Navigating the Road Ahead: Your Ultimate Guide to Car Loan Year Options

Navigating the Road Ahead: Your Ultimate Guide to Car Loan Year Options Carloan.Guidemechanic.com

Embarking on the journey to purchase a new or used vehicle is an exciting prospect. The gleaming paint, the new car smell, the promise of freedom on the open road – it’s all part of the dream. However, beneath the surface of this excitement lies a critical decision that profoundly impacts your financial well-being: choosing the right car loan year option. This seemingly simple choice, often overlooked in favor of focusing solely on the monthly payment, holds the key to unlocking significant savings or, conversely, locking you into a financial burden.

Understanding the various car loan year options is not just about crunching numbers; it’s about aligning your vehicle purchase with your personal financial goals and lifestyle. As an expert in car financing, I’ve seen firsthand how an informed decision can empower buyers, while a hasty one can lead to years of regret. This comprehensive guide will dissect everything you need to know about car loan terms, helping you navigate this crucial financial crossroads with confidence and clarity. Let’s drive into the details and equip you with the knowledge to make the best choice for your unique situation.

Navigating the Road Ahead: Your Ultimate Guide to Car Loan Year Options

What Are Car Loan Year Options and Why Do They Matter So Much?

At its core, a car loan year option, also known as a loan term, refers to the duration over which you agree to repay the money borrowed to purchase your vehicle. This duration is typically expressed in years, ranging from as short as two or three years to as long as seven or even eight years. When you enter into a car loan agreement, you’re essentially committing to a payment schedule that extends across this chosen timeframe.

The significance of this choice cannot be overstated. The loan term directly influences two of the most critical aspects of your car purchase: your monthly payment and the total amount of interest you’ll pay over the life of the loan. A shorter term generally means higher monthly payments but less interest paid overall, while a longer term offers lower monthly payments but accrues more interest over time. It’s a fundamental trade-off that every car buyer must carefully consider.

Based on my experience, many buyers fall into the trap of focusing exclusively on the monthly payment. While affordability is undoubtedly important, a myopic view can lead to selecting a loan term that, while appearing attractive upfront, ultimately costs you far more in the long run. Understanding the interplay between these factors is the first step towards making a financially savvy decision regarding your car loan year options.

The Spectrum of Car Loan Year Options: A Detailed Look

Car loan terms are not one-size-fits-all. They vary widely, each offering distinct advantages and disadvantages depending on your financial situation and priorities. Let’s delve into the most common car loan year options available today.

Short-Term Car Loan Options (2-4 Years)

These are the most aggressive repayment schedules, typically ranging from 24 to 48 months. Buyers opting for these terms are usually looking to pay off their vehicle quickly and minimize interest expenses.

The 3-Year Car Loan (36 Months)

A 3-year car loan is often considered the "sweet spot" for many buyers, particularly those purchasing a new vehicle. It strikes a good balance between manageable monthly payments and significantly reduced interest costs.

Pros of a 3-Year Car Loan:

- Lowest Total Interest Paid: One of the most compelling advantages is the substantial reduction in the total amount of interest you’ll pay over the life of the loan. Because you’re paying off the principal balance faster, there’s less time for interest to accrue.

- Faster Equity Build-Up: With higher monthly payments, you’ll build equity in your vehicle much more quickly. This means you’ll owe less than the car is worth sooner, which is a great position to be in, especially if you plan to trade it in or sell it within a few years.

- Reduced Risk of Negative Equity: Negative equity, or being "upside down" on your loan (owing more than the car is worth), is a common pitfall. A shorter term significantly mitigates this risk, as your repayment outpaces depreciation more effectively.

- Quick Path to Debt-Free Ownership: Achieving full ownership of your vehicle in just three years provides immense financial freedom and peace of mind. You can then allocate those former car payments towards other financial goals, like savings or investments.

Cons of a 3-Year Car Loan:

- Higher Monthly Payments: The most significant drawback is the higher monthly payment. This option requires a more substantial chunk of your budget each month, which might not be feasible for everyone.

