Navigating the Road Ahead: Your Ultimate Guide to Getting a Car Loan with Bad Credit

Navigating the Road Ahead: Your Ultimate Guide to Getting a Car Loan with Bad Credit Carloan.Guidemechanic.com

Embarking on the journey to purchase a car is an exciting prospect, offering freedom, convenience, and independence. However, for many individuals, the dream of a new set of wheels can quickly turn into a daunting challenge, especially when faced with the hurdle of a less-than-perfect credit score. The phrase "bad credit" often conjures images of rejection letters and closed doors, making the idea of securing a car loan seem impossible.

But here’s the good news: getting a car loan with bad credit is absolutely achievable. It requires a strategic approach, thorough preparation, and a clear understanding of the auto financing landscape. This comprehensive guide is designed to empower you with the knowledge, tips, and strategies needed to successfully navigate the process, secure a favorable loan, and drive away in the car you need. We’ll dive deep into every aspect, from understanding your credit to rebuilding it after your purchase, ensuring you have all the tools for success.

Navigating the Road Ahead: Your Ultimate Guide to Getting a Car Loan with Bad Credit

Understanding "Bad Credit" in the Auto Loan World

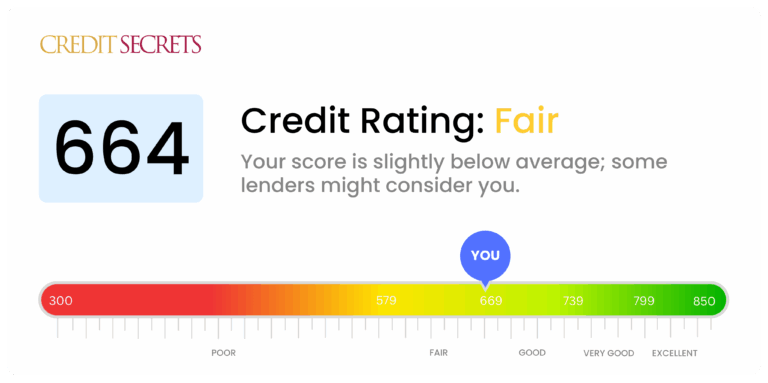

Before we delve into solutions, it’s crucial to grasp what "bad credit" truly means in the context of car loans. Lenders primarily use your credit score as a snapshot of your financial reliability. FICO scores, for instance, typically range from 300 to 850. Generally, a score below 620 is considered "subprime" or "bad credit" by most auto lenders.

Why do lenders care so much? A low credit score signals a higher risk. It suggests a history of missed payments, high debt, or past financial difficulties, making lenders cautious about extending new credit. They perceive a greater chance that you might default on your loan.

However, the auto loan market is vast and diverse. There’s a significant segment dedicated to bad credit car loans, also known as subprime auto loans. These loans are specifically designed for individuals with lower credit scores. While they come with their own set of considerations, primarily higher interest rates, they represent a vital pathway for many to obtain vehicle financing.

Preparing for Your Bad Credit Car Loan Journey

Success in securing a car loan with bad credit starts long before you step onto a dealership lot or click "apply" online. Preparation is your most powerful tool. It allows you to approach lenders from a position of strength, even with a challenging credit history.

1. Know Your Credit Score and Report Inside Out

This is the absolute first step. You cannot fix what you don’t understand. Your credit report contains a detailed history of your borrowing and repayment habits, while your credit score is a numerical representation derived from this data.

Based on my experience, many people skip this crucial first step, only to be surprised by what lenders see. Obtain free copies of your credit report from all three major bureaus (Equifax, Experian, Transunion) through AnnualCreditReport.com. Scrutinize every entry. Look for errors, such as accounts that aren’t yours, incorrect payment statuses, or outdated information. Disputing and correcting these errors can potentially boost your score quickly.

Understanding your report also helps you identify areas for improvement. You’ll see which accounts are hurting you most and can address them strategically.

2. Budget Realistically: What Can You Truly Afford?

Securing a loan is one thing; affording it is another. A common mistake is focusing solely on the monthly payment without considering the total cost of ownership. This includes not just the loan principal and interest, but also insurance, fuel, maintenance, and potential repair costs.

Pro tips from us: Create a detailed monthly budget. List all your income and expenses. Determine how much you can comfortably allocate to car-related costs without straining your finances. Remember, an affordable payment today ensures you don’t fall behind tomorrow, which could further damage your credit. Don’t forget that a higher interest rate on a bad credit car loan means more of your payment goes towards interest, especially at the beginning of the loan term.

3. Save, Save, Save for a Down Payment

A significant down payment is arguably one of the most impactful strategies when getting a car loan with bad credit. It demonstrates your commitment to the loan and reduces the amount you need to borrow, which in turn lowers the lender’s risk.

The benefits are manifold: a larger down payment can lead to a smaller loan amount, lower monthly payments, and potentially a better interest rate. It also provides immediate equity in your vehicle, protecting you against depreciation. Aim for at least 10-20% of the car’s purchase price if possible. Even a few hundred dollars can make a difference in showing a lender your seriousness.

