Navigating the Road Ahead: Your Ultimate Guide to the Bad Credit Car Loan Calculator

Navigating the Road Ahead: Your Ultimate Guide to the Bad Credit Car Loan Calculator Carloan.Guidemechanic.com

Buying a car is more than just a purchase; it’s often a necessity, a gateway to opportunities, and a significant life event. But what if your credit score isn’t quite where you’d like it to be? The thought of securing an auto loan with bad credit can feel daunting, like navigating a dense fog without a compass. This is where a Bad Credit Car Loan Calculator becomes your most powerful tool, transforming uncertainty into clarity.

As an expert blogger and SEO content writer, I understand the challenges and anxieties that come with bad credit car financing. My mission today is to demystify the process, empower you with knowledge, and show you exactly how to leverage this invaluable calculator to make informed decisions. This comprehensive guide will not only explain the calculator but also provide actionable strategies to help you secure a car loan that fits your budget, even with a less-than-perfect credit history.

Navigating the Road Ahead: Your Ultimate Guide to the Bad Credit Car Loan Calculator

The Reality of Bad Credit Car Loans: Understanding the Landscape

Before we dive into the calculator itself, let’s establish a foundational understanding of what "bad credit" means in the context of car loans. Generally, a credit score below 600-620 is considered subprime or bad credit by most lenders. This doesn’t mean you can’t get a loan, but it does mean the terms will likely be less favorable than for someone with excellent credit.

Lenders view borrowers with bad credit as higher risk. This increased risk translates directly into higher interest rates. It’s their way of compensating for the perceived likelihood of default. Understanding this reality is the first step towards setting realistic expectations and effectively using a Bad Credit Car Loan Calculator to plan your purchase.

Based on my experience, many individuals are discouraged before they even begin because they assume bad credit means no car. This simply isn’t true. While the path might be different, a car loan is often still accessible. The key is preparation and understanding the numbers.

Unveiling the Power of the Bad Credit Car Loan Calculator

At its core, a Bad Credit Car Loan Calculator is a digital tool designed to help you estimate your potential monthly car loan payments. For those with bad credit, this tool is even more critical because it helps you factor in the often-higher interest rates you might face. It takes a few key pieces of information and, in return, provides a clear picture of your financial commitment.

This calculator isn’t just about crunching numbers; it’s about giving you control. It allows you to experiment with different scenarios, helping you understand the direct impact of each variable on your monthly budget and the total cost of the loan. This empowerment is invaluable when dealing with the complexities of subprime lending.

The Essential Inputs: What You Need to Know

To effectively use any car loan calculator, especially one tailored for bad credit, you’ll need to input specific data points. Each of these plays a significant role in determining your outcome.

- Loan Amount (or Car Price): This is the total amount of money you need to borrow after any down payment or trade-in value has been subtracted from the car’s purchase price.

- Interest Rate: This is arguably the most crucial input for bad credit borrowers. It’s the cost of borrowing money, expressed as a percentage. For bad credit, this rate will typically be higher.

- Loan Term: Also known as the repayment period, this is the length of time, usually in months, over which you will repay the loan. Common terms range from 36 to 84 months.

- Down Payment: This is the initial lump sum of money you pay upfront for the car. While optional for some, it’s highly recommended and often essential for bad credit borrowers.

The Critical Outputs: What the Calculator Reveals

Once you’ve plugged in your numbers, the Bad Credit Car Loan Calculator will generate vital information, helping you understand the true cost of your loan.

- Estimated Monthly Payment: This is the amount you’ll need to pay each month. This figure is paramount for budgeting.

- Total Interest Paid: This shows the cumulative amount of interest you will pay over the entire loan term. For bad credit loans, this number can be surprisingly high.

- Total Cost of Loan: This is the sum of the loan amount and the total interest paid, giving you the complete financial outlay for your vehicle.

Understanding these outputs is key to determining if a particular car and loan scenario is truly affordable for you.

Why You Absolutely Need a Bad Credit Car Loan Calculator

Many people jump into car shopping without fully understanding the financial implications. For individuals with bad credit, this oversight can be disastrous. A Bad Credit Car Loan Calculator is not a luxury; it’s a necessity.

1. Empowering Informed Decisions

Knowledge is power, especially in finance. By using the calculator, you move from guessing to knowing. You can see, in black and white, what different interest rates or loan terms will do to your monthly budget. This transparency helps you make decisions based on facts, not assumptions.

