Navigating the Road Ahead: Your Ultimate Guide to Poor Credit Car Loans

Navigating the Road Ahead: Your Ultimate Guide to Poor Credit Car Loans Carloan.Guidemechanic.com

Securing a car loan when your credit score isn’t perfect can feel like trying to climb a mountain in flip-flops. Many individuals find themselves in this challenging situation, perhaps due to past financial setbacks, unexpected life events, or simply a lack of credit history. The good news? Having poor credit doesn’t automatically mean you’re destined for public transportation forever.

This comprehensive guide is designed to be your definitive roadmap, offering invaluable insights and actionable strategies for navigating the world of poor credit car loans. We’ll demystify the process, equip you with the knowledge to make informed decisions, and empower you to drive away with a vehicle that meets your needs while also setting you on a path to financial recovery. Our ultimate goal is to transform what seems like an impossible hurdle into a manageable step towards your automotive independence.

Navigating the Road Ahead: Your Ultimate Guide to Poor Credit Car Loans

Understanding the Landscape: What Exactly is "Poor Credit"?

Before we delve into solutions, it’s crucial to understand what "poor credit" actually signifies in the eyes of lenders. Your credit score, primarily FICO and VantageScore, is a three-digit number that summarizes your creditworthiness based on your financial history. It’s a snapshot of your ability to manage debt responsibly.

Generally, a FICO score below 600-620 is considered "poor" or "subprime." Scores in this range signal to lenders a higher risk of default, making them more hesitant to approve loans, or leading them to offer less favorable terms. This isn’t a judgment on your character, but rather a statistical assessment of risk.

Several factors can contribute to a poor credit score. These often include a history of late payments, loan defaults, bankruptcies, repossessions, or an excessive amount of outstanding debt. For some, the issue isn’t negative history, but rather a lack of any credit history at all, which lenders view similarly to poor credit because there’s no track record to evaluate.

The impact of poor credit extends beyond just car loans. It can affect your ability to rent an apartment, get a mortgage, or even secure certain jobs. However, for the purpose of this article, we’ll focus on its specific implications for automotive financing, where lenders use this score to determine their risk exposure and, consequently, the interest rate they’re willing to offer.

Is Getting a Car Loan with Poor Credit Even Possible? (The Resounding Yes!)

Let’s address the elephant in the room: many people mistakenly believe that poor credit means an automatic "no" from every car lender. Based on my experience in the automotive financing world, this simply isn’t true. While it presents a greater challenge, securing a car loan with poor credit is absolutely possible and happens every single day for countless individuals.

The key isn’t to ask if it’s possible, but how to make it happen strategically. Lenders understand that life happens, and not everyone has a perfect financial past. There’s a significant segment of the lending industry specifically dedicated to subprime auto loans, designed for individuals with less-than-ideal credit scores.

These specialized lenders assess risk differently and often look at a broader range of factors beyond just your credit score. They might place more emphasis on your current income stability, your down payment, or the overall debt-to-income ratio. Your job is to present yourself as the most reliable borrower possible within your current circumstances.

Preparing for Your Poor Credit Car Loan Journey: Laying the Groundwork

Success in securing a poor credit car loan hinges on thorough preparation. Walking into a dealership or contacting a lender without understanding your financial standing is a common mistake that can lead to frustration and unfavorable terms. Think of this preparation phase as building a strong foundation for your future vehicle purchase.

1. Know Your Credit Report Inside Out

Your credit report is the most crucial document in this process. It details your borrowing history, payment patterns, and any public records like bankruptcies. Before you even think about applying for a loan, obtain a copy of your credit report from all three major credit bureaus: Experian, Equifax, and TransUnion. You are entitled to a free report from each once a year via AnnualCreditReport.com.

Review these reports meticulously for any inaccuracies. Common errors can include accounts that aren’t yours, incorrect payment statuses, or outdated information. Disputing these errors can potentially boost your score, even if only by a few points, which can make a difference in your loan terms. This process can take time, so start early.

2. Craft a Realistic Budget: What Can You Truly Afford?

This step is non-negotiable. Don’t just consider the monthly car payment; think about the total cost of car ownership. This includes fuel, insurance (which can be significantly higher with poor credit), maintenance, registration, and potential repairs. Using a budget planner will help you determine a comfortable monthly payment range that won’t strain your finances.

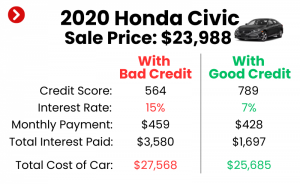

A common mistake is to focus solely on the lowest possible monthly payment without considering the total interest paid over the life of the loan. With poor credit, interest rates will be higher, so a longer loan term to achieve a lower payment can dramatically increase the overall cost of the vehicle. Be realistic about what you can afford each month without compromising other essential expenses.

