Navigating the Road Ahead: Your Ultimate Guide to Car Loans for Less Than Perfect Credit

Navigating the Road Ahead: Your Ultimate Guide to Car Loans for Less Than Perfect Credit Carloan.Guidemechanic.com

The dream of owning a reliable vehicle is universal, a cornerstone of independence and daily life for many. Yet, for a significant number of individuals, the path to car ownership hits a snag: a less-than-perfect credit score. If you’ve found yourself in this situation, perhaps feeling discouraged or uncertain, know this: securing car loans for less than perfect credit is not only possible but entirely achievable with the right knowledge and approach.

This comprehensive guide is designed to be your trusted roadmap. We’ll demystify the process, empower you with practical strategies, and shed light on how to secure a favorable auto loan, even when your credit history has a few bumps. Our goal is to provide you with the insights of an expert, transforming what might seem like an uphill battle into a manageable journey towards driving your next car.

Navigating the Road Ahead: Your Ultimate Guide to Car Loans for Less Than Perfect Credit

Understanding "Less Than Perfect" Credit and Its Impact

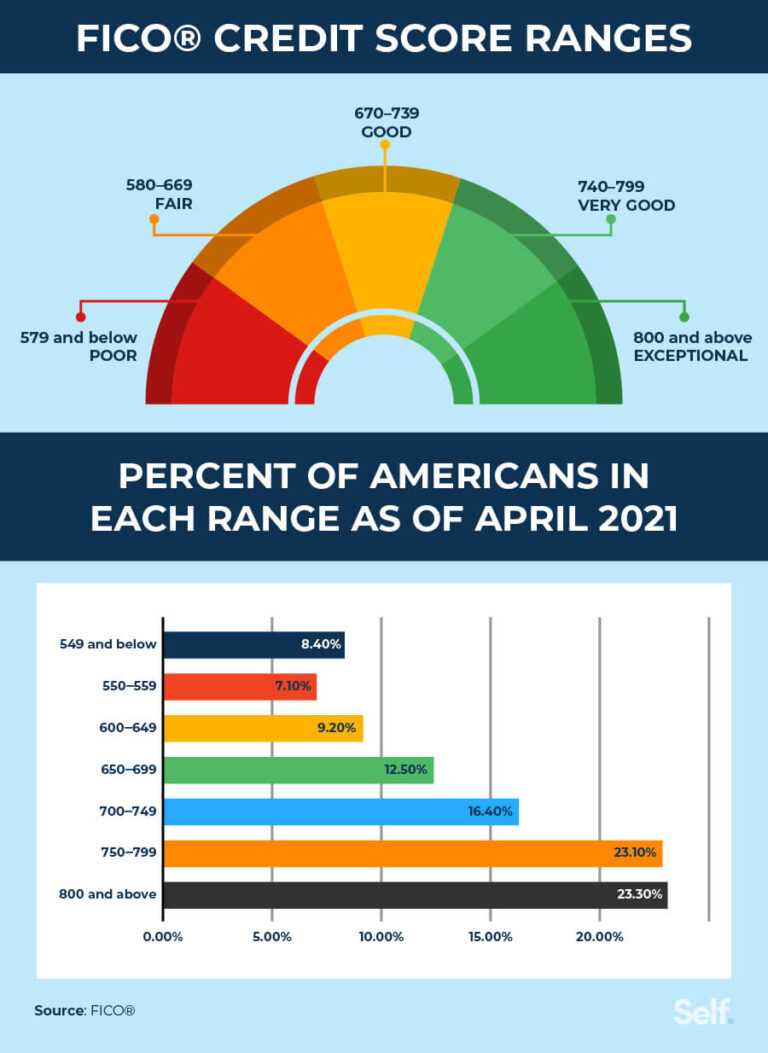

Before we delve into solutions, it’s crucial to understand what "less than perfect" credit truly signifies in the eyes of a lender. Generally, credit scores fall into categories: excellent, good, fair, and poor. A score below 670, and especially below 580 (FICO scale), typically lands you in the "fair" or "poor" category, indicating a higher risk to lenders.

This doesn’t mean you’re uncreditworthy; it simply suggests a history that might include late payments, collections, bankruptcies, or a limited credit history. Lenders use these scores to predict the likelihood of you repaying your loan. A lower score translates to a higher perceived risk, which in turn influences the terms of your loan.

The primary impact you’ll notice with a lower credit score is higher interest rates. Lenders compensate for the increased risk by charging more for the money they lend you. This means your monthly payments will be higher, and the total cost of the car loan over its lifetime will be significantly greater compared to someone with excellent credit.

Furthermore, you might encounter stricter approval criteria. Lenders may require a larger down payment, a co-signer, or shorter loan terms to mitigate their risk. They’ll scrutinize your income, employment stability, and existing debt more closely. Understanding these challenges upfront helps you prepare effectively.

