Navigating the Road Ahead: Your Ultimate Guide to Bad Credit Car Loans With Low Down Payment

Navigating the Road Ahead: Your Ultimate Guide to Bad Credit Car Loans With Low Down Payment Carloan.Guidemechanic.com

Securing a car loan can feel like an uphill battle, especially when your credit score isn’t perfect. Add the challenge of a low down payment, and it might seem impossible to drive off in a new vehicle. However, based on my experience in the automotive financing world, I can confidently tell you that it’s far from impossible. Many people find themselves in this exact situation, and with the right knowledge and approach, you can too.

This comprehensive guide is designed to empower you. We’ll demystify the process of obtaining bad credit car loans with a low down payment, explore your options, and provide actionable strategies to help you get approved and on the road. Our ultimate goal is to equip you with the insights needed to make informed decisions, avoid common pitfalls, and ultimately rebuild your credit along the way.

Navigating the Road Ahead: Your Ultimate Guide to Bad Credit Car Loans With Low Down Payment

The Reality of Bad Credit Car Loans with Low Down Payment: Is It Truly Possible?

The short answer is yes, securing a car loan with bad credit and a low down payment is possible. However, it’s crucial to approach this situation with realistic expectations. Lenders view applicants with lower credit scores as higher risk. A substantial down payment typically mitigates some of that risk for the lender.

When you combine bad credit with a minimal down payment, you are presenting a double challenge. This doesn’t mean doors are closed, but it does mean you’ll likely encounter different terms and conditions compared to someone with excellent credit and a large down payment. Understanding this fundamental dynamic is your first step towards success.

Dispelling Myths vs. Realities

One common myth is that "guaranteed approval" bad credit car loans exist without any money down. The reality is that no legitimate lender can truly offer guaranteed approval car loans for bad credit without first assessing your ability to repay. While some dealerships might advertise this, it often comes with very high interest rates or strict conditions.

Another misconception is that all lenders will automatically reject you. In truth, a significant portion of the auto lending industry specializes in subprime loans, specifically designed for individuals with less-than-perfect credit. These lenders understand that life happens and that a past financial stumble doesn’t define your future payment reliability.

The Role of Your Credit Score in Auto Lending

Your credit score is a numerical representation of your creditworthiness. It tells lenders how likely you are to repay borrowed money. A "bad credit" score, generally considered below 600, signals a higher risk. This directly impacts the interest rate you’ll be offered and, to some extent, the necessity of a down payment.

Lenders use your credit score, along with other factors like income, employment history, and debt-to-income ratio, to assess your overall risk profile. The lower your score, the more critical these other factors become in demonstrating your ability to manage a new financial obligation.

Understanding Your Credit Situation: The First Step to Success

Before you even think about applying for a car loan, you must understand your current credit standing. This isn’t just about knowing a number; it’s about understanding the story your credit report tells. Based on my experience, many people skip this vital step, which can lead to disappointment and multiple unnecessary credit inquiries.

Knowing your credit score and reviewing your full credit report empowers you. It allows you to identify potential errors, understand the specific factors dragging your score down, and prepare informed answers for lenders. This proactive approach shows responsibility, which can positively influence a lender’s perception.

How to Check Your Credit Score and Report

You are legally entitled to a free copy of your credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) once every 12 months. The official website for this is AnnualCreditReport.com. This is a crucial external resource that every consumer should utilize.

While AnnualCreditReport.com provides your report, it doesn’t always include your score. Many credit card companies, banks, and free services now offer free credit score access. Utilize these tools to get a clearer picture. Remember, different scoring models exist, so your score might vary slightly depending on the source.

Factors That Contribute to a Bad Credit Score

Several elements can lead to a low credit score. Common culprits include a history of late payments, high credit card utilization (using a large percentage of your available credit), collections accounts, charge-offs, bankruptcies, or foreclosures. Even having a "thin" credit file, meaning very little credit history, can result in a lower score because lenders have less data to assess your risk.

