Navigating the Road Ahead: Your Ultimate Guide to Car Loans for Young Adults

Navigating the Road Ahead: Your Ultimate Guide to Car Loans for Young Adults Carloan.Guidemechanic.com

The open road, the freedom of personal transport, the sheer independence of having your own set of wheels – for many young adults, buying a first car is a pivotal life moment. It’s a rite of passage, a symbol of growing up, and an essential tool for education, work, and social life. However, securing a car loan, especially when you’re just starting out, can feel like navigating a complex maze without a map.

This isn’t just about getting a loan; it’s about making a smart financial decision that sets you up for future success. In this super comprehensive guide, we’re going to demystify car loans for young adults, providing you with all the insights, tips, and expert advice you need to confidently drive off the lot with a deal that works for you. Forget the confusion and uncertainty; by the end of this article, you’ll be equipped to handle the process like a seasoned pro.

Navigating the Road Ahead: Your Ultimate Guide to Car Loans for Young Adults

Why Car Loans for Young Adults Can Feel Like an Uphill Battle

Let’s be honest: the financial world isn’t always designed with young adults in mind. When it comes to securing a car loan, lenders often look for a proven track record of financial responsibility. This is where many young individuals hit a roadblock.

The Credit Conundrum: The most significant hurdle is often a lack of established credit history. Lenders use your credit score and history to assess your risk. If you haven’t taken out loans or credit cards before, you simply won’t have a score, or it will be very thin. This makes it difficult for lenders to gauge your reliability as a borrower.

Limited Income and Employment History: Many young adults are still in college, working part-time, or just starting their careers. This can mean a lower income compared to older applicants and potentially a shorter employment history. Lenders prefer stable, consistent income, as it indicates a higher likelihood of on-time payments.

Perception of Risk: From a lender’s perspective, young adults can sometimes be perceived as higher risk. This isn’t a judgment on your character, but rather a statistical observation based on repayment patterns and financial stability over time. Understanding this perspective is the first step in overcoming it.

Based on my experience, many young adults approach this process feeling overwhelmed and undervalued by lenders. However, with the right preparation and knowledge, you can absolutely turn the tables and present yourself as a responsible and attractive borrower.

Building Your Financial Foundation: Before You Even Look at Cars

Before you get caught up in the excitement of test drives and shiny new paint jobs, a crucial first step is to lay a solid financial foundation. This preparation will not only increase your chances of loan approval but also ensure you make a smart, sustainable decision.

1. Understand Your True Budget: Beyond the Monthly Payment

Many first-time car buyers focus solely on the monthly loan payment. This is a common mistake that can lead to financial strain down the line. A car comes with numerous ongoing costs that need to be factored into your budget.

Hidden Costs of Car Ownership:

- Insurance: For young adults, especially those under 25, car insurance can be surprisingly expensive. Get quotes before you commit to a car.

- Fuel: Consider your daily commute and weekend plans. Fuel costs add up quickly.

- Maintenance: Regular oil changes, tire rotations, and unexpected repairs are inevitable. Budget for these.

- Registration and Taxes: Annual fees are required to keep your car legal.

- Parking Fees: If you live in an urban area or work in a city, parking can be a significant expense.

Pro tips from us: Create a detailed spreadsheet of all potential car-related expenses. Be honest with yourself about what you can truly afford each month after all these costs are accounted for. Your car payment should fit comfortably within this budget, not stretch it to its limit.

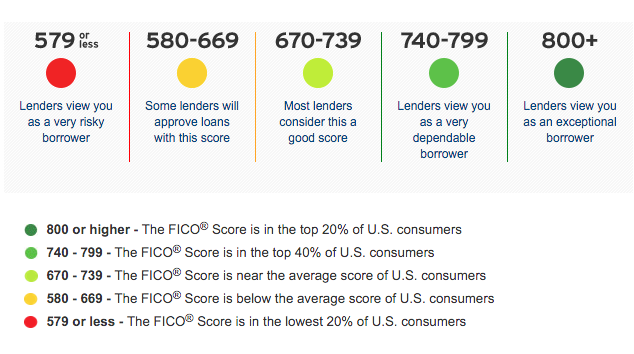

2. Checking Your Credit Score (or Understanding Its Absence)

Your credit score is a three-digit number that summarizes your creditworthiness. For young adults, you might not have one yet, or it might be very low. Don’t panic – this is normal.

If You Have No Credit: This is often referred to as having a "thin file." Lenders have little information to go on. Your strategy will involve proving your reliability in other ways, which we’ll discuss.

If You Have Limited Credit: Perhaps you have a student credit card or a small utility bill history. This is a start! Check your score for free using services like Credit Karma or through your bank. Review your credit report for any errors. Even a limited history can be improved.

Building Credit Proactively: If you have time before buying a car, consider getting a secured credit card. You put down a deposit, and that becomes your credit limit. Using it responsibly and paying it off in full each month is an excellent way to start building a positive credit history.

3. The Power of a Down Payment

Saving for a down payment is one of the smartest moves a young adult can make when buying a car. It offers several significant advantages.