4. Gather All Necessary Documents

Lenders will require a range of documents to verify your identity, income, and residency. Having these prepared in advance streamlines the application process and shows you are organized and serious.

Typical documents include:

- Proof of identity (driver’s license, state ID)

- Proof of residency (utility bill, lease agreement)

- Proof of income (pay stubs from the last few months, tax returns if self-employed)

- Bank statements

- References (sometimes required for subprime loans)

Strategies to Improve Your Chances of Approval

Even with bad credit, there are several powerful strategies you can employ to make your application more appealing to lenders. These go beyond basic preparation and actively mitigate the perceived risk associated with your credit history.

1. Leverage a Significant Down Payment

As mentioned, a substantial down payment is your best friend when seeking a car loan for bad credit. It directly reduces the lender’s exposure. If you put down 20% of the vehicle’s value, the lender is only financing 80%, making the loan less risky from their perspective.

A larger down payment also reduces your monthly payments and the total amount of interest you’ll pay over the life of the loan. This is especially crucial with the higher interest rates typically associated with subprime auto loans. Think of it as investing in your own financial future.

2. Consider a Co-signer with Good Credit

Finding a co-signer with excellent credit can dramatically increase your chances of approval and potentially secure a much better interest rate. A co-signer legally agrees to be responsible for the loan if you default, providing an extra layer of security for the lender.

Pro tips from us: A co-signer should be someone you trust implicitly, and who trusts you. They need to understand the full implications and risks involved, as their credit will also be impacted if payments are missed. Discuss this openly and honestly with any potential co-signer. It’s a significant favor, and clear communication is paramount. Remember, if you fall behind on payments, it will affect both your credit scores.

3. Choose the Right Vehicle (Affordable and Practical)

While you might dream of a luxury SUV, a more modest and reliable vehicle is a wiser choice when working with bad credit. Lenders prefer to finance cars that are easily resellable and hold their value reasonably well.

Opt for a reliable, used car that fits comfortably within your budget, even with higher interest rates. Avoid vehicles that are known for expensive repairs or rapid depreciation. A practical choice reduces your overall financial burden and helps ensure you can make your payments consistently. This is a stepping stone, not necessarily your forever car.

4. Demonstrate Stability: Job History and Residency

Lenders look for stability as a sign of your ability to make consistent payments. A long, stable employment history and consistent residency at the same address tell a story of reliability.

Be prepared to provide documentation proving your employment history (pay stubs, employer contact information) and residency (utility bills, lease agreements). If you’ve recently changed jobs or moved, be ready to explain the circumstances. The more stable your life appears, the more confident a lender will be in your ability to repay.

5. Address Your Debt-to-Income Ratio

Your debt-to-income (DTI) ratio is a critical factor for lenders. It compares your total monthly debt payments to your gross monthly income. A high DTI indicates that too much of your income is already allocated to existing debt, leaving less for a new car loan.

Lenders typically prefer a DTI of 43% or lower, though this can vary. While you might not be able to drastically reduce your debt overnight, understanding your DTI allows you to explain it or show efforts to manage it. Reducing other small debts before applying can significantly improve this ratio and your chances of approval.

Where to Find a Car Loan with Bad Credit

The landscape of auto financing for individuals with bad credit has expanded significantly. No longer are your options limited to just a few places. Knowing where to look can save you time, frustration, and potentially money.

1. Specialized Dealerships (Buy Here, Pay Here)

"Buy Here, Pay Here" (BHPH) dealerships are specifically set up to offer in-house financing, often to customers with poor or no credit. They act as both the seller and the lender, making the process very convenient.

Pros: High approval rates, often don’t check traditional credit scores, quick approval.

Cons: Typically much higher interest rates, limited vehicle selection, vehicles may be older with higher mileage, payments are often weekly or bi-weekly.

Common mistakes to avoid are rushing into a BHPH loan without fully understanding the terms. Always compare their offer to other options, if available, and ensure the vehicle is thoroughly inspected by an independent mechanic.

2. Online Lenders Specializing in Subprime Loans

The digital age has brought a wealth of online lenders who specialize in subprime auto loans. These platforms often have a more streamlined application process and can provide pre-qualification without a hard credit inquiry.

Pros: Convenience (apply from home), quick decisions, comparison shopping is easier, some offer pre-qualification without impacting your credit score.

Cons: May require more self-advocacy, can be overwhelming with choices, interest rates are still generally higher than prime loans.

Based on my experience, online lenders can be a great starting point for individuals with bad credit. They often have more flexible criteria than traditional banks and can quickly give you an idea of what you qualify for.

3. Credit Unions

Credit unions are member-owned financial institutions known for their community focus and often more flexible lending criteria than large banks. If you’re a member or eligible to become one, they can be an excellent option.

Pros: Potentially lower interest rates than other subprime lenders, more personalized service, may be more willing to work with members with challenging credit.