Understanding these factors helps you explain your situation to a lender if asked. It also provides a roadmap for future credit improvement, which is a significant benefit of successfully managing a bad credit car financing option.

The "Low Down Payment" Aspect: What Does It Really Mean?

When we talk about a "low down payment" in the context of bad credit, it generally refers to anything less than 10-20% of the vehicle’s purchase price, sometimes even $0 down. While a larger down payment is always beneficial, it’s not always feasible for everyone. The key is to understand how lenders view this, especially when combined with a challenging credit history.

A down payment demonstrates your commitment to the loan and reduces the amount you need to borrow. For lenders, it lowers their risk because they have less capital tied up in the loan, and it gives you immediate equity in the vehicle. This equity makes you less likely to default on the loan.

Defining "Low Down Payment" for Bad Credit Borrowers

For someone with bad credit, a "low" down payment might be $500, $1,000, or even just the sales tax and fees. Some specialized lenders and Buy Here, Pay Here (BHPH) dealerships do offer car loans for bad credit with no money down, but these often come with specific conditions, such as higher interest rates, shorter loan terms, or limits on vehicle selection.

Pro tips from us: Even if you can only put down a small amount, do it. Every dollar you contribute upfront reduces the total amount you finance, which can lower your monthly payments and the overall interest you pay over the life of the loan. It also shows the lender you are serious.

When a Low/No Down Payment is Genuinely Possible

While challenging, a low or no down payment is most likely to be approved if you have strong mitigating factors. These include a stable and verifiable income, long-term employment history, low existing debt, or the ability to secure a qualified co-signer. Lenders look for indicators of your current financial stability, even if your past credit history is bruised.

The type of vehicle you choose also plays a role. Lenders are more comfortable with low down payments on less expensive, used vehicles. These cars depreciate slower and represent less financial risk for the lender if they need to repossess the vehicle.

Finding Lenders Who Specialize in Bad Credit Auto Loans

Not all lenders are created equal, especially when it comes to understanding bad credit auto loans. You wouldn’t go to a heart surgeon for a broken leg, and similarly, you shouldn’t approach a traditional bank (which often has strict credit requirements) if you have bad credit and a low down payment. The key is to target lenders who specialize in your situation.

Based on my experience, focusing your efforts on the right types of lenders will save you time, reduce frustration, and minimize the number of hard inquiries on your credit report. Each hard inquiry can slightly lower your credit score, so being strategic is important.

Dealerships: Buy Here, Pay Here vs. Subprime Departments

- Buy Here, Pay Here (BHPH) Dealerships: These dealerships act as both the seller and the lender. They often cater specifically to individuals with bad credit or no credit, sometimes offering dealerships for bad credit no money down options. The approval process is typically faster and less dependent on traditional credit scores. However, common mistakes to avoid are not carefully scrutinizing their loan terms. Interest rates can be very high, and vehicle selection might be limited. Always read the fine print.

- Subprime Departments at Traditional Dealerships: Many larger dealerships have finance departments with access to a network of subprime lenders. These lenders are third parties that specialize in working with borrowers with lower credit scores. While still offering higher interest rates than prime loans, they often provide more competitive terms than BHPH lots and a wider selection of vehicles.

Online Lenders Specializing in Bad Credit

The internet has opened up numerous avenues for low down payment auto loan bad credit options. Many online lenders specifically market to individuals with credit challenges. They often have streamlined application processes and can provide pre-approvals quickly.

These lenders can be a great option because they allow you to shop around from the comfort of your home, comparing offers without multiple trips to dealerships. Just ensure they are reputable and check customer reviews. Pro tip: Be wary of any online lender promising "guaranteed approval" without any financial checks.

Credit Unions: Sometimes More Flexible

Credit unions are member-owned financial institutions, and they often have a more personalized approach to lending. While they might still have credit requirements, they can sometimes be more flexible than large banks, especially if you have an existing relationship with them or can demonstrate a strong history of saving.

It’s worth checking with local credit unions, even if you think your credit is too low. They sometimes look beyond just the credit score and consider you as a whole member.

