Navigating the Road Ahead: Your Ultimate Guide to Subprime Car Loans

Navigating the Road Ahead: Your Ultimate Guide to Subprime Car Loans Carloan.Guidemechanic.com

For many, a reliable vehicle isn’t a luxury; it’s a necessity for work, family, and daily life. But what happens when your credit score isn’t quite stellar? The traditional paths to auto financing might seem blocked, leaving you feeling stuck. This is where subprime car loans enter the picture, offering a potential lifeline for those with less-than-perfect credit.

However, these loans come with their own set of complexities and potential pitfalls. As an expert blogger and professional SEO content writer, my mission is to demystify subprime car loans, providing you with a comprehensive, in-depth guide that empowers you to make informed decisions. We’ll explore everything from what they are, how they work, their pros and cons, and crucial strategies for managing them effectively. Our ultimate goal is to equip you with the knowledge to navigate this financial landscape smartly, protecting your financial future while securing the transportation you need.

Navigating the Road Ahead: Your Ultimate Guide to Subprime Car Loans

What Exactly Are Subprime Car Loans?

A subprime car loan is a type of auto financing specifically designed for individuals who have a credit score that falls below what traditional lenders consider "prime." Generally, a credit score below 660-680 is often categorized as subprime, indicating a higher risk of default to lenders. This category can encompass a wide range of credit situations, from those with a few missed payments to individuals with bankruptcies or repossessions in their past.

Unlike prime loans, which are offered to borrowers with excellent credit at the lowest interest rates, subprime loans cater to a different demographic. They exist because lenders recognize that even people with credit challenges still need reliable transportation. These loans provide an opportunity for individuals to secure a vehicle when other financing options might be unavailable.

The core distinction lies in the perceived risk. Because borrowers with lower credit scores are statistically more likely to default on their loans, lenders offering subprime financing take on a greater risk. To offset this increased risk, they typically charge higher interest rates and may impose more stringent terms compared to prime loans. Understanding this fundamental difference is the first step toward approaching subprime auto financing with a clear perspective.

The Mechanics of Subprime Auto Financing

So, how do subprime car loans actually work? The process often mirrors traditional auto financing, but with some crucial differences tailored to the higher risk profile of the borrower. When you apply for a subprime car loan, lenders will still assess your income, debt-to-income ratio, and employment history, but they place a greater emphasis on your ability to make payments going forward, despite past credit issues.

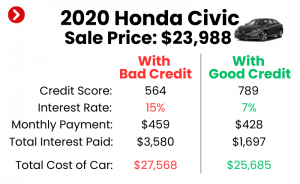

One of the most notable features of subprime loans is the interest rate. As mentioned, these rates are significantly higher than those for prime borrowers, sometimes reaching into double-digit percentages. This means you’ll pay substantially more for the car over the life of the loan. Additionally, subprime loans often come with longer repayment terms, sometimes stretching to 72 or even 84 months. While longer terms can result in lower monthly payments, they also mean you’re paying interest for a longer period, further increasing the total cost of the vehicle and potentially leading to a situation where you owe more than the car is worth (being "upside down" on your loan).

Lenders who offer subprime financing can vary. You might find them through a dealership’s finance department, which often partners with specialized subprime lenders. There are also independent finance companies that focus exclusively on bad credit auto loans. These lenders are adept at assessing risk and structuring loans that, while more expensive, are designed to give borrowers a chance to rebuild their credit. A down payment is also often required, and putting more money down can significantly improve your chances of approval and reduce your overall loan amount.

The Upsides: Why Subprime Loans Can Be a Lifeline

Despite the higher costs, subprime car loans aren’t without their benefits, especially for those in urgent need of transportation. For many, they represent the only viable path to vehicle ownership, providing crucial access to work, school, and essential services. This immediate need can often outweigh the financial drawbacks in the short term.