- Stricter Approval Requirements: Lenders might require a stronger credit score or a larger down payment to approve a shorter-term loan, as the higher monthly payments represent a greater risk if your income isn’t stable.

- Less Budget Flexibility: These higher payments can strain your monthly budget, leaving less room for unexpected expenses or other discretionary spending.

Who it’s Best For: A 3-year car loan is ideal for buyers with a stable, higher income who prioritize minimizing interest costs and quickly building equity. It’s also an excellent choice for those who plan to keep their vehicle for a long time after it’s paid off, or those who frequently upgrade their cars and want to avoid negative equity.

The 4-Year Car Loan (48 Months)

Slightly extending the term to four years offers a slight reduction in monthly payments compared to a 3-year loan, while still keeping the total interest paid relatively low.

Pros of a 4-Year Car Loan:

- More Manageable Monthly Payments: You’ll find the monthly payments to be more accessible than a 3-year term, making it a viable option for a wider range of budgets.

- Good Balance of Interest Savings and Affordability: It still offers significant interest savings compared to longer terms, without the very high monthly payments of a 3-year loan.

- Faster Equity and Lower Negative Equity Risk: While slightly slower than a 3-year term, you still build equity at a healthy pace, keeping the risk of negative equity low.

Cons of a 4-Year Car Loan:

- Higher Total Interest than 3-Year: You will pay slightly more in total interest compared to the shortest terms, as the loan extends for an additional year.

- Still Requires a Solid Budget: While lower than 3-year options, the monthly payments are still substantial and require careful budgeting.

Who it’s Best For: The 4-year car loan is an excellent compromise for buyers who want to pay off their car relatively quickly and save on interest, but need slightly more breathing room in their monthly budget than a 3-year term allows.

Mid-Term Car Loan Options (5 Years)

The 5-year car loan, or 60-month term, has become one of the most popular choices for car buyers. It strikes a widely accepted balance between monthly payment affordability and the total cost of the loan.

The 5-Year Car Loan (60 Months)

This term is a sweet spot for many, offering a comfortable monthly payment without stretching the loan out excessively.

Pros of a 5-Year Car Loan:

- Widely Accessible Monthly Payments: The 60-month term significantly lowers monthly payments compared to 3- or 4-year loans, making it highly attractive for many budgets. This allows buyers to afford a slightly more expensive vehicle or simply free up cash flow for other expenses.

- Manageable Total Interest: While you’ll pay more interest than on shorter terms, it’s often considered a reasonable amount for the benefit of lower monthly payments. The total interest doesn’t typically spiral out of control unless your interest rate is very high.

- Good Balance for New Cars: For new cars, a 5-year loan often aligns well with the initial depreciation curve, meaning you’re less likely to be underwater on your loan for a significant period.

Cons of a 5-Year Car Loan:

- Higher Total Interest than Shorter Terms: The longer duration means more interest accrues over time, increasing the overall cost of the vehicle.

- Slower Equity Build-Up: It takes longer to build substantial equity in your car, and there’s a higher risk of being in a negative equity position during the initial years, especially if you have a small down payment.

- Ownership Outlasts Warranty: Depending on the manufacturer’s warranty, a 5-year loan might mean you’re still making payments after the bumper-to-bumper coverage expires, potentially leading to unexpected repair costs while still paying off the loan.

Who it’s Best For: A 5-year car loan is an ideal choice for the average car buyer who needs affordable monthly payments but still wants to pay off their vehicle within a reasonable timeframe. It’s particularly popular for new car purchases where the depreciation is steepest in the early years.

Long-Term Car Loan Options (6-8 Years)

Longer car loan terms, typically ranging from 72 to 96 months, have become increasingly common as vehicle prices rise. These options prioritize the lowest possible monthly payment.

The 6-Year Car Loan (72 Months)

Extending your loan to six years further reduces the monthly payment, making higher-priced vehicles more "affordable" on a month-to-month basis.

Pros of a 6-Year Car Loan:

- Significantly Lower Monthly Payments: This is the primary advantage, allowing buyers to purchase more expensive vehicles or keep their monthly budget very lean.

