Navigating the Road Ahead: Your Ultimate Guide to Bad Credit Car Loans with a Direct Lender

Navigating the Road Ahead: Your Ultimate Guide to Bad Credit Car Loans with a Direct Lender Carloan.Guidemechanic.com

For many, a car isn’t just a luxury; it’s a necessity. It’s the key to getting to work, picking up children, and managing daily life. However, if your credit score has taken a hit, the dream of owning a reliable vehicle can seem out of reach. Traditional lenders often slam the door shut, leaving you feeling stuck. But what if we told you there’s a powerful solution? Enter the world of Bad Credit Car Loans Direct Lender options.

This comprehensive guide will illuminate the path to securing a vehicle, even when your credit history isn’t perfect. We’ll explore how direct lenders operate, why they might be your best bet, and precisely what you need to do to drive away with confidence. Our goal is to provide you with the most in-depth, actionable advice to transform your car ownership aspirations into reality.

Navigating the Road Ahead: Your Ultimate Guide to Bad Credit Car Loans with a Direct Lender

Understanding the Landscape: What is a Bad Credit Car Loan?

Before we dive into direct lenders, let’s clarify what we mean by "bad credit" in the context of auto financing. Generally, a FICO score below 600-620 is considered "subprime" or "bad credit." This doesn’t mean you’re a bad person; it simply indicates to lenders that you’ve had some financial missteps in the past, such as late payments, defaults, or bankruptcies.

Traditional banks and credit unions typically view these scores as a higher risk. They prefer borrowers with excellent credit histories, as they represent a lower chance of default. Consequently, they often offer the lowest interest rates and most favorable terms.

However, the market for bad credit car loans is specifically designed for individuals in your situation. These loans acknowledge your past challenges but focus on your current ability to repay. They provide a crucial lifeline for those who need a vehicle but are hampered by their credit score. While interest rates may be higher due to the increased risk, these loans make car ownership accessible and offer a unique opportunity to rebuild your credit.

The Power of a Direct Lender for Bad Credit Car Loans

When you’re searching for auto loans for bad credit, you’ll encounter various types of lenders. These generally fall into two categories: indirect lenders (dealerships working with multiple banks) and direct lenders. Understanding the difference is crucial for your success.

A direct lender is an institution that provides loans directly to the borrower. This means you apply to them, they approve or deny your application, and if approved, they fund the loan themselves. Examples include banks, credit unions, and specialized finance companies that focus on specific market segments, such as subprime auto loans.

The power of choosing a direct lender for bad credit car loans lies in this direct relationship. You communicate directly with the source of the funds, often leading to a more streamlined and transparent process. This approach can simplify what might otherwise feel like a daunting journey.

Why Choose a Direct Lender for Your Bad Credit Auto Financing?

Opting for a direct lender can offer distinct advantages when your credit score is less than ideal. These benefits often make the application process smoother and more understandable. They are specifically geared towards helping individuals secure a car loan with bad credit.

-

Personalized Service and Direct Communication:

When you work with a direct lender, you’re dealing directly with the decision-makers. This often translates to more personalized attention and clear communication throughout the application process. You can ask questions directly and get immediate answers without an intermediary. This direct line of communication helps build trust and ensures you understand every aspect of your loan. -

Faster Approval Process:

Direct lenders often have more control over their underwriting criteria and approval process. This can lead to quicker decisions compared to going through a dealership that might need to submit your application to multiple third-party banks. For those in urgent need of a vehicle, this speed can be a significant advantage. Based on my experience in automotive finance, direct lenders can sometimes provide conditional approvals within minutes, speeding up your car buying journey considerably. -

Greater Transparency:

The direct relationship fosters greater transparency regarding loan terms, interest rates, and fees. There’s less room for miscommunication or hidden charges when you’re negotiating directly with the funding source. This transparency is vital when securing a bad credit auto loan, as understanding the full cost is paramount. You’ll have a clear understanding of your repayment schedule and the total amount you’ll owe. -

Potential for Flexible Terms:

While direct lenders still need to mitigate risk, some specialized subprime lenders might be more flexible with their terms. They may consider your individual circumstances more holistically rather than relying solely on an automated credit score assessment. This flexibility can be particularly beneficial if you have a stable income but a recent credit challenge. They might look at your employment history and other financial indicators more closely. -

Focus on Credit Improvement:

Many direct lenders who specialize in bad credit auto financing are also invested in helping you improve your financial standing. By offering you a loan, they give you an opportunity to demonstrate responsible repayment behavior. Successful on-time payments can significantly boost your credit score over time, paving the way for better financial opportunities in the future. This is a crucial benefit often overlooked.

