically higher. You might also find options at buy-here-pay-here (BHPH) dealerships, but proceed with extreme caution due to potentially high rates and unfavorable terms. Always compare offers. You might find our article "Understanding Subprime Auto Lenders" helpful for a deeper dive.

Credit Unions:

Often overlooked, credit unions can be a fantastic option. As member-owned institutions, they sometimes offer more flexible lending criteria and personalized service compared to larger banks. They might be more willing to look beyond your credit score and consider your overall financial situation and relationship with them. If you’re a member of a credit union, or eligible to join one, it’s definitely worth exploring their auto loan options.

Step 5: Be Realistic About Your Vehicle Choice

This isn’t the time to dream of a luxury sports car. Practicality is key.

Focus on Reliable, Affordable Options:

Your primary goal is to secure financing for dependable transportation. Look for a used car that is known for its reliability, has a good maintenance history, and fits comfortably within your budget. A more affordable vehicle means a smaller loan amount, which again reduces the lender’s risk and makes your payments more manageable.

Avoid Luxury or High-Performance Cars:

Lenders will be less inclined to finance an expensive or high-performance vehicle for a high-risk borrower. Such cars often come with higher insurance costs and maintenance, adding further financial strain. Focus on functionality and affordability. This responsible choice demonstrates financial prudence to lenders.

Step 6: Prepare Your Documents Meticulously

Being organized and prepared can streamline the application process and show your seriousness.

Proof of Income, Residence, and Insurance:

Lenders will require verification of your ability to pay. This includes recent pay stubs, bank statements, or tax returns to prove income. They will also need proof of residence (utility bills, lease agreement) and auto insurance coverage. Having these documents ready makes the application process smoother and quicker, showcasing your preparedness.

Gather all necessary personal identification, like your driver’s license and Social Security card. The more comprehensive and organized your documentation, the better impression you make.

Step 7: Negotiate Wisely

Even with bad credit, there’s room for smart negotiation.

Focus on the Total Loan Cost, Not Just Monthly Payments:

Lenders might try to distract you with attractive low monthly payments. Pro tips from us: Always focus on the total cost of the loan, which includes the principal, interest, and any fees. A lower monthly payment spread over a longer term can mean paying significantly more interest overall. Ask for the APR (Annual Percentage Rate) and compare it across different offers.

Understand All Terms and Conditions:

Read every single line of the loan agreement before you sign. Common mistakes to avoid are rushing through the paperwork or assuming you understand everything. Ask questions about prepayment penalties, late fees, and any other clauses that could affect you. Transparency is key. Don’t be afraid to walk away if the terms seem unfair or unclear.

The Path to Rebuilding: Beyond the Loan

Getting approved for bad credit and repo car loans is a victory, but it’s also the beginning of a crucial journey: rebuilding your credit.

Making Timely Payments: The Most Crucial Step

This cannot be stressed enough. Your new auto loan is a powerful tool for credit repair. Every on-time payment you make will be reported to the credit bureaus, gradually chipping away at the negative impact of the repossession and improving your credit score. Set up automatic payments or calendar reminders to ensure you never miss a due date.

Consistency is paramount. Even a single late payment can set you back significantly, negating the positive progress you’ve made. Think of each payment as an investment in your financial future.

Diversifying Credit (Responsibly)

Once you’ve established a consistent payment history with your auto loan, consider cautiously diversifying your credit mix. This doesn’t mean taking on more debt than you can handle. Perhaps a small secured credit card, which requires a deposit equal to your credit limit, could be a next step. Used responsibly, with very low utilization and on-time payments, it can further enhance your credit profile.

The key is to manage all your credit accounts responsibly. A mix of credit types (revolving credit like credit cards and installment loans like your car loan) can be beneficial, but only if you handle them impeccably.

Monitoring Your Credit Reports Regularly

Continue to monitor your credit reports from all three bureaus at least annually, or even more frequently through free services offered by many banks or credit card companies. Check for new errors and track your progress. Seeing your credit score gradually improve can be incredibly motivating. For a deeper dive into improving your credit score, check out our guide on ‘Steps to Boost Your Credit Score Fast’.

This vigilance helps you catch any fraudulent activity or reporting errors early, protecting your progress and your financial identity.