Strategies to Increase Your Chances of Approval

Even with bad credit and a low down payment, there are concrete steps you can take to strengthen your application and improve your odds of approval. Lenders are looking for any reason to say "yes," so present the strongest possible case.

Based on my experience, the more prepared and transparent you are, the better your chances. This means having your financial ducks in a row and being ready to address any concerns a lender might have.

Improving Your Application Profile

- Stable Income and Employment: This is paramount. Lenders want to see a consistent, verifiable source of income that demonstrates your ability to make regular payments. Generally, a minimum income threshold (e.g., $1,500-$2,000 per month) is required, along with at least 6 months to a year of employment history.

- Proof of Residency: Stable residency is another indicator of reliability. Be prepared to provide utility bills, rental agreements, or mortgage statements.

- Cosigner: If you can find a cosigner with good credit, it significantly boosts your chances. A cosigner essentially guarantees the loan if you default, reducing the lender’s risk. Common mistakes to avoid: Ensure your cosigner fully understands their responsibility, as their credit will also be affected if you miss payments.

- Trade-In: Even an older, less valuable car can serve as a small down payment. The value of your trade-in directly reduces the amount you need to finance, making your loan more appealing to lenders.

Managing Expectations for Your Car Loan

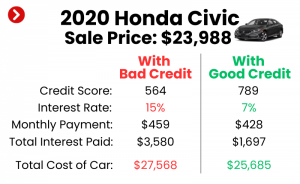

- Higher Interest Rates: With bad credit, higher interest rates are almost a certainty. This is the lender’s way of offsetting the increased risk. Focus on making timely payments, as this can lead to opportunities for refinancing later.

- Potentially Older/Less Expensive Car: You might not get the brand-new luxury vehicle you dreamed of. Be prepared to consider a more affordable, reliable used car. The goal here is to get approved, start rebuilding credit with a car loan, and then upgrade later.

- Understanding Loan Terms: Don’t just look at the monthly payment. Understand the full loan term (e.g., 60 or 72 months) and the total amount you will pay over the life of the loan. A longer term might mean lower monthly payments but significantly more interest paid overall.

The Application Process: What to Expect

Once you’ve done your research and identified potential lenders, it’s time to prepare for the application. Being organized and knowing what to expect can make the process much smoother and less stressful.

Pro tips from us: Treat the car loan application like a job interview. You want to present yourself as a reliable, responsible borrower who is ready to commit to their financial obligations.

Gathering Essential Documents

Lenders will typically ask for a range of documents to verify your identity, income, and residency. Having these ready beforehand will expedite the process:

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Recent pay stubs (usually 2-3 months), bank statements, or tax returns if self-employed.

- Proof of Residency: Utility bill, lease agreement, or mortgage statement.

- References: Sometimes requested, especially by BHPH dealers.

- Trade-in Documents: Title, registration, and payoff information if you still owe money.

Pre-Approval vs. Full Application

- Pre-approval: Many online lenders and some dealerships offer pre-approval. This is a preliminary check that uses a "soft inquiry" on your credit (which doesn’t affect your score) to give you an estimate of what you might qualify for. It’s a great way to gauge your options without committing.

- Full Application: Once you’re ready to proceed with a specific lender and vehicle, you’ll complete a full application. This involves a "hard inquiry" on your credit, which will temporarily ding your score by a few points. However, if you submit multiple auto loan applications within a short window (typically 14-45 days, depending on the scoring model), they are usually grouped as a single inquiry, so shop around efficiently.

Common Pitfalls and How to Avoid Them

- Too Many Hard Inquiries: As mentioned, grouping your applications can mitigate this. Don’t apply randomly to every lender you see. Do your research first.

- Falling for "Guaranteed Approval" Scams: If it sounds too good to be true, it probably is. Legitimate lenders need to verify your ability to pay.