Key Factors Direct Lenders Consider Beyond Your Credit Score

It’s a common misconception that a bad credit score automatically disqualifies you from a car loan. While your score is important, direct lenders specializing in bad credit car loans look at a broader picture. They understand that a credit score is just one piece of your financial story.

Pro tips from our team of finance experts: Don’t let your credit score be the only factor you consider. Focus on strengthening these other areas to present a compelling case to lenders.

-

Stable Income and Employment History:

This is often the most critical factor for a direct lender. Your current income demonstrates your ability to make monthly payments. Lenders prefer to see stable employment, ideally with the same employer for at least six months to a year. A consistent paycheck signals reliability and financial responsibility. The higher your income relative to the loan amount, the more confident a lender will feel about your repayment capacity. -

Debt-to-Income (DTI) Ratio:

Your DTI ratio compares your total monthly debt payments (including your potential new car payment) to your gross monthly income. Lenders use this to assess if you can comfortably afford another monthly obligation. A lower DTI ratio indicates less financial strain and a greater ability to manage new debt. Aim for a DTI ratio below 40% if possible, including your new car payment. -

Down Payment:

A significant down payment is one of the most effective ways to offset bad credit. It reduces the amount you need to borrow, lowers your monthly payments, and shows the lender you’re serious about the purchase. It also reduces the lender’s risk, as you have more equity in the vehicle from day one. Even a 10-20% down payment can make a substantial difference in approval odds and interest rates. -

Co-signer (Optional but Helpful):

If you have a strong co-signer with good credit, it can significantly improve your chances of approval and potentially secure a better interest rate. A co-signer legally agrees to take responsibility for the loan if you default. However, choose a co-signer carefully, as their credit will also be affected if you miss payments. This option should be considered a last resort and with clear understanding from both parties.

Preparing for Your Bad Credit Car Loan Application

Preparation is key to securing any loan, especially a bad credit car loan direct lender. The more organized and informed you are, the better your chances of approval and securing favorable terms. Think of this as laying the groundwork for your financial success.

-

Know Your Credit Score and Report:

Before applying anywhere, pull your credit report from all three major bureaus (Experian, Equifax, TransUnion) via AnnualCreditReport.com. Review it for inaccuracies and dispute any errors. Knowing your score and understanding what’s on your report empowers you to explain any past issues to a lender confidently. This also helps you set realistic expectations for interest rates and loan terms. -

Create a Realistic Budget:

Don’t just think about the monthly car payment. Factor in insurance, fuel, maintenance, and potential repair costs. Use an online calculator to estimate total monthly expenses. Common mistakes to avoid are underestimating these ancillary costs. A detailed budget ensures you can comfortably afford the car without straining your finances, which is crucial for successful repayment. Our article on can provide valuable insights for this step. -

Gather Necessary Documents:

Direct lenders will require specific documentation to verify your identity, income, and residency. Be prepared with:- Proof of income (pay stubs, tax returns)

- Proof of residency (utility bills, lease agreement)

- Valid driver’s license

- Social Security number

- Bank statements

Having these ready streamlines the application process and shows you are serious and organized.

-

Save for a Down Payment:

As mentioned, a down payment can significantly boost your approval chances. Start saving as much as you can. Even a few hundred dollars can make a difference, especially when combined with other strong factors. A larger down payment also reduces your loan-to-value ratio, which is attractive to lenders. -

Improve Your Credit (Even Slightly):

While you might be in a hurry, taking a few weeks or months to make small improvements can pay off. Pay down credit card balances, make all payments on time, and avoid opening new credit accounts. For a deeper dive into improving your credit score, check out our guide on . Every point added to your score can potentially lead to a better interest rate.

The Application Process with a Direct Lender

Applying for a bad credit auto loan with a direct lender is generally straightforward once you’ve done your preparation. The process usually involves a few key steps, whether you apply online or in person. Understanding these steps will help you navigate them smoothly.