3. Prioritize a Substantial Down Payment

For poor credit car loans, a significant down payment is your best friend. It immediately reduces the amount you need to borrow, which lowers the lender’s risk. A smaller loan amount means you’ll pay less interest over time and often makes lenders more willing to approve your application.

Aim for at least 10-20% of the vehicle’s purchase price, if possible. Even a smaller down payment is better than none. Showing a lender that you have capital to invest demonstrates your commitment and financial responsibility. Pro tips from us include saving diligently or even selling an existing, less reliable vehicle to generate down payment funds.

4. Understand Your Trade-In Value (If Applicable)

If you plan to trade in your current vehicle, research its market value beforehand. Websites like Kelley Blue Book (KBB) or Edmunds can provide estimated values based on its condition, mileage, and features. Knowing this value gives you leverage during negotiations and allows you to factor it into your overall budget.

A trade-in acts similarly to a down payment, reducing the amount you need to finance. Be honest about your vehicle’s condition when getting an estimate, as dealerships will conduct their own inspections. Having a realistic expectation prevents disappointment and helps you prepare for the financial aspects of your new purchase.

Finding the Right Lender for Poor Credit Car Loans

Not all lenders are created equal, especially when it comes to poor credit financing. Your approach to finding a lender should be strategic, focusing on those who specialize in or are open to working with individuals with lower credit scores.

1. Explore Specialized Lenders and Dealerships

Many dealerships work with a network of lenders, some of whom specialize in subprime auto loans. These "special finance" departments are equipped to handle applications from individuals with poor credit. They understand the nuances of these situations and can often find a suitable financing option.

"Buy Here, Pay Here" (BHPH) dealerships are another option, as they finance loans directly in-house. While convenient, these often come with significantly higher interest rates and less consumer protection. Based on my experience, BHPH should generally be a last resort, and if you go this route, scrutinize the terms and conditions very carefully.

2. Consider Credit Unions

Credit unions are member-owned financial institutions that often offer more flexible lending criteria and competitive rates compared to traditional banks, even for those with poor credit. They tend to have a more personal approach and may be more willing to look beyond just your credit score, considering your overall financial picture as a member.

Joining a credit union is typically straightforward, often requiring just a small deposit. It’s worth exploring their auto loan options before approaching other lenders, as they can sometimes offer surprisingly good terms.

3. Online Lenders and Lending Marketplaces

The digital age has brought a plethora of online lenders and lending marketplaces that specialize in poor credit car loans. These platforms allow you to compare offers from multiple lenders without multiple hard inquiries on your credit report. They offer convenience and transparency, enabling you to shop from home.

Many online lenders offer pre-qualification, which allows you to see potential loan terms without impacting your credit score. This is an excellent way to gauge your options before committing to a full application.

Pre-qualification vs. Pre-approval: Understanding the Difference

It’s vital to distinguish between these two terms. Pre-qualification is a soft credit check that gives you an estimate of what you might be approved for. It doesn’t affect your credit score and is great for initial research. Pre-approval, on the other hand, involves a hard credit inquiry and provides a firm loan offer, subject to final verification. Getting pre-approved from one or two reputable lenders gives you significant negotiating power at the dealership.

Pro Tip: Avoid applying to too many lenders at once. While comparison shopping is good, multiple hard inquiries in a short period can further ding your credit score. Focus on one or two strong pre-qualification offers before pursuing a full pre-approval.

Strategies to Improve Your Chances of Approval & Get Better Terms

Even with poor credit, there are proactive steps you can take to make your application more attractive to lenders and potentially secure more favorable loan terms.

1. Maximize Your Down Payment

As mentioned earlier, a larger down payment is arguably the most impactful factor. It directly reduces the lender’s risk exposure. For example, if you’re financing a $15,000 car and put down $3,000, the lender is only on the hook for $12,000. This significantly improves your standing compared to someone putting down nothing.

Consider waiting a bit longer to save up more funds if it means a substantial down payment. The long-term savings in interest and the higher likelihood of approval often outweigh the immediate desire for a new car.

2. Consider a Cosigner (with Caution)

A cosigner with good credit can significantly bolster your application. Their creditworthiness acts as a guarantee for the loan, assuring the lender that if you default, they will be responsible for repayment. This reduces the lender’s risk and can lead to lower interest rates.

However, choosing a cosigner is a serious decision. The loan will appear on their credit report, and any late or missed payments will negatively impact their credit, not just yours. Ensure you have an extremely reliable payment plan and open communication with your cosigner to protect both your credit and your relationship.

3. Opt for a Slightly Older or Less Expensive Car

While you might dream of a brand-new luxury vehicle, with poor credit, practicality should be your guiding principle. Financing a less expensive, perhaps slightly older, but still reliable car reduces the total loan amount. This, in turn, makes the loan less risky for the lender and more manageable for you.