- Not Reading the Fine Print: Always understand the full terms of your loan, including interest rates, fees, penalties for late payments, and early payoff clauses. This is particularly important for affordable car loans for bad credit, where terms can sometimes be less favorable.

- Buying More Car Than You Can Afford: Focus on a reliable car that fits your budget, not your dream car. Your primary goal should be to get approved and rebuild your credit.

Beyond Approval: Making Your Bad Credit Car Loan Work For You

Getting approved for a bad credit car loan with a low down payment is a significant achievement, but it’s just the beginning. The real value comes from leveraging this opportunity to improve your financial standing. This loan can be a powerful tool for credit rebuilding, paving the way for better financial opportunities in the future.

This phase is critical for turning a potentially challenging loan into a stepping stone for financial growth. Pro tips from us: View this car loan as an investment in your credit health, not just a way to get a car.

Rebuilding Credit with Timely Payments

The most impactful way to improve credit for a car loan (and for everything else) is to make all your payments on time, every single month. Payment history accounts for 35% of your FICO score, making it the most important factor. Each on-time payment reported to the credit bureaus demonstrates your reliability and gradually improves your credit score.

Consider setting up automatic payments to avoid missing due dates. Even a single late payment can set back your credit repair efforts significantly. Consistency is key here.

Budgeting: Ensuring Affordability

Before you finalize any loan, create a realistic budget that accounts for your new car payment, insurance, fuel, and maintenance costs. A common mistake is to only consider the monthly car payment and forget about these other crucial expenses. If your car loan stretches your budget too thin, you risk falling behind on payments, which defeats the purpose of rebuilding credit.

Our article, "A Comprehensive Guide to Budgeting for Your First Car," could provide valuable insights into managing these expenses effectively. (Internal link placeholder: )

Refinancing: The Future Possibility

Once you’ve made 6-12 months of on-time payments, and your credit score has shown improvement, you may be eligible to refinance your car loan. Refinancing involves taking out a new loan to pay off your existing one, often at a lower interest rate and potentially better terms. This can significantly reduce your monthly payments and the total interest paid over the life of the loan.

Refinancing is a common strategy for individuals who started with bad credit car loans with a low down payment. It’s your reward for diligently managing your initial loan and improving your credit profile. You might also find our article, "Understanding Auto Loan Interest Rates and How to Lower Them," helpful in this process. (Internal link placeholder: )

Pro Tips for Navigating the Bad Credit Car Loan Landscape

Navigating the world of bad credit auto loans requires a strategic mindset and a willingness to be proactive. Here are some final professional tips to ensure you make the best possible decisions.

- Be Realistic About Your Options: Accept that your first car loan with bad credit might not be ideal. Focus on securing a reliable vehicle that gets you approved and allows you to start rebuilding your credit.

- Do Your Research Thoroughly: Compare offers from multiple lenders, including dealerships, online lenders, and credit unions. Don’t settle for the first offer you receive.

- Read the Fine Print, Always: Understand every aspect of your loan agreement. Ask questions until you fully grasp the terms, fees, and penalties.

- Don’t Be Afraid to Walk Away: If a deal feels wrong, or the terms are too punitive, be prepared to walk away. There will always be other options.

- Consider the Total Cost, Not Just the Monthly Payment: A low monthly payment might sound appealing, but if it’s stretched over a very long term with a high interest rate, you could end up paying significantly more for the car than it’s worth.

Conclusion: Your Journey to a Better Financial Future Starts Here

Securing bad credit car loans with a low down payment is a challenge, but it is undeniably achievable. This journey is about more than just getting a set of wheels; it’s about taking a proactive step towards financial recovery and establishing a stronger credit foundation for your future. By understanding your credit, researching your options, and strategically preparing your application, you significantly increase your chances of approval.

Remember, the goal is not just to get a car, but to use this opportunity to demonstrate responsible financial behavior. With diligence and a commitment to on-time payments, your bad credit car loan can become a powerful tool for rebuilding credit with a car loan, ultimately leading to better financial opportunities and a brighter future on the road ahead. Drive forward with confidence and a clear plan!