-

Online vs. In-Person Application:

Many direct lenders offer convenient online application portals. This allows you to apply from the comfort of your home, often with quick preliminary decisions. However, some prefer an in-person visit, especially if your financial situation is complex, as it allows for direct discussion and clarification. Choose the method that best suits your comfort level and the lender’s offerings. -

What to Expect During the Application:

You’ll be asked to provide personal details, employment history, income information, and details about your desired vehicle (if known). The lender will perform a hard credit inquiry, which will temporarily lower your score by a few points. However, multiple inquiries for the same type of loan within a short period (usually 14-45 days) are often grouped as one for scoring purposes. -

Reviewing Loan Offers Carefully:

If approved, you’ll receive a loan offer outlining the annual percentage rate (APR), the loan term (length), and your monthly payment. Do not rush this step. Review every detail. Compare offers from multiple direct lenders if possible. This comparison is critical to ensuring you get the best possible terms for your car loan bad credit situation. -

Common Mistakes to Avoid:

One common mistake we often see applicants make is accepting the first offer without understanding all the terms. Another is stretching the loan term too long to lower monthly payments, which significantly increases the total interest paid over the life of the loan. Always prioritize understanding the total cost of the loan, not just the monthly payment.

Understanding Your Loan Terms and Protecting Yourself

Once you receive an offer from a bad credit car loans direct lender, it’s paramount to understand every aspect of the agreement. This is where you protect yourself from potential pitfalls and ensure you’re making a financially sound decision.

-

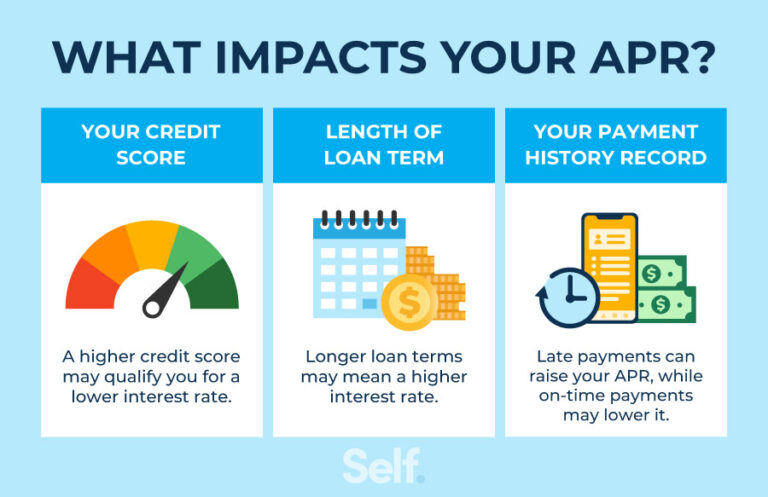

Annual Percentage Rate (APR):

The APR is the total cost of borrowing, expressed as an annual percentage. It includes the interest rate plus any fees. For bad credit auto financing, your APR will likely be higher than for someone with excellent credit. Focus on getting the lowest APR possible, as even a small difference can save you thousands over the loan term. Don’t just look at the interest rate; the APR gives you the full picture. -

Loan Term (Length of Loan):

This is how long you have to repay the loan, typically measured in months (e.g., 36, 48, 60, 72 months). A longer term means lower monthly payments but results in paying more interest over time. A shorter term means higher monthly payments but less total interest paid. Choose a term that balances affordability with the total cost of the loan. -

Fees and Charges:

Be aware of any origination fees, late payment fees, or prepayment penalties. Some lenders charge a fee for processing the loan, while others might penalize you for paying off the loan early. Always ask for a full breakdown of all fees associated with the direct lender auto loan. Transparency here is non-negotiable. -

Understanding the Fine Print:

Read the entire loan agreement before signing. Don’t hesitate to ask questions about anything you don’t understand. Ensure there are no clauses you’re uncomfortable with. This due diligence is your final line of defense against unfavorable terms. -

Avoiding Predatory Lenders:

Unfortunately, some lenders prey on individuals with bad credit. Be wary of anyone promising "guaranteed approval" regardless of your credit, pressuring you to sign immediately, or refusing to provide clear terms in writing. Legitimate bad credit car loans direct lender companies will be transparent and give you time to review the agreement. Always verify a lender’s legitimacy through reviews and regulatory bodies. The Consumer Financial Protection Bureau (CFPB) is an excellent resource for understanding your rights and spotting red flags. (External Link: https://www.consumerfinance.gov/)

Building Your Credit with a Bad Credit Car Loan

One of the most significant long-term benefits of securing a bad credit car loan from a direct lender is the opportunity it presents for credit rebuilding. This isn’t just about getting a car; it’s about setting yourself up for a better financial future.