- Greater Budget Flexibility: Lower payments free up cash flow for other financial obligations or discretionary spending.

- Access to Newer/Higher-Trim Vehicles: For some, a 6-year term is the only way to afford the car they truly need or desire.

Cons of a 6-Year Car Loan:

- Substantially Higher Total Interest Paid: The biggest drawback is the significant increase in total interest costs. Over six years, even a seemingly small interest rate adds up considerably.

- High Risk of Negative Equity: You’re very likely to be "underwater" on your loan for a significant portion of the term, especially in the first few years. This means if your car is totaled or you need to sell it, you might owe more than it’s worth.

- Vehicle Depreciation Outpaces Payments: The car will lose value faster than you pay off the loan, making it harder to trade in or sell without financial loss.

- Extended Debt Period: You’ll be carrying car debt for a much longer period, potentially limiting your ability to save for other goals or take on new financial commitments.

- Increased Maintenance Costs While Still Paying: By the sixth year, maintenance and repair costs on the vehicle are likely to increase, adding to your financial burden while you’re still making loan payments.

Who it’s Best For: A 6-year car loan is typically suited for buyers who absolutely need the lowest possible monthly payment to afford a reliable vehicle and have a very tight budget. It’s often a last resort for those who prioritize monthly cash flow over total cost and understand the associated risks of negative equity and higher interest.

The 7-Year+ Car Loan (84+ Months)

These are the longest available car loan terms, stretching to 84 months or even 96 months (7 or 8 years). They offer the absolute lowest monthly payments.

Pros of a 7-Year+ Car Loan:

- Lowest Possible Monthly Payments: These terms provide the ultimate in monthly payment affordability, making almost any vehicle appear within reach.

- Maximum Budget Flexibility (Monthly): They free up the most cash flow each month, which can be appealing for those managing multiple financial commitments.

Cons of a 7-Year+ Car Loan:

- Astronomically High Total Interest: This is where interest costs truly skyrocket. You could end up paying thousands more in interest compared to shorter terms.

- Extreme Risk of Negative Equity: You will almost certainly be underwater on your loan for most of the term, making selling or trading in the car a financially damaging proposition.

- Paying for a Worn-Out Car: By the time you pay off an 84-month loan, your vehicle could be 7 or 8 years old, potentially requiring significant maintenance and repairs, all while you were still making payments.

- Limited Financial Freedom: Being tied to a car loan for such a long period can severely restrict your financial freedom for nearly a decade.

- Higher Interest Rates: Lenders often charge higher interest rates for longer terms due to the increased risk of default and the prolonged period of depreciation.

Who it’s Best For: From our perspective, 7-year+ car loans should generally be approached with extreme caution and are rarely recommended. They are typically only considered by those who absolutely cannot afford a shorter term but desperately need a specific vehicle, and fully understand the substantial long-term financial implications. It’s often a sign that the buyer might be overextending their budget for the car they are choosing.

Factors to Consider When Choosing Your Car Loan Year Option

Selecting the right car loan term is a highly personal decision that should be based on a thorough evaluation of several key financial and lifestyle factors. Based on my experience, overlooking any of these can lead to buyer’s remorse.

1. Your Monthly Budget and Affordability

This is, for most people, the most immediate and impactful consideration. Can you comfortably afford the monthly payment without stretching yourself too thin?

Pro tips from us: Don’t just look at the payment in isolation. Consider all your other monthly expenses, savings goals, and an emergency fund. Your car payment should ideally not exceed 10-15% of your net monthly income. A higher payment on a shorter term might be uncomfortable now but lead to greater financial freedom later.

2. The Total Cost of the Loan

While monthly payments are important, the total cost of the loan—including all principal and interest—is arguably more critical for your long-term financial health.

Common mistakes to avoid are focusing solely on the "low monthly payment" without calculating how much extra you’ll pay in interest over the full term. Use online calculators to compare the total cost of different loan terms. You might be surprised how much more you pay for the convenience of a lower monthly payment on a longer term.

