Navigating the Road Ahead: Your Ultimate Guide to Best Car Loan Companies for Bad Credit

Navigating the Road Ahead: Your Ultimate Guide to Best Car Loan Companies for Bad Credit Carloan.Guidemechanic.com

Securing a car loan can feel like an uphill battle when your credit score isn’t pristine. Many individuals dream of the freedom and necessity a personal vehicle provides, only to be met with skepticism from traditional lenders. The good news? Having bad credit doesn’t mean your dream of car ownership is out of reach.

As an expert blogger and SEO content writer with extensive experience in personal finance and auto lending, I’ve seen countless individuals successfully navigate this very path. This comprehensive guide will equip you with the knowledge, strategies, and insights needed to find the best car loan companies for bad credit, transforming a daunting challenge into a manageable journey. We’ll delve deep into understanding your options, avoiding common pitfalls, and ultimately, driving away in your new (or new-to-you) vehicle.

Navigating the Road Ahead: Your Ultimate Guide to Best Car Loan Companies for Bad Credit

Understanding Bad Credit and Its Impact on Car Loans

Before we explore solutions, let’s clearly define what "bad credit" typically means in the lending world. Your credit score, often a FICO score, ranges from 300 to 850. Generally, scores below 600-620 are considered "subprime" or "bad credit." This range signals to lenders a higher risk of default.

When you apply for a loan with a low credit score, lenders perceive a greater chance you might not repay the money. This hesitancy often leads to higher interest rates, stricter terms, or even outright rejections from conventional banks. However, it’s crucial to understand that many lenders specialize in working with individuals in your exact situation.

The need for a reliable car is more than just a convenience for many; it’s a necessity for work, family, and daily life. This understanding drives the existence of specialized lenders who are willing to look beyond just your credit score. They consider other vital factors, which we’ll explore shortly.

Debunking Myths: "Guaranteed Approval" and "No Credit Check" Loans

You might encounter advertisements promising "guaranteed approval car loans" or "no credit check auto loans." While these sound incredibly appealing, especially for someone with bad credit, it’s essential to approach them with extreme caution. Based on my experience, these phrases often mask less-than-ideal scenarios.

"Guaranteed approval" usually comes with significant caveats. It might mean you’ll be approved, but at an incredibly high interest rate, for a very old car, or with an unmanageable down payment. These loans can sometimes trap borrowers in cycles of debt.

Similarly, "no credit check" loans, while seemingly offering a shortcut, often come from "Buy Here, Pay Here" dealerships. While these can be an option, they typically report only positive payment history to one credit bureau (if at all), limiting your ability to rebuild credit. They also tend to charge higher interest rates and may not offer competitive pricing on vehicles.

Pro tip from us: Be wary of any offer that sounds too good to be true, especially when it comes to financing. Always read the fine print and compare multiple offers before committing. Transparency is key when dealing with bad credit auto financing.

Key Factors Lenders Consider for Bad Credit Applicants

Even with a low credit score, lenders specializing in bad credit auto loans look at a holistic financial picture. They want to ensure you have the capacity to repay the loan. Understanding these factors can help you prepare a stronger application.

Here are the primary considerations:

- Income Stability: Lenders want to see consistent employment and a steady income. They’ll typically ask for pay stubs, bank statements, or tax returns to verify your ability to make monthly payments. A long history with your current employer is a strong positive.

- Debt-to-Income Ratio (DTI): This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI indicates you have more disposable income to cover new loan payments. Lenders prefer a DTI below 40%, but this can vary.

- Down Payment Size: A substantial down payment significantly reduces the loan amount and the lender’s risk. It shows your commitment and can often lead to better loan terms, even with bad credit.

- Co-signer Availability: Having a co-signer with good credit can dramatically improve your chances of approval and secure a lower interest rate. The co-signer essentially guarantees the loan if you default.

- Vehicle Choice: Lenders might be more willing to approve a loan for a less expensive, older vehicle than a brand-new luxury car. A more affordable car reduces their financial exposure.

- Proof of Residence: Lenders will verify your address to ensure stability. Utility bills or a lease agreement can serve as proof.

By focusing on these areas, you can present yourself as a more reliable borrower, despite your credit history.

Top Strategies for Securing a Car Loan with Bad Credit

Navigating the subprime auto loan market requires a strategic approach. Here’s how you can proactively improve your chances of approval and secure favorable terms.

1. Know Your Credit Score and Report

Before you even think about applying, get a copy of your credit report from all three major bureaus (Experian, Equifax, and TransUnion). You can do this annually for free at AnnualCreditReport.com. Review it for any errors or inaccuracies that might be unfairly dragging down your score. Disputing and correcting these can sometimes boost your score surprisingly quickly.