-

How On-Time Payments Help:

Your payment history is the single most important factor in your credit score (accounting for 35% of your FICO score). Making every car loan payment on time, every month, will have a profoundly positive impact. It demonstrates financial responsibility and reliability to all future lenders. -

Importance of Reporting to Credit Bureaus:

Ensure your direct lender reports your payment activity to all three major credit bureaus. Most reputable lenders do, but it’s worth confirming. If they don’t, your good payment behavior won’t be reflected in your credit score, negating the credit-building benefit. This is a critical question to ask before finalizing your loan.

Life After Approval: Making the Most of Your Loan

Congratulations, you’ve secured your bad credit car loan! But the journey doesn’t end there. Responsible management of your loan is crucial for both your immediate financial health and your long-term credit improvement.

-

Financial Discipline is Key:

Stick to your budget diligently. Make your car payments a priority. Consider setting up automatic payments to avoid missing due dates. This simple step can prevent late fees and ensure your credit score continues to improve. -

Refinancing Options Down the Road:

As you make consistent, on-time payments, your credit score will gradually improve. After 12-18 months of responsible repayment, you might qualify for refinancing your auto loan for bad credit at a lower interest rate. Refinancing can significantly reduce your monthly payments and the total interest you pay over the remaining loan term. Keep an eye on your credit score and current interest rates for this opportunity.

Common Myths and Misconceptions about Bad Credit Car Loans

The world of bad credit auto financing is often shrouded in misconceptions that can deter potential borrowers. Let’s debunk some common myths to provide a clearer picture.

-

Myth 1: "No credit check loans" are the best option.

While some lenders advertise "no credit check" car loans, these are often lease-to-own agreements or have extremely high interest rates and fees. They rarely report to credit bureaus, meaning they won’t help rebuild your credit. A legitimate bad credit car loans direct lender will perform a credit check, but they’ll look beyond just your score. -

Myth 2: You’ll always pay exorbitant rates.

While interest rates will be higher than for prime borrowers, they aren’t always "exorbitant." The rate depends on your specific credit profile, income, down payment, and the lender. By shopping around and preparing, you can find competitive rates within the subprime market. -

Myth 3: It’s impossible to get approved with bad credit.

This is simply not true. The entire industry of subprime auto loans exists to serve individuals with less-than-perfect credit. While approval isn’t guaranteed, it’s certainly possible with the right approach and preparation, especially when working with a specialized direct lender for bad credit auto loans.

Pro Tips for Success with a Bad Credit Car Loan

As experts in this field, we want to equip you with every advantage. Here are our top pro tips to ensure your success in obtaining and managing a bad credit car loan direct lender.

- Research Thoroughly: Don’t just apply to the first lender you find. Compare offers from at least 3-5 direct lenders specializing in bad credit. Look at their reputation, customer reviews, and BBB ratings.

- Negotiate Wisely: Even with bad credit, there’s often room for negotiation on the car’s price or the loan terms. Be confident in your prepared budget and don’t be afraid to walk away if the deal isn’t right.

- Understand the Total Cost: Always calculate the total amount you will pay over the life of the loan, including interest and fees. This gives you a clear picture beyond just the monthly payment.

- Don’t Overextend Yourself: It’s tempting to buy a more expensive car once approved. However, sticking to a car you can comfortably afford, even if it’s less flashy, is a smarter long-term financial decision.

- Maintain Open Communication: If you ever anticipate difficulty making a payment, contact your lender immediately. They may be able to work with you on a temporary solution, which is always better than missing a payment and damaging your credit further.

The Road Ahead: Driving Towards Financial Freedom

Securing a bad credit car loan direct lender isn’t just about getting a new set of wheels; it’s about taking control of your financial future. It’s a testament to your resilience and commitment to improving your creditworthiness. By choosing a direct lender, preparing diligently, understanding your loan terms, and making consistent on-time payments, you can achieve both reliable transportation and a significant boost to your credit score.

Don’t let past financial challenges define your present or future. With the right knowledge and a strategic approach, the road to car ownership and improved credit is well within your reach. Start your research today, gather your documents, and take that confident step towards driving the car you need and deserve. The journey might have a few bumps, but with this guide, you’re well-equipped to navigate them successfully.