One of the most significant advantages, and often overlooked, is the opportunity to rebuild credit. Successfully managing a subprime car loan by making consistent, on-time payments can have a profoundly positive impact on your credit score. Each timely payment reported to credit bureaus demonstrates financial responsibility, gradually improving your credit profile over time. This can open doors to better financial products and lower interest rates in the future, effectively using the loan as a stepping stone.

Pro tips from us: View a subprime car loan not just as a means to get a car, but as a strategic tool for credit rehabilitation. Focus diligently on making every payment on time. This discipline can transform a challenging financial situation into a powerful credit-building experience. It’s about more than just the car; it’s about improving your financial trajectory.

Furthermore, subprime loans can offer a degree of flexibility that might not be available with prime lenders. Some specialized subprime lenders are more willing to work with unique financial situations, understanding that life can throw curveballs. They often look at your current income and stability more broadly than traditional banks might, offering a more personalized approach to approval.

Understanding the Downsides and Risks

While subprime car loans offer a solution for many, it’s crucial to approach them with a clear understanding of the significant downsides and risks involved. Ignoring these potential pitfalls can lead to further financial distress, making your situation worse rather than better.

The most prominent disadvantage is the high interest rate. Because you’re deemed a higher risk, lenders charge more to compensate. This means a car that might cost $20,000 with a prime loan could end up costing you $25,000, $30,000, or even more over the life of a subprime loan due to accumulated interest. A higher interest rate directly translates to a much larger total repayment amount, significantly increasing the financial burden.

Common mistakes to avoid are focusing solely on the monthly payment without considering the total cost of the loan. A low monthly payment might seem attractive, but it often comes at the expense of a much longer loan term and a much higher overall interest paid. Always calculate the total cost of the loan before signing any agreement.

Another major risk is the potential for repossession. If you miss payments, even a few, the lender has the right to repossess your vehicle. This not only leaves you without transportation but also severely damages your credit score, making it even harder to get future loans. Being "upside down" on your loan – owing more than the car is worth – is also a common issue with subprime loans due to rapid depreciation and long loan terms. This makes it difficult to sell the car or refinance without incurring a loss.

Based on my experience, many borrowers fall into a cycle of debt when they don’t fully grasp these implications. They get stuck with an expensive car loan, struggle to make payments, and their financial situation deteriorates further. Understanding these risks upfront allows you to prepare and potentially mitigate them.

Is a Subprime Car Loan Right for You? A Self-Assessment

Deciding whether a subprime car loan is the right path requires honest self-assessment and careful consideration of your financial situation. It’s not a one-size-fits-all solution, and what works for one person might be detrimental to another.

A subprime loan might be a viable option if you have an urgent, unavoidable need for a vehicle and have exhausted all other alternatives. For instance, if securing reliable transportation is essential for maintaining employment, and public transport is not an option, a subprime loan could be a temporary necessity. Crucially, you must also have a clear, realistic plan to improve your credit score and eventually refinance the loan or pay it off early. Your income should be stable and sufficient to comfortably cover the higher monthly payments, along with all other living expenses.

However, you should reconsider a subprime loan if your income is unstable or fluctuates significantly. Without a consistent ability to make payments, you’re at high risk of default and repossession. Similarly, if you haven’t taken the time to create a detailed budget and understand exactly how the loan payments will impact your overall finances, you might be setting yourself up for failure. Don’t rush into a decision out of desperation.

Pro tips from us: Before even looking at cars, sit down and create a comprehensive budget. Account for the loan payment, insurance (which can also be higher for subprime borrowers), fuel, and maintenance. If the numbers don’t add up comfortably, it’s a clear sign to explore other options or wait until your financial situation improves. A car should enhance your life, not become another source of stress.

How to Secure a Subprime Car Loan (and Do It Smartly)

If, after careful consideration, you decide a subprime car loan is your best option, there are smart steps you can take to improve your chances of approval and secure the most favorable terms possible. Approaching the process strategically can save you a significant amount of money and stress.