3. Interest Rates

Interest rates play a pivotal role in the total cost of your loan. Generally, shorter loan terms come with lower interest rates because lenders perceive less risk over a shorter period.

As an expert, I’ve observed that a 1% difference in interest rate over seven years can amount to thousands of dollars. Always compare interest rates across different loan terms and lenders. Even a slightly lower rate can save you a substantial sum, especially on a longer loan.

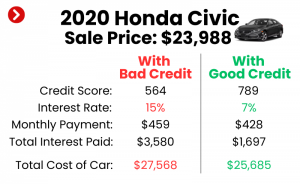

4. Your Credit Score

Your credit score is a major determinant of the interest rate you’ll be offered and, by extension, the overall cost of your loan. A higher credit score signals lower risk to lenders, resulting in more favorable terms.

If your credit score isn’t where you’d like it to be, consider working on improving it before applying for a car loan. Even a few months of diligent effort can make a significant difference in the interest rate you qualify for. For more on this, you might find our guide on Understanding Your Credit Score for a Car Loan helpful. (Internal Link 1)

5. Car Depreciation and Resale Value

Cars begin to depreciate the moment they leave the dealership lot. Depreciation is the rate at which your car loses value over time. Longer loan terms often mean you’re paying off the car slower than it’s losing value, leading to negative equity.

Pro tips from us: Try to align your loan term with the car’s depreciation curve. Shorter terms help you build equity faster, reducing the risk of being upside down. Consider a vehicle’s projected resale value; some cars hold their value better than others, which can mitigate the risks of longer terms. For a deeper dive into this, check out our Ultimate Guide to Car Depreciation. (Internal Link 2)

6. How Long You Plan to Keep the Car

This is a straightforward but often overlooked factor. If you typically trade in your car every 3-4 years, a 7-year loan makes little financial sense.

Based on my experience, it’s wise to match your loan term to your expected ownership period. If you plan to keep the car until it’s paid off and then some, a slightly longer term might be acceptable if it means a significantly lower interest rate. If you plan to upgrade frequently, prioritize shorter terms to avoid negative equity.

7. Your Future Financial Goals

Consider how a car loan fits into your broader financial picture. Are you saving for a house down payment, retirement, or a child’s education?

A high monthly car payment or a long-term debt commitment can hinder progress towards these other goals. Evaluate whether the car loan helps or hurts your overall financial strategy. Sometimes, a slightly older, less expensive car with a shorter loan term is the smarter financial move.

8. Down Payment Amount

The size of your down payment directly impacts the amount you need to borrow. A larger down payment reduces your loan principal, which can make shorter terms more affordable or reduce your overall interest paid.

Pro tips from us: Aim for at least a 10-20% down payment, especially for new cars, to help offset initial depreciation and reduce your loan-to-value (LTV) ratio. A substantial down payment provides immediate equity and can significantly improve your car loan year options.

Common Mistakes to Avoid When Selecting Car Loan Year Options

Navigating car financing can be complex, and it’s easy to make missteps that can cost you dearly. Here are some common mistakes to avoid:

- Focusing Solely on Low Monthly Payments: This is perhaps the most prevalent error. While a low monthly payment is appealing, it often comes at the expense of a longer term and significantly more interest paid over time. Always ask for the total cost of the loan.

- Ignoring the Total Cost of the Loan: As discussed, the total interest paid can add thousands to the price of your vehicle. Failing to consider this figure means you’re not getting the full financial picture.

- Not Considering Future Depreciation: Many buyers don’t think about what their car will be worth in a few years. If you’re planning to trade in, being underwater on your loan due to rapid depreciation and a long loan term can be a costly surprise.

- Overstretching Your Budget: Just because a lender approves you for a certain loan amount or term doesn’t mean you should take it. Don’t let the excitement of a new car push you into a financial commitment that makes you uncomfortable or strains your budget.

- Not Shopping Around for Rates: Never settle for the first loan offer you receive, especially from the dealership. Common mistakes to avoid include not getting pre-approved from multiple lenders (banks, credit unions, online lenders) before stepping onto the lot. This gives you leverage and a benchmark for comparison.