Understanding your score helps you set realistic expectations. It also allows you to address any issues before a lender sees them. For more details on understanding your score, you might find our article on Understanding Your Credit Score helpful.

2. Budget Wisely: Determine What You Can Truly Afford

Don’t just focus on the monthly payment; consider the total cost of ownership. This includes the car payment, insurance, fuel, maintenance, and registration fees. Overextending yourself financially is a common mistake that can lead to missed payments and further damage to your credit.

Create a realistic budget that accounts for all your expenses. This clarity will guide you towards a car and a loan payment that fits comfortably within your financial means.

3. Save for a Down Payment

This is perhaps the single most impactful step you can take. A larger down payment reduces the amount you need to borrow, thereby lowering your monthly payments and the total interest paid over the life of the loan. It also signals to lenders that you are serious and financially responsible.

Even a down payment of 10-20% can make a significant difference in your approval odds and interest rate. For practical tips on how to save, check out our guide on Tips for Saving for a Down Payment.

4. Consider a Co-signer

If you have a trusted friend or family member with good credit, asking them to co-sign your loan can be a game-changer. Their good credit history essentially "backs" your application, making lenders much more comfortable. This often results in a lower interest rate than you’d get on your own.

However, be aware of the responsibilities. A co-signer is equally responsible for the loan. If you miss payments, their credit score will also suffer, and they could be on the hook for the entire debt. Ensure both parties fully understand this commitment.

5. Explore Different Lender Types

Not all lenders are created equal, especially when it comes to bad credit car loans. It’s crucial to shop around and explore various avenues.

Best Car Loan Companies for Bad Credit: Where to Look

When you have bad credit, the "best" company isn’t always a household name. Instead, it’s often a lender that specializes in your situation, offers flexible terms, and provides transparency. Here are the types of companies and characteristics to seek out:

A. Online Lending Marketplaces

These platforms connect borrowers with a network of lenders, many of whom specialize in subprime auto loans. They streamline the application process and allow you to compare multiple offers without impacting your credit score with multiple hard inquiries initially.

- What they offer: A single application can be submitted to many lenders, providing pre-qualification offers. This allows for rate comparison from the comfort of your home.

- Benefits for bad credit: They cast a wide net, increasing your chances of finding an approval. Many offer soft credit pulls for pre-qualification, meaning your score isn’t affected until you choose a specific lender and proceed.

- Characteristics to look for: User-friendly interfaces, a broad network of reputable lenders (including subprime specialists), and clear explanations of terms.

B. Direct Online Lenders Specializing in Bad Credit

Beyond marketplaces, some online lenders focus solely on applicants with less-than-perfect credit. These companies often use alternative data points beyond just your credit score to assess risk, such as employment history and income stability.

- What they offer: Tailored loan programs designed specifically for bad credit borrowers. They often have faster approval processes and can be more understanding of past financial difficulties.

- Benefits for bad credit: Their expertise in subprime lending means they are equipped to evaluate your application more thoroughly, often leading to approvals where traditional banks might decline.

- Characteristics to look for: Transparency in their rates and fees, good customer reviews, and reporting payments to all three major credit bureaus (essential for rebuilding your credit).

C. Credit Unions

Credit unions are member-owned financial cooperatives that often offer more lenient lending criteria and lower interest rates than traditional banks. They prioritize their members’ financial well-being.

- What they offer: Personalized service, competitive rates, and a willingness to look beyond just your credit score, especially if you have an existing relationship or become a member.

- Benefits for bad credit: Their community-focused approach often means more flexibility for bad credit borrowers. They might consider your entire financial history and relationship with the credit union.

- Pro Tip: Consider joining a local credit union before applying for a loan. Building a banking relationship can sometimes open doors to better loan opportunities.

D. Dealerships with Subprime Financing Departments (or "Buy Here, Pay Here" Options)

Many larger dealerships have dedicated finance departments that work with a variety of lenders, including those specializing in bad credit. "Buy Here, Pay Here" dealerships are another option, where the dealership itself is the lender.

- What they offer: Convenience of a one-stop shop for buying a car and securing financing. "Buy Here, Pay Here" offers direct approval based on your income, often with less emphasis on credit score.

- Benefits for bad credit: Often quicker approvals, especially with "Buy Here, Pay Here" options. Dealerships can sometimes leverage relationships with lenders to get approvals for challenging cases.

- Common Mistakes: Not comparing rates from external lenders before committing to dealership financing. "Buy Here, Pay Here" loans often come with very high interest rates and may not help rebuild your credit effectively. Always ask if they report to all three credit bureaus.

What to Look For in a Lender (Even with Bad Credit)

Regardless of the type of lender you choose, these characteristics are paramount:

- Transparency: All terms, conditions, interest rates (APR), and fees should be clearly disclosed upfront. No hidden surprises.

- No Prepayment Penalties: You want the option to pay off your loan early without incurring extra charges, which can save you significant interest.