Cons: Requires membership, typically a smaller institution with fewer branches, may still have strict approval criteria for very low scores.

4. Traditional Banks (More Challenging, but Possible)

While traditional banks are often the toughest nut to crack with bad credit, they shouldn’t be entirely ruled out, especially if you have a relationship with one. If you have a stable job, a good down payment, or a strong co-signer, your existing bank might consider your application.

Pros: Generally the lowest interest rates if approved, established reputation.

Cons: Stricter credit score requirements, approval is less likely with truly bad credit without significant mitigating factors.

Navigating the Application and Approval Process

Once you’ve done your preparation and identified potential lenders, it’s time to apply. This stage requires careful attention to detail and a strategic mindset.

1. Pre-qualification vs. Pre-approval: Know the Difference

It’s vital to understand these terms. Pre-qualification is a soft inquiry that gives you an estimate of what you might qualify for, without impacting your credit score. It’s a great way to gauge your options. Pre-approval, on the other hand, is a more thorough review (often involving a hard credit inquiry) that results in a conditional offer for a specific loan amount and interest rate.

From my perspective as an expert blogger, this is where many people get overwhelmed. Aim for pre-qualification first to explore options. Once you’re serious about a specific vehicle and lender, pursue pre-approval. Having a pre-approval letter in hand gives you significant negotiating power at the dealership, as you know your financing terms upfront.

2. Understanding Loan Offers: APR, Loan Term, Total Cost

When reviewing loan offers, don’t just look at the monthly payment. Focus on the Annual Percentage Rate (APR), which includes the interest rate plus any fees, giving you the true cost of borrowing. Also, consider the loan term (how long you have to pay it back).

A longer loan term might mean lower monthly payments, but it also means you’ll pay significantly more in interest over time. With a bad credit car loan, where interest rates are already high, extending the term too much can lead to paying double or triple the car’s value. Always calculate the total cost of the loan (monthly payment x loan term + down payment).

3. Reading the Fine Print: Hidden Fees and Penalties

Loan agreements can be complex. Take your time to read every single line of the contract before signing. Look out for origination fees, prepayment penalties (though less common in auto loans), late payment fees, and any other charges that might increase your overall cost.

If anything is unclear, ask for clarification. Don’t be afraid to walk away if you feel pressured or if the terms seem predatory. Transparency is key.

4. Negotiating: Not Just the Car Price, But Loan Terms Too

Many people think negotiation only applies to the car’s price. However, you can also negotiate loan terms, especially if you have multiple offers. If a dealership knows you’re pre-approved elsewhere, they might be more willing to match or beat those terms to secure your business.

Remember, the dealership makes money on both the car sale and the financing. Use this to your advantage. Focus on the out-the-door price of the car and then on the APR and loan term separately.

Post-Loan: Rebuilding Your Credit

Securing a car loan with bad credit isn’t just about getting a vehicle; it’s a golden opportunity to rebuild your credit score. This loan, if managed responsibly, can be a powerful tool for improving your financial standing.

1. Make Timely Payments, Every Single Time

This is the most critical step. Your payment history accounts for 35% of your FICO score. Every on-time payment you make will positively impact your credit report and gradually increase your score.

Pro tips from us: Set up automatic payments from your bank account to ensure you never miss a due date. If possible, consider paying slightly more than the minimum monthly payment. This helps reduce the principal faster and saves you money on interest in the long run. Even if you’re only paying an extra $5 or $10, it adds up.

2. Monitor Your Credit for Improvements

Regularly check your credit report to see the positive impact of your timely car loan payments. As your score improves, you’ll gain access to better financial products and lower interest rates in the future.

Seeing your score rise can be incredibly motivating and reinforces good financial habits. It also allows you to catch any new errors that might appear.

3. Future Credit Opportunities: Refinancing and Beyond

As your credit score improves, you might qualify for better interest rates. Consider refinancing your bad credit car loan after 12-18 months of consistent, on-time payments. Refinancing can significantly reduce your monthly payments and the total interest paid over the life of the loan.

This positive payment history also opens doors to other credit opportunities, like credit cards with better terms or even a mortgage, helping you achieve broader financial goals. Your car loan becomes a stepping stone to a healthier financial future.

Conclusion: Your Path to Car Ownership is Clear

Getting a car loan with bad credit might seem like an uphill battle, but with the right knowledge and a strategic approach, it’s a completely surmountable challenge. This journey is not just about acquiring a car; it’s about taking control of your financial narrative and rebuilding your credit for a brighter future.

Remember, preparation is key: know your credit, budget wisely, and save for a down payment. Utilize strategies like co-signers and choosing an affordable vehicle to strengthen your application. Explore all your lending options, from online specialists to credit unions. Most importantly, once you secure your bad credit car loan, commit to making every payment on time. This dedication will not only secure your vehicle but also pave the way for a stronger credit score and improved financial health.

Don’t let a past financial setback define your future mobility. Take these steps, empower yourself with information, and drive confidently towards your car ownership goals. The road ahead is open, and with perseverance, you’re well on your way.