First, check your credit report thoroughly. This isn’t just about knowing your score, but understanding what’s on your report. Identify any errors and work to dispute them, as this can sometimes improve your score quickly. Knowing your credit history also helps you anticipate what lenders will see. Next, set a realistic budget for the total cost of the car, not just the monthly payment. Remember, a subprime loan comes with higher interest, so aim for a vehicle that is well within your means.

Saving for a significant down payment is perhaps one of the most impactful steps you can take. A larger down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid. It also signals to lenders that you are a serious and committed borrower, often leading to better loan offers.

Shop around for lenders. Don’t just accept the first offer you receive from a dealership. Apply with multiple lenders, including specialized subprime lenders and credit unions, if they offer such programs. Comparing offers can reveal significant differences in interest rates and terms. Based on my experience, getting pre-approved by a lender before you visit a dealership puts you in a much stronger negotiating position. You’ll know exactly what you can afford and what interest rate to expect.

Finally, understand all terms and conditions before you sign anything. Read the entire loan agreement carefully. Pay close attention to the interest rate, annual percentage rate (APR), loan term, any prepayment penalties, and late fees. Don’t hesitate to ask questions until you fully understand every aspect of the contract.

Strategies for Managing Your Subprime Loan Effectively

Once you’ve secured a subprime car loan, the journey isn’t over; in fact, this is where the real work begins. Effective management of your loan is paramount to avoiding financial pitfalls and leveraging it as a tool for credit improvement. Your primary goal should be to transform this subprime loan into a stepping stone for a brighter financial future.

The most critical strategy is to make payments on time, every time. This cannot be stressed enough. Late payments not only incur fees but also negatively impact your credit score, undermining the very reason many opt for a subprime loan. Set up automatic payments or calendar reminders to ensure you never miss a due date. Consistency is key to demonstrating financial responsibility.

Consider refinancing your loan as soon as your credit score improves. Once you’ve made 6-12 months of on-time payments and your credit score shows significant improvement, start exploring options to refinance your subprime loan into a prime loan with a lower interest rate. This can save you thousands of dollars over the life of the loan. For more detailed guidance on this, check out our article on Refinancing Your Car Loan: When and How to Save Money.

If your budget allows, pay more than the minimum monthly payment. Even an extra $20 or $50 a month can significantly reduce the principal balance, leading to less interest paid over time and helping you pay off the loan faster. This strategy can be particularly effective with high-interest subprime loans. Lastly, build an emergency fund. Life is unpredictable, and an emergency fund can be a financial cushion, ensuring you can still make your car payments even if an unexpected expense arises, preventing default.

Alternatives to Subprime Car Loans

While subprime car loans can be a solution, they shouldn’t always be your first resort. Exploring alternatives, especially if your need for a vehicle isn’t immediate, can save you money and protect your financial health in the long run.

One of the most straightforward alternatives is saving up for a used car. Even a modest down payment can help, but if you can save enough to buy an inexpensive, reliable used car outright, you avoid interest payments altogether. This allows you to drive debt-free while you work on improving your credit score for future, better financing options.

Consider public transportation or ride-sharing services if available in your area. For some, these options can be more cost-effective than car ownership, especially when factoring in insurance, fuel, maintenance, and loan payments. This might be a temporary solution until your financial standing improves.

Another viable option is to find a co-signer with excellent credit. A co-signer essentially guarantees the loan, making the lender more comfortable offering you a prime rate. However, this comes with a significant caveat: if you default, your co-signer is equally responsible for the debt. This arrangement should only be pursued with someone you trust implicitly and with a clear understanding of the risks for both parties.

Finally, explore secured personal loans if your credit situation allows. While less common for car purchases, some lenders might offer secured personal loans using other assets as collateral, potentially at a lower interest rate than a subprime auto loan. However, always exercise caution with secured loans, as you risk losing the collateral if you default.