- Reporting to Credit Bureaus: This is crucial for rebuilding your credit. Ensure the lender reports your on-time payments to all three major credit bureaus.

- Good Customer Service: You should feel comfortable asking questions and receiving clear, helpful answers.

- Pre-qualification Options: A pre-qualification allows you to see potential rates and terms without a hard inquiry on your credit report.

The Application Process for Bad Credit Car Loans

The application process for a bad credit car loan is similar to a standard loan, but with a few extra considerations.

- Gather Your Documents: Be prepared with proof of identity (driver’s license), proof of income (pay stubs, bank statements, tax returns), proof of residence (utility bill), and potentially a list of references.

- Fill Out the Application Accurately: Provide honest and complete information. Any discrepancies can delay your application or lead to rejection.

- Understand the Offer: Don’t just look at the monthly payment. Pay close attention to the Annual Percentage Rate (APR), the loan term (length of the loan), and the total cost of the loan over its lifetime. A lower monthly payment over a longer term often means paying significantly more in interest overall.

- Read the Fine Print: This is where hidden fees or unfavorable terms can reside. Don’t hesitate to ask for clarification on anything you don’t understand.

Based on my experience, diligence at this stage can save you thousands of dollars and prevent future headaches. Never feel rushed into signing.

Improving Your Credit Score While Paying Off Your Car Loan

Securing a car loan with bad credit is not just about getting a car; it’s also a powerful opportunity to rebuild your credit. Your car loan can become a positive entry on your credit report.

- Make On-Time Payments: This is the most crucial step. Consistency shows lenders you are responsible.

- Keep Credit Utilization Low: If you have credit cards, try to keep your balances low relative to your credit limits.

- Monitor Your Credit Report: Regularly check your credit report for any changes or errors.

By responsibly managing your car loan, you’ll see your credit score steadily improve over time, opening doors to better financial opportunities in the future.

Common Mistakes to Avoid When Getting a Bad Credit Car Loan

Even with the best intentions, it’s easy to fall into common traps. Pro tips from us include avoiding these pitfalls:

- Not Shopping Around: This is the biggest mistake. Accepting the first offer without comparing it to others almost guarantees you’re not getting the best deal.

- Buying More Car Than You Can Afford: Don’t let the excitement of a new car blind you to your financial limits. High monthly payments can quickly become unsustainable.

- Ignoring the Total Cost: Focus on the APR and the total amount you’ll pay over the loan term, not just the monthly payment. A longer loan term might offer lower monthly payments but results in significantly more interest paid.

- Falling for "Guaranteed Approval" Scams: As discussed, these often come with predatory rates and terms. If it sounds too good to be true, it probably is.

- Not Considering a Down Payment: Even a small down payment can drastically improve your loan terms and reduce your overall cost.

- Not Reading the Fine Print: Every clause in your loan agreement is important. Understand what you’re signing.

Frequently Asked Questions (FAQs)

Can I get a car loan with a 500 credit score?

Yes, it is possible to get a car loan with a 500 credit score, but it will be challenging. You’ll likely face higher interest rates and may need a larger down payment or a co-signer. Lenders specializing in subprime loans are your best bet.

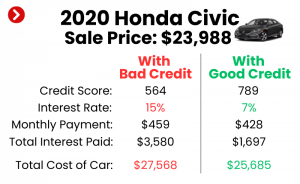

What is a reasonable interest rate for bad credit?

"Reasonable" is relative. For excellent credit, rates can be as low as 3-5%. For bad credit (e.g., FICO under 600), rates can range from 10% to 25% or even higher, depending on your specific score, the lender, the car, and the loan term. Always aim for the lowest possible rate you can secure. You can find general interest rate averages on trusted financial sites like the Consumer Financial Protection Bureau (CFPB) or MyFICO.com (https://www.myfico.com/credit-education/credit-scores).

How much down payment do I need for a bad credit car loan?

While there’s no fixed amount, aiming for at least 10-20% of the vehicle’s purchase price is highly recommended. The more you put down, the better your chances of approval and securing a lower interest rate. Some lenders may approve you with no down payment, but this will result in higher monthly payments and interest costs.

The Road Ahead: Driving Towards Financial Freedom

Getting a car loan with bad credit is undeniably more challenging than with good credit, but it is far from impossible. By understanding the landscape, preparing thoroughly, and choosing the right lending partners, you can successfully secure the financing you need. Remember, this isn’t just about getting a car; it’s an opportunity to demonstrate financial responsibility and actively rebuild your credit for a brighter financial future.

Be patient, be persistent, and most importantly, be informed. With the strategies outlined in this guide, you’re well-equipped to navigate the complexities and drive away with confidence. What has your experience been like finding car loans with challenging credit? Share your stories and tips in the comments below!