2. Realistic Budgeting and Affordability Assessment

Perhaps the most significant benefit is the ability to assess true affordability. It’s easy to fall in love with a car, but the calculator forces you to confront the numbers. Can you really afford that $400 monthly payment? What if the interest rate is 18% instead of 12%? The calculator provides those answers instantly.

Pro tips from us: Always factor in other car-related expenses like insurance, fuel, and maintenance into your overall budget, not just the loan payment. The calculator handles the loan, but you’re responsible for the rest.

3. Strengthening Your Negotiation Position

Walking into a dealership armed with an estimated monthly payment based on realistic interest rates for your credit score gives you a massive advantage. You know what you can afford and what terms are reasonable. This prevents you from being swayed by aggressive sales tactics and helps you negotiate from a position of strength.

Common mistakes to avoid are going into a dealership without any idea of what you can afford. This leaves you vulnerable to accepting less favorable terms than you might otherwise qualify for.

4. Avoiding Predatory Lending Practices

Unfortunately, the subprime lending market can sometimes attract less reputable lenders. By understanding your potential payments and total costs beforehand, you’re better equipped to spot a predatory loan offer that might have unusually high fees or an exorbitant interest rate designed to trap you.

5. Strategic Financial Planning

Beyond just the car, using the calculator contributes to your broader financial planning. It helps you understand the long-term impact of debt, especially high-interest debt. It allows you to strategize on how much down payment you might need or how short you can realistically make your loan term to minimize interest paid.

Based on my experience, those who utilize these tools proactively are far more likely to achieve financial stability and avoid buyer’s remorse.

Navigating the Inputs: A Deep Dive into Each Variable

Now, let’s break down each input of the Bad Credit Car Loan Calculator with specific considerations for those with bad credit.

Car Price vs. Loan Amount: What Can You Really Afford?

When you have bad credit, securing a loan for a brand-new, expensive vehicle is often unrealistic. Focus on the actual loan amount you need. This is calculated as: Car Purchase Price – Down Payment – Trade-in Value (if any).

- Determining a Realistic Car Price: Start by researching reliable used cars that fit your essential needs, not just your wants. Look at market values for these vehicles. A lower car price directly translates to a lower loan amount, which is always beneficial for bad credit borrowers as it reduces risk for the lender.

- The Role of Trade-ins: If you have an existing vehicle, its trade-in value can act like a down payment, reducing the amount you need to borrow. Ensure you get an independent appraisal of your trade-in’s value before heading to a dealership.

Interest Rates for Bad Credit: Setting Realistic Expectations

This is often the most challenging aspect for bad credit borrowers. Your interest rate is heavily influenced by your credit score, but other factors also play a role.

- Factors Influencing Rates:

- Credit Score: The lower your score, the higher the rate.

- Debt-to-Income (DTI) Ratio: Lenders look at how much of your gross monthly income goes towards debt payments. A high DTI can signal higher risk.

- Loan Term: Shorter terms often come with slightly lower rates because the lender’s money is at risk for less time.

- Down Payment: A larger down payment can signal less risk, potentially leading to a slightly better rate.

- Lender Type: Different lenders (banks, credit unions, subprime lenders, Buy Here Pay Here lots) offer varying rates.

- Realistic Expectations: For bad credit (e.g., scores below 600), interest rates can range anywhere from 10% to 25% or even higher, depending on the specifics of your situation and the current market. Use the calculator to see the impact of these higher rates.

- How to Find Competitive Rates: Don’t just accept the first offer. Get pre-approved by multiple lenders. Credit unions often have more favorable rates for their members, even those with bad credit. Online lenders specializing in subprime loans can also be a good option.

- Pro Tip: Get pre-approved to compare rates without impacting your credit score significantly. Most pre-approvals use a "soft pull" on your credit. Only when you formally apply will a "hard pull" occur.

- Internal Link Idea: For a deeper dive into how interest rates are determined and what factors influence them, read our comprehensive guide on .

Loan Term: The Double-Edged Sword

The loan term is the length of time you have to repay the loan. While a longer term means lower monthly payments, it also means you pay significantly more in total interest.

- Shorter vs. Longer Terms:

- Shorter Term (e.g., 36-48 months): Higher monthly payments, but you pay much less in total interest. You own the car outright faster. This is generally preferred if you can afford the payments.