- Not Understanding the Fine Print: Always read the loan agreement carefully. Look for prepayment penalties, late fees, and any additional charges. Make sure you understand all the terms and conditions before signing.

Pro Tips for Navigating Car Loan Year Options

As an expert blogger, I want to equip you with the best strategies for making an informed decision:

- Get Pre-Approved: Before you even visit a dealership, get pre-approved for a car loan from at least two or three different lenders. This gives you a clear understanding of the interest rate and loan terms you qualify for, empowering you to negotiate confidently.

- Understand Your Credit Score: Know your credit score and review your credit report for any errors. A good score is your best asset for securing favorable interest rates and better car loan year options.

- Calculate Total Costs, Not Just Monthly Payments: Always use an online car loan calculator to compare different loan terms (e.g., 3-year vs. 5-year vs. 7-year) and see the total interest paid for each scenario. This transparency is crucial.

- Consider a Larger Down Payment: Even a slightly larger down payment can significantly reduce your principal, leading to lower monthly payments or allowing you to choose a shorter loan term without breaking your budget.

- Refinancing Options: If you initially took a longer-term loan with a higher interest rate, especially if your credit has improved, consider refinancing. Pro tips from us: Refinancing can help you shorten your term, lower your interest rate, or both, saving you money in the long run.

- Match the Loan Term to Your Car Ownership Plans: This cannot be stressed enough. If you keep cars for a decade, a 5-year loan might be perfect. If you trade in every three years, aim for a 3-year term.

Real-World Scenarios: Choosing the Right Car Loan Term

Let’s illustrate how different car loan year options might suit various individuals:

- Scenario 1: The Budget-Conscious Family. A young family needs a reliable SUV but has a tight monthly budget due to other commitments like a mortgage and childcare. They might opt for a 5-year or even a 6-year loan to keep monthly payments manageable, prioritizing cash flow over minimal interest. They understand the higher total cost but need the monthly flexibility.

- Scenario 2: The Aspiring Entrepreneur. A young professional with a stable income and a strong desire to be debt-free quickly wants to purchase a new sedan. They would likely choose a 3-year or 4-year loan. Their goal is to pay off the car quickly, minimize interest, and free up their income for investments or starting a business.

- Scenario 3: The Luxury Car Enthusiast. Someone buying a high-end luxury vehicle, which depreciates rapidly, would be wise to consider a shorter loan term (3-4 years) with a substantial down payment. This strategy helps them stay ahead of the depreciation curve and avoid significant negative equity, especially if they plan to upgrade in a few years.

The Impact of the Current Economic Climate on Car Loan Year Options

It’s important to remember that the economic landscape plays a significant role in car loan decisions. Rising interest rates, for instance, make longer loan terms even more expensive in terms of total interest paid. When rates are high, the temptation to stretch out a loan to lower monthly payments becomes stronger, but the financial penalty in the long run is amplified. Conversely, in a low-interest-rate environment, the difference in total interest between shorter and longer terms might be less dramatic, making longer terms relatively more appealing for some. Always keep an eye on current interest rate trends from trusted sources like the Consumer Financial Protection Bureau (CFPB) to inform your decision. (External Link 1)

Conclusion: Your Car Loan, Your Future

Choosing the right car loan year option is a pivotal step in your car buying journey. It’s not merely a contractual obligation; it’s a strategic financial decision that can profoundly impact your budget, your savings, and your long-term financial health. By understanding the nuances of short-term, mid-term, and long-term loans, and by carefully considering your personal financial situation, you empower yourself to make a choice that aligns with your goals.

Remember, the lowest monthly payment isn’t always the best deal. The goal is to find a balance between affordability, total cost, and your overall financial well-being. Take the time to research, compare offers, and ask questions. With the insights provided in this comprehensive guide, you are now well-equipped to navigate the various car loan year options and drive away with confidence, knowing you’ve made a smart and informed decision. Happy driving!