Reducing Your Loan Amount: A larger down payment means you’re borrowing less money, which translates to lower monthly payments and less interest paid over the life of the loan.

Improving Your Loan Terms: Lenders view a substantial down payment as a sign of financial commitment and responsibility. This can make you a more attractive borrower, potentially leading to a lower interest rate.

Reducing "Upside Down" Risk: Cars depreciate rapidly. A down payment helps prevent you from owing more on the car than it’s worth (being "upside down" or "underwater") early in the loan term. This is particularly important if you ever need to sell the car before the loan is paid off.

Aim for at least 10-20% of the car’s purchase price as a down payment if possible. Even a smaller down payment is better than none.

4. Gathering Necessary Documents

Lenders will require specific documents to verify your identity, income, and residency. Having these ready will streamline the application process.

Typical Documents Include:

- Proof of Identity: Driver’s license, passport.

- Proof of Income: Recent pay stubs (2-3 months), W-2 forms, tax returns if self-employed, bank statements.

- Proof of Residency: Utility bills, lease agreement, bank statements showing your address.

- Social Security Number: For credit checks.

- Vehicle Information: If you’ve already picked out a car (make, model, VIN).

Common mistakes to avoid are showing up without all your paperwork. This can delay your application and even make you appear unprepared, which doesn’t instill confidence in lenders.

Navigating the Loan Landscape: Types of Car Loans for Young Adults

Understanding where to get your loan is just as important as knowing how to prepare for it. Different lenders offer different terms and have varying criteria.

1. Traditional Banks and Credit Unions

These are often excellent starting points for car loans.

Banks: Large financial institutions that offer a wide range of loan products. They typically have competitive rates for well-qualified borrowers. However, they might be stricter on credit history for young adults.

Credit Unions: Member-owned financial cooperatives. They are known for often having lower interest rates and more flexible lending criteria, especially for members. If you’re a student or have family members who are part of a credit union, it’s definitely worth exploring. They often prioritize relationships and community over strict credit scores.

Pros: Generally competitive rates, established reputation, clear terms.

Cons: Can be stricter on credit history, especially for young adults with limited or no credit.

2. Dealership Financing

Most car dealerships offer in-house financing or work with a network of lenders. This can be convenient, as you can apply for the loan and buy the car all in one place.

Pros: Convenience, ability to sometimes get approved even with limited credit (dealers have access to subprime lenders), potential for promotional rates on new cars.

Cons: Interest rates can sometimes be higher, less transparency in negotiations (you’re negotiating the car price and loan terms simultaneously), potential for pushy sales tactics.

Based on my experience, it’s always best to secure pre-approval from a bank or credit union before stepping into a dealership. This gives you a benchmark and strengthens your negotiating position.

3. Co-signer Loans: A Powerful Ally

For young adults with little or no credit, a co-signer can be a game-changer. A co-signer is someone (usually a parent or guardian) with good credit who agrees to be equally responsible for the loan.

How it Works: If you fail to make payments, the lender can pursue the co-signer for the debt. This significantly reduces the risk for the lender, making them more likely to approve your loan and offer better terms.

Benefits:

- Increased chance of approval.

- Potentially lower interest rates.

- An opportunity to build your own credit history.

Risks:

- For the Co-signer: Their credit score will be impacted if you miss payments. They are legally obligated to pay if you default. It can strain relationships.

- For You: A missed payment impacts both your credit and your co-signer’s, creating potential tension.

Pro tips from us: Only consider a co-signer if you are absolutely confident in your ability to make every payment on time. Have an open and honest conversation with your co-signer about the responsibilities and risks involved.

4. Bad Credit / No Credit Loans (Specialty Lenders)

If traditional routes aren’t working, some lenders specialize in loans for individuals with poor or no credit. These are often referred to as "subprime" lenders.

What to Expect:

- Higher Interest Rates: Significantly higher, reflecting the increased risk to the lender.

- Shorter Loan Terms: To reduce the total interest paid, but this means higher monthly payments.

- Stricter Requirements: They might require a larger down payment or collateral.

Common mistakes to avoid are falling prey to predatory lenders. Be wary of "guaranteed approval" schemes, excessively high fees, or lenders who pressure you into signing without fully understanding the terms. Always compare offers and read the fine print.

The Application Process: A Step-by-Step Guide

Once you’ve done your homework, it’s time to put your plan into action. The application process doesn’t have to be intimidating.

1. Researching Lenders and Comparing Offers

Don’t just go with the first offer you receive. This is perhaps the most important step in securing a favorable car loan.

Shop Around: Apply to multiple banks, credit unions, and even online lenders. Each will have different criteria and rates.

Focus on APR: The Annual Percentage Rate (APR) is the true cost of borrowing, as it includes both the interest rate and any fees. A lower APR means less money out of your pocket over the life of the loan.

Internal Link: For a deeper dive into comparing different loan types, you might find our guide, "," helpful.

2. The Power of Pre-Approval

Getting pre-approved for a loan before you visit a dealership is a game-changer.

What is Pre-Approval? A lender reviews your financial information and tentatively agrees to lend you a certain amount at a specific interest rate, subject to final verification and vehicle approval.