Beyond the Loan: Rebuilding Your Credit for a Brighter Financial Future

Securing a subprime car loan can be a means to an end, but the ultimate goal should always be to improve your financial health and credit score. This loan can be a powerful tool for credit rebuilding if managed correctly, paving the way for better opportunities down the road.

Every on-time payment you make on your subprime car loan is a positive mark on your credit report. Lenders and credit bureaus see this consistent behavior as a strong indicator of your reliability and ability to manage debt. Over time, these positive entries will help offset negative marks from your past, steadily increasing your credit score. This is why consistent, timely payments are non-negotiable.

Beyond your car loan, there are other crucial credit-building strategies you should employ. Focus on paying down other outstanding debts, especially high-interest credit card balances. Keep your credit utilization low, ideally below 30% of your available credit. Avoid opening too many new credit accounts simultaneously, as this can signal risk to lenders. Regularly monitor your credit report for errors and dispute any inaccuracies.

Ultimately, this journey is about financial literacy and discipline. Understanding how credit works, budgeting effectively, and making responsible financial choices will serve you far beyond this particular car loan. It’s about empowering yourself to take control of your financial future, ensuring that the need for a subprime loan becomes a temporary chapter, not a recurring theme. For a comprehensive approach to improving your financial standing, read our guide on How to Improve Your Credit Score Fast: Actionable Steps.

Frequently Asked Questions About Subprime Auto Loans

Navigating subprime car loans often brings up a host of questions. Here are some of the most common inquiries, answered concisely to provide you with clarity.

-

What credit score is considered subprime?

Generally, a credit score below 660-680 is considered subprime, though the exact cutoff can vary slightly between lenders. Scores below 580 are often categorized as deep subprime. -

Can I get a subprime loan with no down payment?

While possible, it’s less common and typically results in higher interest rates and monthly payments. Lenders prefer a down payment as it reduces their risk and shows your commitment. A significant down payment often improves your chances of approval and can secure better terms. -

How long do subprime loans last?

Subprime car loan terms are often longer than prime loans, commonly ranging from 60 to 84 months, and sometimes even longer. This helps reduce monthly payments but significantly increases the total interest paid over time. -

Will a subprime loan hurt my credit?

No, if managed responsibly, a subprime loan can actually help your credit. Making consistent, on-time payments will build positive credit history. However, missing payments will severely damage your credit score. -

Can I get out of a subprime loan early?

Yes, you can typically pay off a subprime loan early. In fact, doing so can save you a substantial amount in interest. Check your loan agreement for any prepayment penalties, though these are less common with car loans than with some other types of financing. -

What is the average interest rate for subprime car loans?

Average interest rates for subprime car loans can vary widely based on your specific credit score, loan term, and lender, but they typically range from 10% to 25% or even higher. This is significantly higher than prime loan rates, which can be as low as 3-6%. -

Where can I find reputable subprime lenders?

You can often find subprime lenders through dealership finance departments that work with multiple banks, or through specialized online lenders and credit unions. It’s crucial to research and compare multiple offers. The Consumer Financial Protection Bureau (CFPB) offers resources on understanding auto loans and your rights as a consumer. Visit the CFPB website for more information on auto loans.

Conclusion: Driving Towards a Smarter Financial Future

Navigating the world of subprime car loans can feel daunting, but with the right knowledge and a strategic approach, it doesn’t have to be a dead end. We’ve explored what these loans are, how they function, and the critical balance between their benefits and their inherent risks. From understanding the higher interest rates to recognizing the opportunity for credit rebuilding, you are now equipped with a comprehensive understanding.

Remember, a subprime car loan should be viewed as a tool – a means to an end, not an end in itself. Your ultimate goal is to secure the transportation you need while simultaneously working to improve your financial health. By making timely payments, exploring refinancing options, and implementing broader credit-building strategies, you can transform a challenging financial situation into a powerful stepping stone. Approach subprime auto financing with caution, diligence, and a clear plan, and you’ll be well on your way to driving towards a brighter, more stable financial future.