Dispelling Common Myths About Bad Credit Car Loans

The landscape of car loans for less than perfect credit is often shrouded in misconceptions. Let’s tackle some of these myths head-on, so you can approach your search with confidence and clarity.

One prevalent myth is that securing any auto loan with bad credit is impossible. This is simply not true. While it presents more challenges, countless individuals with bruised credit histories successfully obtain car loans every day. The key is knowing where to look and how to present yourself as a reliable borrower.

Another common misconception is that you’re guaranteed to be ripped off or fall victim to predatory lenders. While vigilance is always necessary, there are many reputable lenders who specialize in subprime auto loans. These lenders understand that life happens and people deserve second chances. They operate within fair lending practices, albeit with terms that reflect the perceived risk.

Finally, some believe that having bad credit means you have no options or bargaining power. This is far from the truth. While your options might be narrower, you still have choices. By understanding your financial situation, preparing thoroughly, and comparing offers, you absolutely retain agency in the process. Empowering yourself with knowledge is your best defense and your strongest negotiating tool.

Preparing for Your Car Loan Application: Essential Steps

Success in securing car loans for less than perfect credit hinges on meticulous preparation. This isn’t just about showing up; it’s about proving you’re a responsible borrower ready to commit.

1. Check Your Credit Score and Report

This is the absolute first step. You cannot begin to navigate this process effectively without knowing your starting point. Your credit report provides a detailed history of your borrowing and repayment activities, while your credit score is a numerical representation of that history.

Why it’s important: Understanding your score gives you an idea of what kind of loan terms to expect. More critically, checking your credit report allows you to identify and dispute any errors. Based on my experience, inaccuracies on credit reports are surprisingly common and can unfairly lower your score. Correcting these errors can sometimes significantly improve your standing before you even apply.

How to get it: You are entitled to a free copy of your credit report from each of the three major credit bureaus (Experian, Equifax, and TransUnion) once every 12 months. Visit AnnualCreditReport.com – this is the only federally authorized source for free credit reports. Review each report carefully for discrepancies and follow the instructions provided by the credit bureaus to dispute any incorrect information.

2. Determine Your Realistic Budget

Before you even glance at a car, you need to firmly establish what you can genuinely afford. This goes beyond just the monthly car payment. Consider the holistic cost of car ownership.

Affordability factors: Your budget needs to account for the car payment itself, but also for insurance, fuel costs, routine maintenance, and potential repair expenses. A general rule of thumb is that your total car-related expenses, including the loan payment, should not exceed 10-15% of your net monthly income.

Debt-to-income (DTI) ratio: Lenders will scrutinize your DTI ratio, which compares your total monthly debt payments to your gross monthly income. A high DTI ratio signals that you might be overextended, making new debt a higher risk. Aim for a DTI below 43%, though lower is always better. Pro tips from us: Create a detailed personal budget. Track all your income and expenses for a month or two. This real-world data will give you an accurate picture of your disposable income, preventing you from overcommitting to a car payment you can’t sustain.

3. Save for a Down Payment

A substantial down payment is one of the most powerful tools you have when seeking car loans for less than perfect credit. It significantly improves your chances of approval and can secure more favorable terms.

Benefits of a larger down payment:

- Reduces lender risk: A down payment shows the lender you have "skin in the game" and are serious about your commitment. It also immediately reduces the amount they need to finance, lowering their exposure.

- Lowers your loan amount: This directly translates to lower monthly payments and less interest paid over the life of the loan.

- Builds equity faster: You start with a stronger position against depreciation, reducing the risk of being "upside down" on your loan (owing more than the car is worth).

- Potentially better interest rates: Lenders may offer slightly better rates if they see a significant upfront investment from you.

Aim for at least 10-20% of the car’s purchase price, if possible. Even a 5% down payment is better than nothing. Every dollar you put down reduces your borrowing needs and improves your profile.

4. Gather Necessary Documents

Being prepared with all required paperwork streamlines the application process and demonstrates your seriousness. Don’t wait until you’re at the dealership or lender’s office to scramble for these items.

Common documents include:

- Proof of income: Recent pay stubs (last 2-3 months), W-2 forms, tax returns (if self-employed), or bank statements.

- Proof of residence: Utility bills, lease agreement, or mortgage statements showing your current address.

- Proof of identity: Valid government-issued ID (driver’s license, passport).

- Proof of insurance: While you won’t have the specific car insured yet, proof of existing insurance can sometimes be helpful.

- References: Some lenders may request personal or professional references.

Having these documents neatly organized and readily available will make the application process much smoother and faster.

Exploring Your Lending Options: Where to Look

When your credit isn’t perfect, you need to know where to focus your search for lenders. Not all financial institutions are equally equipped or willing to provide car loans for less than perfect credit.