- Longer Term (e.g., 60-84 months): Lower monthly payments, making the car seem more affordable. However, you pay substantially more in total interest over the life of the loan, and you risk being "upside down" (owing more than the car is worth) for a longer period.

- Common Mistake to Avoid: Stretching the loan out too long just to get a lower monthly payment. While it might seem manageable now, the extra interest paid can be astronomical, and you might find yourself with a car that’s worth far less than you owe on it. Use the Bad Credit Car Loan Calculator to compare a 60-month term versus a 72-month or 84-month term; the difference in total interest paid will be eye-opening.

The Power of a Down Payment: Your Best Ally

A down payment is an upfront payment you make towards the car’s purchase price. For bad credit borrowers, a substantial down payment is incredibly beneficial.

- Why It’s Critical with Bad Credit:

- Reduces Loan Amount: Less money borrowed means less interest paid overall.

- Shows Commitment: A significant down payment signals to lenders that you are serious about the purchase and have some financial stability, making you a less risky borrower.

- Lowers Interest Burden: With a smaller loan principal, even a high interest rate will result in less total interest paid.

- Helps Avoid Being Upside Down: A larger down payment creates immediate equity in the vehicle, reducing the risk of owing more than the car is worth.

- How Much is Enough? While any down payment helps, aiming for 10-20% of the car’s purchase price is ideal. Even $500 or $1,000 can make a difference. Every dollar you put down is a dollar you don’t borrow and don’t pay interest on.

Beyond the Calculator: Strategies for Securing a Bad Credit Car Loan

The calculator is your planning tool, but you’ll need a solid strategy to turn those plans into reality.

1. Improving Your Credit Score (Even a Little Helps!)

Even a slight improvement in your credit score can significantly impact the interest rate you’re offered. Focus on:

- Paying all bills on time.

- Reducing existing credit card balances.

- Disputing any errors on your credit report.

Internal Link Idea: For detailed steps on how to quickly boost your credit score, check out our guide on .

2. Saving for a Larger Down Payment

Prioritize saving money. The more you can put down, the better your loan terms will likely be, and the lower your monthly payments will be. Every extra dollar saved means less borrowed.

3. Finding a Co-signer (Pros and Cons)

A co-signer with good credit can significantly improve your chances of approval and help you secure a lower interest rate.

- Pros: Better rates, higher chance of approval.

- Cons: The co-signer is equally responsible for the loan. If you miss payments, their credit will be affected, and they could be sued. This can strain relationships. Only consider this with someone you trust implicitly and who fully understands the risks.

4. Considering a Less Expensive Vehicle

Resist the urge to buy more car than you need or can afford. A reliable, affordable used car is a much wiser choice when you have bad credit. It reduces the loan amount, monthly payments, and total interest.

5. Shopping Around for Lenders

Don’t settle for the first loan offer. Seek quotes from:

- Credit Unions: Often more forgiving and offer better rates than traditional banks for members.

- Online Lenders: Many specialize in bad credit auto loans.

- Dealership Finance Departments: While convenient, compare their offers with those you’ve secured independently.

- Subprime Lenders: These specialize in lending to individuals with bad credit, but be extra vigilant about terms and rates.

6. Understanding Your Debt-to-Income (DTI) Ratio

Lenders look at your DTI ratio – the percentage of your gross monthly income that goes towards debt payments. A lower DTI (ideally below 40-45%) makes you a more attractive borrower. Try to reduce other debts before applying for a car loan if your DTI is high.

7. Getting Pre-Approved

As mentioned, pre-approval is a game-changer. It gives you a concrete loan offer (or at least an estimate) before you even step foot on a dealership lot. This allows you to shop for a car with confidence, knowing exactly what you can afford and at what rate.

Common Pitfalls and How to Avoid Them

Even with the best intentions, it’s easy to stumble when navigating bad credit car loans.

- Falling for "Guaranteed Approval" Scams: Be wary of any lender promising "guaranteed approval" regardless of your credit score. These often come with extremely high interest rates, hidden fees, or unfavorable terms. Always read the fine print.

- Not Understanding the Full Cost of the Loan: Focus on the total cost of the loan (principal + interest), not just the monthly payment. A low monthly payment might hide a much longer term and significantly more interest paid over time.

- Ignoring the Fine Print: Always read your loan agreement carefully. Understand the interest rate (APR), any fees, prepayment penalties, and late payment clauses. Don’t be afraid to ask questions.