Avoiding New Debt and Living Within Your Means

While rebuilding, it’s vital to avoid taking on unnecessary new debt. Focus on living within your means, creating a budget, and sticking to it. Every dollar you save and every unnecessary expense you avoid contributes to your financial stability and reduces the temptation to take on more credit than you can afford.

Your goal is to demonstrate a consistent pattern of responsible financial behavior, which is the cornerstone of excellent credit.

Pro Tips for Accelerating Credit Repair

- Pay More Than the Minimum: If possible, pay a little extra on your car loan each month. This reduces the principal faster, saves you money on interest, and shows an even stronger commitment to timely payments.

- Keep Old Accounts Open (If Positive): If you have old credit cards with good history, even if you don’t use them, keep them open. This contributes to your length of credit history.

- Dispute Any Remaining Errors: Be persistent in disputing any inaccurate information on your credit report.

- Consider a Secured Credit Card: As mentioned, a secured card can be a safe way to build positive credit if managed correctly.

Common Mistakes to Avoid When Seeking Bad Credit And Repo Car Loans

The path to getting a car loan after a repossession is fraught with potential pitfalls. Being aware of these can save you significant headaches and financial setbacks.

Falling for "Guaranteed Approval" Scams

As discussed, legitimate lenders do not offer "guaranteed approval." These offers often come from predatory lenders or dealerships with extremely high interest rates, hidden fees, and unfavorable terms. Common mistakes to avoid are letting desperation override your judgment. Always scrutinize any offer that sounds too good to be true. It usually is.

Not Reading the Fine Print

This is a critical error many people make. Loan documents can be lengthy and filled with legal jargon, but every word matters. Failing to understand the interest rate, total loan amount, fees, penalties for late payments, and early payoff clauses can lead to nasty surprises down the road. Take your time, ask questions, and don’t sign until you are completely comfortable.

Taking on an Unaffordable Loan

It’s easy to get excited about the prospect of a new car and agree to payments that stretch your budget thin. However, an unaffordable loan is a recipe for disaster, potentially leading to another default and further damage to your credit. Be realistic about what you can truly afford each month, considering all your other expenses. Pro tips from us: Create a detailed budget and stick to it. Your goal is to keep the car, not just get it.

Ignoring Your Credit Report Post-Loan

Just because you got the loan doesn’t mean your credit journey is over. Ignoring your credit report means you won’t see if your payments are being reported correctly, if new errors appear, or if your score is improving as it should. Continuous monitoring is essential for sustained financial health.

Pro Tips From Us: Your Long-Term Financial Success

Navigating bad credit and repo car loans is more than just getting a vehicle; it’s about setting a foundation for long-term financial success.

- Patience and Persistence are Virtues: Rebuilding credit and overcoming a repossession takes time. There’s no quick fix. Be patient with yourself and persistent in your efforts. Every positive step, no matter how small, contributes to your recovery.

- Embrace Financial Literacy: The more you understand about personal finance, credit, and lending, the better equipped you’ll be to make informed decisions. Read articles, take online courses, and seek advice from trusted financial advisors. Knowledge is power.

- Focus on the Long Game: Your immediate need is a car, but your ultimate goal should be financial stability and a strong credit profile. Use this car loan as a stepping stone, a demonstration of your renewed commitment to responsible money management. This long-term perspective will guide your decisions and help you avoid future pitfalls.

Conclusion: Driving Towards a Brighter Financial Future

Securing bad credit and repo car loans is undoubtedly one of the more challenging financial hurdles to overcome. The sting of a repossession and the limitations of a poor credit score can feel overwhelming, making reliable transportation seem like an unreachable dream. However, as we’ve explored, it is far from impossible.

By understanding the landscape, meticulously preparing your finances, exploring specialized lending options, and adopting a disciplined approach to rebuilding your credit, you can absolutely navigate this road successfully. This isn’t just about getting a car; it’s about seizing an opportunity to rewrite your financial narrative, demonstrate responsibility, and build a stronger, more secure future.

Remember, every on-time payment you make is a brick in the foundation of your improved credit score. Take a deep breath, gather your resources, and embark on this journey with confidence. Your path to reliable transportation and financial recovery starts now.