1. Subprime Lenders/Specialized Auto Lenders

These are often the go-to for individuals with lower credit scores. Subprime lenders specialize in working with borrowers who don’t qualify for traditional prime loans. They understand the nuances of bad credit and have lending models tailored to this demographic.

How they operate: These lenders typically assess risk differently, looking beyond just the credit score to factors like income stability, employment history, and debt-to-income ratio. They might offer loans with higher interest rates and sometimes shorter terms to offset the increased risk.

Benefits and potential downsides: The main benefit is accessibility; they are often your best bet for approval. The downside, as mentioned, is the higher cost of borrowing. It’s crucial to carefully review all terms and conditions to ensure they are manageable and transparent. Always compare offers from multiple subprime lenders.

2. Credit Unions

Often overlooked, credit unions can be excellent alternatives to traditional banks, especially for those with less-than-perfect credit. They are member-owned financial cooperatives, which means their primary focus is on serving their members rather than maximizing profits for shareholders.

Member-focused approach: Credit unions are often more flexible and willing to work with members who have challenging credit histories. They might consider your overall relationship with the credit union, rather than solely relying on your credit score. This can sometimes lead to more favorable interest rates or more lenient terms compared to other lenders.

To apply, you typically need to become a member, which usually involves opening a savings account. It’s worth exploring local credit unions and inquiring about their auto loan options for individuals with your credit profile.

3. Dealership Financing (Buy Here, Pay Here)

Many dealerships offer in-house financing, particularly those that advertise "bad credit, no credit" options. These are often referred to as "Buy Here, Pay Here" (BHPH) dealerships.

How they work: With BHPH, the dealership itself is the lender. This can be convenient as it streamlines the car buying and financing process under one roof. They often have very flexible approval criteria, focusing heavily on your income and ability to make payments.

Pros and cons: The biggest pro is the ease of approval, even with very poor credit or no credit history. However, common mistakes to avoid are jumping into a BHPH loan without understanding the significant downsides. These loans typically come with much higher interest rates, shorter loan terms, and often older, higher-mileage vehicles. Additionally, they may not report your payments to all three credit bureaus, which diminishes their potential for credit building. Always exhaust other lending options before considering BHPH.

4. Co-Signer Option

If you have a trusted individual with excellent credit, a co-signer can significantly improve your chances of approval and potentially secure a better interest rate.

How it works: A co-signer essentially guarantees the loan. If you fail to make payments, they are legally responsible for the debt. This reduces the risk for the lender, as they have a second, more creditworthy party to pursue if you default.

Choosing wisely: This is a serious commitment for both parties. The co-signer’s credit will be affected by the loan, good or bad. Ensure both you and your co-signer fully understand the responsibilities involved. A co-signer should be someone you trust implicitly, and who trusts you to make timely payments.

The Application Process: What to Expect

Navigating the application process for car loans for less than perfect credit requires a strategic approach. It’s more than just filling out forms; it’s about making informed decisions.

1. Pre-Approval: Your Strategic Advantage

Seeking pre-approval is a critical step, especially when dealing with less-than-perfect credit. It empowers you by giving you a clear financial picture before you even set foot on a car lot.

Benefits of pre-approval:

- Know your budget: You’ll understand the maximum loan amount you qualify for, your estimated interest rate, and your potential monthly payments. This prevents you from falling in love with a car you can’t afford.

- Negotiating power: Armed with a pre-approval, you become a cash buyer in the eyes of the dealership. This allows you to focus solely on negotiating the car’s price, rather than getting tangled in financing discussions at the same time.

- Minimize credit impact: Many pre-approvals involve a "soft inquiry" on your credit report, which doesn’t harm your score. Once you choose a specific lender, a "hard inquiry" will occur, but by narrowing down your options, you minimize multiple hard pulls.

2. Comparing Offers

Do not accept the first offer you receive. This is a common mistake that can cost you thousands of dollars over the life of the loan. Actively seek and compare offers from at least 3-5 different lenders.

What to compare:

- Annual Percentage Rate (APR): This is the true cost of borrowing, encompassing the interest rate and other fees. A lower APR is always better.

- Loan Term: Shorter terms mean higher monthly payments but less interest paid overall. Longer terms reduce monthly payments but significantly increase total interest. Find a balance that fits your budget without excessive interest.

- Total Cost of the Loan: Multiply your monthly payment by the number of months in the loan term, then add any upfront fees. This gives you the full picture. Don’t just look at the monthly payment in isolation; a lower monthly payment over a very long term can mean paying far more in total.

3. Negotiating Terms

Even with less-than-perfect credit, you have some room to negotiate. Remember, dealerships and lenders want to make a sale.