Benefits:

- Know Your Budget: You’ll know exactly how much you can afford, preventing you from falling in love with a car outside your price range.

- Stronger Negotiating Position: You walk into the dealership as a cash buyer, effectively, as you already have financing secured. This allows you to negotiate the car’s price separately from the loan terms.

- Reduces Stress: You can focus on finding the right car, not scrambling for financing.

3. Submitting Your Application

Once you’ve chosen a lender and are ready to apply, ensure all your documents are in order.

Be Honest and Thorough: Provide accurate information. Any discrepancies can lead to delays or rejection.

Highlight Your Strengths: Even if you have limited credit, emphasize any positive financial habits. Do you have a steady job? A good savings record? A history of paying rent on time? These can all be mentioned.

External Link: For more detailed information on credit scores and how they impact loan applications, visit the Consumer Financial Protection Bureau’s excellent resource on understanding your credit.

4. Understanding the Loan Offer

Once you receive a loan offer, scrutinize every detail before signing.

Key Elements to Review:

- APR (Annual Percentage Rate): As discussed, this is the total cost.

- Loan Term: The length of the loan (e.g., 36, 48, 60 months). Longer terms mean lower monthly payments but more interest paid over time.

- Total Cost of the Loan: Multiply your monthly payment by the number of months, then add any fees. This gives you the full picture.

- Any Fees: Origination fees, processing fees, early repayment penalties.

Pro tips from us: Never feel rushed into signing. Take the loan offer home, review it carefully, and don’t hesitate to ask questions about anything you don’t understand.

Common Mistakes Young Adults Make (and How to Avoid Them)

Securing a car loan is a significant financial step. Avoiding common pitfalls can save you stress and money in the long run.

1. Not Budgeting Properly

As mentioned, focusing only on the monthly payment is a recipe for disaster. Failing to account for insurance, maintenance, and fuel can lead to missed payments and financial distress.

How to Avoid: Create a comprehensive budget that includes all car-related expenses before you even start shopping. Stick to it rigorously.

2. Ignoring the APR

The interest rate sounds simple, but the APR includes all costs. A low interest rate with high fees can be worse than a slightly higher interest rate with no fees.

How to Avoid: Always compare offers based on the APR, not just the advertised interest rate. This gives you the true cost of borrowing.

3. Impulse Buying

Getting swept up in the excitement of a new car can lead to poor financial decisions. You might accept unfavorable loan terms just to drive off the lot.

How to Avoid: Do your research. Stick to your budget. Get pre-approved. Don’t let a salesperson pressure you into a quick decision.

4. Not Reading the Fine Print

Loan documents can be lengthy and full of jargon. Skipping over them can lead to nasty surprises later.

How to Avoid: Read every single word of your loan agreement. Ask for clarification on anything you don’t understand. If something doesn’t feel right, walk away.

5. Over-relying on a Co-signer

While a co-signer can be a huge help, remember that the primary responsibility is yours. Treat the loan as if you’re the only one responsible for it.

How to Avoid: Understand the full implications for your co-signer. Make every payment on time, not just for your credit, but for your relationship.

Beyond the Loan: Building Credit and Financial Responsibility

Securing a car loan as a young adult is more than just getting a vehicle; it’s an incredible opportunity to build a strong financial future.

1. How a Car Loan Can Build Credit

When you make your car loan payments on time, every single month, this positive activity is reported to the credit bureaus. Over time, this consistent positive reporting will:

- Establish a Credit History: If you had no credit, you’re now building one.

- Improve Your Credit Score: If you had limited credit, on-time payments will steadily increase your score.

- Diversify Your Credit Mix: A car loan is an installment loan, which differs from revolving credit (like credit cards). Having a mix of credit types can positively impact your score.

A well-managed car loan demonstrates to future lenders that you are a reliable borrower, making it easier to get approved for mortgages, personal loans, or better credit card offers down the line.

2. Making Payments on Time, Every Time

This cannot be stressed enough. Timely payments are the bedrock of good credit. Set up automatic payments from your bank account to ensure you never miss a due date. If you anticipate a challenge, contact your lender before the payment is due to discuss options.

Internal Link: For more guidance on managing debt and building good financial habits, check out our article, "."

3. Financial Literacy for the Future

Your first car loan is a real-world lesson in personal finance. Embrace it as a learning experience. Understanding interest rates, amortization schedules, and the impact of debt will serve you well for the rest of your life. The skills you develop now in budgeting, saving, and responsible borrowing are invaluable.

Driving Forward with Confidence

Buying a car and securing a loan as a young adult is a significant milestone, fraught with both excitement and potential challenges. However, by arming yourself with knowledge, being diligent in your preparation, and making informed decisions, you can navigate this process successfully.

Remember, this journey is about more than just getting a set of keys; it’s about establishing your financial independence and building a foundation for a responsible and prosperous future. Take your time, ask questions, and don’t be afraid to walk away from a deal that doesn’t feel right. With this guide, you now have the tools to secure the best car loans for young adults and drive confidently towards your goals. Start planning today, and take control of your financial destiny!