A lower loan amount also means lower monthly payments, which is crucial for demonstrating consistent on-time payments and rebuilding your credit. Think of your first poor credit car loan as a stepping stone, not your forever car.

4. Provide Proof of Stable Income

Lenders want to see that you have a consistent and sufficient income to cover your monthly car payments. Be prepared to provide documentation such as pay stubs, bank statements, or tax returns. Stable employment for at least six months, or preferably a year, can significantly strengthen your application.

Even if your income isn’t exceptionally high, demonstrating its reliability and consistency is key. Lenders prioritize predictability when assessing your ability to repay.

5. Understand Your Debt-to-Income (DTI) Ratio

Your debt-to-income ratio is a crucial metric. It’s the percentage of your gross monthly income that goes towards paying your monthly debt payments (credit cards, student loans, mortgage, etc.). Lenders prefer a DTI ratio below 43%, as it indicates you have enough disposable income to handle new debt.

A high DTI suggests you’re already stretched thin, making new loan approval challenging. If your DTI is high, consider paying down other debts before applying for a car loan. Even a small reduction can make a difference.

The Application Process for Poor Credit Car Loans: What to Expect

Once you’ve done your preparation, the application process itself is fairly straightforward, but requires attention to detail.

Gather all necessary documents beforehand. This typically includes:

- Proof of identity (driver’s license)

- Proof of residence (utility bill)

- Proof of income (pay stubs, bank statements)

- Proof of insurance

- Trade-in title (if applicable)

Be completely honest on your application. Any misrepresentations can lead to immediate denial or, worse, legal trouble. Lenders will verify the information you provide, so transparency is always the best policy. Read all terms and conditions carefully, understanding the interest rate, loan term, and any fees associated with the loan.

Navigating the Dealership Experience with Poor Credit

Walking into a dealership with poor credit can feel intimidating, but remember, you’ve prepared for this. Being informed and confident is your best defense.

Be prepared for scrutiny regarding your financial situation. Dealerships are businesses, and they need to assess risk. Don’t be offended by questions about your employment history or current financial obligations; it’s part of their process.

Don’t settle for the first offer. Even with poor credit, there’s often room for negotiation, especially if you have a pre-approval in hand. If you’ve been pre-approved by an outside lender, you can use that offer as leverage to see if the dealership’s finance department can beat it. This creates competition and works in your favor.

Focus on the total loan amount and the overall cost of the loan, not just the monthly payment. Dealerships sometimes try to "stretch" the loan term to lower the monthly payment, which significantly increases the total interest you pay. Common mistakes to avoid include getting fixated on a low monthly payment without understanding the longer-term financial implications.

Additionally, be wary of unnecessary add-ons like extended warranties or excessive protection plans if you don’t truly need them. These can inflate your loan amount and, consequently, your interest payments. Scrutinize every line item on the final contract before signing.

Beyond the Loan: Rebuilding Credit Through Car Payments

A poor credit car loan isn’t just a means to get a car; it’s a powerful tool for credit rebuilding. This is where the real value lies, turning a challenging situation into a stepping stone for a brighter financial future.

The most critical step is making all your payments on time, every single month. Payment history is the largest factor in your credit score, accounting for 35% of your FICO score. Consistent, on-time payments will gradually, but surely, improve your credit score over the life of the loan.

As your credit score improves, you’ll gain access to better financial products, including lower interest rates on future loans (like mortgages or personal loans) and credit cards. This loan can be a testament to your renewed financial responsibility, opening doors that were previously closed. It demonstrates to future lenders that you can manage a significant debt successfully.

Alternatives to Traditional Poor Credit Car Loans

While our focus is on securing a poor credit car loan, it’s worth briefly mentioning alternatives if you find the terms too restrictive or simply prefer a different path.

- Saving Up to Buy Outright: If your need for a car isn’t immediate, saving up to buy a used car with cash eliminates the need for a loan and interest payments entirely.

- Public Transportation/Ridesharing: For those in urban areas, relying on public transport or ridesharing services can be a temporary solution while you save or improve your credit.

- Borrowing from Family/Friends: If this is an option, ensure you formalize the agreement with a written contract detailing repayment terms to avoid misunderstandings and protect relationships.

Driving Towards a Brighter Financial Future

Securing a car loan with poor credit is undeniably a journey with its share of challenges, but it’s far from an impossible feat. By understanding your credit, meticulously preparing your finances, strategically seeking out the right lenders, and negotiating wisely, you can transform this daunting process into a successful acquisition.

Remember, this car loan isn’t just about getting from point A to point B; it’s an opportunity. It’s your chance to demonstrate financial responsibility, rebuild your credit score, and lay the groundwork for a more stable financial future. Take the information and pro tips shared here, apply them diligently, and drive forward with confidence. The road to better credit starts now.