Focus your negotiation:

- Car Price: Always negotiate the purchase price of the vehicle first, before discussing financing.

- Interest Rate: If you have multiple pre-approvals, leverage them. Tell one lender about a better offer from another; they might be willing to match or beat it.

- Beware of add-ons: Dealerships often try to upsell you on extended warranties, paint protection, or other accessories. While some might be useful, many are overpriced. Decline anything you don’t genuinely need or can’t get cheaper elsewhere. These add-ons inflate your loan amount and increase the interest you pay.

Choosing the Right Vehicle

With car loans for less than perfect credit, your vehicle choice is more critical than ever. This isn’t the time for luxury or unnecessary features; it’s about practicality and affordability.

Focus on a car that is reliable, fuel-efficient, and within your budget. A used car, especially one a few years old, can be an excellent option. Used cars have already taken the biggest depreciation hit, meaning you get more car for your money and a potentially lower loan amount. This reduces your financial exposure and makes the loan more manageable. Avoid buying more car than you can comfortably afford, as this puts undue stress on your finances and increases the risk of default.

Strategies for Improving Your Credit Score While Repaying

Securing a car loan with bad credit is just the first step; the real long-term win is using this loan to rebuild your credit. Your consistent, responsible payments can significantly improve your credit score over time.

1. Make On-Time Payments – Every Single Time

This is, without a doubt, the most crucial factor in credit building. Payment history accounts for 35% of your FICO score.

Consistency is key: Set up automatic payments from your bank account to ensure you never miss a due date. Even a single late payment (30+ days past due) can severely damage your credit score. Think of each on-time payment as a positive entry on your credit report, steadily building your reliability as a borrower.

2. Keep Your Credit Utilization Low (on other accounts)

While your car loan is an installment loan, your revolving credit accounts (like credit cards) also play a role. Keep your credit card balances as low as possible, ideally below 30% of your available credit limit. High utilization signals financial stress.

3. Avoid New Debt

During the period you’re actively trying to rebuild your credit, try to avoid taking on new loans or opening new credit cards. Each new inquiry and new account can temporarily impact your score. Focus your financial energy on managing your existing debt responsibly.

For more in-depth strategies on credit improvement, check out our guide on . This resource provides actionable steps to accelerate your credit rebuilding journey.

Common Mistakes to Avoid When Getting a Car Loan with Bad Credit

Navigating the subprime auto loan market can be tricky. Being aware of potential pitfalls can save you significant financial heartache.

- Not checking your credit report: As discussed, this leaves you vulnerable to errors and unaware of your true standing.

- Accepting the first offer: Without comparing multiple lenders, you might settle for an exorbitant interest rate or unfavorable terms. Always shop around.

- Buying more car than you can afford: This is a recipe for financial stress and potential default. Stick to your budget, even if it means a less glamorous vehicle.

- Ignoring the total cost of the loan: Focusing solely on the monthly payment can be deceptive. A low monthly payment over an extended term often means paying significantly more in total interest.

- Falling for predatory lenders: Be wary of lenders who guarantee approval without checking anything, pressure you into signing immediately, or have overly vague terms. If it sounds too good to be true, it probably is.

Pro Tips for Long-Term Success

Securing your car loan is a victory, but the journey doesn’t end there. Think long-term to maximize the benefits and improve your financial standing further.

Refinancing Opportunities

Once you’ve made 6-12 months of on-time payments on your car loan, and ideally, your credit score has improved, consider refinancing. Many borrowers with improved credit can qualify for a new loan with a lower interest rate, which can significantly reduce your monthly payments and the total interest paid over the remaining loan term. It’s a smart move to save money and free up cash flow.

Building an Emergency Fund

Unexpected car repairs or other financial setbacks can derail your ability to make car payments. Building an emergency fund provides a crucial safety net. Aim for at least 3-6 months of essential living expenses. This buffer ensures that life’s inevitable curveballs don’t jeopardize your car loan payments or your newly improving credit score.

For more insights into making smart vehicle purchases and financial decisions, explore our article on .

Conclusion: Driving Towards a Brighter Financial Future

Securing car loans for less than perfect credit is undoubtedly a challenge, but it is far from an impossible feat. By arming yourself with knowledge, meticulously preparing your finances, and approaching the process strategically, you can absolutely find a loan that fits your needs and budget.

Remember, this car loan isn’t just a means to get a vehicle; it’s an opportunity. It’s a chance to demonstrate financial responsibility, build a positive payment history, and actively work towards improving your credit score. Each on-time payment is a step forward, paving the way for better financial opportunities in the future. Don’t let past credit issues define your present or future. Take control, prepare diligently, and drive confidently towards your goals.

Have you successfully secured a car loan with less-than-perfect credit? Share your experiences and tips in the comments below – your insights could help others on their journey!