- Buying More Car Than You Can Afford: This is the most common mistake. Just because a lender approves you for a certain amount doesn’t mean you should borrow that much. Stick to your budget, which you’ve meticulously planned using your Bad Credit Car Loan Calculator.

- Not Factoring in Insurance and Maintenance: Beyond the loan payment, cars come with ongoing costs. Insurance premiums can be higher for newer cars or for drivers with a history of bad credit. Don’t forget fuel and routine maintenance. Neglecting these can lead to financial strain.

Based on years of advising individuals, I’ve seen how quickly excitement can turn into regret if these common mistakes aren’t avoided. Preparation is your best defense.

Real-World Application: A Step-by-Step Guide to Using the Calculator

Let’s put theory into practice. Here’s how you’d use a Bad Credit Car Loan Calculator:

- Gather Your Financial Information: Know your approximate credit score, your monthly income, and your current monthly debt obligations.

- Estimate a Car Price: Based on your needs and budget, research a realistic car price range. Let’s say you’re looking at a reliable used car for $15,000.

- Input Your Potential Down Payment: Decide how much you can comfortably put down. Let’s say you’ve saved $2,000.

- Loan Amount will then be $15,000 – $2,000 = $13,000.

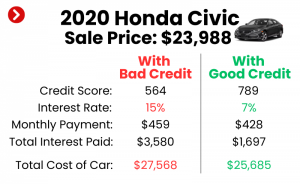

- Research Realistic Interest Rates for Your Credit Tier: Based on your credit score (e.g., in the 550-600 range), you might estimate an interest rate between 15% and 20%. Let’s start with 18%.

- Experiment with Different Loan Terms:

- Scenario A: 60-month term: Plug in $13,000 (loan amount), 18% (interest rate), 60 months (term).

- Result: Monthly payment of X, Total Interest Paid of Y, Total Cost of Loan of Z.

- Scenario B: 72-month term: Plug in $13,000 (loan amount), 18% (interest rate), 72 months (term).

- Result: Monthly payment of A, Total Interest Paid of B, Total Cost of Loan of C.

- Scenario A: 60-month term: Plug in $13,000 (loan amount), 18% (interest rate), 60 months (term).

- Analyze the Results: Compare the monthly payments and, critically, the total interest paid across scenarios. Notice how a longer term lowers the monthly payment but significantly increases the total interest.

- Adjust and Refine:

- If the monthly payment is too high, can you increase your down payment?

- Can you find a slightly cheaper car?

- Can you improve your credit score even a few points to potentially get a slightly lower rate?

- What if you aim for a 60-month term but make slightly larger payments when you can, to pay it off faster?

This iterative process, powered by the calculator, allows you to find the sweet spot between affordability and minimizing interest.

The Path to Financial Recovery: How a Car Loan Can Help (or Hurt)

Securing a car loan with bad credit isn’t just about getting a vehicle; it can also be a strategic step towards financial recovery.

- Positive Impact: If you consistently make your car loan payments on time, every single month, it will be reported to credit bureaus. This demonstrates responsible financial behavior and can significantly improve your credit score over time. A car loan is often one of the first major installment loans people with bad credit can use to rebuild their credit history.

- Negative Impact: Conversely, if you miss payments or default on the loan, it will severely damage your credit score further. This makes it even harder to secure future loans or other forms of credit. The vehicle could also be repossessed.

The importance of responsible borrowing cannot be overstated. Use the Bad Credit Car Loan Calculator to ensure your payments are truly manageable, giving you the best chance to make on-time payments and use this loan as a stepping stone to better credit.

External Link: For more detailed advice on managing debt and improving your financial health, consider visiting the Consumer Financial Protection Bureau (CFPB) website at consumerfinance.gov.

Conclusion: Drive Towards a Brighter Financial Future

Acquiring a car with bad credit can feel like an uphill battle, but it doesn’t have to be. The Bad Credit Car Loan Calculator is an indispensable tool that empowers you with clarity, helps you budget effectively, and strengthens your negotiating position. It allows you to explore different scenarios, understand the true cost of borrowing, and make financially sound decisions.

Remember, a less-than-perfect credit score isn’t a life sentence. With careful planning, strategic saving, and the intelligent use of tools like the car loan calculator, you can secure the transportation you need and even use this opportunity to rebuild your credit for a brighter financial future. Don’t let bad credit deter you; instead, use this guide and the calculator to chart your course to success. Start planning today, and drive towards your goals with confidence!